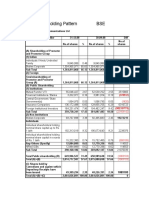

APL Apollo Antique Stock Broking Coverage Aprl 17

APL Apollo Antique Stock Broking Coverage Aprl 17

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Discover EasytronicDocument77 pagesDiscover EasytronicMohamed Mohamed100% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Rain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImproveDocument8 pagesRain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImprovedidwaniasNo ratings yet

- Rbi Allowed Banks To Increase Limit From 10 To 15 PercentDocument10 pagesRbi Allowed Banks To Increase Limit From 10 To 15 PercentdidwaniasNo ratings yet

- IDEA One PagerDocument6 pagesIDEA One PagerdidwaniasNo ratings yet

- Industry Report Card April 2018Document16 pagesIndustry Report Card April 2018didwaniasNo ratings yet

- Information Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsDocument8 pagesInformation Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsdidwaniasNo ratings yet

- MARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodayDocument2 pagesMARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodaydidwaniasNo ratings yet

- Shareholding Pattern BSEDocument3 pagesShareholding Pattern BSEdidwaniasNo ratings yet

- 'A' Grade Turnaround: Associated Cement CompaniesDocument3 pages'A' Grade Turnaround: Associated Cement CompaniesdidwaniasNo ratings yet

- BHEL One PagerDocument1 pageBHEL One PagerdidwaniasNo ratings yet

- The Subprime Meltdown: Understanding Accounting-Related AllegationsDocument7 pagesThe Subprime Meltdown: Understanding Accounting-Related AllegationsdidwaniasNo ratings yet

- CKP PresentationDocument39 pagesCKP PresentationdidwaniasNo ratings yet

- Nurturing A Distinct Corporate Identity,: DifferentlyDocument10 pagesNurturing A Distinct Corporate Identity,: DifferentlydidwaniasNo ratings yet

- Ready Reckoner, November 2015Document92 pagesReady Reckoner, November 2015didwaniasNo ratings yet

- IndiaEconomicsOverheating090207 MF PDFDocument4 pagesIndiaEconomicsOverheating090207 MF PDFdidwaniasNo ratings yet

- Competitors' Product Knowledge and Marketing in Changing ScenarioDocument62 pagesCompetitors' Product Knowledge and Marketing in Changing ScenariodidwaniasNo ratings yet

- Strategy, Knowledge and Success: Presented byDocument55 pagesStrategy, Knowledge and Success: Presented bydidwaniasNo ratings yet

- Perancangan Sistem Informasi Geografis Perlengkapan Jalan Berbasis Daerah Rawan KecelakaanDocument9 pagesPerancangan Sistem Informasi Geografis Perlengkapan Jalan Berbasis Daerah Rawan KecelakaanAlya ArhamNo ratings yet

- NCHRP RPT 539Document101 pagesNCHRP RPT 539danniitoshNo ratings yet

- Fabrication Erection and Installation Procedure For PipingDocument35 pagesFabrication Erection and Installation Procedure For Pipingmohd as shahiddin jafri100% (1)

- Kodiak Marine: Supercharged 6.2L LSADocument48 pagesKodiak Marine: Supercharged 6.2L LSAmecanica gomesNo ratings yet

- WP05 AI.4 ICAO - Review New ANP PDFDocument265 pagesWP05 AI.4 ICAO - Review New ANP PDFMaverickNo ratings yet

- Design 7 PujDocument11 pagesDesign 7 PujJerika ToraldeNo ratings yet

- Summary For Ielts-1-70Document70 pagesSummary For Ielts-1-70Doan BùiNo ratings yet

- Uber and The Sharing Economy - Global Market Expansion and Reception Sample AnalysisDocument7 pagesUber and The Sharing Economy - Global Market Expansion and Reception Sample AnalysisRitika SharmaNo ratings yet

- A20 High Strength Low Alloy SteelsDocument7 pagesA20 High Strength Low Alloy SteelsMarcoAntonioNo ratings yet

- Dom Bobr Wagon PDFDocument42 pagesDom Bobr Wagon PDFShantanu DuttaNo ratings yet

- L-7 Electrical Survey Requirements U7Document10 pagesL-7 Electrical Survey Requirements U7MaryNo ratings yet

- Full Service Carrier Product Rating Criteria: What Are The Different Classes of Service On A Plane?Document5 pagesFull Service Carrier Product Rating Criteria: What Are The Different Classes of Service On A Plane?Vyl CebrerosNo ratings yet

- Models of Daily Life in Ancient EgyptDocument214 pagesModels of Daily Life in Ancient EgyptNona ANo ratings yet

- Germanischer Lloyd - Over 24m Rig DesignDocument16 pagesGermanischer Lloyd - Over 24m Rig DesignhelciomarceloNo ratings yet

- Mi8161 Ux Special en GB Id 62288Document56 pagesMi8161 Ux Special en GB Id 62288Sergio Alejandro Gonzales ArancibiaNo ratings yet

- W Wiir Riin NG GD Diia AG GR RA AM M: - English - 7/2017Document704 pagesW Wiir Riin NG GD Diia AG GR RA AM M: - English - 7/2017PavelNo ratings yet

- Assignment 2 EOT 1032Document5 pagesAssignment 2 EOT 1032Rajbir SinghNo ratings yet

- New Holland Series TM Tractors Models TM120, TM130, TM140, TM155, TM175 and TM190Document24 pagesNew Holland Series TM Tractors Models TM120, TM130, TM140, TM155, TM175 and TM190احمد الشبراوى100% (2)

- TicketDocument2 pagesTicketjohnwick6151No ratings yet

- Reading Skills: Present Perfect: Julio Antonio Rodríguez LaraDocument2 pagesReading Skills: Present Perfect: Julio Antonio Rodríguez LaraGhaisani NabihatiNo ratings yet

- Filter Kit - All ModelsDocument26 pagesFilter Kit - All Modelsnrit999_stdNo ratings yet

- DaewooDocument32 pagesDaewooyaqoob008No ratings yet

- Road PatternsDocument3 pagesRoad PatternsMubasheer KNo ratings yet

- Volkswagen Service Training Engine Management SystemsDocument10 pagesVolkswagen Service Training Engine Management Systemsrichard100% (57)

- SL 1063Document3 pagesSL 1063Yarisa VangeNo ratings yet

- Bicycle Tyre Cost Calculation: New 222+ 510 Tyre Compound Ingredients Price/Kg 80 KG Batch Batch PriceDocument4 pagesBicycle Tyre Cost Calculation: New 222+ 510 Tyre Compound Ingredients Price/Kg 80 KG Batch Batch PriceBKDNo ratings yet

- Age of Steam Ships: Stories and History of All 50 Vessels Which Sail in TransatlanticDocument13 pagesAge of Steam Ships: Stories and History of All 50 Vessels Which Sail in TransatlanticGianfrancoNo ratings yet

- North 24 ParganasDocument4 pagesNorth 24 ParganasShraddha ChowdhuryNo ratings yet

- Bastos Silva Santos Nesto PDFDocument14 pagesBastos Silva Santos Nesto PDFStipo LuksicNo ratings yet

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Discover EasytronicDocument77 pagesDiscover EasytronicMohamed Mohamed100% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Rain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImproveDocument8 pagesRain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImprovedidwaniasNo ratings yet

- Rbi Allowed Banks To Increase Limit From 10 To 15 PercentDocument10 pagesRbi Allowed Banks To Increase Limit From 10 To 15 PercentdidwaniasNo ratings yet

- IDEA One PagerDocument6 pagesIDEA One PagerdidwaniasNo ratings yet

- Industry Report Card April 2018Document16 pagesIndustry Report Card April 2018didwaniasNo ratings yet

- Information Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsDocument8 pagesInformation Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsdidwaniasNo ratings yet

- MARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodayDocument2 pagesMARKET ESTIMATES FOR Sep, 2008 Results To Be Announced TodaydidwaniasNo ratings yet

- Shareholding Pattern BSEDocument3 pagesShareholding Pattern BSEdidwaniasNo ratings yet

- 'A' Grade Turnaround: Associated Cement CompaniesDocument3 pages'A' Grade Turnaround: Associated Cement CompaniesdidwaniasNo ratings yet

- BHEL One PagerDocument1 pageBHEL One PagerdidwaniasNo ratings yet

- The Subprime Meltdown: Understanding Accounting-Related AllegationsDocument7 pagesThe Subprime Meltdown: Understanding Accounting-Related AllegationsdidwaniasNo ratings yet

- CKP PresentationDocument39 pagesCKP PresentationdidwaniasNo ratings yet

- Nurturing A Distinct Corporate Identity,: DifferentlyDocument10 pagesNurturing A Distinct Corporate Identity,: DifferentlydidwaniasNo ratings yet

- Ready Reckoner, November 2015Document92 pagesReady Reckoner, November 2015didwaniasNo ratings yet

- IndiaEconomicsOverheating090207 MF PDFDocument4 pagesIndiaEconomicsOverheating090207 MF PDFdidwaniasNo ratings yet

- Competitors' Product Knowledge and Marketing in Changing ScenarioDocument62 pagesCompetitors' Product Knowledge and Marketing in Changing ScenariodidwaniasNo ratings yet

- Strategy, Knowledge and Success: Presented byDocument55 pagesStrategy, Knowledge and Success: Presented bydidwaniasNo ratings yet

- Perancangan Sistem Informasi Geografis Perlengkapan Jalan Berbasis Daerah Rawan KecelakaanDocument9 pagesPerancangan Sistem Informasi Geografis Perlengkapan Jalan Berbasis Daerah Rawan KecelakaanAlya ArhamNo ratings yet

- NCHRP RPT 539Document101 pagesNCHRP RPT 539danniitoshNo ratings yet

- Fabrication Erection and Installation Procedure For PipingDocument35 pagesFabrication Erection and Installation Procedure For Pipingmohd as shahiddin jafri100% (1)

- Kodiak Marine: Supercharged 6.2L LSADocument48 pagesKodiak Marine: Supercharged 6.2L LSAmecanica gomesNo ratings yet

- WP05 AI.4 ICAO - Review New ANP PDFDocument265 pagesWP05 AI.4 ICAO - Review New ANP PDFMaverickNo ratings yet

- Design 7 PujDocument11 pagesDesign 7 PujJerika ToraldeNo ratings yet

- Summary For Ielts-1-70Document70 pagesSummary For Ielts-1-70Doan BùiNo ratings yet

- Uber and The Sharing Economy - Global Market Expansion and Reception Sample AnalysisDocument7 pagesUber and The Sharing Economy - Global Market Expansion and Reception Sample AnalysisRitika SharmaNo ratings yet

- A20 High Strength Low Alloy SteelsDocument7 pagesA20 High Strength Low Alloy SteelsMarcoAntonioNo ratings yet

- Dom Bobr Wagon PDFDocument42 pagesDom Bobr Wagon PDFShantanu DuttaNo ratings yet

- L-7 Electrical Survey Requirements U7Document10 pagesL-7 Electrical Survey Requirements U7MaryNo ratings yet

- Full Service Carrier Product Rating Criteria: What Are The Different Classes of Service On A Plane?Document5 pagesFull Service Carrier Product Rating Criteria: What Are The Different Classes of Service On A Plane?Vyl CebrerosNo ratings yet

- Models of Daily Life in Ancient EgyptDocument214 pagesModels of Daily Life in Ancient EgyptNona ANo ratings yet

- Germanischer Lloyd - Over 24m Rig DesignDocument16 pagesGermanischer Lloyd - Over 24m Rig DesignhelciomarceloNo ratings yet

- Mi8161 Ux Special en GB Id 62288Document56 pagesMi8161 Ux Special en GB Id 62288Sergio Alejandro Gonzales ArancibiaNo ratings yet

- W Wiir Riin NG GD Diia AG GR RA AM M: - English - 7/2017Document704 pagesW Wiir Riin NG GD Diia AG GR RA AM M: - English - 7/2017PavelNo ratings yet

- Assignment 2 EOT 1032Document5 pagesAssignment 2 EOT 1032Rajbir SinghNo ratings yet

- New Holland Series TM Tractors Models TM120, TM130, TM140, TM155, TM175 and TM190Document24 pagesNew Holland Series TM Tractors Models TM120, TM130, TM140, TM155, TM175 and TM190احمد الشبراوى100% (2)

- TicketDocument2 pagesTicketjohnwick6151No ratings yet

- Reading Skills: Present Perfect: Julio Antonio Rodríguez LaraDocument2 pagesReading Skills: Present Perfect: Julio Antonio Rodríguez LaraGhaisani NabihatiNo ratings yet

- Filter Kit - All ModelsDocument26 pagesFilter Kit - All Modelsnrit999_stdNo ratings yet

- DaewooDocument32 pagesDaewooyaqoob008No ratings yet

- Road PatternsDocument3 pagesRoad PatternsMubasheer KNo ratings yet

- Volkswagen Service Training Engine Management SystemsDocument10 pagesVolkswagen Service Training Engine Management Systemsrichard100% (57)

- SL 1063Document3 pagesSL 1063Yarisa VangeNo ratings yet

- Bicycle Tyre Cost Calculation: New 222+ 510 Tyre Compound Ingredients Price/Kg 80 KG Batch Batch PriceDocument4 pagesBicycle Tyre Cost Calculation: New 222+ 510 Tyre Compound Ingredients Price/Kg 80 KG Batch Batch PriceBKDNo ratings yet

- Age of Steam Ships: Stories and History of All 50 Vessels Which Sail in TransatlanticDocument13 pagesAge of Steam Ships: Stories and History of All 50 Vessels Which Sail in TransatlanticGianfrancoNo ratings yet

- North 24 ParganasDocument4 pagesNorth 24 ParganasShraddha ChowdhuryNo ratings yet

- Bastos Silva Santos Nesto PDFDocument14 pagesBastos Silva Santos Nesto PDFStipo LuksicNo ratings yet