Download as pdf or txt

You might also like

- Unit 3 Personal & Business Finance LODDocument54 pagesUnit 3 Personal & Business Finance LODAngelaNo ratings yet

- ICOF II PresentationDocument32 pagesICOF II PresentationAarambh wagh100% (1)

- Case Study 2 - Starting Right Corporation (Group 4)Document8 pagesCase Study 2 - Starting Right Corporation (Group 4)JanNo ratings yet

- Statement of Transactions: Sundaram Finance LimitedDocument1 pageStatement of Transactions: Sundaram Finance LimitedBhavin SagarNo ratings yet

- 21U 2093 H MidtermDocument14 pages21U 2093 H MidtermAkshit GoyalNo ratings yet

- Capital Market Corporate ProfileDocument40 pagesCapital Market Corporate ProfilePinank TurakhiaNo ratings yet

- Portfolio Activity Unit 3Document2 pagesPortfolio Activity Unit 3klm klm100% (1)

- Financial Statement Analysis of TataDocument32 pagesFinancial Statement Analysis of TataVISHNU SATHEESHNo ratings yet

- 03 Success of Equity Funding Deal v2 11-07-2020 AJDocument42 pages03 Success of Equity Funding Deal v2 11-07-2020 AJarunjoshi12345No ratings yet

- Understanding Private Equity.: 70 W. Chippewa Street, Suite 500, Buffalo, NY 14202 716.566.2900Document17 pagesUnderstanding Private Equity.: 70 W. Chippewa Street, Suite 500, Buffalo, NY 14202 716.566.2900Dharmik SolankiNo ratings yet

- Guide To Project Reports, Project Appraisal & Project FinanceDocument26 pagesGuide To Project Reports, Project Appraisal & Project FinanceSALONI GOYALNo ratings yet

- Basic Corporate FinanceDocument36 pagesBasic Corporate FinanceGirish BhangaleNo ratings yet

- 1.1 Company Profile 1.2 Brief Study of Equity ProductsDocument67 pages1.1 Company Profile 1.2 Brief Study of Equity ProductsRudra SharmaNo ratings yet

- MDLY 4Q19 Investor Presentation v3Document21 pagesMDLY 4Q19 Investor Presentation v3Dan NadNo ratings yet

- Investment Banking: Summers PreparationDocument31 pagesInvestment Banking: Summers PreparationManu JanardananNo ratings yet

- CFLecture1 2notesDocument30 pagesCFLecture1 2notesYashveer SinghNo ratings yet

- Venture CapitalDocument42 pagesVenture CapitalKellaNo ratings yet

- Scalene Company ProfileDocument13 pagesScalene Company Profiledarjimulchand77No ratings yet

- HDFC LTD. MBA Interview QuestiomDocument14 pagesHDFC LTD. MBA Interview QuestiomRohitNo ratings yet

- Financing The New VentureDocument46 pagesFinancing The New Venturearchanasingh22100% (5)

- Saratoga Investor Relation Presentation 9M19 Final - PublicDocument15 pagesSaratoga Investor Relation Presentation 9M19 Final - Publicsigitsutoko8765No ratings yet

- W2 WCorporateDocument14 pagesW2 WCorporateWay2 WealthNo ratings yet

- SIP Presentation On AU Small Finance BankDocument13 pagesSIP Presentation On AU Small Finance BankMadhurNo ratings yet

- Financial ManagementDocument23 pagesFinancial ManagementRiad ChowdhuryNo ratings yet

- B&A ProfileDocument4 pagesB&A ProfileHittMan BajgainNo ratings yet

- Scott Droney - Financing Start-Up and GrowthDocument40 pagesScott Droney - Financing Start-Up and GrowthScott DroneyNo ratings yet

- Corporate Finance: Lecture Note Packet 2 Capital Structure, Dividend Policy & ValuationDocument246 pagesCorporate Finance: Lecture Note Packet 2 Capital Structure, Dividend Policy & ValuationKanchan VarshneyNo ratings yet

- IB - Lecture 1Document42 pagesIB - Lecture 1hoang phuongthao25No ratings yet

- Presentation 5Document27 pagesPresentation 5surendra jaiswalNo ratings yet

- On Debt MarketsDocument73 pagesOn Debt MarketsrashmiNo ratings yet

- Leverage Capital Group - ProfileDocument23 pagesLeverage Capital Group - Profileanon_601430920No ratings yet

- Slide 1Document24 pagesSlide 1Akash SinghNo ratings yet

- Private Equity Overview 3Document22 pagesPrivate Equity Overview 3Dương Thị Lệ QuyênNo ratings yet

- Introduction To Accounting Part 1Document45 pagesIntroduction To Accounting Part 1Катерина ГузманNo ratings yet

- BCK Chapter4 S2 and Ch5 S1Document63 pagesBCK Chapter4 S2 and Ch5 S1krishnaaravindeNo ratings yet

- Jm-Financial-Ltd ProspectusDocument39 pagesJm-Financial-Ltd Prospectusvishakha chaudharyNo ratings yet

- Ranjeet Ranjan2Document23 pagesRanjeet Ranjan2Ranjeet RanjanNo ratings yet

- Startup FundingDocument17 pagesStartup FundingAftab AlamNo ratings yet

- Private EquityDocument9 pagesPrivate Equitysv798dctq9No ratings yet

- UNIT V - VentureexitstrategyDocument23 pagesUNIT V - Ventureexitstrategymevitsn6No ratings yet

- Introduction To Financial AccountingDocument4 pagesIntroduction To Financial AccountingDee soniNo ratings yet

- 01 Fin - Introduction To Financial ManagementDocument19 pages01 Fin - Introduction To Financial Managementshahin shekhNo ratings yet

- Presentation 2 - The Overview of Corporate Finance (Final)Document24 pagesPresentation 2 - The Overview of Corporate Finance (Final)sanjuladasanNo ratings yet

- U E V C /PE: Nderstanding Quity Enture ApitalDocument24 pagesU E V C /PE: Nderstanding Quity Enture ApitalSudhanyu VeldurthyNo ratings yet

- Intermediate Accounting: The Canadian Financial Reporting EnvironmentDocument35 pagesIntermediate Accounting: The Canadian Financial Reporting EnvironmentashleyalicerogersNo ratings yet

- Private Equity Part 1 - LongDocument45 pagesPrivate Equity Part 1 - LongLinh Linh NguyễnNo ratings yet

- Business Plan ReferenceDocument18 pagesBusiness Plan ReferenceAditya KothiwalNo ratings yet

- Venture Capital in Developing Countries: Challenges: DR - Akhil Goyal Nims University-IMCDocument22 pagesVenture Capital in Developing Countries: Challenges: DR - Akhil Goyal Nims University-IMCAKHIL GOYALNo ratings yet

- Lesson 4 - Financing For EntrepreneursDocument42 pagesLesson 4 - Financing For EntrepreneursNazir NasarudiinNo ratings yet

- Cornett Finance 5e Chapter 01Document33 pagesCornett Finance 5e Chapter 01Lu LiNo ratings yet

- Chapter 14Document32 pagesChapter 14erteyNo ratings yet

- Redit Ating AgenciesDocument44 pagesRedit Ating AgencieschumbavambaNo ratings yet

- Unit-1 Important Role of Capital MarketsDocument17 pagesUnit-1 Important Role of Capital Marketsshunlae37No ratings yet

- Econ 371 Business Finance 1: Pirapa TharmalingamDocument26 pagesEcon 371 Business Finance 1: Pirapa TharmalingamSamantha YuNo ratings yet

- Nexus8 (VN-SG Coverage)Document20 pagesNexus8 (VN-SG Coverage)Tran DuongNo ratings yet

- NPK Notes Roshan Desai Sir 5 Financial ManagementDocument43 pagesNPK Notes Roshan Desai Sir 5 Financial ManagementSatwik RaiNo ratings yet

- Presentation DCMDocument5 pagesPresentation DCMsuvarna27No ratings yet

- Introduction To Idfc AmcDocument101 pagesIntroduction To Idfc AmcSAKINAMANDSAURWALANo ratings yet

- PEVC Society - M - A 101Document15 pagesPEVC Society - M - A 101Ayan MurmuNo ratings yet

- 31 The Upscaling Business of Private EquityDocument12 pages31 The Upscaling Business of Private EquityCritiNo ratings yet

- Chandu SvitDocument85 pagesChandu SvitkhayyumNo ratings yet

- Fundamentals of Financial Management: R.P. RustagiDocument16 pagesFundamentals of Financial Management: R.P. Rustagiimranrog11No ratings yet

- Dividend Investing: Passive Income and Growth Investing for BeginnersFrom EverandDividend Investing: Passive Income and Growth Investing for BeginnersNo ratings yet

- Dividend Investing: Simplified - The Step-by-Step Guide to Make Money and Create Passive Income in the Stock Market with Dividend Stocks: Stock Market Investing for Beginners Book, #1From EverandDividend Investing: Simplified - The Step-by-Step Guide to Make Money and Create Passive Income in the Stock Market with Dividend Stocks: Stock Market Investing for Beginners Book, #1Rating: 2 out of 5 stars2/5 (1)

- Bse Sme Ipo IndexDocument4 pagesBse Sme Ipo IndexBhavin SagarNo ratings yet

- August 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsDocument10 pagesAugust 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsBhavin SagarNo ratings yet

- Qtrly - Reportq1 FY 2008 2009Document2 pagesQtrly - Reportq1 FY 2008 2009Bhavin SagarNo ratings yet

- Yap 31 1 19Document345 pagesYap 31 1 19Bhavin SagarNo ratings yet

- Nebbia Mutual NDADocument3 pagesNebbia Mutual NDABhavin SagarNo ratings yet

- Revised Market Making Agreement 31.03Document13 pagesRevised Market Making Agreement 31.03Bhavin SagarNo ratings yet

- Revised Underwriting Agreement 31.03Document14 pagesRevised Underwriting Agreement 31.03Bhavin SagarNo ratings yet

- Amalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDDocument10 pagesAmalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDBhavin SagarNo ratings yet

- List of Valuation ReportsDocument18 pagesList of Valuation ReportsBhavin SagarNo ratings yet

- Capital Reduction - Escorts LTD - GalacticoDocument10 pagesCapital Reduction - Escorts LTD - GalacticoBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- Revised RV - Draft Valuation Report - Hakuna MatataDocument11 pagesRevised RV - Draft Valuation Report - Hakuna MatataBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- 02 Corporate Orange Powerpoint Presentations 16x9 1Document13 pages02 Corporate Orange Powerpoint Presentations 16x9 1Bhavin SagarNo ratings yet

- Corporate Deck - InternationalDocument16 pagesCorporate Deck - InternationalBhavin SagarNo ratings yet

- MCA FinanicialsDocument50 pagesMCA FinanicialsBhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- Bulk DealsDocument63 pagesBulk DealsBhavin SagarNo ratings yet

- Valuation Assignement - WIPDocument2 pagesValuation Assignement - WIPBhavin SagarNo ratings yet

- Bhavin Valuation Cases For FY21Document17 pagesBhavin Valuation Cases For FY21Bhavin SagarNo ratings yet

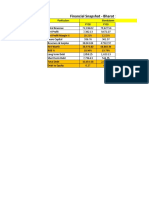

- Bharat Serums & Vaccines LTD - Financial SnapshotDocument2 pagesBharat Serums & Vaccines LTD - Financial SnapshotBhavin SagarNo ratings yet

- Bhavin - Valuation Cases - May 2021Document3 pagesBhavin - Valuation Cases - May 2021Bhavin SagarNo ratings yet

- Capital Budgeting TechniquesDocument60 pagesCapital Budgeting Techniquesaxl11No ratings yet

- Inflation Accounting: Presented ByDocument24 pagesInflation Accounting: Presented ByjasminerathodNo ratings yet

- Credit ProposalDocument43 pagesCredit ProposalndmudhosiNo ratings yet

- Bus 262 Business Finance Student Final Part HW Corona 2020Document4 pagesBus 262 Business Finance Student Final Part HW Corona 2020Olatowode OluwatosinNo ratings yet

- Business Finance - ACC501 Fall 2006 Assignment 02 SolutionDocument3 pagesBusiness Finance - ACC501 Fall 2006 Assignment 02 Solutionsamuel kebedeNo ratings yet

- Syndicate 5 - Krakatau Steel ADocument19 pagesSyndicate 5 - Krakatau Steel AEdlyn Valmai Devina SNo ratings yet

- Ind AS 102Document86 pagesInd AS 102Deepika GuptaNo ratings yet

- Chapter 23Document6 pagesChapter 23bridge1985No ratings yet

- Editor in chief,+EJBMR 1033+R300821Document7 pagesEditor in chief,+EJBMR 1033+R300821BigPalabraNo ratings yet

- No. SEBI/LAD-NRO/GN/2015-16/013 in Exercise of The Powers Conferred by Section 11Document147 pagesNo. SEBI/LAD-NRO/GN/2015-16/013 in Exercise of The Powers Conferred by Section 11Huzaifa SalimNo ratings yet

- PDF Advanced Accounting Chapter 1 DDDocument20 pagesPDF Advanced Accounting Chapter 1 DDGarp BarrocaNo ratings yet

- IAS 16 Notes.Document8 pagesIAS 16 Notes.Arsalan AliNo ratings yet

- MCQ Direct TaxDocument53 pagesMCQ Direct TaxSwetha MalladiNo ratings yet

- Econ Ex 7Document12 pagesEcon Ex 7manalastas.maridellevictoriaNo ratings yet

- HFUNDSDocument1 pageHFUNDSHernán CornejoNo ratings yet

- Vce Final Report - Vardhan Consulting EngineersDocument18 pagesVce Final Report - Vardhan Consulting EngineersHarshit AroraNo ratings yet

- Angel Investor List - Smallbiz America CapitalDocument6 pagesAngel Investor List - Smallbiz America CapitalJohn BanaskiNo ratings yet

- FA1 BPP Chapter 2 Assets, Liabilities & Accounting EquationDocument19 pagesFA1 BPP Chapter 2 Assets, Liabilities & Accounting EquationS RaihanNo ratings yet

- Consolated Balance Sheet: Advance Accounting-II (Chapter-3.4)Document8 pagesConsolated Balance Sheet: Advance Accounting-II (Chapter-3.4)Md Shah AlamNo ratings yet

- Bond ValuationDocument15 pagesBond Valuationrana ahmedNo ratings yet

- PIMCO ETFs ISS - Smart PassiveDocument4 pagesPIMCO ETFs ISS - Smart Passivefreebanker777741No ratings yet

- Chapter 9 PDFDocument29 pagesChapter 9 PDFYhunie Nhita Itha50% (2)

- Pi 13 Lampiran Peta Okupasi Bidang Logistik Dan Supply ChainDocument81 pagesPi 13 Lampiran Peta Okupasi Bidang Logistik Dan Supply ChainZeo BentNo ratings yet

- NHPC 3Document49 pagesNHPC 3Hitesh Mittal100% (1)

- ThesisDocument72 pagesThesisRaja SekharNo ratings yet

- Financial Management K45Document4 pagesFinancial Management K45Nguyễn LâmNo ratings yet

- FINC521Document20 pagesFINC521Ayushi GargNo ratings yet