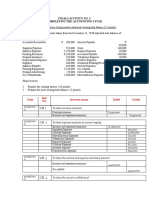

Net 57,000 Date (5.II.e)

Net 57,000 Date (5.II.e)

You might also like

- WuposReceipt PDFDocument1 pageWuposReceipt PDFParvej Ansari100% (1)

- Quiz 9 FinacrDocument9 pagesQuiz 9 FinacrJen Ner100% (5)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Answers and Solutions For Business Combination Chapter 3 and Chapter 4Document4 pagesAnswers and Solutions For Business Combination Chapter 3 and Chapter 4Kyree Vlade0% (1)

- CH Proble 3 8 PDFDocument29 pagesCH Proble 3 8 PDFYogun Bayona100% (1)

- Far Eastern University: Post-Test1-Cash and Cash EquivalentsDocument9 pagesFar Eastern University: Post-Test1-Cash and Cash EquivalentschristineNo ratings yet

- Answer 1Document7 pagesAnswer 1Mylene HeragaNo ratings yet

- AC - Acctg Gov Quiz 01 SolutionsDocument12 pagesAC - Acctg Gov Quiz 01 SolutionsErjohn Papa100% (1)

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- Group 8 Audit of Insurance Industry Including HMODocument16 pagesGroup 8 Audit of Insurance Industry Including HMOKyree VladeNo ratings yet

- BUAd 801Document47 pagesBUAd 801Adetunji Taiwo100% (1)

- Jones Electrical DistributionDocument5 pagesJones Electrical DistributionAsif AliNo ratings yet

- SOLUTION Illustrative Problem Government Accounting ProcessDocument7 pagesSOLUTION Illustrative Problem Government Accounting ProcessVicente, Liza Mae C.No ratings yet

- Illustrative Problem Basic RecordingDocument36 pagesIllustrative Problem Basic RecordingLeila OuanoNo ratings yet

- Annex J - Special Account - DomesticDocument4 pagesAnnex J - Special Account - Domesticjaymark canayaNo ratings yet

- Government AccountingDocument3 pagesGovernment Accountingchibi.otaku.neesanNo ratings yet

- Je Homework GovaccDocument6 pagesJe Homework GovaccEizzel SamsonNo ratings yet

- Ramos Acctg 2200 Lab3Document2 pagesRamos Acctg 2200 Lab3Danica RamosNo ratings yet

- Akuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Document2 pagesAkuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Muhamad Rizal DinyatNo ratings yet

- PDF Review Materials For Finals Q - CompressDocument20 pagesPDF Review Materials For Finals Q - CompressAndrea Florence Guy Vidal100% (1)

- Activity #6Document20 pagesActivity #6JEWELL ANN PENARANDANo ratings yet

- Annex H Regular Agency FundDocument125 pagesAnnex H Regular Agency FundKelvin CaldinoNo ratings yet

- FA1 Financial StatementsDocument5 pagesFA1 Financial StatementsamirNo ratings yet

- Jay Cesar System Developer Worksheet DECEMBER 31 2019 Unadjusted Trial Balance REFDocument4 pagesJay Cesar System Developer Worksheet DECEMBER 31 2019 Unadjusted Trial Balance REFAdam CuencaNo ratings yet

- Statement of CashflowDocument9 pagesStatement of CashflowOwen Lustre50% (2)

- Retained Income Fund: Illustrative EntriesDocument2 pagesRetained Income Fund: Illustrative EntriesKelvin CaldinoNo ratings yet

- Annex L - Retained IncomeDocument2 pagesAnnex L - Retained IncomeMark Ronnier VedañaNo ratings yet

- Annex L of GamDocument7 pagesAnnex L of GamKelvin CaldinoNo ratings yet

- Statement of Cash FlowDocument2 pagesStatement of Cash FlowHaidee Flavier Sabido100% (1)

- Exam OldQuestionPaper14072023010719Document39 pagesExam OldQuestionPaper14072023010719Ashish KumarNo ratings yet

- Illustrative Entries For Regular Agency FundDocument24 pagesIllustrative Entries For Regular Agency FundYixing XingNo ratings yet

- Ifa 4Document15 pagesIfa 4Kyrelle Mae LozadaNo ratings yet

- Toaz - Info Prelim Midterm PRDocument98 pagesToaz - Info Prelim Midterm PRClandestine SoulNo ratings yet

- QUIZ 9 fINACRDocument9 pagesQUIZ 9 fINACRJen NerNo ratings yet

- Local Media6884512623317631833Document29 pagesLocal Media6884512623317631833Yogun BayonaNo ratings yet

- CA Foundation Accounts A MTP 2 June 2023Document12 pagesCA Foundation Accounts A MTP 2 June 2023Vranda RastogiNo ratings yet

- 9420 - Government Accounting ManualDocument8 pages9420 - Government Accounting ManualShannen D. CalimagNo ratings yet

- Module 7 GAM IllustrationDocument21 pagesModule 7 GAM IllustrationElla EspenesinNo ratings yet

- Exercises Lesson - 3 - 0809 PDFDocument11 pagesExercises Lesson - 3 - 0809 PDFkashijee40No ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- 9024 - Government Accounting ManualDocument8 pages9024 - Government Accounting ManualAljur SalamedaNo ratings yet

- LQ 1 Sec C Solution PDFDocument14 pagesLQ 1 Sec C Solution PDFmaria evangelistaNo ratings yet

- Week 4 P4.21 Modified Question PDFDocument1 pageWeek 4 P4.21 Modified Question PDFalexandraNo ratings yet

- DAA5014 Tutorial Topic 3 QuestionsDocument4 pagesDAA5014 Tutorial Topic 3 QuestionstyrenshunhengNo ratings yet

- ACCT 1005 - Worksheet - 2Document12 pagesACCT 1005 - Worksheet - 2Rick SimmsNo ratings yet

- CH Chapter 3Document2 pagesCH Chapter 3Joseph NarizNo ratings yet

- Activity 2Document5 pagesActivity 2Ashley Timbreza BetitaNo ratings yet

- Service BusinessDocument12 pagesService BusinessRemalyn AmmakNo ratings yet

- Examination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsDocument3 pagesExamination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- Accounting Cycle SimulationDocument15 pagesAccounting Cycle SimulationMc Clent CervantesNo ratings yet

- Particulars Debit Credit: © The Institute of Chartered Accountants of IndiaDocument46 pagesParticulars Debit Credit: © The Institute of Chartered Accountants of IndiaOveyaaNo ratings yet

- MTP 15 28 Answers 1703566022Document11 pagesMTP 15 28 Answers 1703566022nilesh.nkj1325No ratings yet

- FR111. FFA Solution CMA January 2022 ExaminationDocument5 pagesFR111. FFA Solution CMA January 2022 ExaminationMohammed Javed UddinNo ratings yet

- Problem 2 - AccountingcyleDocument13 pagesProblem 2 - AccountingcyleGio BurburanNo ratings yet

- Tum CompanyDocument4 pagesTum CompanyNguyen My Khanh (K18 HCM)No ratings yet

- PRACITCE MATERIAL for Lecture#5,6,7Document21 pagesPRACITCE MATERIAL for Lecture#5,6,7usama.50844No ratings yet

- PART B - SET A (Odd Groups - 1,3,5,7,9)Document4 pagesPART B - SET A (Odd Groups - 1,3,5,7,9)ngocanhhlee.11No ratings yet

- Solution Fin Accting FundamentalsDocument7 pagesSolution Fin Accting Fundamentalsabhaymvyas1144No ratings yet

- Company Final Accounts: Solutions To Assignment ProblemsDocument9 pagesCompany Final Accounts: Solutions To Assignment ProblemsPalavesa KrishnanNo ratings yet

- Financial Accounting and Reporting Problems Freebie PDFDocument46 pagesFinancial Accounting and Reporting Problems Freebie PDFC/PVT DAET, SHAINA JOYNo ratings yet

- Updates - Midterm Lspu ExamDocument6 pagesUpdates - Midterm Lspu ExamAngelo HilomaNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Question and Answer of Group 8 - Audit of Insurance Industry Including HMODocument32 pagesQuestion and Answer of Group 8 - Audit of Insurance Industry Including HMOKyree VladeNo ratings yet

- Overall Role and ResponsibilityDocument9 pagesOverall Role and ResponsibilityKyree VladeNo ratings yet

- De Vera, Kyle (AP1 - Assign3 - Inventories)Document3 pagesDe Vera, Kyle (AP1 - Assign3 - Inventories)Kyree VladeNo ratings yet

- Pamantasan NG Lungsod NG Pasig: Test I - IdentificationDocument2 pagesPamantasan NG Lungsod NG Pasig: Test I - IdentificationKyree VladeNo ratings yet

- Group 8 Audit Plan of Insurance Company ManulifeDocument19 pagesGroup 8 Audit Plan of Insurance Company ManulifeKyree VladeNo ratings yet

- Audit of Insurance Industry Including Hmo: Specialized IndustriesDocument47 pagesAudit of Insurance Industry Including Hmo: Specialized IndustriesKyree VladeNo ratings yet

- Chapter 4 Revenues and Other ReceiptsDocument10 pagesChapter 4 Revenues and Other ReceiptsKyree VladeNo ratings yet

- Dokumento Nang PagtitiponDocument3 pagesDokumento Nang PagtitiponKyree VladeNo ratings yet

- ShiftDocument2 pagesShiftKyree VladeNo ratings yet

- This Study Resource Was: The Expenditure CycleDocument2 pagesThis Study Resource Was: The Expenditure CycleKyree VladeNo ratings yet

- De Vera, Kyle C. (StraMa - Webinar)Document3 pagesDe Vera, Kyle C. (StraMa - Webinar)Kyree VladeNo ratings yet

- KYLE DE VERA BSA-3A (Auditing & Assurance in SPCL Industries MT Exam) AnswersDocument3 pagesKYLE DE VERA BSA-3A (Auditing & Assurance in SPCL Industries MT Exam) AnswersKyree Vlade100% (1)

- JowanDocument3 pagesJowanKyree VladeNo ratings yet

- De Vera, Kyle (Activity - Pearson R)Document2 pagesDe Vera, Kyle (Activity - Pearson R)Kyree VladeNo ratings yet

- Based On The Movie JOBS and On The Lessons Learned So Far, What Do You Think Is The Biggest Stumbling Block For APPLE?Document2 pagesBased On The Movie JOBS and On The Lessons Learned So Far, What Do You Think Is The Biggest Stumbling Block For APPLE?Kyree VladeNo ratings yet

- JOBS2013 - Movie Analysis (Kyle de Vera BSA-3A)Document2 pagesJOBS2013 - Movie Analysis (Kyle de Vera BSA-3A)Kyree VladeNo ratings yet

- Principles of TeachingDocument2 pagesPrinciples of TeachingKyree VladeNo ratings yet

- Retrieved November 18, 2019 From: BibliographyDocument3 pagesRetrieved November 18, 2019 From: BibliographyKyree VladeNo ratings yet

- Information Systems For Managers - N (1A) UpdatedDocument11 pagesInformation Systems For Managers - N (1A) UpdatedIsha TilokaniNo ratings yet

- TXN 04122020 23092020 04122020 NatWestDocument8 pagesTXN 04122020 23092020 04122020 NatWestwendyclaridg75No ratings yet

- Welcome Letter 111306743Document6 pagesWelcome Letter 111306743Tabe alamNo ratings yet

- Corporateprofile 230312 134230 PDFDocument18 pagesCorporateprofile 230312 134230 PDFHavana RavaliarisonNo ratings yet

- Bio-Data of The Promoters / Guarantors: Annexure 1Document41 pagesBio-Data of The Promoters / Guarantors: Annexure 1Anuj NijhonNo ratings yet

- BFSI and NBFC Products and Services - Project Work IdeasDocument5 pagesBFSI and NBFC Products and Services - Project Work IdeasDivya Jayaraman100% (1)

- IFR Definitive GuideDocument257 pagesIFR Definitive Guidehussaisz100% (1)

- Challan No. Challan No. Challan No.: Account Number Account Number Account NumberDocument1 pageChallan No. Challan No. Challan No.: Account Number Account Number Account NumberwithraviNo ratings yet

- FIN619 Final ProjectDocument9 pagesFIN619 Final Projectcs619finalproject.com100% (1)

- UIIC ClaimFormDocument2 pagesUIIC ClaimFormkarthikvel80No ratings yet

- AISDocument2 pagesAISMichelle BabaNo ratings yet

- Experiment 9: Bank Database ObjectiveDocument4 pagesExperiment 9: Bank Database Objectiveprudhvi chowdaryNo ratings yet

- Functions of Bangladesh BankDocument33 pagesFunctions of Bangladesh Bankledpro100% (4)

- Mercantile Answer To BAR2017Document13 pagesMercantile Answer To BAR2017Angela CanaresNo ratings yet

- Weekly Current Affairs - May 4th WeekDocument10 pagesWeekly Current Affairs - May 4th WeekCheenaNo ratings yet

- Client Relationship Management Skills: Euromoney TrainingDocument4 pagesClient Relationship Management Skills: Euromoney Trainingrajjusingh68No ratings yet

- Cash Management Thesis PDFDocument4 pagesCash Management Thesis PDFstaceywilsonbaltimore100% (2)

- Banking 18-4-2022Document17 pagesBanking 18-4-2022KAMLESH DEWANGANNo ratings yet

- Viray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentDocument13 pagesViray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentCarren Paulet Villar CuyosNo ratings yet

- Internet Banking IntroductionDocument4 pagesInternet Banking Introductionaihjaaz a71% (7)

- Heart of Darkness Essay TopicsDocument4 pagesHeart of Darkness Essay Topicsafibzfwdkaesyf100% (2)

- Bpo201 Batlag Group6 Finmgt2201Document55 pagesBpo201 Batlag Group6 Finmgt2201Mark MercadoNo ratings yet

- CCD - Other Channels V5.1Document2 pagesCCD - Other Channels V5.1Pranay ShitoleNo ratings yet

- Jurnal Cash Flow Ke 2Document24 pagesJurnal Cash Flow Ke 2sarahNo ratings yet

- Tgpala Aicte Income Tax Programme 2015 16 UPDATEDDocument27 pagesTgpala Aicte Income Tax Programme 2015 16 UPDATEDniranjannlgNo ratings yet

- What Is HJR 192Document4 pagesWhat Is HJR 192Nikolay BotevNo ratings yet

- FacultyDocument11 pagesFacultysubhojit007No ratings yet

Download as docx, pdf, or txt

You might also like

- WuposReceipt PDFDocument1 pageWuposReceipt PDFParvej Ansari100% (1)

- Quiz 9 FinacrDocument9 pagesQuiz 9 FinacrJen Ner100% (5)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Answers and Solutions For Business Combination Chapter 3 and Chapter 4Document4 pagesAnswers and Solutions For Business Combination Chapter 3 and Chapter 4Kyree Vlade0% (1)

- CH Proble 3 8 PDFDocument29 pagesCH Proble 3 8 PDFYogun Bayona100% (1)

- Far Eastern University: Post-Test1-Cash and Cash EquivalentsDocument9 pagesFar Eastern University: Post-Test1-Cash and Cash EquivalentschristineNo ratings yet

- Answer 1Document7 pagesAnswer 1Mylene HeragaNo ratings yet

- AC - Acctg Gov Quiz 01 SolutionsDocument12 pagesAC - Acctg Gov Quiz 01 SolutionsErjohn Papa100% (1)

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- Group 8 Audit of Insurance Industry Including HMODocument16 pagesGroup 8 Audit of Insurance Industry Including HMOKyree VladeNo ratings yet

- BUAd 801Document47 pagesBUAd 801Adetunji Taiwo100% (1)

- Jones Electrical DistributionDocument5 pagesJones Electrical DistributionAsif AliNo ratings yet

- SOLUTION Illustrative Problem Government Accounting ProcessDocument7 pagesSOLUTION Illustrative Problem Government Accounting ProcessVicente, Liza Mae C.No ratings yet

- Illustrative Problem Basic RecordingDocument36 pagesIllustrative Problem Basic RecordingLeila OuanoNo ratings yet

- Annex J - Special Account - DomesticDocument4 pagesAnnex J - Special Account - Domesticjaymark canayaNo ratings yet

- Government AccountingDocument3 pagesGovernment Accountingchibi.otaku.neesanNo ratings yet

- Je Homework GovaccDocument6 pagesJe Homework GovaccEizzel SamsonNo ratings yet

- Ramos Acctg 2200 Lab3Document2 pagesRamos Acctg 2200 Lab3Danica RamosNo ratings yet

- Akuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Document2 pagesAkuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Muhamad Rizal DinyatNo ratings yet

- PDF Review Materials For Finals Q - CompressDocument20 pagesPDF Review Materials For Finals Q - CompressAndrea Florence Guy Vidal100% (1)

- Activity #6Document20 pagesActivity #6JEWELL ANN PENARANDANo ratings yet

- Annex H Regular Agency FundDocument125 pagesAnnex H Regular Agency FundKelvin CaldinoNo ratings yet

- FA1 Financial StatementsDocument5 pagesFA1 Financial StatementsamirNo ratings yet

- Jay Cesar System Developer Worksheet DECEMBER 31 2019 Unadjusted Trial Balance REFDocument4 pagesJay Cesar System Developer Worksheet DECEMBER 31 2019 Unadjusted Trial Balance REFAdam CuencaNo ratings yet

- Statement of CashflowDocument9 pagesStatement of CashflowOwen Lustre50% (2)

- Retained Income Fund: Illustrative EntriesDocument2 pagesRetained Income Fund: Illustrative EntriesKelvin CaldinoNo ratings yet

- Annex L - Retained IncomeDocument2 pagesAnnex L - Retained IncomeMark Ronnier VedañaNo ratings yet

- Annex L of GamDocument7 pagesAnnex L of GamKelvin CaldinoNo ratings yet

- Statement of Cash FlowDocument2 pagesStatement of Cash FlowHaidee Flavier Sabido100% (1)

- Exam OldQuestionPaper14072023010719Document39 pagesExam OldQuestionPaper14072023010719Ashish KumarNo ratings yet

- Illustrative Entries For Regular Agency FundDocument24 pagesIllustrative Entries For Regular Agency FundYixing XingNo ratings yet

- Ifa 4Document15 pagesIfa 4Kyrelle Mae LozadaNo ratings yet

- Toaz - Info Prelim Midterm PRDocument98 pagesToaz - Info Prelim Midterm PRClandestine SoulNo ratings yet

- QUIZ 9 fINACRDocument9 pagesQUIZ 9 fINACRJen NerNo ratings yet

- Local Media6884512623317631833Document29 pagesLocal Media6884512623317631833Yogun BayonaNo ratings yet

- CA Foundation Accounts A MTP 2 June 2023Document12 pagesCA Foundation Accounts A MTP 2 June 2023Vranda RastogiNo ratings yet

- 9420 - Government Accounting ManualDocument8 pages9420 - Government Accounting ManualShannen D. CalimagNo ratings yet

- Module 7 GAM IllustrationDocument21 pagesModule 7 GAM IllustrationElla EspenesinNo ratings yet

- Exercises Lesson - 3 - 0809 PDFDocument11 pagesExercises Lesson - 3 - 0809 PDFkashijee40No ratings yet

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- 9024 - Government Accounting ManualDocument8 pages9024 - Government Accounting ManualAljur SalamedaNo ratings yet

- LQ 1 Sec C Solution PDFDocument14 pagesLQ 1 Sec C Solution PDFmaria evangelistaNo ratings yet

- Week 4 P4.21 Modified Question PDFDocument1 pageWeek 4 P4.21 Modified Question PDFalexandraNo ratings yet

- DAA5014 Tutorial Topic 3 QuestionsDocument4 pagesDAA5014 Tutorial Topic 3 QuestionstyrenshunhengNo ratings yet

- ACCT 1005 - Worksheet - 2Document12 pagesACCT 1005 - Worksheet - 2Rick SimmsNo ratings yet

- CH Chapter 3Document2 pagesCH Chapter 3Joseph NarizNo ratings yet

- Activity 2Document5 pagesActivity 2Ashley Timbreza BetitaNo ratings yet

- Service BusinessDocument12 pagesService BusinessRemalyn AmmakNo ratings yet

- Examination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsDocument3 pagesExamination Question and Answers, Set C (Problem Solving), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- Accounting Cycle SimulationDocument15 pagesAccounting Cycle SimulationMc Clent CervantesNo ratings yet

- Particulars Debit Credit: © The Institute of Chartered Accountants of IndiaDocument46 pagesParticulars Debit Credit: © The Institute of Chartered Accountants of IndiaOveyaaNo ratings yet

- MTP 15 28 Answers 1703566022Document11 pagesMTP 15 28 Answers 1703566022nilesh.nkj1325No ratings yet

- FR111. FFA Solution CMA January 2022 ExaminationDocument5 pagesFR111. FFA Solution CMA January 2022 ExaminationMohammed Javed UddinNo ratings yet

- Problem 2 - AccountingcyleDocument13 pagesProblem 2 - AccountingcyleGio BurburanNo ratings yet

- Tum CompanyDocument4 pagesTum CompanyNguyen My Khanh (K18 HCM)No ratings yet

- PRACITCE MATERIAL for Lecture#5,6,7Document21 pagesPRACITCE MATERIAL for Lecture#5,6,7usama.50844No ratings yet

- PART B - SET A (Odd Groups - 1,3,5,7,9)Document4 pagesPART B - SET A (Odd Groups - 1,3,5,7,9)ngocanhhlee.11No ratings yet

- Solution Fin Accting FundamentalsDocument7 pagesSolution Fin Accting Fundamentalsabhaymvyas1144No ratings yet

- Company Final Accounts: Solutions To Assignment ProblemsDocument9 pagesCompany Final Accounts: Solutions To Assignment ProblemsPalavesa KrishnanNo ratings yet

- Financial Accounting and Reporting Problems Freebie PDFDocument46 pagesFinancial Accounting and Reporting Problems Freebie PDFC/PVT DAET, SHAINA JOYNo ratings yet

- Updates - Midterm Lspu ExamDocument6 pagesUpdates - Midterm Lspu ExamAngelo HilomaNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Question and Answer of Group 8 - Audit of Insurance Industry Including HMODocument32 pagesQuestion and Answer of Group 8 - Audit of Insurance Industry Including HMOKyree VladeNo ratings yet

- Overall Role and ResponsibilityDocument9 pagesOverall Role and ResponsibilityKyree VladeNo ratings yet

- De Vera, Kyle (AP1 - Assign3 - Inventories)Document3 pagesDe Vera, Kyle (AP1 - Assign3 - Inventories)Kyree VladeNo ratings yet

- Pamantasan NG Lungsod NG Pasig: Test I - IdentificationDocument2 pagesPamantasan NG Lungsod NG Pasig: Test I - IdentificationKyree VladeNo ratings yet

- Group 8 Audit Plan of Insurance Company ManulifeDocument19 pagesGroup 8 Audit Plan of Insurance Company ManulifeKyree VladeNo ratings yet

- Audit of Insurance Industry Including Hmo: Specialized IndustriesDocument47 pagesAudit of Insurance Industry Including Hmo: Specialized IndustriesKyree VladeNo ratings yet

- Chapter 4 Revenues and Other ReceiptsDocument10 pagesChapter 4 Revenues and Other ReceiptsKyree VladeNo ratings yet

- Dokumento Nang PagtitiponDocument3 pagesDokumento Nang PagtitiponKyree VladeNo ratings yet

- ShiftDocument2 pagesShiftKyree VladeNo ratings yet

- This Study Resource Was: The Expenditure CycleDocument2 pagesThis Study Resource Was: The Expenditure CycleKyree VladeNo ratings yet

- De Vera, Kyle C. (StraMa - Webinar)Document3 pagesDe Vera, Kyle C. (StraMa - Webinar)Kyree VladeNo ratings yet

- KYLE DE VERA BSA-3A (Auditing & Assurance in SPCL Industries MT Exam) AnswersDocument3 pagesKYLE DE VERA BSA-3A (Auditing & Assurance in SPCL Industries MT Exam) AnswersKyree Vlade100% (1)

- JowanDocument3 pagesJowanKyree VladeNo ratings yet

- De Vera, Kyle (Activity - Pearson R)Document2 pagesDe Vera, Kyle (Activity - Pearson R)Kyree VladeNo ratings yet

- Based On The Movie JOBS and On The Lessons Learned So Far, What Do You Think Is The Biggest Stumbling Block For APPLE?Document2 pagesBased On The Movie JOBS and On The Lessons Learned So Far, What Do You Think Is The Biggest Stumbling Block For APPLE?Kyree VladeNo ratings yet

- JOBS2013 - Movie Analysis (Kyle de Vera BSA-3A)Document2 pagesJOBS2013 - Movie Analysis (Kyle de Vera BSA-3A)Kyree VladeNo ratings yet

- Principles of TeachingDocument2 pagesPrinciples of TeachingKyree VladeNo ratings yet

- Retrieved November 18, 2019 From: BibliographyDocument3 pagesRetrieved November 18, 2019 From: BibliographyKyree VladeNo ratings yet

- Information Systems For Managers - N (1A) UpdatedDocument11 pagesInformation Systems For Managers - N (1A) UpdatedIsha TilokaniNo ratings yet

- TXN 04122020 23092020 04122020 NatWestDocument8 pagesTXN 04122020 23092020 04122020 NatWestwendyclaridg75No ratings yet

- Welcome Letter 111306743Document6 pagesWelcome Letter 111306743Tabe alamNo ratings yet

- Corporateprofile 230312 134230 PDFDocument18 pagesCorporateprofile 230312 134230 PDFHavana RavaliarisonNo ratings yet

- Bio-Data of The Promoters / Guarantors: Annexure 1Document41 pagesBio-Data of The Promoters / Guarantors: Annexure 1Anuj NijhonNo ratings yet

- BFSI and NBFC Products and Services - Project Work IdeasDocument5 pagesBFSI and NBFC Products and Services - Project Work IdeasDivya Jayaraman100% (1)

- IFR Definitive GuideDocument257 pagesIFR Definitive Guidehussaisz100% (1)

- Challan No. Challan No. Challan No.: Account Number Account Number Account NumberDocument1 pageChallan No. Challan No. Challan No.: Account Number Account Number Account NumberwithraviNo ratings yet

- FIN619 Final ProjectDocument9 pagesFIN619 Final Projectcs619finalproject.com100% (1)

- UIIC ClaimFormDocument2 pagesUIIC ClaimFormkarthikvel80No ratings yet

- AISDocument2 pagesAISMichelle BabaNo ratings yet

- Experiment 9: Bank Database ObjectiveDocument4 pagesExperiment 9: Bank Database Objectiveprudhvi chowdaryNo ratings yet

- Functions of Bangladesh BankDocument33 pagesFunctions of Bangladesh Bankledpro100% (4)

- Mercantile Answer To BAR2017Document13 pagesMercantile Answer To BAR2017Angela CanaresNo ratings yet

- Weekly Current Affairs - May 4th WeekDocument10 pagesWeekly Current Affairs - May 4th WeekCheenaNo ratings yet

- Client Relationship Management Skills: Euromoney TrainingDocument4 pagesClient Relationship Management Skills: Euromoney Trainingrajjusingh68No ratings yet

- Cash Management Thesis PDFDocument4 pagesCash Management Thesis PDFstaceywilsonbaltimore100% (2)

- Banking 18-4-2022Document17 pagesBanking 18-4-2022KAMLESH DEWANGANNo ratings yet

- Viray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentDocument13 pagesViray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentCarren Paulet Villar CuyosNo ratings yet

- Internet Banking IntroductionDocument4 pagesInternet Banking Introductionaihjaaz a71% (7)

- Heart of Darkness Essay TopicsDocument4 pagesHeart of Darkness Essay Topicsafibzfwdkaesyf100% (2)

- Bpo201 Batlag Group6 Finmgt2201Document55 pagesBpo201 Batlag Group6 Finmgt2201Mark MercadoNo ratings yet

- CCD - Other Channels V5.1Document2 pagesCCD - Other Channels V5.1Pranay ShitoleNo ratings yet

- Jurnal Cash Flow Ke 2Document24 pagesJurnal Cash Flow Ke 2sarahNo ratings yet

- Tgpala Aicte Income Tax Programme 2015 16 UPDATEDDocument27 pagesTgpala Aicte Income Tax Programme 2015 16 UPDATEDniranjannlgNo ratings yet

- What Is HJR 192Document4 pagesWhat Is HJR 192Nikolay BotevNo ratings yet

- FacultyDocument11 pagesFacultysubhojit007No ratings yet