Download as xlsx, pdf, or txt

You might also like

- Shrieves Casting Company Chapter 12 (11ed-11) Cash Flow Estimation and Risk AnalysisDocument12 pagesShrieves Casting Company Chapter 12 (11ed-11) Cash Flow Estimation and Risk AnalysisHayat Omer Malik100% (1)

- Chapter 10 Impairment of Assets (Pas 36)Document11 pagesChapter 10 Impairment of Assets (Pas 36)Krissa Mae Longos100% (1)

- AccountingDocument12 pagesAccountingpearl042008No ratings yet

- Intermediate Accounting CASEDocument12 pagesIntermediate Accounting CASERashimNo ratings yet

- Case Study - Nike IncDocument6 pagesCase Study - Nike Inc80starboy80No ratings yet

- Assignment 2Document25 pagesAssignment 2Jiaxi WNo ratings yet

- Reviewer Financial ManagementDocument7 pagesReviewer Financial Managementldeguzman210000000953No ratings yet

- Bodie10ce SM CH19Document12 pagesBodie10ce SM CH19beadand1No ratings yet

- Practice SetDocument10 pagesPractice Setkaeya alberichNo ratings yet

- Airjet Best Parts Financial Analysis: Capital Budgeting For A New MachineDocument5 pagesAirjet Best Parts Financial Analysis: Capital Budgeting For A New Machinedaijamaija1No ratings yet

- Dwnload Full Foundations of Financial Management Canadian 10th Edition Block Solutions Manual PDFDocument20 pagesDwnload Full Foundations of Financial Management Canadian 10th Edition Block Solutions Manual PDFfruitfulbrawnedom7er4100% (14)

- Solutions Chapter 24Document5 pagesSolutions Chapter 24Avi SeligNo ratings yet

- Full Download Solution Manual For Analysis For Financial Management 12th Edition PDF Full ChapterDocument36 pagesFull Download Solution Manual For Analysis For Financial Management 12th Edition PDF Full Chapterbuoyala6sjff100% (21)

- Solution Manual For Analysis For Financial Management 12th EditionDocument21 pagesSolution Manual For Analysis For Financial Management 12th Editionmissitcantaboc6sp100% (46)

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- DepreciationDocument8 pagesDepreciationfarhadcse30No ratings yet

- AFM - Mock Exam Answers - Dec18Document21 pagesAFM - Mock Exam Answers - Dec18David LeeNo ratings yet

- Modjo Comprehensive FM AssignmentDocument4 pagesModjo Comprehensive FM Assignmentnatnaelbtamu haNo ratings yet

- What Is DepreciationDocument5 pagesWhat Is DepreciationFaisal NadeemNo ratings yet

- SBR Assigment-Liam'sDocument7 pagesSBR Assigment-Liam'sbuls eyeNo ratings yet

- Final Statement Assessment 1Document7 pagesFinal Statement Assessment 1AssignemntNo ratings yet

- Financial Acct II - Section IDocument13 pagesFinancial Acct II - Section I66 SACHINNo ratings yet

- Financial Analysis Report of Park Hotels and Resort For The Year 2018Document13 pagesFinancial Analysis Report of Park Hotels and Resort For The Year 2018Muhammad HarisNo ratings yet

- Capital BugetingDocument6 pagesCapital BugetingMichael ReyesNo ratings yet

- Financial Accounting Theory and Analysis Text and Cases 12th Edition Schroeder Solutions ManualDocument21 pagesFinancial Accounting Theory and Analysis Text and Cases 12th Edition Schroeder Solutions Manualtryphenakhuongbz4rn100% (32)

- Mock 2 Section C.thapelo MolibeliDocument17 pagesMock 2 Section C.thapelo MolibeliLerato SelloNo ratings yet

- Cash Flow Estimation & Risk AnalysisDocument6 pagesCash Flow Estimation & Risk AnalysisShreenivasan K AnanthanNo ratings yet

- Management AccountingDocument101 pagesManagement AccountingKartikNo ratings yet

- Fae3e SM ch12Document27 pagesFae3e SM ch12JarkeeNo ratings yet

- Solutions To QuestionsDocument16 pagesSolutions To QuestionsAndi Advan Jr.No ratings yet

- Bbap18011158 Fin 2013 (WM) Financial ManagementDocument8 pagesBbap18011158 Fin 2013 (WM) Financial ManagementRaynold RaphaelNo ratings yet

- Chapter 13 - SeatworkDocument8 pagesChapter 13 - SeatworkNicole ClaireNo ratings yet

- Module 6 AND 7 AnswerDocument30 pagesModule 6 AND 7 AnswerSophia DayaoNo ratings yet

- Mercury Athletics Footwear Case: B52.FIN.448 Advanced Financial Management Professor Roni KisinDocument7 pagesMercury Athletics Footwear Case: B52.FIN.448 Advanced Financial Management Professor Roni KisinFaith AllenNo ratings yet

- Lockheed Tri Star and Capital Budgeting Case Analysis: ProfessorDocument8 pagesLockheed Tri Star and Capital Budgeting Case Analysis: ProfessorlicservernoidaNo ratings yet

- Allied Food ProductsDocument5 pagesAllied Food Productsbusinessdoctor23No ratings yet

- BPP Revision Kit Sample Answers 1Document8 pagesBPP Revision Kit Sample Answers 1Kian TuckNo ratings yet

- Question 1-: A. Calculation of Eoq For Hard PlasticDocument6 pagesQuestion 1-: A. Calculation of Eoq For Hard PlasticAdesina OlufemiNo ratings yet

- Jun 2003 SolutionsDocument10 pagesJun 2003 SolutionsJosh LebetkinNo ratings yet

- Capital Investment Analysis: Class Discussion QuestionsDocument44 pagesCapital Investment Analysis: Class Discussion QuestionsMoko ajaNo ratings yet

- Chapter 10 Impairment of Assets (Pas 36)Document11 pagesChapter 10 Impairment of Assets (Pas 36)Princess TaoinganNo ratings yet

- Advanced Financial AccountingDocument7 pagesAdvanced Financial AccountingRupesh MaharjanNo ratings yet

- FM SD21 AsDocument6 pagesFM SD21 AsRamcharan KeshavNo ratings yet

- Valuation: Aswath DamodaranDocument100 pagesValuation: Aswath DamodaranAsif IqbalNo ratings yet

- Present ValueDocument8 pagesPresent ValueFarrukhsgNo ratings yet

- Investment Appraisal 1Document13 pagesInvestment Appraisal 1Arslan ArifNo ratings yet

- Lecture 5. Depreciation, Bad Debts, Provision For Doubtful DebtsDocument32 pagesLecture 5. Depreciation, Bad Debts, Provision For Doubtful DebtsazizbektokhirbekovNo ratings yet

- 2 Cash - Flows QuestionsDocument4 pages2 Cash - Flows QuestionsAndré BravoNo ratings yet

- Final Exam Financial Management NameDocument6 pagesFinal Exam Financial Management NameInsatiable LifeNo ratings yet

- MODADV3 Quiz 3 - 12062021Document6 pagesMODADV3 Quiz 3 - 12062021Maha Bianca Charisma CastroNo ratings yet

- Soutions To Practice Problems For Modules 1 & 2Document17 pagesSoutions To Practice Problems For Modules 1 & 2b1234naNo ratings yet

- PDF NotesDocument7 pagesPDF NotesBinoy TrevadiaNo ratings yet

- Fa4e SM Ch08Document20 pagesFa4e SM Ch08michaelkwok1100% (1)

- 5, 6 & 7 Capital BudgetingDocument42 pages5, 6 & 7 Capital BudgetingNaman AgarwalNo ratings yet

- Faculty Name - Sandeep Bhatiya: Financial Accounting FundamentalDocument34 pagesFaculty Name - Sandeep Bhatiya: Financial Accounting FundamentalNamrata PrasadNo ratings yet

- Financial Management in The Sport Industry 2nd Brown Solution ManualDocument10 pagesFinancial Management in The Sport Industry 2nd Brown Solution Manualkimberlyfernandezfgzsediptj100% (50)

- Impairment of AssetDocument10 pagesImpairment of AssetJerome_JadeNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

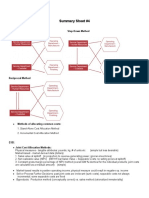

- Summary Sheet #4: Direct Method Step-Down MethodDocument5 pagesSummary Sheet #4: Direct Method Step-Down MethodJiaxi WNo ratings yet

- Summary Sheet #5Document4 pagesSummary Sheet #5Jiaxi WNo ratings yet

- Summary SheetDocument4 pagesSummary SheetJiaxi WNo ratings yet

- Assignment 3Document14 pagesAssignment 3Jiaxi WNo ratings yet

- Tax Assignment 1Document8 pagesTax Assignment 1Jiaxi WNo ratings yet

- Assignment 5Document7 pagesAssignment 5Jiaxi WNo ratings yet

- Marriott Corp PresentationDocument11 pagesMarriott Corp PresentationJiaxi WNo ratings yet

- PAWNSHOPSDocument1 pagePAWNSHOPSBianca SiguenzaNo ratings yet

- MCQ For Final Exam Functions Bank Oct 18 IIDocument27 pagesMCQ For Final Exam Functions Bank Oct 18 IISubba RaoNo ratings yet

- REXEL SA - Research Report - FinalDocument6 pagesREXEL SA - Research Report - FinalGlen BorgNo ratings yet

- Ben DoverDocument2 pagesBen DoverZerohedge0% (1)

- Concept of Universal Banking - Conceptual Framework and PracticeDocument9 pagesConcept of Universal Banking - Conceptual Framework and PracticedeepakNo ratings yet

- Godrej Prima Offer DeckDocument24 pagesGodrej Prima Offer DeckBharat SharmaNo ratings yet

- University of Rajasthan, Jaipur: ExaminationDocument1 pageUniversity of Rajasthan, Jaipur: ExaminationGodra English ClassesNo ratings yet

- SAP IRPA Estimation PDFDocument1 pageSAP IRPA Estimation PDFJMNo ratings yet

- ReSA-WCM-BUDGETING 240531 153818Document23 pagesReSA-WCM-BUDGETING 240531 153818Rayhanah IbrahimNo ratings yet

- Ps 3Document5 pagesPs 3Phong TrNo ratings yet

- Chapter 1 Group 8Document3 pagesChapter 1 Group 8emanuela patreciaNo ratings yet

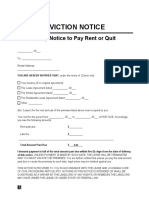

- Louisiana Eviction Notice 5 Day Pay Rent or QuitDocument3 pagesLouisiana Eviction Notice 5 Day Pay Rent or QuitJoe VuNo ratings yet

- 03 - Interest Rate DerivativesDocument65 pages03 - Interest Rate DerivativesRonnie KurtzbardNo ratings yet

- Company 1 PDFDocument5 pagesCompany 1 PDFDhriti KarnaniNo ratings yet

- MGT201 Final Term Subjective Solved With Reference 2014Document18 pagesMGT201 Final Term Subjective Solved With Reference 2014maryamNo ratings yet

- Chapter 15 - Purchase and Purchase Returns Day BooksDocument13 pagesChapter 15 - Purchase and Purchase Returns Day Booksshemida100% (2)

- Complaint Against Zions BankDocument56 pagesComplaint Against Zions BankThe Salt Lake TribuneNo ratings yet

- Various Factors Affecting Marketing FunctionDocument19 pagesVarious Factors Affecting Marketing Functionrk0522100% (1)

- Information Systems Engineering Coursework Assignment - UK University BSC Final YearDocument14 pagesInformation Systems Engineering Coursework Assignment - UK University BSC Final YearTDiscoverNo ratings yet

- Definition of Capital AllowancesDocument9 pagesDefinition of Capital AllowancesAdesolaNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument7 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancesknagarNo ratings yet

- Cambridge IGCSE (9-1) : ACCOUNTING 0985/22Document20 pagesCambridge IGCSE (9-1) : ACCOUNTING 0985/22Adityo Sandhy PutraNo ratings yet

- CV Imran KhanDocument3 pagesCV Imran Khanimran khanNo ratings yet

- Transaction History c08Document1 pageTransaction History c08Nabiel RHNo ratings yet

- Brown POQDocument4 pagesBrown POQJonas GonzalesNo ratings yet

- Chapter 1: Big Daddy: Long and ShortDocument2 pagesChapter 1: Big Daddy: Long and Shortshawshiuan_ongNo ratings yet

- Ratifying OrdinanceDocument2 pagesRatifying OrdinanceAmelia BersamiraNo ratings yet

- Practiceset 2Document5 pagesPracticeset 2nikmrisanraiNo ratings yet

- Draft AtapDocument9 pagesDraft AtapMuhd ArifNo ratings yet

- Zarai Taraqiati Bank Limited Consolidated Statement of Financial Position As at December 31, 2015 Note 2015 2014 Rupees in '000 AssetsDocument5 pagesZarai Taraqiati Bank Limited Consolidated Statement of Financial Position As at December 31, 2015 Note 2015 2014 Rupees in '000 AssetsFaisal AwanNo ratings yet