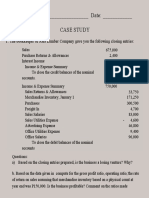

Global Reciprocal College Inctax-1 Final Examination 1st Semester, SY 2020-2021 Problem 1

Global Reciprocal College Inctax-1 Final Examination 1st Semester, SY 2020-2021 Problem 1

You might also like

- 14.0 Final Quiz 1 Tax On IndividualsDocument8 pages14.0 Final Quiz 1 Tax On IndividualsRezhel Vyrneth Turgo100% (1)

- 9.2 Assignment - Allowable DeductionsDocument5 pages9.2 Assignment - Allowable Deductionssam imperialNo ratings yet

- Corporation ActivityDocument4 pagesCorporation ActivityLFGS FinalsNo ratings yet

- Auditing TheoryDocument27 pagesAuditing Theorysharielles /No ratings yet

- Chapter 13 Part 1Document11 pagesChapter 13 Part 1Danielle Angel MalanaNo ratings yet

- Handout 3Document51 pagesHandout 3Jilian Kate Alpapara Bustamante100% (1)

- Higher Education Department: Maryhill College, IncDocument4 pagesHigher Education Department: Maryhill College, Incpat patNo ratings yet

- Acctng 321 Advanced Financial Accounting and Reporting 2: Eastern Samar State UniversityDocument4 pagesAcctng 321 Advanced Financial Accounting and Reporting 2: Eastern Samar State UniversityNhel AlvaroNo ratings yet

- Lesson 6Document12 pagesLesson 6sharielles /No ratings yet

- Final Project Report On Investment BankingDocument26 pagesFinal Project Report On Investment BankingSophia Ali78% (9)

- Quiz On Chapter 13B&CDocument23 pagesQuiz On Chapter 13B&Cdianne caballeroNo ratings yet

- Fringe Benefits, de Minimis Benefits, Filing of Income Tax ReturnDocument5 pagesFringe Benefits, de Minimis Benefits, Filing of Income Tax ReturndgdeguzmanNo ratings yet

- 8.2 Assignment - Regular Income Tax For IndividualsDocument8 pages8.2 Assignment - Regular Income Tax For Individualssam imperialNo ratings yet

- False False True True True FalseDocument7 pagesFalse False True True True Falsegazer beam100% (1)

- CH10 Long Term Decision Payongayong-3Document1 pageCH10 Long Term Decision Payongayong-3Nadi HoodNo ratings yet

- True or FalseDocument76 pagesTrue or FalsepangytpangytNo ratings yet

- Intermediate Accounting 3 - January 24, 2023, F2F DiscussionDocument8 pagesIntermediate Accounting 3 - January 24, 2023, F2F DiscussionZhaira Kim CantosNo ratings yet

- 4.1 Assignment - Final Tax On Passive Income (To Be Answered in Lecture)Document6 pages4.1 Assignment - Final Tax On Passive Income (To Be Answered in Lecture)Charles Mateo100% (3)

- Jay Mariz C. Ramirez Juan Dela Cruz: 1. Exempt de Minimis Benefits: P124,500Document3 pagesJay Mariz C. Ramirez Juan Dela Cruz: 1. Exempt de Minimis Benefits: P124,500Jay Mariz C. RamirezNo ratings yet

- Business Tax 4Document24 pagesBusiness Tax 4Cheska AtienzaNo ratings yet

- Tax On Idividuals: Practice ProblemsDocument17 pagesTax On Idividuals: Practice ProblemsLealyn CuestaNo ratings yet

- Chapter 1 5 Income Tax MCDocument14 pagesChapter 1 5 Income Tax MCNoella Marie BaronNo ratings yet

- Cultivating A Synergic Relationship With ShareholdersDocument6 pagesCultivating A Synergic Relationship With ShareholdersJeric Lagyaban AstrologioNo ratings yet

- Taxation Final Pre Board Oct 2016Document13 pagesTaxation Final Pre Board Oct 2016Maryane AngelaNo ratings yet

- IT Module No. 7: Introduction To Regular Income TaxDocument13 pagesIT Module No. 7: Introduction To Regular Income TaxjakeNo ratings yet

- Vdocuments - MX - Answers Chapter 3 Vol 2 RvsedDocument13 pagesVdocuments - MX - Answers Chapter 3 Vol 2 RvsedmirayNo ratings yet

- Income Tax Banggawan Ch11 CompressDocument10 pagesIncome Tax Banggawan Ch11 CompressRhian BarzanaNo ratings yet

- Output TaxDocument15 pagesOutput TaxAmie Jane MirandaNo ratings yet

- c2 Premium Liability Lets Get It PDFDocument15 pagesc2 Premium Liability Lets Get It PDFCris VillarNo ratings yet

- MAS1Document48 pagesMAS1ryan angelica allanicNo ratings yet

- Osd CorrectionDocument2 pagesOsd CorrectionSai BomNo ratings yet

- Chapter 7: Business Taxes: ProblemsDocument8 pagesChapter 7: Business Taxes: ProblemsAva DoveNo ratings yet

- Tax 3216Document5 pagesTax 3216Rich William PagaduanNo ratings yet

- 025872995Document140 pages025872995Nhorelajne ManaogNo ratings yet

- BUSE 3 - Practice ProblemDocument8 pagesBUSE 3 - Practice ProblemPang SiulienNo ratings yet

- ACCO 20133 - UNIT IX - UpdatedDocument29 pagesACCO 20133 - UNIT IX - UpdatedHarvey AguilarNo ratings yet

- Add: Desired Ending Raw Materials Inventory (130% From Following Month's Production and 2000Document4 pagesAdd: Desired Ending Raw Materials Inventory (130% From Following Month's Production and 2000Kyla Kim AriasNo ratings yet

- Fringe Benefits ScenariosDocument2 pagesFringe Benefits ScenariosKatherine BorjaNo ratings yet

- Fin Man - Module 3 ContinuitionDocument6 pagesFin Man - Module 3 ContinuitionFrancine PrietoNo ratings yet

- Review of The Accounting Process Problems 2-1. (Tiger Company)Document5 pagesReview of The Accounting Process Problems 2-1. (Tiger Company)Joana MagtuboNo ratings yet

- Income Taxation Mcqs&ProblemsDocument14 pagesIncome Taxation Mcqs&ProblemsJayrald LacabaNo ratings yet

- 03 - Task - Performance - 1 (15) Business TaxationDocument4 pages03 - Task - Performance - 1 (15) Business TaxationAries Christian S PadillaNo ratings yet

- Lim Tax 5 Quiz AnswerDocument4 pagesLim Tax 5 Quiz AnswerIvan AnaboNo ratings yet

- Week 10 CorporationssDocument9 pagesWeek 10 CorporationssAdrian MontemayorNo ratings yet

- Assessment 1 Tax 1Document3 pagesAssessment 1 Tax 1Judy Ann GacetaNo ratings yet

- MixDocument32 pagesMixUnnecessary BuyingNo ratings yet

- SITUS OF DIVIDEND INCOME - QuizzerDocument2 pagesSITUS OF DIVIDEND INCOME - Quizzerbrr brrNo ratings yet

- 2021 Audited Financial Statement of Puregold Price Club Inc Parent 1 111021Document64 pages2021 Audited Financial Statement of Puregold Price Club Inc Parent 1 111021Merille Vasquez100% (1)

- QUIZ 4 - Income TaxDocument4 pagesQUIZ 4 - Income TaxTUAZON JR., NESTOR A.No ratings yet

- Tax 1 AssignmentDocument3 pagesTax 1 AssignmentKira YamashiNo ratings yet

- 146 155Document3 pages146 155Star Ramirez50% (2)

- P20,000 P18,000 P2,000 P0: 2 PointsDocument10 pagesP20,000 P18,000 P2,000 P0: 2 PointsKatrina Dela CruzNo ratings yet

- Transfer and Business TaxationDocument131 pagesTransfer and Business TaxationMr.AccntngNo ratings yet

- Vergara, Gian Bianca F. BSAT-4A Recitation: Compensation IncomeDocument4 pagesVergara, Gian Bianca F. BSAT-4A Recitation: Compensation Incomelena cpaNo ratings yet

- InventoryDocument4 pagesInventoryChris LutzNo ratings yet

- Deductions From Gross Income 2 1Document42 pagesDeductions From Gross Income 2 1Katherine Ederosas100% (1)

- Find Study Resources: Answered Step-By-StepDocument12 pagesFind Study Resources: Answered Step-By-StepBisag AsaNo ratings yet

- Chapter 4 EXERCISES - Estates and TrustsDocument9 pagesChapter 4 EXERCISES - Estates and TrustscathyydumpNo ratings yet

- Chapter 14 Answer PDF FreeDocument24 pagesChapter 14 Answer PDF FreeAang GrandeNo ratings yet

- Self Check: Direction: Open The File Self Check Number 5 in Your LMS or Flash Email Account. It Is AnDocument13 pagesSelf Check: Direction: Open The File Self Check Number 5 in Your LMS or Flash Email Account. It Is AnDanah Paz MamanaoNo ratings yet

- It Chapter 11Document5 pagesIt Chapter 11Rena Jocelle NalzaroNo ratings yet

- FBTDocument4 pagesFBTRogienel ReyesNo ratings yet

- SW06Document6 pagesSW06Nadi HoodNo ratings yet

- Statement of The ProblemDocument2 pagesStatement of The Problemsharielles /No ratings yet

- Exercise 2Document2 pagesExercise 2sharielles /No ratings yet

- APA Citation PRESENTATIONDocument19 pagesAPA Citation PRESENTATIONsharielles /No ratings yet

- Aaspin Lecture No. 1Document3 pagesAaspin Lecture No. 1sharielles /No ratings yet

- AUCISE Case-Study-2Document1 pageAUCISE Case-Study-2sharielles /No ratings yet

- Case Study AUSCISEDocument2 pagesCase Study AUSCISEsharielles /No ratings yet

- BDO Unibank 2021 Annual Report Financial SupplementsDocument236 pagesBDO Unibank 2021 Annual Report Financial Supplementssharielles /No ratings yet

- Review On Related LiteratureDocument1 pageReview On Related Literaturesharielles /No ratings yet

- Preparatory Video #1Document2 pagesPreparatory Video #1sharielles /No ratings yet

- Quiz No. 1-AFAR-08 AFAR-09ADocument7 pagesQuiz No. 1-AFAR-08 AFAR-09Asharielles /No ratings yet

- Aacap1 2021-2022 Midterm ExaminationDocument18 pagesAacap1 2021-2022 Midterm Examinationsharielles /No ratings yet

- Prelimary Examinations - AFAR01Document12 pagesPrelimary Examinations - AFAR01sharielles /No ratings yet

- Chapter 5 Designing Overall Responses and Further Audit Procedures - CompressDocument32 pagesChapter 5 Designing Overall Responses and Further Audit Procedures - Compresssharielles /No ratings yet

- Group 2 Written ReportDocument4 pagesGroup 2 Written Reportsharielles /No ratings yet

- AACAP - Exercise 2Document4 pagesAACAP - Exercise 2sharielles /No ratings yet

- ACC1AIS Week 8 Homework ExercisesDocument4 pagesACC1AIS Week 8 Homework Exercisessharielles /No ratings yet

- RFLIB Midterm Examination FINALDocument7 pagesRFLIB Midterm Examination FINALsharielles /No ratings yet

- Business Recovery Plan V1Document13 pagesBusiness Recovery Plan V1sharielles /No ratings yet

- Life and Works of Rizal Quiz 2Document4 pagesLife and Works of Rizal Quiz 2sharielles /No ratings yet

- Cygnus Industries Inc.Document19 pagesCygnus Industries Inc.sharielles /No ratings yet

- Acc Financial MarketsDocument153 pagesAcc Financial Marketssharielles /No ratings yet

- Week 4 - Introduction To EthicsDocument9 pagesWeek 4 - Introduction To Ethicssharielles /No ratings yet

- MODULE 4 Relevant CostingDocument9 pagesMODULE 4 Relevant Costingsharielles /No ratings yet

- MODULE 3 Absorption & Variable CostingDocument7 pagesMODULE 3 Absorption & Variable Costingsharielles /No ratings yet

- MODULE 1 Introduction To Management Accounting & Strategic MGTDocument9 pagesMODULE 1 Introduction To Management Accounting & Strategic MGTsharielles /No ratings yet

- MODULE 2 CVP AnalysisDocument8 pagesMODULE 2 CVP Analysissharielles /No ratings yet

- Week 3 - Corporate Governance Responsibilities and AccountabilitiesDocument28 pagesWeek 3 - Corporate Governance Responsibilities and Accountabilitiessharielles /No ratings yet

- Week 5 - Business EthicsDocument34 pagesWeek 5 - Business Ethicssharielles /No ratings yet

- 00 - Anti - Violence Against Women and Their ChildrenDocument17 pages00 - Anti - Violence Against Women and Their Childrenronan.villagonzaloNo ratings yet

- Power Up MocoDocument7 pagesPower Up MocoParents' Coalition of Montgomery County, MarylandNo ratings yet

- Presentation On Benazir's Second TenureDocument16 pagesPresentation On Benazir's Second TenureFatimaNo ratings yet

- Varsha Mishra XB13 DisabilityDocument6 pagesVarsha Mishra XB13 DisabilityKanchan ManhasNo ratings yet

- Financial Ratio Template Free V61Document9 pagesFinancial Ratio Template Free V61Tommy RamadanNo ratings yet

- Voting Rights Amendments Notes CompleteDocument4 pagesVoting Rights Amendments Notes Completeapi-328061525No ratings yet

- OTA Tech PDFDocument169 pagesOTA Tech PDFlightstar10No ratings yet

- SB 994Document7 pagesSB 994ABC Action NewsNo ratings yet

- Holmes. The Age of Justinian and Theodora. July 1905. Volume 2.Document426 pagesHolmes. The Age of Justinian and Theodora. July 1905. Volume 2.Patrologia Latina, Graeca et Orientalis100% (1)

- Gandhi and National MovementDocument30 pagesGandhi and National MovementArun kumar SethiNo ratings yet

- Application Form - PLO AMP - County Reps and AmbassadorsDocument6 pagesApplication Form - PLO AMP - County Reps and AmbassadorsLazarus Kadett Ndivayele100% (1)

- Code of Practice On ConsultationDocument16 pagesCode of Practice On Consultationaeo9898No ratings yet

- Ch.3: Powers and Functions of Administrative Agencies A. in GeneralDocument8 pagesCh.3: Powers and Functions of Administrative Agencies A. in GeneralNalule Peace KNo ratings yet

- Government Finance: Taxation in The United States United States Federal BudgetDocument7 pagesGovernment Finance: Taxation in The United States United States Federal BudgetKatt RinaNo ratings yet

- Asnake InternshipDocument36 pagesAsnake Internshipkassahungedefaye3120% (1)

- Electronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationDocument10 pagesElectronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationStan J. CaterboneNo ratings yet

- P&R AnalysisDocument29 pagesP&R Analysiscontact.xinanneNo ratings yet

- Accounting Hawk - LawDocument24 pagesAccounting Hawk - LawClaire BarbaNo ratings yet

- A5 - Fringe Benefit TaxationDocument3 pagesA5 - Fringe Benefit TaxationJomer FernandezNo ratings yet

- AT.3403 - Risk-Based FS Audit ProcessDocument5 pagesAT.3403 - Risk-Based FS Audit ProcessMonica GarciaNo ratings yet

- Liham - Pahintulot: Republic of The Philippines Department of Education Schools Division of PalawanDocument12 pagesLiham - Pahintulot: Republic of The Philippines Department of Education Schools Division of PalawanMarbert GarganzaNo ratings yet

- Self Defense For WomenDocument16 pagesSelf Defense For WomenJoseph NithaiahNo ratings yet

- Annual Report 2017 18Document122 pagesAnnual Report 2017 18Ali AhmedNo ratings yet

- Hosea: Author and DateDocument3 pagesHosea: Author and DateWilliam Ng'ongaNo ratings yet

- The Reform Branch of The ReformationDocument2 pagesThe Reform Branch of The Reformationcristina ignacioNo ratings yet

- Plaintiffs-Appellees Vs Vs Defendant-Appellant Jose T. Sumcad Ramon B. de Los Reyes Angel IlaganDocument3 pagesPlaintiffs-Appellees Vs Vs Defendant-Appellant Jose T. Sumcad Ramon B. de Los Reyes Angel IlaganAehrold GarmaNo ratings yet

- 8071939554Document1 page8071939554Vishnu SasindranNo ratings yet

- Apple: December 11-12-2016:itpm Senior Trading Mentor Raj Malhotra Interview On Why Traders FailDocument3 pagesApple: December 11-12-2016:itpm Senior Trading Mentor Raj Malhotra Interview On Why Traders FaildenisNo ratings yet

- Aath Graphic OrganizerDocument4 pagesAath Graphic Organizerapi-438882571No ratings yet

Download as xlsx, pdf, or txt

You might also like

- 14.0 Final Quiz 1 Tax On IndividualsDocument8 pages14.0 Final Quiz 1 Tax On IndividualsRezhel Vyrneth Turgo100% (1)

- 9.2 Assignment - Allowable DeductionsDocument5 pages9.2 Assignment - Allowable Deductionssam imperialNo ratings yet

- Corporation ActivityDocument4 pagesCorporation ActivityLFGS FinalsNo ratings yet

- Auditing TheoryDocument27 pagesAuditing Theorysharielles /No ratings yet

- Chapter 13 Part 1Document11 pagesChapter 13 Part 1Danielle Angel MalanaNo ratings yet

- Handout 3Document51 pagesHandout 3Jilian Kate Alpapara Bustamante100% (1)

- Higher Education Department: Maryhill College, IncDocument4 pagesHigher Education Department: Maryhill College, Incpat patNo ratings yet

- Acctng 321 Advanced Financial Accounting and Reporting 2: Eastern Samar State UniversityDocument4 pagesAcctng 321 Advanced Financial Accounting and Reporting 2: Eastern Samar State UniversityNhel AlvaroNo ratings yet

- Lesson 6Document12 pagesLesson 6sharielles /No ratings yet

- Final Project Report On Investment BankingDocument26 pagesFinal Project Report On Investment BankingSophia Ali78% (9)

- Quiz On Chapter 13B&CDocument23 pagesQuiz On Chapter 13B&Cdianne caballeroNo ratings yet

- Fringe Benefits, de Minimis Benefits, Filing of Income Tax ReturnDocument5 pagesFringe Benefits, de Minimis Benefits, Filing of Income Tax ReturndgdeguzmanNo ratings yet

- 8.2 Assignment - Regular Income Tax For IndividualsDocument8 pages8.2 Assignment - Regular Income Tax For Individualssam imperialNo ratings yet

- False False True True True FalseDocument7 pagesFalse False True True True Falsegazer beam100% (1)

- CH10 Long Term Decision Payongayong-3Document1 pageCH10 Long Term Decision Payongayong-3Nadi HoodNo ratings yet

- True or FalseDocument76 pagesTrue or FalsepangytpangytNo ratings yet

- Intermediate Accounting 3 - January 24, 2023, F2F DiscussionDocument8 pagesIntermediate Accounting 3 - January 24, 2023, F2F DiscussionZhaira Kim CantosNo ratings yet

- 4.1 Assignment - Final Tax On Passive Income (To Be Answered in Lecture)Document6 pages4.1 Assignment - Final Tax On Passive Income (To Be Answered in Lecture)Charles Mateo100% (3)

- Jay Mariz C. Ramirez Juan Dela Cruz: 1. Exempt de Minimis Benefits: P124,500Document3 pagesJay Mariz C. Ramirez Juan Dela Cruz: 1. Exempt de Minimis Benefits: P124,500Jay Mariz C. RamirezNo ratings yet

- Business Tax 4Document24 pagesBusiness Tax 4Cheska AtienzaNo ratings yet

- Tax On Idividuals: Practice ProblemsDocument17 pagesTax On Idividuals: Practice ProblemsLealyn CuestaNo ratings yet

- Chapter 1 5 Income Tax MCDocument14 pagesChapter 1 5 Income Tax MCNoella Marie BaronNo ratings yet

- Cultivating A Synergic Relationship With ShareholdersDocument6 pagesCultivating A Synergic Relationship With ShareholdersJeric Lagyaban AstrologioNo ratings yet

- Taxation Final Pre Board Oct 2016Document13 pagesTaxation Final Pre Board Oct 2016Maryane AngelaNo ratings yet

- IT Module No. 7: Introduction To Regular Income TaxDocument13 pagesIT Module No. 7: Introduction To Regular Income TaxjakeNo ratings yet

- Vdocuments - MX - Answers Chapter 3 Vol 2 RvsedDocument13 pagesVdocuments - MX - Answers Chapter 3 Vol 2 RvsedmirayNo ratings yet

- Income Tax Banggawan Ch11 CompressDocument10 pagesIncome Tax Banggawan Ch11 CompressRhian BarzanaNo ratings yet

- Output TaxDocument15 pagesOutput TaxAmie Jane MirandaNo ratings yet

- c2 Premium Liability Lets Get It PDFDocument15 pagesc2 Premium Liability Lets Get It PDFCris VillarNo ratings yet

- MAS1Document48 pagesMAS1ryan angelica allanicNo ratings yet

- Osd CorrectionDocument2 pagesOsd CorrectionSai BomNo ratings yet

- Chapter 7: Business Taxes: ProblemsDocument8 pagesChapter 7: Business Taxes: ProblemsAva DoveNo ratings yet

- Tax 3216Document5 pagesTax 3216Rich William PagaduanNo ratings yet

- 025872995Document140 pages025872995Nhorelajne ManaogNo ratings yet

- BUSE 3 - Practice ProblemDocument8 pagesBUSE 3 - Practice ProblemPang SiulienNo ratings yet

- ACCO 20133 - UNIT IX - UpdatedDocument29 pagesACCO 20133 - UNIT IX - UpdatedHarvey AguilarNo ratings yet

- Add: Desired Ending Raw Materials Inventory (130% From Following Month's Production and 2000Document4 pagesAdd: Desired Ending Raw Materials Inventory (130% From Following Month's Production and 2000Kyla Kim AriasNo ratings yet

- Fringe Benefits ScenariosDocument2 pagesFringe Benefits ScenariosKatherine BorjaNo ratings yet

- Fin Man - Module 3 ContinuitionDocument6 pagesFin Man - Module 3 ContinuitionFrancine PrietoNo ratings yet

- Review of The Accounting Process Problems 2-1. (Tiger Company)Document5 pagesReview of The Accounting Process Problems 2-1. (Tiger Company)Joana MagtuboNo ratings yet

- Income Taxation Mcqs&ProblemsDocument14 pagesIncome Taxation Mcqs&ProblemsJayrald LacabaNo ratings yet

- 03 - Task - Performance - 1 (15) Business TaxationDocument4 pages03 - Task - Performance - 1 (15) Business TaxationAries Christian S PadillaNo ratings yet

- Lim Tax 5 Quiz AnswerDocument4 pagesLim Tax 5 Quiz AnswerIvan AnaboNo ratings yet

- Week 10 CorporationssDocument9 pagesWeek 10 CorporationssAdrian MontemayorNo ratings yet

- Assessment 1 Tax 1Document3 pagesAssessment 1 Tax 1Judy Ann GacetaNo ratings yet

- MixDocument32 pagesMixUnnecessary BuyingNo ratings yet

- SITUS OF DIVIDEND INCOME - QuizzerDocument2 pagesSITUS OF DIVIDEND INCOME - Quizzerbrr brrNo ratings yet

- 2021 Audited Financial Statement of Puregold Price Club Inc Parent 1 111021Document64 pages2021 Audited Financial Statement of Puregold Price Club Inc Parent 1 111021Merille Vasquez100% (1)

- QUIZ 4 - Income TaxDocument4 pagesQUIZ 4 - Income TaxTUAZON JR., NESTOR A.No ratings yet

- Tax 1 AssignmentDocument3 pagesTax 1 AssignmentKira YamashiNo ratings yet

- 146 155Document3 pages146 155Star Ramirez50% (2)

- P20,000 P18,000 P2,000 P0: 2 PointsDocument10 pagesP20,000 P18,000 P2,000 P0: 2 PointsKatrina Dela CruzNo ratings yet

- Transfer and Business TaxationDocument131 pagesTransfer and Business TaxationMr.AccntngNo ratings yet

- Vergara, Gian Bianca F. BSAT-4A Recitation: Compensation IncomeDocument4 pagesVergara, Gian Bianca F. BSAT-4A Recitation: Compensation Incomelena cpaNo ratings yet

- InventoryDocument4 pagesInventoryChris LutzNo ratings yet

- Deductions From Gross Income 2 1Document42 pagesDeductions From Gross Income 2 1Katherine Ederosas100% (1)

- Find Study Resources: Answered Step-By-StepDocument12 pagesFind Study Resources: Answered Step-By-StepBisag AsaNo ratings yet

- Chapter 4 EXERCISES - Estates and TrustsDocument9 pagesChapter 4 EXERCISES - Estates and TrustscathyydumpNo ratings yet

- Chapter 14 Answer PDF FreeDocument24 pagesChapter 14 Answer PDF FreeAang GrandeNo ratings yet

- Self Check: Direction: Open The File Self Check Number 5 in Your LMS or Flash Email Account. It Is AnDocument13 pagesSelf Check: Direction: Open The File Self Check Number 5 in Your LMS or Flash Email Account. It Is AnDanah Paz MamanaoNo ratings yet

- It Chapter 11Document5 pagesIt Chapter 11Rena Jocelle NalzaroNo ratings yet

- FBTDocument4 pagesFBTRogienel ReyesNo ratings yet

- SW06Document6 pagesSW06Nadi HoodNo ratings yet

- Statement of The ProblemDocument2 pagesStatement of The Problemsharielles /No ratings yet

- Exercise 2Document2 pagesExercise 2sharielles /No ratings yet

- APA Citation PRESENTATIONDocument19 pagesAPA Citation PRESENTATIONsharielles /No ratings yet

- Aaspin Lecture No. 1Document3 pagesAaspin Lecture No. 1sharielles /No ratings yet

- AUCISE Case-Study-2Document1 pageAUCISE Case-Study-2sharielles /No ratings yet

- Case Study AUSCISEDocument2 pagesCase Study AUSCISEsharielles /No ratings yet

- BDO Unibank 2021 Annual Report Financial SupplementsDocument236 pagesBDO Unibank 2021 Annual Report Financial Supplementssharielles /No ratings yet

- Review On Related LiteratureDocument1 pageReview On Related Literaturesharielles /No ratings yet

- Preparatory Video #1Document2 pagesPreparatory Video #1sharielles /No ratings yet

- Quiz No. 1-AFAR-08 AFAR-09ADocument7 pagesQuiz No. 1-AFAR-08 AFAR-09Asharielles /No ratings yet

- Aacap1 2021-2022 Midterm ExaminationDocument18 pagesAacap1 2021-2022 Midterm Examinationsharielles /No ratings yet

- Prelimary Examinations - AFAR01Document12 pagesPrelimary Examinations - AFAR01sharielles /No ratings yet

- Chapter 5 Designing Overall Responses and Further Audit Procedures - CompressDocument32 pagesChapter 5 Designing Overall Responses and Further Audit Procedures - Compresssharielles /No ratings yet

- Group 2 Written ReportDocument4 pagesGroup 2 Written Reportsharielles /No ratings yet

- AACAP - Exercise 2Document4 pagesAACAP - Exercise 2sharielles /No ratings yet

- ACC1AIS Week 8 Homework ExercisesDocument4 pagesACC1AIS Week 8 Homework Exercisessharielles /No ratings yet

- RFLIB Midterm Examination FINALDocument7 pagesRFLIB Midterm Examination FINALsharielles /No ratings yet

- Business Recovery Plan V1Document13 pagesBusiness Recovery Plan V1sharielles /No ratings yet

- Life and Works of Rizal Quiz 2Document4 pagesLife and Works of Rizal Quiz 2sharielles /No ratings yet

- Cygnus Industries Inc.Document19 pagesCygnus Industries Inc.sharielles /No ratings yet

- Acc Financial MarketsDocument153 pagesAcc Financial Marketssharielles /No ratings yet

- Week 4 - Introduction To EthicsDocument9 pagesWeek 4 - Introduction To Ethicssharielles /No ratings yet

- MODULE 4 Relevant CostingDocument9 pagesMODULE 4 Relevant Costingsharielles /No ratings yet

- MODULE 3 Absorption & Variable CostingDocument7 pagesMODULE 3 Absorption & Variable Costingsharielles /No ratings yet

- MODULE 1 Introduction To Management Accounting & Strategic MGTDocument9 pagesMODULE 1 Introduction To Management Accounting & Strategic MGTsharielles /No ratings yet

- MODULE 2 CVP AnalysisDocument8 pagesMODULE 2 CVP Analysissharielles /No ratings yet

- Week 3 - Corporate Governance Responsibilities and AccountabilitiesDocument28 pagesWeek 3 - Corporate Governance Responsibilities and Accountabilitiessharielles /No ratings yet

- Week 5 - Business EthicsDocument34 pagesWeek 5 - Business Ethicssharielles /No ratings yet

- 00 - Anti - Violence Against Women and Their ChildrenDocument17 pages00 - Anti - Violence Against Women and Their Childrenronan.villagonzaloNo ratings yet

- Power Up MocoDocument7 pagesPower Up MocoParents' Coalition of Montgomery County, MarylandNo ratings yet

- Presentation On Benazir's Second TenureDocument16 pagesPresentation On Benazir's Second TenureFatimaNo ratings yet

- Varsha Mishra XB13 DisabilityDocument6 pagesVarsha Mishra XB13 DisabilityKanchan ManhasNo ratings yet

- Financial Ratio Template Free V61Document9 pagesFinancial Ratio Template Free V61Tommy RamadanNo ratings yet

- Voting Rights Amendments Notes CompleteDocument4 pagesVoting Rights Amendments Notes Completeapi-328061525No ratings yet

- OTA Tech PDFDocument169 pagesOTA Tech PDFlightstar10No ratings yet

- SB 994Document7 pagesSB 994ABC Action NewsNo ratings yet

- Holmes. The Age of Justinian and Theodora. July 1905. Volume 2.Document426 pagesHolmes. The Age of Justinian and Theodora. July 1905. Volume 2.Patrologia Latina, Graeca et Orientalis100% (1)

- Gandhi and National MovementDocument30 pagesGandhi and National MovementArun kumar SethiNo ratings yet

- Application Form - PLO AMP - County Reps and AmbassadorsDocument6 pagesApplication Form - PLO AMP - County Reps and AmbassadorsLazarus Kadett Ndivayele100% (1)

- Code of Practice On ConsultationDocument16 pagesCode of Practice On Consultationaeo9898No ratings yet

- Ch.3: Powers and Functions of Administrative Agencies A. in GeneralDocument8 pagesCh.3: Powers and Functions of Administrative Agencies A. in GeneralNalule Peace KNo ratings yet

- Government Finance: Taxation in The United States United States Federal BudgetDocument7 pagesGovernment Finance: Taxation in The United States United States Federal BudgetKatt RinaNo ratings yet

- Asnake InternshipDocument36 pagesAsnake Internshipkassahungedefaye3120% (1)

- Electronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationDocument10 pagesElectronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationStan J. CaterboneNo ratings yet

- P&R AnalysisDocument29 pagesP&R Analysiscontact.xinanneNo ratings yet

- Accounting Hawk - LawDocument24 pagesAccounting Hawk - LawClaire BarbaNo ratings yet

- A5 - Fringe Benefit TaxationDocument3 pagesA5 - Fringe Benefit TaxationJomer FernandezNo ratings yet

- AT.3403 - Risk-Based FS Audit ProcessDocument5 pagesAT.3403 - Risk-Based FS Audit ProcessMonica GarciaNo ratings yet

- Liham - Pahintulot: Republic of The Philippines Department of Education Schools Division of PalawanDocument12 pagesLiham - Pahintulot: Republic of The Philippines Department of Education Schools Division of PalawanMarbert GarganzaNo ratings yet

- Self Defense For WomenDocument16 pagesSelf Defense For WomenJoseph NithaiahNo ratings yet

- Annual Report 2017 18Document122 pagesAnnual Report 2017 18Ali AhmedNo ratings yet

- Hosea: Author and DateDocument3 pagesHosea: Author and DateWilliam Ng'ongaNo ratings yet

- The Reform Branch of The ReformationDocument2 pagesThe Reform Branch of The Reformationcristina ignacioNo ratings yet

- Plaintiffs-Appellees Vs Vs Defendant-Appellant Jose T. Sumcad Ramon B. de Los Reyes Angel IlaganDocument3 pagesPlaintiffs-Appellees Vs Vs Defendant-Appellant Jose T. Sumcad Ramon B. de Los Reyes Angel IlaganAehrold GarmaNo ratings yet

- 8071939554Document1 page8071939554Vishnu SasindranNo ratings yet

- Apple: December 11-12-2016:itpm Senior Trading Mentor Raj Malhotra Interview On Why Traders FailDocument3 pagesApple: December 11-12-2016:itpm Senior Trading Mentor Raj Malhotra Interview On Why Traders FaildenisNo ratings yet

- Aath Graphic OrganizerDocument4 pagesAath Graphic Organizerapi-438882571No ratings yet