Download as pdf or txt

You might also like

- Rules Governing Redeemable and Treasury SharesDocument2 pagesRules Governing Redeemable and Treasury SharesmarjNo ratings yet

- Mas.m-1404. Financial Statements AnalysisDocument22 pagesMas.m-1404. Financial Statements AnalysisCharry Ramos25% (4)

- Indonesia Morning CuppaDocument7 pagesIndonesia Morning CuppaNonera AnggreniNo ratings yet

- Indonesia Morning CuppaDocument8 pagesIndonesia Morning CuppaRicky ChandraNo ratings yet

- IND Morning Cuppa 15 Sep 2021Document9 pagesIND Morning Cuppa 15 Sep 2021alvin maulana.pNo ratings yet

- Report Ind Morning 11 Nov 2021 EditedDocument9 pagesReport Ind Morning 11 Nov 2021 EditedPT SKSNo ratings yet

- Report Ind Morning 11 Nov 2021Document9 pagesReport Ind Morning 11 Nov 2021PT SKSNo ratings yet

- Report Ind Morning 11 Nov 2021 EditedDocument9 pagesReport Ind Morning 11 Nov 2021 EditedPT SKSNo ratings yet

- Indonesia Morning CuppaDocument8 pagesIndonesia Morning Cuppaalvin maulana.pNo ratings yet

- Indonesia Morning CuppaDocument8 pagesIndonesia Morning CuppaPT SKSNo ratings yet

- Indonesia Morning CuppaDocument9 pagesIndonesia Morning Cuppaalvin maulana.pNo ratings yet

- Sudan Africa RE SPDocument4 pagesSudan Africa RE SPsamia saidNo ratings yet

- Indonesia Morning CuppaDocument9 pagesIndonesia Morning CuppaSteven OtnielNo ratings yet

- Relative ValuationDocument1 pageRelative Valuationjuan.farrelNo ratings yet

- 202003261100349638864web Final Industry Consumption Report February 2020 PDFDocument17 pages202003261100349638864web Final Industry Consumption Report February 2020 PDFpraful s.gNo ratings yet

- (2019-03-11) Gustavo Lopetegui - IAPG Houston - Energy in Argentina Investment Opportunities For The International Community - Pub PDFDocument14 pages(2019-03-11) Gustavo Lopetegui - IAPG Houston - Energy in Argentina Investment Opportunities For The International Community - Pub PDFIgnacio LabaquiNo ratings yet

- Statistik Energi IRENADocument4 pagesStatistik Energi IRENAadm.sierbatamNo ratings yet

- LPG Consumption Report-032023-WebVersionDocument15 pagesLPG Consumption Report-032023-WebVersionAmrit IyerNo ratings yet

- Andorra Europe RE SPDocument4 pagesAndorra Europe RE SPBrian ChangNo ratings yet

- Afghanistan Asia RE SPDocument4 pagesAfghanistan Asia RE SPjunkthingsandspamandstuffNo ratings yet

- Fiji Oceania RE SPDocument4 pagesFiji Oceania RE SPDaniel MosqueraNo ratings yet

- Covid-19 - Impact On RetailDocument9 pagesCovid-19 - Impact On RetailK61 ĐỖ QUỲNH NGUYÊNNo ratings yet

- Light-Duty Vehicle Efficiency Standards: FactsheetDocument2 pagesLight-Duty Vehicle Efficiency Standards: FactsheetYohannes AlemuNo ratings yet

- IRENA 2022 - Philippines - Asia - RE - SPDocument4 pagesIRENA 2022 - Philippines - Asia - RE - SPysblnclNo ratings yet

- Jamaica - Central America and The Caribbean - RE - SPDocument4 pagesJamaica - Central America and The Caribbean - RE - SPnfitzpatrick743No ratings yet

- Morocco Africa RE SPDocument4 pagesMorocco Africa RE SPMaro GueniariNo ratings yet

- Tuvalu Oceania RE SPDocument4 pagesTuvalu Oceania RE SPonalogNo ratings yet

- Financial Results For The Three Months Ended June 30, 2019: July 29, 2019 1Document8 pagesFinancial Results For The Three Months Ended June 30, 2019: July 29, 2019 1Giancarlo Di VonaNo ratings yet

- F23 - OEE DashboardDocument10 pagesF23 - OEE DashboardAnand RNo ratings yet

- Cote Divoire - Africa - RE - SPDocument4 pagesCote Divoire - Africa - RE - SPowusuansahphilip17No ratings yet

- Michelin - PPT FY 2023 ResultsDocument66 pagesMichelin - PPT FY 2023 ResultsANUBHAV NARWALNo ratings yet

- FD BeaterDocument5 pagesFD BeaterMove OnNo ratings yet

- Zimbabwe Africa RE SPDocument4 pagesZimbabwe Africa RE SPwashington munatsiNo ratings yet

- Covid 19 - Impact On RetailDocument9 pagesCovid 19 - Impact On Retailsimluong.31221023375No ratings yet

- Covid-19 - Impact On RetailDocument9 pagesCovid-19 - Impact On RetailPhạm Phương ThảoNo ratings yet

- Cameroon Africa RE SPDocument4 pagesCameroon Africa RE SPLise LaureNo ratings yet

- LiquiLoans - Prime Retail Fixed Income Investment Opportunity - Oct. 2022Document25 pagesLiquiLoans - Prime Retail Fixed Income Investment Opportunity - Oct. 2022Vivek SinghalNo ratings yet

- Pra-Raker Kemendag 2021: Akselerasi Pemulihan Ekonomi Nasional Melalui Peningkatan Peran PerwadagDocument38 pagesPra-Raker Kemendag 2021: Akselerasi Pemulihan Ekonomi Nasional Melalui Peningkatan Peran PerwadagDedy Lampe PRayaNo ratings yet

- Malaysian House Price Index (MHPI)Document2 pagesMalaysian House Price Index (MHPI)Afiq KhidhirNo ratings yet

- Deficit: BUDGET DEFICIT (Excluding Grants) / GDP RATIO IN 2002 AND 2003Document10 pagesDeficit: BUDGET DEFICIT (Excluding Grants) / GDP RATIO IN 2002 AND 2003Mayank GargNo ratings yet

- Indonesia Automotive 2023 Full Year ReportDocument45 pagesIndonesia Automotive 2023 Full Year Reportandriyas1234No ratings yet

- GPCA Facts and Figures - 2021Document61 pagesGPCA Facts and Figures - 2021Rania YaseenNo ratings yet

- 19 4Q - Earning Release of LGEDocument19 pages19 4Q - Earning Release of LGEОverlord 4No ratings yet

- Indonesia Morning CuppaDocument9 pagesIndonesia Morning CuppaOzanNo ratings yet

- Construction Indus OuputDocument1 pageConstruction Indus OuputPraveen Varma VNo ratings yet

- Spanish Food Retail Market Recent TrendsDocument20 pagesSpanish Food Retail Market Recent Trends1220inboxNo ratings yet

- Earnings Yield EYDocument23 pagesEarnings Yield EYwutthicsaNo ratings yet

- Basic Statistics 2020Document6 pagesBasic Statistics 2020Harshil JainNo ratings yet

- LOreal RIF2021 C BABULE ENDocument20 pagesLOreal RIF2021 C BABULE ENJay ZNo ratings yet

- Proximus Consensus Ahead of q1 2023Document4 pagesProximus Consensus Ahead of q1 2023Laurent MillerNo ratings yet

- Qatar Quarterly Equity HandbookDocument60 pagesQatar Quarterly Equity Handbook123bingoNo ratings yet

- Tube Molding Report - Sept 2010.Document3 pagesTube Molding Report - Sept 2010.Ogero Otekki MusaNo ratings yet

- Retail Industry Retail Industry Retail IndustryDocument8 pagesRetail Industry Retail Industry Retail IndustryTanmay PokaleNo ratings yet

- Apollo Hospitals Enterprise Limited NSEI APOLLOHOSP FinancialsDocument40 pagesApollo Hospitals Enterprise Limited NSEI APOLLOHOSP Financialsakumar4uNo ratings yet

- 2020 Deloitte India Workforce and Increment Trends Survey - Participant Report PDFDocument82 pages2020 Deloitte India Workforce and Increment Trends Survey - Participant Report PDFAbhishek GuptaNo ratings yet

- Viet Nam - Asia - RE - SPDocument4 pagesViet Nam - Asia - RE - SPPhan Tuấn AnhNo ratings yet

- Emerson Capital Quarterly Performance - 3Q 2009Document1 pageEmerson Capital Quarterly Performance - 3Q 2009Joseph HarrisonNo ratings yet

- Panel 1Document26 pagesPanel 1Dewa TidurNo ratings yet

- Iraq - Middle East - RE - SPDocument4 pagesIraq - Middle East - RE - SPNadeen Al-janabiNo ratings yet

- Presentacion Mayo 19Document7 pagesPresentacion Mayo 19Miguel Angel JaramilloNo ratings yet

- Assignment 1Document2 pagesAssignment 1anwarNo ratings yet

- Middle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsFrom EverandMiddle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsNo ratings yet

- Crayons Advertising Limited - RHPDocument277 pagesCrayons Advertising Limited - RHPRuchir AggarwalNo ratings yet

- Polimex RekomendacjaDocument4 pagesPolimex Rekomendacjap_barankiewiczNo ratings yet

- Dokumen - Pub Security Analysis and Portfolio Management 2eDocument1,054 pagesDokumen - Pub Security Analysis and Portfolio Management 2eTop Five ProductsNo ratings yet

- Chapter 2 - Investment AlternativesDocument15 pagesChapter 2 - Investment AlternativesWaseem Liaquat Khan80% (5)

- Final JMF Annual Report 12-13 - WebDocument134 pagesFinal JMF Annual Report 12-13 - WebRichard JonesNo ratings yet

- INSTRUMENTSDocument41 pagesINSTRUMENTS微微No ratings yet

- Chapter - 3Document38 pagesChapter - 3martha clarNo ratings yet

- Handbook of Income Tax (HIT) by Farid Mohmmad NasirDocument43 pagesHandbook of Income Tax (HIT) by Farid Mohmmad NasirPiyal HossainNo ratings yet

- RFBT (2 of 2) Preweek B94 - QuestionnaireDocument16 pagesRFBT (2 of 2) Preweek B94 - QuestionnaireSilver LilyNo ratings yet

- Futures Dec 2013Document53 pagesFutures Dec 2013anudoraNo ratings yet

- Final DissertationDocument34 pagesFinal DissertationKeran VarmaNo ratings yet

- Test Bank For Principles of Managerial Finance 14th Edition Lawrence J Gitman Chad J Zutter DownloadDocument62 pagesTest Bank For Principles of Managerial Finance 14th Edition Lawrence J Gitman Chad J Zutter Downloadjessicashawcwynztimjf100% (24)

- DEBENTURES and WarrantsDocument7 pagesDEBENTURES and Warrantspurehearts100% (1)

- REG AB Static Pool & Structural Diagrams of Flow of FundsDocument22 pagesREG AB Static Pool & Structural Diagrams of Flow of FundsCarrieonicNo ratings yet

- ACCV GEFE Nov 2022Document7 pagesACCV GEFE Nov 2022Le Van ChauNo ratings yet

- Celex 32022R1288 en TXT PDFDocument72 pagesCelex 32022R1288 en TXT PDFMicheleNo ratings yet

- Vetiva Research - FY'10 Earnings Season - Are Banks Still In-The-MoneyDocument4 pagesVetiva Research - FY'10 Earnings Season - Are Banks Still In-The-MoneyRasaq Muhammed AbiolaNo ratings yet

- Riti Project ReportDocument37 pagesRiti Project ReportMadhukar Singh roll no 26No ratings yet

- 1-SECP - Saboohi IsrarDocument15 pages1-SECP - Saboohi Israranum naeemNo ratings yet

- Sacmdd PDFDocument379 pagesSacmdd PDFYash ModiNo ratings yet

- The Banking Law Reviewer Hot JuristDocument28 pagesThe Banking Law Reviewer Hot Juristgrego centillas100% (3)

- AOA of HN CitiPagesDocument57 pagesAOA of HN CitiPagesNibras Abdullah KarimNo ratings yet

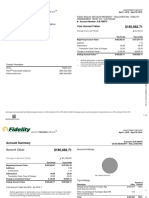

- Your Account Value:: Fidelity Rollover Ira David Moriarty - Rollover Ira - Fidelity Management Trust Co - CustodianDocument6 pagesYour Account Value:: Fidelity Rollover Ira David Moriarty - Rollover Ira - Fidelity Management Trust Co - CustodianMarcus GreenNo ratings yet

- Securities Law Main Book (Edition 6) PDFDocument238 pagesSecurities Law Main Book (Edition 6) PDFmadhav agarwal100% (1)

- Cir V Phil American Accident InsuranceDocument13 pagesCir V Phil American Accident InsuranceXianyue04No ratings yet

- Philippines Foreign Investment Negative ListDocument2 pagesPhilippines Foreign Investment Negative ListAnjanette MangalindanNo ratings yet

- Corporate Income TaxDocument14 pagesCorporate Income Tax36. Lê Minh Phương 12A3No ratings yet

- Maybank - Aviation Report On CaamDocument7 pagesMaybank - Aviation Report On CaamNinerMike MysNo ratings yet