Download as odt, pdf, or txt

You might also like

- THAI - LE THAO - DUYEN - Component B - APDDocument14 pagesTHAI - LE THAO - DUYEN - Component B - APDĐạt TrầnNo ratings yet

- Management Control SystemsDocument76 pagesManagement Control Systemspanpatil swapnil100% (5)

- Driving Growth Through KPI MonitoringDocument11 pagesDriving Growth Through KPI MonitoringHilary OnuorahNo ratings yet

- Evaluating The Quality of Performance MeasuresDocument6 pagesEvaluating The Quality of Performance MeasuresPedada Sai kumarNo ratings yet

- Datasheet Financial Management SeDocument6 pagesDatasheet Financial Management SeALHNo ratings yet

- MAS.2901 - Overview of MASDocument6 pagesMAS.2901 - Overview of MASdaemonspadechocoyNo ratings yet

- Study Unit 1.1Document1 pageStudy Unit 1.1Vee-Jaye VirginoNo ratings yet

- Public Sector Management Accounting and ControlDocument16 pagesPublic Sector Management Accounting and ControlWong Yong Sheng WongNo ratings yet

- Ringkasan AB PDFDocument52 pagesRingkasan AB PDFBintanKamilaNo ratings yet

- Strategy Chapter 6 - Strategic ImplementationDocument16 pagesStrategy Chapter 6 - Strategic ImplementationVân Anh Nguyễn NgọcNo ratings yet

- Lecture 6 - Performance Management in Public SectorDocument4 pagesLecture 6 - Performance Management in Public SectorChuah Chong AnnNo ratings yet

- Presentation On Strategic Management: Made By: Sanchit Gupta Aman Preet Singh Shilpi Sharma Sarthak Goel Lakshay WadhwaDocument19 pagesPresentation On Strategic Management: Made By: Sanchit Gupta Aman Preet Singh Shilpi Sharma Sarthak Goel Lakshay WadhwaNidhi GuptaNo ratings yet

- The Value of OperationsDocument20 pagesThe Value of Operationsabc123No ratings yet

- Department of Accountancy: Management Accounting ConceptsDocument3 pagesDepartment of Accountancy: Management Accounting ConceptsAbdulrahman M. MacacuaNo ratings yet

- TQM & Daily Work ManagementDocument31 pagesTQM & Daily Work ManagementHarry EdwardNo ratings yet

- Elec1 NotesDocument7 pagesElec1 NotesJames RavelaNo ratings yet

- Corporate Performance Management: Framework, Approach and Challenges ObservedDocument9 pagesCorporate Performance Management: Framework, Approach and Challenges ObservedVu HoangNo ratings yet

- Confiabilidad Del EquipoDocument47 pagesConfiabilidad Del EquipoAngello Ever Morales ArrietaNo ratings yet

- Control Function of ManagementDocument14 pagesControl Function of ManagementOscar PozadasNo ratings yet

- Strategic Management: Birat Shrestha/ Resta JhaDocument32 pagesStrategic Management: Birat Shrestha/ Resta JhaKhanal NilambarNo ratings yet

- CTQM - SR. Manager, Chief Manager - 24 Nov 2023Document5 pagesCTQM - SR. Manager, Chief Manager - 24 Nov 2023Anurag BahugunaNo ratings yet

- Two Day Programme On Finance For Non Finance ExecutivesDocument6 pagesTwo Day Programme On Finance For Non Finance ExecutivessandystaysNo ratings yet

- Overview of MASDocument6 pagesOverview of MASDonna AmbaganNo ratings yet

- Synopsis - Chapter 8 - Session 2Document4 pagesSynopsis - Chapter 8 - Session 2sajedulNo ratings yet

- TQM Finals #8Document5 pagesTQM Finals #8Khriestal BalatbatNo ratings yet

- Performance Management: Yesterday-Today-Tomorrow by Effendi IbnoeDocument24 pagesPerformance Management: Yesterday-Today-Tomorrow by Effendi IbnoeFathoni RezaNo ratings yet

- Supplemental Notes On StratManDocument3 pagesSupplemental Notes On StratManWere dooomedNo ratings yet

- PMS Guidelines 1Document23 pagesPMS Guidelines 1TayesaNo ratings yet

- Session 15 - Performance ManagementDocument28 pagesSession 15 - Performance Managementarun kumarNo ratings yet

- KPI Approach For EG v1.0Document5 pagesKPI Approach For EG v1.0Ashish GuptaNo ratings yet

- Strategic Management: Prof. Amol AnkushDocument252 pagesStrategic Management: Prof. Amol AnkushhimanshuNo ratings yet

- Management BasicsDocument72 pagesManagement Basicsma964399No ratings yet

- Unit05 MBO & BSC - HandoutDocument46 pagesUnit05 MBO & BSC - HandoutQuỳnh Anh Bùi ThịNo ratings yet

- Custodio, Pearl Joyce B. March 10, 2017: How To Use The Balanced ScorecardDocument3 pagesCustodio, Pearl Joyce B. March 10, 2017: How To Use The Balanced ScorecardCustodioPearlJoyceNo ratings yet

- KPI S and Performance Management GCDocument34 pagesKPI S and Performance Management GCLeonardo Medici100% (5)

- Introduction To CMDocument33 pagesIntroduction To CMHAKUNA MATATANo ratings yet

- Strama Chapter 1-4Document9 pagesStrama Chapter 1-4Angelica CaduaNo ratings yet

- Chapter - 8 Controlling: Class XII: Business Studies 1Document6 pagesChapter - 8 Controlling: Class XII: Business Studies 1Mahlet100% (1)

- Management Accounting Environment (Final)Document3 pagesManagement Accounting Environment (Final)Mica R.No ratings yet

- On-the-Job Training Blueprint - Chef Concierge - Assistant Chef ConciergeDocument41 pagesOn-the-Job Training Blueprint - Chef Concierge - Assistant Chef ConciergeRHTi BDNo ratings yet

- Human Capital ROIDocument23 pagesHuman Capital ROIMona Abouzied IbrahimNo ratings yet

- Cost Accounting (Chapter 1-3)Document5 pagesCost Accounting (Chapter 1-3)eunice0% (1)

- (Pegr2C2Mtsp) : - Is A Set of Managerial Decisions and Actions ThatDocument2 pages(Pegr2C2Mtsp) : - Is A Set of Managerial Decisions and Actions ThatYvonne BerdosNo ratings yet

- Lecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesLecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro Davaoace ender zeroNo ratings yet

- Test Bank For Business Research Methods 12th Edition by CooperDocument4 pagesTest Bank For Business Research Methods 12th Edition by CooperLala AlalNo ratings yet

- Dipfm Syllabus and Study GuideDocument4 pagesDipfm Syllabus and Study Guidekakes_hussainNo ratings yet

- Performance Management and KPIDocument46 pagesPerformance Management and KPIJonas Onstrup HansenNo ratings yet

- Concept Notes 7 - BORMGTDocument9 pagesConcept Notes 7 - BORMGTIan ReyesNo ratings yet

- Target Operating Model Customer Service 20Document5 pagesTarget Operating Model Customer Service 20VINENNo ratings yet

- 1 The Essence of Performance ManagementDocument44 pages1 The Essence of Performance ManagementndiNo ratings yet

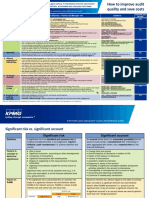

- How To Improve Audit Quality and Save CostsDocument2 pagesHow To Improve Audit Quality and Save CostsSalauddin Kader ACCANo ratings yet

- Lecture 1 - Managerial Accounting - July 2020Document4 pagesLecture 1 - Managerial Accounting - July 2020MARCOS GUADALOPENo ratings yet

- Finance For Non Financial Managers BrochureDocument4 pagesFinance For Non Financial Managers Brochureenworld9No ratings yet

- Management Process PODCDocument57 pagesManagement Process PODCyourhunkieNo ratings yet

- Balanced Scorecard For ClassDocument16 pagesBalanced Scorecard For ClassNicole Villamil AntiqueNo ratings yet

- Datasheet Workday Financial ManagementDocument6 pagesDatasheet Workday Financial Managementtechoutloud.infoNo ratings yet

- Budgeting StrategiesDocument4 pagesBudgeting StrategiesJaya ShankarNo ratings yet

- Goal Setting GuideDocument6 pagesGoal Setting GuidesamlwmNo ratings yet

- Follow The Trend1.1Document11 pagesFollow The Trend1.1S Radhakrishna BhandaryNo ratings yet

- Chapter 6 - Organization StudyDocument21 pagesChapter 6 - Organization StudyRed SecretarioNo ratings yet

- Upload 3 Documents To Download: TKDN SmsDocument2 pagesUpload 3 Documents To Download: TKDN SmsLucia AngelinaNo ratings yet

- Esd Module PDFDocument100 pagesEsd Module PDFkeith Nkala0% (1)

- Weidenfeld-Hoffmann Scholarships Statement Form For 2023-24 EntryDocument4 pagesWeidenfeld-Hoffmann Scholarships Statement Form For 2023-24 EntryOmer Oksuzler (sultanomar)No ratings yet

- Walt Disney World Thesis StatementDocument7 pagesWalt Disney World Thesis Statementzaivlghig100% (2)

- DIGESTDocument9 pagesDIGESTNhaz PasandalanNo ratings yet

- Renders Chapter Six HomeworkDocument8 pagesRenders Chapter Six HomeworkAsad Ehsan Warraich0% (1)

- Division 1 - Duties of Owners, Tenants, Occupants and Visitors 1. Payment of Strata FeesDocument17 pagesDivision 1 - Duties of Owners, Tenants, Occupants and Visitors 1. Payment of Strata FeesPritish TandonNo ratings yet

- Final - PSM - Incident InvestigationDocument29 pagesFinal - PSM - Incident InvestigationSimon TounsiNo ratings yet

- AccountDetails Aslam MDocument1 pageAccountDetails Aslam MPancho G ReyesNo ratings yet

- DDM MaswiDocument7 pagesDDM MaswiELIAKIM C MASWINo ratings yet

- Important RemindersDocument4 pagesImportant RemindersJulie Rose Gasco AmbongNo ratings yet

- ZOTA 15062023165216 Outcome15062023Document7 pagesZOTA 15062023165216 Outcome15062023Ankk TenderzNo ratings yet

- Principles of Marketing Module 7Document15 pagesPrinciples of Marketing Module 7Raphael BillanesNo ratings yet

- IAS Hub Web UI PDFDocument1 pageIAS Hub Web UI PDFKABIR BATRANo ratings yet

- A Guide On Tax Incentives/ ExemptionsDocument52 pagesA Guide On Tax Incentives/ ExemptionsWavah Mugabi NateNo ratings yet

- CIR Vs Burmeister Wain Scandinavian Contractor - FullDocument6 pagesCIR Vs Burmeister Wain Scandinavian Contractor - FullCheryl ChurlNo ratings yet

- Ong Vs CADocument5 pagesOng Vs CATherese Gail JimenezNo ratings yet

- Overview of Risk-Based Audit Process: Mary Rose A. CotanasDocument19 pagesOverview of Risk-Based Audit Process: Mary Rose A. CotanasJnn CycNo ratings yet

- Name Sex Place / Date of Birth Nationality Status ReligionDocument2 pagesName Sex Place / Date of Birth Nationality Status ReligionEli KempNo ratings yet

- Core Competency: Submitted byDocument8 pagesCore Competency: Submitted byMaheshKumarBagartiNo ratings yet

- Supply Chain Management NDocument288 pagesSupply Chain Management NInfotech Edge100% (1)

- Mba Financial AssgDocument10 pagesMba Financial Assgseifu deraraNo ratings yet

- A Study On Selected Equity Mutual FundsDocument5 pagesA Study On Selected Equity Mutual FundsEditor IJTSRDNo ratings yet

- Business Valuation: Economic ConditionsDocument10 pagesBusiness Valuation: Economic ConditionscuteheenaNo ratings yet

- Material Requirement Planning Case StudyDocument7 pagesMaterial Requirement Planning Case StudyAKHIL GOYALNo ratings yet

- FI108 Umoja Cost and Management Accounting Overview CBT v15Document85 pagesFI108 Umoja Cost and Management Accounting Overview CBT v15totoNo ratings yet

- CV PDF (1) - 1 Enea QafaDocument2 pagesCV PDF (1) - 1 Enea QafaEnea QafaNo ratings yet