Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5835)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Circle Society Monumental Scam Telegram GroupDocument749 pagesCircle Society Monumental Scam Telegram GroupGigi KentNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Project Case OR1 Sem2 - 2021Document21 pagesProject Case OR1 Sem2 - 2021Ha NguyenNo ratings yet

- Accounting Fundamentals Module 1Document25 pagesAccounting Fundamentals Module 1Ramneek SinghNo ratings yet

- Emotions and Moral CourageDocument4 pagesEmotions and Moral CourageXiaoyu KensameNo ratings yet

- KANTIAN-ETHICSDocument3 pagesKANTIAN-ETHICSXiaoyu KensameNo ratings yet

- Fringe Benefits and Withholding TaxDocument7 pagesFringe Benefits and Withholding TaxXiaoyu KensameNo ratings yet

- Table 1: Demographic Profile: Variables NDocument5 pagesTable 1: Demographic Profile: Variables NXiaoyu KensameNo ratings yet

- ETHICSDocument1 pageETHICSXiaoyu KensameNo ratings yet

- Summary of Final Tax Under The Nirc, As Amended Individual Citizen AlienDocument16 pagesSummary of Final Tax Under The Nirc, As Amended Individual Citizen AlienXiaoyu KensameNo ratings yet

- Mode of Payment Person Liable Who FileDocument12 pagesMode of Payment Person Liable Who FileXiaoyu KensameNo ratings yet

- Regression Correlation ActivityDocument2 pagesRegression Correlation ActivityXiaoyu KensameNo ratings yet

- Estates and TrustsDocument4 pagesEstates and TrustsXiaoyu KensameNo ratings yet

- Chapter 12-13 SummaryDocument4 pagesChapter 12-13 SummaryXiaoyu KensameNo ratings yet

- Chapter 3 SummaryDocument3 pagesChapter 3 SummaryXiaoyu KensameNo ratings yet

- Chapter 6 SummaryDocument3 pagesChapter 6 SummaryXiaoyu KensameNo ratings yet

- Chapter 2 SummaryDocument3 pagesChapter 2 SummaryXiaoyu KensameNo ratings yet

- Chapter 11 SummaryDocument3 pagesChapter 11 SummaryXiaoyu KensameNo ratings yet

- Chapter 5 SummaryDocument4 pagesChapter 5 SummaryXiaoyu KensameNo ratings yet

- Chapter 8 SummaryDocument5 pagesChapter 8 SummaryXiaoyu KensameNo ratings yet

- Market Capitalization Versus Market ValueDocument3 pagesMarket Capitalization Versus Market ValueIdrisNo ratings yet

- BAIN REPORT European Banking PDFDocument32 pagesBAIN REPORT European Banking PDFRicardo EstellesNo ratings yet

- The Entrepreneural Mind. JollibebsDocument4 pagesThe Entrepreneural Mind. JollibebsJambi LagonoyNo ratings yet

- Comparing Meas With Equal Lives: P A, 12 %, 10 MV P F, 12%, 10 MV (1.12)Document3 pagesComparing Meas With Equal Lives: P A, 12 %, 10 MV P F, 12%, 10 MV (1.12)Jed CernechezNo ratings yet

- Financial Management - Chapter 1 NotesDocument2 pagesFinancial Management - Chapter 1 Notessjshubham2No ratings yet

- FEIA 2&5m Question With AnswerDocument5 pagesFEIA 2&5m Question With Answerprashanthuddar6No ratings yet

- WRD 27e - IE PPT - Ch01 - ADADocument64 pagesWRD 27e - IE PPT - Ch01 - ADAYuchen WangNo ratings yet

- Datacamp Python 3Document36 pagesDatacamp Python 3Luca FarinaNo ratings yet

- Impact of Behavioral Factors On Investors Financial DecisionDocument30 pagesImpact of Behavioral Factors On Investors Financial DecisionpalwashaNo ratings yet

- Dividend TheoriesDocument38 pagesDividend TheoriesMuhammad Azhar Ibné Habib JoomunNo ratings yet

- Exercises For Chapter 10: With SolutionsDocument2 pagesExercises For Chapter 10: With SolutionsshamashmNo ratings yet

- Statements of Financial Position As at 31 December 2009 and 2010Document3 pagesStatements of Financial Position As at 31 December 2009 and 2010mohitgaba19No ratings yet

- A Synopsis Report ON Investment Decision AT Icici Bank LTD: Submitted byDocument9 pagesA Synopsis Report ON Investment Decision AT Icici Bank LTD: Submitted byMOHAMMED KHAYYUMNo ratings yet

- 2020-07-03-CERA - NS-Ambit Capital PVT Lt-Cera Sanitaryware (BUY) Pain Is Inevitable!-89001883Document9 pages2020-07-03-CERA - NS-Ambit Capital PVT Lt-Cera Sanitaryware (BUY) Pain Is Inevitable!-89001883akanksha satijaNo ratings yet

- Your Mind and Your Money - 2-15-10Document2 pagesYour Mind and Your Money - 2-15-10Swapnil SinghNo ratings yet

- 1st Quarter Week 1 - Statement of Financial PositionDocument13 pages1st Quarter Week 1 - Statement of Financial PositionJuvilyn Cariaga FelipeNo ratings yet

- Coca Cola (KO) Balance Sheet PDFDocument2 pagesCoca Cola (KO) Balance Sheet PDFKhmao Sros67% (3)

- wk7 Cost of Capital PDFDocument53 pageswk7 Cost of Capital PDFLito Jose Perez LalantaconNo ratings yet

- Research ProposalDocument19 pagesResearch Proposalዝምታ ተሻለNo ratings yet

- NOTES G RCCP Stocks, StockholdersDocument3 pagesNOTES G RCCP Stocks, StockholdersMelissa Kayla ManiulitNo ratings yet

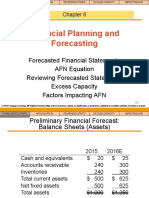

- Financial Planning and ForecastingDocument15 pagesFinancial Planning and ForecastingNicolaus BagaskaraNo ratings yet

- Bangladesh Stock Market Analysis ReportDocument46 pagesBangladesh Stock Market Analysis Reportanon_472625099100% (2)

- 4 HDF MuskanDocument2 pages4 HDF MuskanApurv DixitNo ratings yet

- Introduction - Joint Stock CompanyDocument5 pagesIntroduction - Joint Stock Companyiisjaffer100% (3)

- Relationship Between Corporate Governance Practices and Firms Performance of Indian ContextDocument6 pagesRelationship Between Corporate Governance Practices and Firms Performance of Indian ContextJai VermaNo ratings yet

- Berkshire Hathaway Research PaperDocument8 pagesBerkshire Hathaway Research PaperDennis KimNo ratings yet

- Assessment of Security Analysis and Portfolio Management in Indian Stock MarketDocument5 pagesAssessment of Security Analysis and Portfolio Management in Indian Stock MarketEditor IJTSRDNo ratings yet