Download as pdf or txt

You might also like

- Turnaround at Preston Plant Assignment 3Document5 pagesTurnaround at Preston Plant Assignment 3melinda fahrianiNo ratings yet

- Horngrens Financial and Managerial Accounting 6th Edition Nobles Test BankDocument85 pagesHorngrens Financial and Managerial Accounting 6th Edition Nobles Test Bankmatthewavilawpkrnztjxs100% (33)

- (Seymour B. Chatman) Story and Discourse Narrativ (BookFi - Org) # PDFDocument278 pages(Seymour B. Chatman) Story and Discourse Narrativ (BookFi - Org) # PDFmelinda fahrianiNo ratings yet

- Financial Statement Analysis and The Prediction of Financial DistressDocument77 pagesFinancial Statement Analysis and The Prediction of Financial DistressJosé Manuel EstebanNo ratings yet

- 1112 - 公司理財 syllabusDocument4 pages1112 - 公司理財 syllabus劉丞彬No ratings yet

- SummaryDocument31 pagesSummaryuyiNo ratings yet

- MertonDocument12 pagesMertonrajivagarwalNo ratings yet

- A Critical Analysis of The Use of Financial Statements in Assessing The Performance of An OrganizationDocument65 pagesA Critical Analysis of The Use of Financial Statements in Assessing The Performance of An Organizationjkillerdnum1No ratings yet

- Entrepreneurial Financial Management An Applied Approach 4th Edition Ebook PDFDocument58 pagesEntrepreneurial Financial Management An Applied Approach 4th Edition Ebook PDFdouglas.smith397100% (56)

- Full download Entrepreneurial Financial Management: An Applied Approach 4th Edition, (Ebook PDF) file pdf all chapter on 2024Document44 pagesFull download Entrepreneurial Financial Management: An Applied Approach 4th Edition, (Ebook PDF) file pdf all chapter on 2024ogumameikun100% (1)

- (Download PDF) Entrepreneurial Financial Management An Applied Approach 4Th Edition PDF Full Chapter PDFDocument33 pages(Download PDF) Entrepreneurial Financial Management An Applied Approach 4Th Edition PDF Full Chapter PDFwedleresron100% (10)

- Mastering Corporate Finance Essentials: The Critical Quantitative Methods and Tools in FinanceFrom EverandMastering Corporate Finance Essentials: The Critical Quantitative Methods and Tools in FinanceNo ratings yet

- Managerial FinanceDocument47 pagesManagerial FinanceAinul Mardhiyah100% (1)

- SSRN Id1708148Document55 pagesSSRN Id1708148Siti LailaNo ratings yet

- SummaryDocument39 pagesSummaryAsh JeffNo ratings yet

- Financial Accounting Robert Libby Online Ebook Texxtbook Full Chapter PDFDocument69 pagesFinancial Accounting Robert Libby Online Ebook Texxtbook Full Chapter PDFfrank.morin751100% (12)

- Financial Crisis Dissertation ExamplesDocument7 pagesFinancial Crisis Dissertation ExamplesWriteMyBusinessPaperUK100% (1)

- Impact of The Covid 11Document9 pagesImpact of The Covid 11saleem razaNo ratings yet

- Financial Regulation Dissertation TopicsDocument7 pagesFinancial Regulation Dissertation TopicsBuyWritingPaperUK100% (1)

- Debt Literacy, Financial Experiences and OverindebtnessDocument49 pagesDebt Literacy, Financial Experiences and OverindebtnessasadnbcNo ratings yet

- Case Studies in Finance 8th Edition Bruner Solutions Manual instant download all chapterDocument34 pagesCase Studies in Finance 8th Edition Bruner Solutions Manual instant download all chaptersoukkofaktor31100% (5)

- MSC Finance Dissertation ExampleDocument6 pagesMSC Finance Dissertation ExampleHelpMeWriteAPaperMurfreesboro100% (1)

- Creating a Balanced Scorecard for a Financial Services OrganizationFrom EverandCreating a Balanced Scorecard for a Financial Services OrganizationNo ratings yet

- MSC Accounting and Finance Dissertation TopicsDocument5 pagesMSC Accounting and Finance Dissertation TopicsAcademicPaperWritersSingapore100% (1)

- Credit Line Channel 'Fixed Spread'Document95 pagesCredit Line Channel 'Fixed Spread'Jason WongNo ratings yet

- Critical #1Document6 pagesCritical #1egielynruizdacutanNo ratings yet

- Accounting For Financial Services: Questions Selected byDocument25 pagesAccounting For Financial Services: Questions Selected byGhulam MurtazaNo ratings yet

- Journal of Financial Economics: Karl V. Lins, Henri Servaes, Peter TufanoDocument17 pagesJournal of Financial Economics: Karl V. Lins, Henri Servaes, Peter TufanofulshukNo ratings yet

- RsikDocument4 pagesRsikUjjwal AkashNo ratings yet

- Full Case Studies in Finance 8Th Edition Bruner Solutions Manual Online PDF All ChapterDocument34 pagesFull Case Studies in Finance 8Th Edition Bruner Solutions Manual Online PDF All Chaptereelaniaaquamarine922100% (6)

- Research Paper On Campaign FinanceDocument5 pagesResearch Paper On Campaign Financehubegynowig3100% (1)

- OFRwp 2016 06 - Map of Collateral UsesDocument26 pagesOFRwp 2016 06 - Map of Collateral UsesAbde SfcNo ratings yet

- Football Finance Dissertation TopicsDocument8 pagesFootball Finance Dissertation TopicsPaperWritingWebsiteCanada100% (1)

- 113 - Factoring As A Financing Option Evidence From The UKDocument20 pages113 - Factoring As A Financing Option Evidence From The UKwajih chtibaNo ratings yet

- Claude Verzija 2 DevelopemtDocument18 pagesClaude Verzija 2 DevelopemtIvan MedićNo ratings yet

- Unilever Case Study SynthesisDocument5 pagesUnilever Case Study SynthesisMissie Jane AnteNo ratings yet

- Investment Manager Analysis: A Comprehensive Guide to Portfolio Selection, Monitoring and OptimizationFrom EverandInvestment Manager Analysis: A Comprehensive Guide to Portfolio Selection, Monitoring and OptimizationRating: 3.5 out of 5 stars3.5/5 (1)

- Managing Risk and Performance: A Guide for Government Decision MakersFrom EverandManaging Risk and Performance: A Guide for Government Decision MakersRating: 2 out of 5 stars2/5 (1)

- 2014 2C Sink or Swim How CasDocument15 pages2014 2C Sink or Swim How CasAndyNgoNo ratings yet

- Financial Management Literature Review PDFDocument8 pagesFinancial Management Literature Review PDFc5praq5p100% (1)

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Dissertation Topics in Accounting and Finance Related To AuditingDocument6 pagesDissertation Topics in Accounting and Finance Related To AuditingPaySomeoneToWriteMyPaperGilbertNo ratings yet

- Solution Manual For Auditing and Assurance Services 7th Edition by Timothy LouwersDocument12 pagesSolution Manual For Auditing and Assurance Services 7th Edition by Timothy Louwersarboreal.reveillej17ku100% (47)

- 7470Document30 pages7470ketumsaubiNo ratings yet

- (Download PDF) International Monetary Financial Economics 1st Edition Daniels Solutions Manual Full ChapterDocument30 pages(Download PDF) International Monetary Financial Economics 1st Edition Daniels Solutions Manual Full Chapteraunantinoel100% (8)

- Empirical Capital Structure: A ReviewDocument21 pagesEmpirical Capital Structure: A ReviewLinda FitriNo ratings yet

- Dissertation Proposal Financial CrisisDocument4 pagesDissertation Proposal Financial CrisisBestPaperWritingServiceClarksville100% (1)

- SummaryDocument37 pagesSummaryAJ SuriNo ratings yet

- Accenture Rethinking Risk Financial Institutions CFO CRODocument40 pagesAccenture Rethinking Risk Financial Institutions CFO CROkumarch2012No ratings yet

- 10 1 1 200 3296 PDFDocument49 pages10 1 1 200 3296 PDFjr centenoNo ratings yet

- Effect of Credit Management On Performance of Commercial Banks in Rwanda A Case Study of Equity Bank Rwanda LTDDocument12 pagesEffect of Credit Management On Performance of Commercial Banks in Rwanda A Case Study of Equity Bank Rwanda LTDChethana FrancisNo ratings yet

- Credit Rating Agencies DissertationDocument7 pagesCredit Rating Agencies Dissertationdipsekator1983100% (1)

- Dissertation Topics On Financial RegulationDocument6 pagesDissertation Topics On Financial RegulationIDon'TWantToWriteMyPaperSingapore100% (1)

- Instant Download Corporate Finance 11th Edition Ebook PDF PDF ScribdDocument41 pagesInstant Download Corporate Finance 11th Edition Ebook PDF PDF Scribdlydia.hawkins293100% (54)

- The New Wealth Management: The Financial Advisor's Guide to Managing and Investing Client AssetsFrom EverandThe New Wealth Management: The Financial Advisor's Guide to Managing and Investing Client AssetsNo ratings yet

- Commercial Bank Risk Management An Analysis of TheDocument50 pagesCommercial Bank Risk Management An Analysis of TheajayNo ratings yet

- International Monetary Financial Economics 1st Edition Daniels Solutions Manual instant download all chapterDocument30 pagesInternational Monetary Financial Economics 1st Edition Daniels Solutions Manual instant download all chaptergondakimeta100% (4)

- Abnormal Disclosure Tone and Going Concern Modified Audit ReportsDocument16 pagesAbnormal Disclosure Tone and Going Concern Modified Audit ReportsfathiyaNo ratings yet

- AcSB CP Contributions ResponsesDocument297 pagesAcSB CP Contributions ResponsesShankar ThapaNo ratings yet

- Literature Review On Trade FinanceDocument7 pagesLiterature Review On Trade Financefvfj1pqe100% (1)

- Social Media Influencer, Brand Awareness, and Purchase Decision Among Generation Z in SurabayaDocument9 pagesSocial Media Influencer, Brand Awareness, and Purchase Decision Among Generation Z in Surabayamelinda fahrianiNo ratings yet

- Memahami Pasar-Pasar Emerging (Understanding Markets Oleh: Dr. HartonoDocument23 pagesMemahami Pasar-Pasar Emerging (Understanding Markets Oleh: Dr. Hartonomelinda fahrianiNo ratings yet

- Strategic Implications of Emerging Chinese Multinationals:: The Haier Case StudyDocument8 pagesStrategic Implications of Emerging Chinese Multinationals:: The Haier Case Studymelinda fahrianiNo ratings yet

- Marketing Management: Dealing With CompetitionDocument13 pagesMarketing Management: Dealing With Competitionmelinda fahrianiNo ratings yet

- Translation 2 An Introduction To Oral Translation/ InterpretingDocument15 pagesTranslation 2 An Introduction To Oral Translation/ Interpretingmelinda fahrianiNo ratings yet

- There Isnt Arent Present Simple NegativeDocument2 pagesThere Isnt Arent Present Simple Negativemelinda fahrianiNo ratings yet

- Imus Campus Cavite Civic Center Palico IV, Imus, CaviteDocument13 pagesImus Campus Cavite Civic Center Palico IV, Imus, CaviterueNo ratings yet

- New Microsoft Excel WorksheetDocument2 pagesNew Microsoft Excel WorksheetArvi SunNo ratings yet

- Red Depositarios Al 02 Dic - 2020Document553 pagesRed Depositarios Al 02 Dic - 2020Carlos Andres LduNo ratings yet

- The Impact of Financial Leverage On Return and Risk (#243040) - 211441Document12 pagesThe Impact of Financial Leverage On Return and Risk (#243040) - 211441Prabhmeet SethiNo ratings yet

- Mid Term PPT - Bhavesh Rathod BMS2199Document8 pagesMid Term PPT - Bhavesh Rathod BMS2199bnrathod0902No ratings yet

- Assessment of Internal Control Over Cash (The Case of Wegagen Bank, Wolkite Branch)Document29 pagesAssessment of Internal Control Over Cash (The Case of Wegagen Bank, Wolkite Branch)kassahun mesele100% (6)

- e Banking ReportDocument40 pagese Banking Reportleeshee351No ratings yet

- Panchaganga Farmers Service Cooperative Society LTD HemmadyDocument55 pagesPanchaganga Farmers Service Cooperative Society LTD HemmadySakshath ShettyNo ratings yet

- An Automated Teller MachineDocument23 pagesAn Automated Teller MachineLakshmi LekhaNo ratings yet

- Retail LoansDocument3 pagesRetail LoansMonisha Bhatia0% (1)

- Important - Terms - of - Indian - Economy - 1 - 2 - 1 - 49 Part 2Document8 pagesImportant - Terms - of - Indian - Economy - 1 - 2 - 1 - 49 Part 2Balraj PrajeshNo ratings yet

- Flow Chart For Revenue CollectionDocument6 pagesFlow Chart For Revenue CollectionAdy IbikunleNo ratings yet

- Vidhi Hura B052 Financial PlanDocument3 pagesVidhi Hura B052 Financial PlanVidhi HuraNo ratings yet

- NW Best Referece For Your ReserchDocument109 pagesNW Best Referece For Your ReserchKirubelNo ratings yet

- Africa: Country Capital CurrencyDocument2 pagesAfrica: Country Capital CurrencyAdriana CapusteanuNo ratings yet

- Dokumen - Tips - The Curious Loan Approval Case AnalysisDocument2 pagesDokumen - Tips - The Curious Loan Approval Case AnalysisAyren Dela CruzNo ratings yet

- Clearing System of Exim BankDocument191 pagesClearing System of Exim BankMehedi Hasan SajjadNo ratings yet

- Unofficial Guide To Boston For Babson Students and PartnersDocument101 pagesUnofficial Guide To Boston For Babson Students and PartnersBaldev RawatNo ratings yet

- PPTs On Definition, Structure and Function of Banking Laws Unit - 1Document23 pagesPPTs On Definition, Structure and Function of Banking Laws Unit - 1Ravi saxenaNo ratings yet

- Lessons Learned From Decentralised Finance (Defi)Document22 pagesLessons Learned From Decentralised Finance (Defi)alexander benNo ratings yet

- Bookkeeping Guide For Lawyers - The Law Society (PDFDrive)Document107 pagesBookkeeping Guide For Lawyers - The Law Society (PDFDrive)ConeliusNo ratings yet

- Control Accounts: Unit 4Document2 pagesControl Accounts: Unit 4Shadman ChowdhuryNo ratings yet

- Livin 01Document2 pagesLivin 01im phoneNo ratings yet

- Lesson One - Banking Partners PDFDocument2 pagesLesson One - Banking Partners PDFJOHN MENDOZA GALLEGOSNo ratings yet

- Stop Payment OrdersDocument25 pagesStop Payment Orderssintayehusisay300No ratings yet

- Bank of Palestine Has A Long Embedded Presence and Experience in Palestine Dating Back ToDocument5 pagesBank of Palestine Has A Long Embedded Presence and Experience in Palestine Dating Back ToKaram AbuAloufNo ratings yet

- Sr. No Course Outline Topics: Chapter - 7 Bank Reconciliation Statement (BRS)Document11 pagesSr. No Course Outline Topics: Chapter - 7 Bank Reconciliation Statement (BRS)muhammad zainNo ratings yet

- BRM Assignment 3Document3 pagesBRM Assignment 3HabtamuNo ratings yet

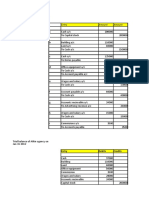

- Journal Entry For Atkin AgencyDocument4 pagesJournal Entry For Atkin AgencySamarth LahotiNo ratings yet