Download as docx, pdf, or txt

You might also like

- Revised Proposal For Final Project FIn619Document7 pagesRevised Proposal For Final Project FIn619AbdulRehman100% (5)

- Biz Orgs Attack OutlineDocument5 pagesBiz Orgs Attack OutlineSam Hughes100% (2)

- Chapter 11Document10 pagesChapter 11HusainiBachtiarNo ratings yet

- Emerging Trend in Corporate GovernanceDocument13 pagesEmerging Trend in Corporate Governancedeepak60% (5)

- Dividend Policy Q and ADocument3 pagesDividend Policy Q and AMd. HabibullahNo ratings yet

- Quizzer RETAINED EARNINGSDocument5 pagesQuizzer RETAINED EARNINGSPrincess Frean VillegasNo ratings yet

- Baring Bank CaseDocument16 pagesBaring Bank CaseArjun GunasekaranNo ratings yet

- Corporate Governance Failure at SatyamDocument4 pagesCorporate Governance Failure at SatyamPoojaa ShirsatNo ratings yet

- Unstoppable FraudDocument12 pagesUnstoppable FraudMc Tiey Mohd NoorNo ratings yet

- Corporate Governance in SatyamDocument6 pagesCorporate Governance in Satyamnishan_patel_3No ratings yet

- Key Facts, Key Figures, Key Data, Key InformationDocument4 pagesKey Facts, Key Figures, Key Data, Key InformationPrateek TaoriNo ratings yet

- Audit and AssuranceDocument8 pagesAudit and AssuranceJoe AndrewNo ratings yet

- Fraudulent Financial Reporting Practices: Case Study of Satyam Computer LimitedDocument13 pagesFraudulent Financial Reporting Practices: Case Study of Satyam Computer LimitedmetopeNo ratings yet

- Fraud DetectionDocument24 pagesFraud DetectionGauravPrakashNo ratings yet

- Group 7B Satyam MandelaDocument17 pagesGroup 7B Satyam MandelaPrateek TaoriNo ratings yet

- Intro To Forensic Final Project CompilationDocument15 pagesIntro To Forensic Final Project Compilationapi-282483815No ratings yet

- Capitalism in A Post Enron WorldDocument10 pagesCapitalism in A Post Enron WorldSony Soha100% (1)

- The Role of The Non-Executive DirectorDocument20 pagesThe Role of The Non-Executive DirectordigitalbooksNo ratings yet

- India'S Satyam Scandal: Evidence The Too Large To Indict Mindset of Accounting Regulators Is A Global PhenomenonDocument10 pagesIndia'S Satyam Scandal: Evidence The Too Large To Indict Mindset of Accounting Regulators Is A Global PhenomenonvinayNo ratings yet

- Individual Assignment BM055-3.5-2 Ethics and Corporate GovernanceDocument17 pagesIndividual Assignment BM055-3.5-2 Ethics and Corporate GovernanceChin Kai WenNo ratings yet

- Satyam ScamDocument7 pagesSatyam ScamJeevan YadavNo ratings yet

- Triton Energy LTDDocument3 pagesTriton Energy LTDoctaeviaNo ratings yet

- Corporate Accounting Fraud: A Case Study of Satyam Computers LimitedDocument14 pagesCorporate Accounting Fraud: A Case Study of Satyam Computers LimitedVidushi Puri0% (1)

- Vanishing CompaniesDocument7 pagesVanishing CompaniesVinay Artwani100% (1)

- Exam Form: Assignment Exam Time: 3 DaysDocument16 pagesExam Form: Assignment Exam Time: 3 DaysTrang DươngNo ratings yet

- Fraudulent Reporting Practices: The Inside Story of India's EnronDocument15 pagesFraudulent Reporting Practices: The Inside Story of India's EnronManish ShahNo ratings yet

- Corporate GovernanceDocument10 pagesCorporate GovernanceBhuwan GulatiNo ratings yet

- FASA Case Analysis Group 5Document3 pagesFASA Case Analysis Group 5sohilbankar7No ratings yet

- Governance Failure at SatyamDocument19 pagesGovernance Failure at SatyamAnil KardamNo ratings yet

- Article 20062023 V1Document2 pagesArticle 20062023 V1haresh swaminathanNo ratings yet

- Coperate Governance EXECUTIVE SUMMARY (Case 6)Document5 pagesCoperate Governance EXECUTIVE SUMMARY (Case 6)HumaRiazNo ratings yet

- Corporate Accounting FraudDocument17 pagesCorporate Accounting Fraudanimes prustyNo ratings yet

- Ethics in AccountsDocument7 pagesEthics in AccountsArun Kumar NairNo ratings yet

- Unstoppable Fraud, Scandals and Manipulation - An Urgent Call For An Islamic-Based Code of EthicsDocument6 pagesUnstoppable Fraud, Scandals and Manipulation - An Urgent Call For An Islamic-Based Code of EthicsAK FleurNo ratings yet

- Presentation Description: Financial Statement Fraud & Corporate Governancethe Satyam CaseDocument5 pagesPresentation Description: Financial Statement Fraud & Corporate Governancethe Satyam CaseRandolph LangstiehNo ratings yet

- Corporate Governance and The Role of Forensic Accountants in Saudi ArabiaDocument8 pagesCorporate Governance and The Role of Forensic Accountants in Saudi ArabiaTJPRC PublicationsNo ratings yet

- Audit and SocietyDocument3 pagesAudit and SocietymayhemclubNo ratings yet

- Why Is Forensic Accounting Required?Document6 pagesWhy Is Forensic Accounting Required?Neha Singh0% (1)

- SSRN Id2277512Document34 pagesSSRN Id2277512Takhleeq AkhterNo ratings yet

- Case study on evidence of corporate fraud: 1、 Company profileDocument5 pagesCase study on evidence of corporate fraud: 1、 Company profileMely DennisNo ratings yet

- WatchdogDocument4 pagesWatchdogRuskanulMaarifNo ratings yet

- Financial Statement Fraud Control Audit Testing and Internal Auditing Expectation GapDocument7 pagesFinancial Statement Fraud Control Audit Testing and Internal Auditing Expectation GapRia MeilanNo ratings yet

- Fraud Financial ReoportingDocument35 pagesFraud Financial Reoportinganubha srivastavaNo ratings yet

- HO Time We Set The Standard For Corporate GovernanceDocument3 pagesHO Time We Set The Standard For Corporate GovernanceAlair JuniorNo ratings yet

- Case 1.5 Lincoln Savings and Loan AssociationDocument17 pagesCase 1.5 Lincoln Savings and Loan AssociationAlexa RodriguezNo ratings yet

- Adrian Cadbury Report: The Origin of The ReportDocument16 pagesAdrian Cadbury Report: The Origin of The Reportप्रदीप बागलNo ratings yet

- Business Case Study Presentation-1Document11 pagesBusiness Case Study Presentation-1Deepak RajoriyaNo ratings yet

- Accounts Draft 1Document7 pagesAccounts Draft 1NORZADIAN DOMAINNo ratings yet

- Nyaradzai Maorera M142278 Abigail Mudhungwaza M152107Document5 pagesNyaradzai Maorera M142278 Abigail Mudhungwaza M152107Nyaradzai MaoreraNo ratings yet

- Group Project Far 661Document19 pagesGroup Project Far 661azri2701No ratings yet

- Bhasin SatyamDemiseCaseStudy IJMSSR May2016Document20 pagesBhasin SatyamDemiseCaseStudy IJMSSR May2016Sultana ChowdhuryNo ratings yet

- Forensic Accounting ArticleDocument8 pagesForensic Accounting ArticleAzizul AviNo ratings yet

- IJCRT1813221Document5 pagesIJCRT1813221ishaisha1940No ratings yet

- Statutory Auditors' IndependenceDocument51 pagesStatutory Auditors' IndependenceIshidNo ratings yet

- The Infamous Tyco Scam of 2002Document2 pagesThe Infamous Tyco Scam of 2002sharlenemarieduranNo ratings yet

- Group-05 - AIS 2306 - ADocument5 pagesGroup-05 - AIS 2306 - AMahir RahmanNo ratings yet

- To Fiddle or Not To FiddleDocument7 pagesTo Fiddle or Not To FiddleUmmu Atiqah Zainulabid100% (1)

- Germic I 1Document52 pagesGermic I 1Raejayne IllesesNo ratings yet

- B.E May 2010Document2 pagesB.E May 2010ashisingh89No ratings yet

- Management Ethics - TransmileDocument12 pagesManagement Ethics - TransmileUmar othman100% (1)

- Advances and Issues in Fraud Research (A Commentary) - 2018 - 18pDocument18 pagesAdvances and Issues in Fraud Research (A Commentary) - 2018 - 18pKhaled Al-SanabaniNo ratings yet

- 1 Student of MBA& Assistant Professor Shoolini University, Himachal Pradesh, IndiaDocument11 pages1 Student of MBA& Assistant Professor Shoolini University, Himachal Pradesh, IndiaRakib HasanNo ratings yet

- ZERO TO MASTERY IN CORPORATE GOVERNANCE: Become Zero To Hero In Corporate Governance, This Book Covers A-Z Corporate Governance Concepts, 2022 Latest EditionFrom EverandZERO TO MASTERY IN CORPORATE GOVERNANCE: Become Zero To Hero In Corporate Governance, This Book Covers A-Z Corporate Governance Concepts, 2022 Latest EditionNo ratings yet

- The What, The Why, The How: Mergers and AcquisitionsFrom EverandThe What, The Why, The How: Mergers and AcquisitionsRating: 2 out of 5 stars2/5 (1)

- Eshfaque Alam DastagirDocument3 pagesEshfaque Alam DastagirEshfaque Alam DastagirNo ratings yet

- ManagementAccounting (TermPaper)Document11 pagesManagementAccounting (TermPaper)Eshfaque Alam Dastagir100% (1)

- Agrani Bank ICB BCBL BASIC Bank Eastern Bank: Bank Year Bailout Loan GrowthDocument14 pagesAgrani Bank ICB BCBL BASIC Bank Eastern Bank: Bank Year Bailout Loan GrowthEshfaque Alam DastagirNo ratings yet

- EIA (Assignment 02)Document7 pagesEIA (Assignment 02)Eshfaque Alam DastagirNo ratings yet

- Merger ConsolidationDocument8 pagesMerger ConsolidationRena Mae Lava MuycoNo ratings yet

- CHAPTER 9 - Earnings Management SummaryDocument3 pagesCHAPTER 9 - Earnings Management SummaryVanadisa SamuelNo ratings yet

- Examiners' Report 2013: LA3021 Company Law - Zone ADocument13 pagesExaminers' Report 2013: LA3021 Company Law - Zone AamashaNo ratings yet

- Unit 9 SharesDocument39 pagesUnit 9 Shareskonica chhotwaniNo ratings yet

- Legal Forms of Organizations Methods of Departmentalization: Sole ProprietorshipDocument2 pagesLegal Forms of Organizations Methods of Departmentalization: Sole ProprietorshipNaomi Aira Gole CruzNo ratings yet

- Heirs of GamboaDocument2 pagesHeirs of GamboaRaymart SalamidaNo ratings yet

- LT Roleplay - ScriptDocument3 pagesLT Roleplay - ScriptAMAL J MATHEW 2127007No ratings yet

- Annual Compliance Calendar - Companies Act, 2013: Applicability Private Company (Other Than Small Company)Document4 pagesAnnual Compliance Calendar - Companies Act, 2013: Applicability Private Company (Other Than Small Company)Gangour IndiaNo ratings yet

- Board Resolution - StockholdersDocument3 pagesBoard Resolution - StockholdersAiza Madum100% (2)

- Company Law Question BankDocument180 pagesCompany Law Question BankDebashish SharmaNo ratings yet

- Auditing Problems: RequiredDocument2 pagesAuditing Problems: RequiredvhhhNo ratings yet

- Intermediate (IPC) Course Paper 3B Financial Management Chapter 4 Unit 2Document62 pagesIntermediate (IPC) Course Paper 3B Financial Management Chapter 4 Unit 2saiNo ratings yet

- India Pesticides LimitedDocument318 pagesIndia Pesticides LimitedArvind SarafNo ratings yet

- Lecture 2 Statement of Changes in Equity Multiple ChoiceDocument5 pagesLecture 2 Statement of Changes in Equity Multiple ChoiceJeane Mae Boo100% (1)

- FORM PAS 4 - Draft Format - CommonDocument12 pagesFORM PAS 4 - Draft Format - Commonlegal shuruNo ratings yet

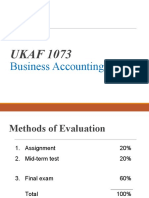

- UKAF 1073: Business Accounting IIDocument61 pagesUKAF 1073: Business Accounting IIalibabaNo ratings yet

- The Valuation Coundrum in The United Tech - Pytheon Merger)Document4 pagesThe Valuation Coundrum in The United Tech - Pytheon Merger)Tayba AwanNo ratings yet

- Issue of Right Share and Bonus ShareDocument15 pagesIssue of Right Share and Bonus ShareRahulNo ratings yet

- 2022 - Chapter01 - Why Value ValueValueDocument13 pages2022 - Chapter01 - Why Value ValueValueElias MacherNo ratings yet

- Lecture 7 Forms of Business OwnershipDocument19 pagesLecture 7 Forms of Business OwnershipSAMUEL ACHEAMPONGNo ratings yet

- Topic 1: Financial Manager (3 Fundamental Questions)Document8 pagesTopic 1: Financial Manager (3 Fundamental Questions)KHAkadsbdhsg100% (1)

- Code of Corporate Governance: The Board'S Governance ResponsibilitiesDocument12 pagesCode of Corporate Governance: The Board'S Governance ResponsibilitiesMartha TanNo ratings yet

- Atlas Battery Annual-Report 2015Document132 pagesAtlas Battery Annual-Report 2015adeelngNo ratings yet

- Mercantile LawDocument7 pagesMercantile LawAliNo ratings yet

- Com Rev NotesDocument30 pagesCom Rev NotesOmie Jehan Hadji-AzisNo ratings yet

- BSP MORB - Sec. 122 (Limits of Stockholdings in A Single Bank) (With Appendix 4) PDFDocument9 pagesBSP MORB - Sec. 122 (Limits of Stockholdings in A Single Bank) (With Appendix 4) PDFVictor GalangNo ratings yet