Download as docx, pdf, or txt

You might also like

- Statement of Purpose SampleDocument39 pagesStatement of Purpose SampleHưng Dương Công76% (51)

- Criminal Complaint Us 494 RW Sec. 34 of The Indian Penal code-Drafting-Criminal Template-1096Document3 pagesCriminal Complaint Us 494 RW Sec. 34 of The Indian Penal code-Drafting-Criminal Template-1096jonshon kripakaran100% (3)

- Financial Accounting and Reporting - Problems ReviewDocument5 pagesFinancial Accounting and Reporting - Problems ReviewARIS100% (1)

- Accounting English IIDocument14 pagesAccounting English IIJaprax LailyasNo ratings yet

- FAR - Estimating Inventory - StudentDocument3 pagesFAR - Estimating Inventory - StudentPamelaNo ratings yet

- FAR Estimating Inventory StudentDocument3 pagesFAR Estimating Inventory StudentMary Aquino0% (1)

- Kieso 15e SGV1 Ch09Document30 pagesKieso 15e SGV1 Ch09anilegna99No ratings yet

- CH 09Document32 pagesCH 09errahahahaNo ratings yet

- Unit 2: Inventories: Special Valuation Methods 2.0 Aims and ObjectivesDocument17 pagesUnit 2: Inventories: Special Valuation Methods 2.0 Aims and ObjectivesNesru SirajNo ratings yet

- ch08 SMDocument17 pagesch08 SMAhmadYaseenNo ratings yet

- Act CH 9 QuizDocument5 pagesAct CH 9 QuizLamia AkterNo ratings yet

- Unit 2Document31 pagesUnit 2Nigussie BerhanuNo ratings yet

- Act CH 9 QuizDocument4 pagesAct CH 9 QuizLamia AkterNo ratings yet

- Asset - Inventory - For Posting PDFDocument8 pagesAsset - Inventory - For Posting PDFNhicoleChoiNo ratings yet

- Reporting and Interpreting Cost of Goods Sold and Inventory: Answers To QuestionsDocument61 pagesReporting and Interpreting Cost of Goods Sold and Inventory: Answers To Questionschanyoung4951No ratings yet

- Chapter 28 - Gross Profit and Retail Method: ANSWER 28-1Document12 pagesChapter 28 - Gross Profit and Retail Method: ANSWER 28-1Cyrus IsanaNo ratings yet

- Unit 2Document30 pagesUnit 2yebegashet100% (1)

- Libby 4ce Solutions Manual - Ch08Document66 pagesLibby 4ce Solutions Manual - Ch087595522No ratings yet

- Inventories - Inventory Estimation MethodsDocument17 pagesInventories - Inventory Estimation MethodsmarkNo ratings yet

- Week 08 - 02 - Module 19 - Accounting For InventoriesDocument17 pagesWeek 08 - 02 - Module 19 - Accounting For Inventories지마리No ratings yet

- FARC Lesson 4 IAS 2 - InventoriesDocument15 pagesFARC Lesson 4 IAS 2 - InventoriesSlicebearNo ratings yet

- Inventory Important NotesDocument11 pagesInventory Important NotesRommel VinluanNo ratings yet

- Cost & Management AccountingDocument9 pagesCost & Management AccountingshubhmNo ratings yet

- AS2 - Accounting StandardsDocument2 pagesAS2 - Accounting Standardsabhishekbehal5012No ratings yet

- Financial Accounting 7Th Edition Libby Solutions Manual Full Chapter PDFDocument67 pagesFinancial Accounting 7Th Edition Libby Solutions Manual Full Chapter PDFMichaelMurrayewrsd100% (14)

- Chapter 18 Standard Costing Incorporating Standards Into The Accounting RecordDocument1 pageChapter 18 Standard Costing Incorporating Standards Into The Accounting RecordZunaira ButtNo ratings yet

- Cost Accounting Questions and Their AnswersDocument5 pagesCost Accounting Questions and Their Answerszulqarnainhaider450_No ratings yet

- Inventorty PDFDocument2 pagesInventorty PDFJoelo De VeraNo ratings yet

- Ch#15 MARGINAL COSTINGDocument12 pagesCh#15 MARGINAL COSTINGeaglerealestate31No ratings yet

- Resume Psak 14: Inventories: Conversion CostDocument9 pagesResume Psak 14: Inventories: Conversion Costcindy azarine dimitriNo ratings yet

- ch09 PDFDocument40 pagesch09 PDFerylpaez100% (2)

- Marginal Costing With Decision MakingDocument38 pagesMarginal Costing With Decision MakingHaresh Sahitya0% (1)

- Costing and Profit PlanningDocument27 pagesCosting and Profit PlanningSIDDHANT CHUGHNo ratings yet

- NIC 2 (2021) - 2023 V CICLO en-USDocument6 pagesNIC 2 (2021) - 2023 V CICLO en-USMj264No ratings yet

- Resume 4Document5 pagesResume 4MariaNo ratings yet

- Pas 2Document8 pagesPas 2Miya LaideNo ratings yet

- Inventories: Indian Accounting Standard (Ind AS) 2Document11 pagesInventories: Indian Accounting Standard (Ind AS) 2aman2645No ratings yet

- Nepal Accounting Standards On InventoriesDocument8 pagesNepal Accounting Standards On InventoriesGemini_0804No ratings yet

- Cost & Management Accounting 1Document3 pagesCost & Management Accounting 1Engr Sonia LohanaNo ratings yet

- Friedlan4e SM Ch07Document55 pagesFriedlan4e SM Ch07NischalaGunisettiNo ratings yet

- Chapter 6 Costing by Products and Joint ProductsDocument2 pagesChapter 6 Costing by Products and Joint ProductsfahadNo ratings yet

- Sta. Ana AsynchTaskNov16Document2 pagesSta. Ana AsynchTaskNov16John Christopher Sta AnaNo ratings yet

- Allocation Forcosts of JointProducts ByproductsDocument4 pagesAllocation Forcosts of JointProducts ByproductsMd. Ridoy HossainNo ratings yet

- Pas 2 InventoriesDocument5 pagesPas 2 InventoriesAndrea LopezNo ratings yet

- Inventory Ind As 2Document32 pagesInventory Ind As 2Shailesh SatarkarNo ratings yet

- ML Actual CostingDocument3 pagesML Actual CostingViswanath RudraradhyaNo ratings yet

- This Study Resource Was: Lecture NotesDocument3 pagesThis Study Resource Was: Lecture NotesWymple Kate Alexis FaisanNo ratings yet

- Financial Accounting 8Th Edition Libby Solutions Manual Full Chapter PDFDocument77 pagesFinancial Accounting 8Th Edition Libby Solutions Manual Full Chapter PDFDawnZimmermanxwcq100% (12)

- Marginal Costing 300 Level-1Document23 pagesMarginal Costing 300 Level-1simon danielNo ratings yet

- Financial Accounting Practice and Review InventoryDocument3 pagesFinancial Accounting Practice and Review Inventoryukandi rukmanaNo ratings yet

- Inventories Wit Ans Key (Pria)Document22 pagesInventories Wit Ans Key (Pria)Samantha Marie Arevalo100% (2)

- Inflation Accounting: BY, Nadeem Zehera Prathiksha Pooja J Raheela Banu Ramya JDocument36 pagesInflation Accounting: BY, Nadeem Zehera Prathiksha Pooja J Raheela Banu Ramya JLikitha T AppajiNo ratings yet

- US Internal Revenue Service: rp-03-51Document5 pagesUS Internal Revenue Service: rp-03-51IRSNo ratings yet

- 1 Inventories and ShortDocument6 pages1 Inventories and ShortHussein FokeerNo ratings yet

- IA 1 Quiz 3 InventoriesDocument11 pagesIA 1 Quiz 3 InventoriesJo HarahNo ratings yet

- Unit 12 Marginal Costing and CVP AnalysisDocument24 pagesUnit 12 Marginal Costing and CVP AnalysisGaurang LakshaneNo ratings yet

- Absorption CostingDocument23 pagesAbsorption Costingarman_277276271No ratings yet

- Marginal Costing: Definition: (CIMA London)Document4 pagesMarginal Costing: Definition: (CIMA London)Pankaj2cNo ratings yet

- Inventories - Lower of Cost and NRVDocument12 pagesInventories - Lower of Cost and NRVmarkNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

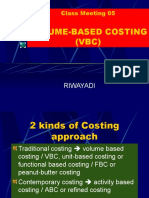

- 05 & 06 VBCDocument62 pages05 & 06 VBCSyafri iNo ratings yet

- Statistics For Management and Economics-: Sixth EditionDocument42 pagesStatistics For Management and Economics-: Sixth EditionSyafri iNo ratings yet

- Examples of Probability ProblemsDocument8 pagesExamples of Probability ProblemsSyafri iNo ratings yet

- Sales BudegetingDocument9 pagesSales BudegetingSyafri iNo ratings yet

- This Scenario Applies To Questions 1 and 2: A Study Was Done To Compare The LungDocument6 pagesThis Scenario Applies To Questions 1 and 2: A Study Was Done To Compare The LungSyafri iNo ratings yet

- Describing Data:: Frequency Tables, Frequency Distributions, and Graphic PresentationDocument21 pagesDescribing Data:: Frequency Tables, Frequency Distributions, and Graphic PresentationSyafri iNo ratings yet

- Soal Income Tax Article 23Document1 pageSoal Income Tax Article 23Syafri iNo ratings yet

- ELECTRICAL MACHINES-II-ELECTRICAL-5th-2021-22Document2 pagesELECTRICAL MACHINES-II-ELECTRICAL-5th-2021-22sameer mohantyNo ratings yet

- Lecture 20Document29 pagesLecture 20Axel Coronado PopperNo ratings yet

- Astm A-285Document2 pagesAstm A-285LoriGalbanusNo ratings yet

- Virtual Reality and Artificial Intelligence in Motion SimulatorsDocument18 pagesVirtual Reality and Artificial Intelligence in Motion SimulatorsSyed RazviNo ratings yet

- Level 1: 20 Part 1 - Listening ComprehensionDocument3 pagesLevel 1: 20 Part 1 - Listening ComprehensionVictor DiazNo ratings yet

- Indian Coal AnalysisDocument3 pagesIndian Coal AnalysisK.S.MAYILVAGHANAN100% (1)

- Dovewell Oilfield Services LTDDocument28 pagesDovewell Oilfield Services LTDlibyashuaaNo ratings yet

- 12.8 Reading+listeningDocument15 pages12.8 Reading+listeningPhạm Minh Trí VõNo ratings yet

- UPRM Ingenieria Mecanica Curriculo #1Document2 pagesUPRM Ingenieria Mecanica Curriculo #1Yosef DeleonNo ratings yet

- Listening Test: Directions: For Each Question in This Part, You Will Hear Four Statements About A Picture in YourDocument40 pagesListening Test: Directions: For Each Question in This Part, You Will Hear Four Statements About A Picture in YourTrương Hữu LộcNo ratings yet

- Alves Doa - Way Intl 102723Document5 pagesAlves Doa - Way Intl 102723michaelgracias700No ratings yet

- TLS and DTLS (Notes Materials) : Mr. S P Maniraj Dr. S Suresh Mr. M PrabuDocument14 pagesTLS and DTLS (Notes Materials) : Mr. S P Maniraj Dr. S Suresh Mr. M PrabuSuresh SNo ratings yet

- Aditya Solanki Expriment No.2Document5 pagesAditya Solanki Expriment No.2Kertik SinghNo ratings yet

- Megaman PatternDocument9 pagesMegaman PatternBelen Solis Maravillas100% (2)

- Lesson Plan - CultureDocument3 pagesLesson Plan - CultureSharan HansNo ratings yet

- Instruction Manual: MissionDocument93 pagesInstruction Manual: Missionamjad atayaNo ratings yet

- What Made The Tata Nano A Failure: A Winter Project OnDocument90 pagesWhat Made The Tata Nano A Failure: A Winter Project Onyash ranaNo ratings yet

- Flexible Budgets and Performance AnalysisDocument37 pagesFlexible Budgets and Performance AnalysisSana IjazNo ratings yet

- L410 Flight ManualDocument722 pagesL410 Flight ManualTim Lin100% (1)

- Born To WinDocument23 pagesBorn To WinSuvra PattanaikNo ratings yet

- PATANJALIDocument16 pagesPATANJALIAbhishek PandeyNo ratings yet

- MEDICAL DEVICES: Guidance DocumentDocument15 pagesMEDICAL DEVICES: Guidance DocumentPhạm Thu HuyềnNo ratings yet

- Failure Modes and Effect AnalysisDocument17 pagesFailure Modes and Effect AnalysisWahid KdrtNo ratings yet

- Ttlga 1250Document2 pagesTtlga 1250anerak0412No ratings yet

- Conquest of Manila: Asynchronous Activities Before Session 1Document4 pagesConquest of Manila: Asynchronous Activities Before Session 1Marbie Ann SimbahanNo ratings yet

- Handheld Air Particle Counter MET ONE HHPC+ Series BrochureDocument4 pagesHandheld Air Particle Counter MET ONE HHPC+ Series BrochureFirdaus ZaidNo ratings yet

- Thread & FastenerDocument35 pagesThread & Fastenermani317No ratings yet

- Dede Aditya Saputra - Chapter IiDocument16 pagesDede Aditya Saputra - Chapter IiSS English AcademyNo ratings yet