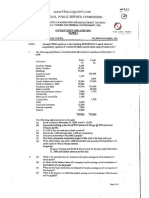

AP-01B Correction of Errors

AP-01B Correction of Errors

You might also like

- Anandam Manufacturing CompanyDocument9 pagesAnandam Manufacturing CompanyAijaz AslamNo ratings yet

- Translation of Financial Statements of Foreign AffiliatesDocument15 pagesTranslation of Financial Statements of Foreign Affiliatesayu wanasari100% (2)

- Ca (Bsaf - Bba.mba)Document5 pagesCa (Bsaf - Bba.mba)kashif aliNo ratings yet

- 03 Correction of Error CTDIDocument15 pages03 Correction of Error CTDIAiden PatsNo ratings yet

- Composition of Trade and Other Receivables1Document5 pagesComposition of Trade and Other Receivables1CJ alandyNo ratings yet

- Accounting EstimatesDocument6 pagesAccounting EstimatesChinNo ratings yet

- Process CostingDocument18 pagesProcess CostingCheliah Mae ImperialNo ratings yet

- This Study Resource Was: Pre-QE ExaminationDocument8 pagesThis Study Resource Was: Pre-QE ExaminationMarcus MonocayNo ratings yet

- A-Standards of Ethical Conduct For Management AccountantsDocument4 pagesA-Standards of Ethical Conduct For Management AccountantsChhun Mony RathNo ratings yet

- Quiz - Partnership Law Nov 7 2020Document4 pagesQuiz - Partnership Law Nov 7 2020eunicemaraNo ratings yet

- 03 - Partnership DissolutionDocument38 pages03 - Partnership DissolutionDonise Ronadel SantosNo ratings yet

- Conceptual Framework and Accounting StandardsDocument4 pagesConceptual Framework and Accounting StandardsGilyn NaputoNo ratings yet

- Financial Management BSATDocument9 pagesFinancial Management BSATEma Dupilas GuianalanNo ratings yet

- COSTCO Section 1Document11 pagesCOSTCO Section 1Paula BautistaNo ratings yet

- Partnetship DissolutionDocument45 pagesPartnetship DissolutionDe Gala ShailynNo ratings yet

- Afar NotesDocument20 pagesAfar NotesChristian James Umali BrionesNo ratings yet

- Shareholder's Equity Concept MapDocument1 pageShareholder's Equity Concept MapAbigailRefamonteNo ratings yet

- Depreciated Separately.: Property, Plant and EquipmentDocument5 pagesDepreciated Separately.: Property, Plant and EquipmentEmma Mariz GarciaNo ratings yet

- Cash & Cash Equivalents Composition & Other Topics CashDocument5 pagesCash & Cash Equivalents Composition & Other Topics CashEurich Gibarr Gavina EstradaNo ratings yet

- Chapter 4 DiscussionDocument11 pagesChapter 4 DiscussionArah OpalecNo ratings yet

- AuditDocument4 pagesAuditRoxanneNo ratings yet

- Finals - Inventories Exercises WithoutDocument10 pagesFinals - Inventories Exercises WithoutA.B AmpuanNo ratings yet

- Unit I: Overview of The Audit Process Audit Planning: Applied AuditingDocument8 pagesUnit I: Overview of The Audit Process Audit Planning: Applied AuditingAlexis Erica Bansuan OvaloNo ratings yet

- Partnership Problem SetDocument8 pagesPartnership Problem SetMary Rose ArguellesNo ratings yet

- Notes - FAR - InvestmentDocument7 pagesNotes - FAR - InvestmentElaineJrV-IgotNo ratings yet

- Lupisan-Baysa PDFDocument206 pagesLupisan-Baysa PDFRicart Von LauretaNo ratings yet

- Basic Accounting Equation Exercises 2Document2 pagesBasic Accounting Equation Exercises 2Ace Joseph TabaderoNo ratings yet

- Module 4 - Introduction To Partnership and Partnership FormationDocument14 pagesModule 4 - Introduction To Partnership and Partnership Formation1BSA5-ABM Espiritu, CharlesNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document14 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Cost Accounting Quiz 6 - Joint CostDocument5 pagesCost Accounting Quiz 6 - Joint CostSheenNo ratings yet

- 1 Partnership Accounting QuestionnairesDocument11 pages1 Partnership Accounting QuestionnairesShiela MayNo ratings yet

- ADVACCDocument3 pagesADVACCCianne AlcantaraNo ratings yet

- Asset Standard Initial Measurement Subsequent Measurement Included in Profit or Loss Financial POSITION PresentationDocument3 pagesAsset Standard Initial Measurement Subsequent Measurement Included in Profit or Loss Financial POSITION PresentationDidhane MartinezNo ratings yet

- Mary Joy Asis - RevalidaDocument16 pagesMary Joy Asis - RevalidaJoseph AsisNo ratings yet

- CH 07Document24 pagesCH 07xxxxxxxxxNo ratings yet

- AFAR 1 Partnership Accounting (Installment Liquidation)Document3 pagesAFAR 1 Partnership Accounting (Installment Liquidation)Jeepee JohnNo ratings yet

- Philippine Financial Reporting Standards: Number TitleDocument4 pagesPhilippine Financial Reporting Standards: Number TitleAlexis AlipudoNo ratings yet

- Performance Task 2 Project Scheduling PERT CPM Summer 2022 Bus Math 43 Management Science II PDFDocument17 pagesPerformance Task 2 Project Scheduling PERT CPM Summer 2022 Bus Math 43 Management Science II PDFVanessa PuaNo ratings yet

- AE 231 Governance Business Ethics Risk Management and Internal ControlDocument23 pagesAE 231 Governance Business Ethics Risk Management and Internal ControlMyles DaroyNo ratings yet

- The Environment of Financial Accounting and ReportingDocument12 pagesThe Environment of Financial Accounting and ReportingJi Baltazar100% (1)

- Ref 1 Prelim Quiz 1Document7 pagesRef 1 Prelim Quiz 1Melanie MinaNo ratings yet

- 2.3 Taxation Coverage For Performance Task 1Document33 pages2.3 Taxation Coverage For Performance Task 1?????No ratings yet

- Tutorial 3 - Process CostingDocument5 pagesTutorial 3 - Process Costingsouayeh wejdenNo ratings yet

- Accounting Adjusting EntriesDocument6 pagesAccounting Adjusting EntriescamilleNo ratings yet

- AGS CUP 6 Auditing Elimination RoundDocument17 pagesAGS CUP 6 Auditing Elimination RoundKenneth RobledoNo ratings yet

- Use The Following Information For The Next Two Questions.: Act1108 Financial Management Inventory Management - ExercisesDocument1 pageUse The Following Information For The Next Two Questions.: Act1108 Financial Management Inventory Management - ExercisesMaryrose SumulongNo ratings yet

- Chapter 7: Receivables: Principles of AccountingDocument50 pagesChapter 7: Receivables: Principles of AccountingRohail Javed100% (1)

- Additional Data For The Period Were ProvidedDocument3 pagesAdditional Data For The Period Were Providedmoncarla lagon100% (1)

- Intermediate Accounting Test Bank With SolManDocument40 pagesIntermediate Accounting Test Bank With SolManbpadz04No ratings yet

- Ce2 - FS Analysis 2Document7 pagesCe2 - FS Analysis 2Jamira Andrie AzuraNo ratings yet

- FAR 0 Merged Handouts and ReviewersDocument31 pagesFAR 0 Merged Handouts and ReviewersKin LeeNo ratings yet

- D12Document12 pagesD12neo14No ratings yet

- Cfas Lecture (Midterm)Document4 pagesCfas Lecture (Midterm)KianJohnCentenoTuricoNo ratings yet

- Advacc Quiz On PartnershipDocument10 pagesAdvacc Quiz On PartnershipLenie Lyn Pasion TorresNo ratings yet

- Ch07 The Conversion Cycle PDFDocument50 pagesCh07 The Conversion Cycle PDFVRNo ratings yet

- AdjustmentDocument5 pagesAdjustmentBeta TesterNo ratings yet

- Edoc - Pub Problems Solving Masdocx PDFDocument6 pagesEdoc - Pub Problems Solving Masdocx PDFReznakNo ratings yet

- Error CorrectionDocument7 pagesError CorrectionRizzel SubaNo ratings yet

- DocumentDocument5 pagesDocumentRica RegorisNo ratings yet

- Correction of Error LECTUREDocument3 pagesCorrection of Error LECTUREKobe bryantNo ratings yet

- Accounting ChangesDocument3 pagesAccounting Changesmary aligmayoNo ratings yet

- Auditing Problems Lecture On Correction of ErrorsDocument6 pagesAuditing Problems Lecture On Correction of Errorskarlo100% (3)

- Received 699254285006944Document1 pageReceived 699254285006944markNo ratings yet

- Received 1028986051587098Document1 pageReceived 1028986051587098markNo ratings yet

- MGT1107 Management Science Chapter 1Document20 pagesMGT1107 Management Science Chapter 1mark100% (1)

- MGT1107 Management Science Case 2Document22 pagesMGT1107 Management Science Case 2markNo ratings yet

- MGT1107 Management Science Case 3Document19 pagesMGT1107 Management Science Case 3markNo ratings yet

- Module 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesDocument3 pagesModule 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesmarkNo ratings yet

- MGT1107 Management Science Chapter 2Document23 pagesMGT1107 Management Science Chapter 2markNo ratings yet

- Module 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesDocument3 pagesModule 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesmarkNo ratings yet

- Jobli Group ResearchDocument22 pagesJobli Group ResearchmarkNo ratings yet

- Solution To AP05 - InvestmentsDocument17 pagesSolution To AP05 - InvestmentsmarkNo ratings yet

- R.A 11032 - Ease of Doing Business and Efficient Government Service Delivey ActDocument17 pagesR.A 11032 - Ease of Doing Business and Efficient Government Service Delivey ActmarkNo ratings yet

- 6870 - FAR First PreboardDocument14 pages6870 - FAR First PreboardZiee00No ratings yet

- Financial Analysis - Chapter 9 - Annisa Nabila Kanti - 155020307121021Document3 pagesFinancial Analysis - Chapter 9 - Annisa Nabila Kanti - 155020307121021Annisa Nabila KantiNo ratings yet

- Balaji TelefilmsDocument23 pagesBalaji TelefilmsShraddha TiwariNo ratings yet

- 01 Long QuizDocument6 pages01 Long Quizgiana riveraNo ratings yet

- List of Banks in EthiopiaDocument20 pagesList of Banks in EthiopiaTewodros2014No ratings yet

- Audit Problems 1 - PPE and IntangiblesDocument10 pagesAudit Problems 1 - PPE and IntangiblesPaula De RuedaNo ratings yet

- Week 05 2022 Topic 5 Lecture Leases Part BDocument19 pagesWeek 05 2022 Topic 5 Lecture Leases Part BErnest LeongNo ratings yet

- Sept 2021 Insight PartiiDocument133 pagesSept 2021 Insight Partiirowan betNo ratings yet

- AccountingDocument6 pagesAccountingGourav SaxenaNo ratings yet

- MCQ-IV Sem Cooperative Management and AdministrationDocument15 pagesMCQ-IV Sem Cooperative Management and Administrationthanish sivakumar100% (1)

- Appreciation and Depreciation Wo AnswersDocument4 pagesAppreciation and Depreciation Wo AnswersZoe BradshawNo ratings yet

- Ebook Cierre Fiscal y ContableDocument125 pagesEbook Cierre Fiscal y ContableAngel RejosNo ratings yet

- Fa 1 CompreDocument16 pagesFa 1 CompreTwainNo ratings yet

- Nisha Readymade 1300000Document12 pagesNisha Readymade 1300000afroz khanNo ratings yet

- Capital Formation in Agriculture PDFDocument17 pagesCapital Formation in Agriculture PDFArya SenapatiNo ratings yet

- Business DeductionsDocument46 pagesBusiness Deductionsdavid.ellis1245No ratings yet

- Owning & Operating of EquipmentDocument52 pagesOwning & Operating of EquipmentIan Louis Steve SantosNo ratings yet

- Internal Control Measures: Page 1 of 7Document7 pagesInternal Control Measures: Page 1 of 7Lucy HeartfiliaNo ratings yet

- AC1011.7.1 Midterm Examinations Questions and AnswersDocument20 pagesAC1011.7.1 Midterm Examinations Questions and AnswersrheaNo ratings yet

- Group4 Cityu8b Assignment Corporate FinanceDocument16 pagesGroup4 Cityu8b Assignment Corporate Financeđức nguyên anhNo ratings yet

- Answer:: Department of Finance and InvestmentDocument3 pagesAnswer:: Department of Finance and Investmentنايف محمد القباتليNo ratings yet

- Fin AcctgDocument9 pagesFin AcctgCarl Angelo0% (1)

- WRD 27e - SE PPT - Ch03 - ADADocument19 pagesWRD 27e - SE PPT - Ch03 - ADANovrissa DianiNo ratings yet

- Finch 11713Document166 pagesFinch 11713Ali ReynoldsNo ratings yet

- Aditya Birla Money SWOTDocument9 pagesAditya Birla Money SWOTGaurav SinghNo ratings yet

- Chap 007Document165 pagesChap 007Certified Public AccountantNo ratings yet

- Accountin & Auditing I & II PDFDocument123 pagesAccountin & Auditing I & II PDFSom DevNo ratings yet

- E TranspharmaDocument7 pagesE TranspharmaLucas Moraes Teixeira SalgadoNo ratings yet

Download as doc, pdf, or txt

You might also like

- Anandam Manufacturing CompanyDocument9 pagesAnandam Manufacturing CompanyAijaz AslamNo ratings yet

- Translation of Financial Statements of Foreign AffiliatesDocument15 pagesTranslation of Financial Statements of Foreign Affiliatesayu wanasari100% (2)

- Ca (Bsaf - Bba.mba)Document5 pagesCa (Bsaf - Bba.mba)kashif aliNo ratings yet

- 03 Correction of Error CTDIDocument15 pages03 Correction of Error CTDIAiden PatsNo ratings yet

- Composition of Trade and Other Receivables1Document5 pagesComposition of Trade and Other Receivables1CJ alandyNo ratings yet

- Accounting EstimatesDocument6 pagesAccounting EstimatesChinNo ratings yet

- Process CostingDocument18 pagesProcess CostingCheliah Mae ImperialNo ratings yet

- This Study Resource Was: Pre-QE ExaminationDocument8 pagesThis Study Resource Was: Pre-QE ExaminationMarcus MonocayNo ratings yet

- A-Standards of Ethical Conduct For Management AccountantsDocument4 pagesA-Standards of Ethical Conduct For Management AccountantsChhun Mony RathNo ratings yet

- Quiz - Partnership Law Nov 7 2020Document4 pagesQuiz - Partnership Law Nov 7 2020eunicemaraNo ratings yet

- 03 - Partnership DissolutionDocument38 pages03 - Partnership DissolutionDonise Ronadel SantosNo ratings yet

- Conceptual Framework and Accounting StandardsDocument4 pagesConceptual Framework and Accounting StandardsGilyn NaputoNo ratings yet

- Financial Management BSATDocument9 pagesFinancial Management BSATEma Dupilas GuianalanNo ratings yet

- COSTCO Section 1Document11 pagesCOSTCO Section 1Paula BautistaNo ratings yet

- Partnetship DissolutionDocument45 pagesPartnetship DissolutionDe Gala ShailynNo ratings yet

- Afar NotesDocument20 pagesAfar NotesChristian James Umali BrionesNo ratings yet

- Shareholder's Equity Concept MapDocument1 pageShareholder's Equity Concept MapAbigailRefamonteNo ratings yet

- Depreciated Separately.: Property, Plant and EquipmentDocument5 pagesDepreciated Separately.: Property, Plant and EquipmentEmma Mariz GarciaNo ratings yet

- Cash & Cash Equivalents Composition & Other Topics CashDocument5 pagesCash & Cash Equivalents Composition & Other Topics CashEurich Gibarr Gavina EstradaNo ratings yet

- Chapter 4 DiscussionDocument11 pagesChapter 4 DiscussionArah OpalecNo ratings yet

- AuditDocument4 pagesAuditRoxanneNo ratings yet

- Finals - Inventories Exercises WithoutDocument10 pagesFinals - Inventories Exercises WithoutA.B AmpuanNo ratings yet

- Unit I: Overview of The Audit Process Audit Planning: Applied AuditingDocument8 pagesUnit I: Overview of The Audit Process Audit Planning: Applied AuditingAlexis Erica Bansuan OvaloNo ratings yet

- Partnership Problem SetDocument8 pagesPartnership Problem SetMary Rose ArguellesNo ratings yet

- Notes - FAR - InvestmentDocument7 pagesNotes - FAR - InvestmentElaineJrV-IgotNo ratings yet

- Lupisan-Baysa PDFDocument206 pagesLupisan-Baysa PDFRicart Von LauretaNo ratings yet

- Basic Accounting Equation Exercises 2Document2 pagesBasic Accounting Equation Exercises 2Ace Joseph TabaderoNo ratings yet

- Module 4 - Introduction To Partnership and Partnership FormationDocument14 pagesModule 4 - Introduction To Partnership and Partnership Formation1BSA5-ABM Espiritu, CharlesNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document14 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Cost Accounting Quiz 6 - Joint CostDocument5 pagesCost Accounting Quiz 6 - Joint CostSheenNo ratings yet

- 1 Partnership Accounting QuestionnairesDocument11 pages1 Partnership Accounting QuestionnairesShiela MayNo ratings yet

- ADVACCDocument3 pagesADVACCCianne AlcantaraNo ratings yet

- Asset Standard Initial Measurement Subsequent Measurement Included in Profit or Loss Financial POSITION PresentationDocument3 pagesAsset Standard Initial Measurement Subsequent Measurement Included in Profit or Loss Financial POSITION PresentationDidhane MartinezNo ratings yet

- Mary Joy Asis - RevalidaDocument16 pagesMary Joy Asis - RevalidaJoseph AsisNo ratings yet

- CH 07Document24 pagesCH 07xxxxxxxxxNo ratings yet

- AFAR 1 Partnership Accounting (Installment Liquidation)Document3 pagesAFAR 1 Partnership Accounting (Installment Liquidation)Jeepee JohnNo ratings yet

- Philippine Financial Reporting Standards: Number TitleDocument4 pagesPhilippine Financial Reporting Standards: Number TitleAlexis AlipudoNo ratings yet

- Performance Task 2 Project Scheduling PERT CPM Summer 2022 Bus Math 43 Management Science II PDFDocument17 pagesPerformance Task 2 Project Scheduling PERT CPM Summer 2022 Bus Math 43 Management Science II PDFVanessa PuaNo ratings yet

- AE 231 Governance Business Ethics Risk Management and Internal ControlDocument23 pagesAE 231 Governance Business Ethics Risk Management and Internal ControlMyles DaroyNo ratings yet

- The Environment of Financial Accounting and ReportingDocument12 pagesThe Environment of Financial Accounting and ReportingJi Baltazar100% (1)

- Ref 1 Prelim Quiz 1Document7 pagesRef 1 Prelim Quiz 1Melanie MinaNo ratings yet

- 2.3 Taxation Coverage For Performance Task 1Document33 pages2.3 Taxation Coverage For Performance Task 1?????No ratings yet

- Tutorial 3 - Process CostingDocument5 pagesTutorial 3 - Process Costingsouayeh wejdenNo ratings yet

- Accounting Adjusting EntriesDocument6 pagesAccounting Adjusting EntriescamilleNo ratings yet

- AGS CUP 6 Auditing Elimination RoundDocument17 pagesAGS CUP 6 Auditing Elimination RoundKenneth RobledoNo ratings yet

- Use The Following Information For The Next Two Questions.: Act1108 Financial Management Inventory Management - ExercisesDocument1 pageUse The Following Information For The Next Two Questions.: Act1108 Financial Management Inventory Management - ExercisesMaryrose SumulongNo ratings yet

- Chapter 7: Receivables: Principles of AccountingDocument50 pagesChapter 7: Receivables: Principles of AccountingRohail Javed100% (1)

- Additional Data For The Period Were ProvidedDocument3 pagesAdditional Data For The Period Were Providedmoncarla lagon100% (1)

- Intermediate Accounting Test Bank With SolManDocument40 pagesIntermediate Accounting Test Bank With SolManbpadz04No ratings yet

- Ce2 - FS Analysis 2Document7 pagesCe2 - FS Analysis 2Jamira Andrie AzuraNo ratings yet

- FAR 0 Merged Handouts and ReviewersDocument31 pagesFAR 0 Merged Handouts and ReviewersKin LeeNo ratings yet

- D12Document12 pagesD12neo14No ratings yet

- Cfas Lecture (Midterm)Document4 pagesCfas Lecture (Midterm)KianJohnCentenoTuricoNo ratings yet

- Advacc Quiz On PartnershipDocument10 pagesAdvacc Quiz On PartnershipLenie Lyn Pasion TorresNo ratings yet

- Ch07 The Conversion Cycle PDFDocument50 pagesCh07 The Conversion Cycle PDFVRNo ratings yet

- AdjustmentDocument5 pagesAdjustmentBeta TesterNo ratings yet

- Edoc - Pub Problems Solving Masdocx PDFDocument6 pagesEdoc - Pub Problems Solving Masdocx PDFReznakNo ratings yet

- Error CorrectionDocument7 pagesError CorrectionRizzel SubaNo ratings yet

- DocumentDocument5 pagesDocumentRica RegorisNo ratings yet

- Correction of Error LECTUREDocument3 pagesCorrection of Error LECTUREKobe bryantNo ratings yet

- Accounting ChangesDocument3 pagesAccounting Changesmary aligmayoNo ratings yet

- Auditing Problems Lecture On Correction of ErrorsDocument6 pagesAuditing Problems Lecture On Correction of Errorskarlo100% (3)

- Received 699254285006944Document1 pageReceived 699254285006944markNo ratings yet

- Received 1028986051587098Document1 pageReceived 1028986051587098markNo ratings yet

- MGT1107 Management Science Chapter 1Document20 pagesMGT1107 Management Science Chapter 1mark100% (1)

- MGT1107 Management Science Case 2Document22 pagesMGT1107 Management Science Case 2markNo ratings yet

- MGT1107 Management Science Case 3Document19 pagesMGT1107 Management Science Case 3markNo ratings yet

- Module 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesDocument3 pagesModule 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesmarkNo ratings yet

- MGT1107 Management Science Chapter 2Document23 pagesMGT1107 Management Science Chapter 2markNo ratings yet

- Module 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesDocument3 pagesModule 3 of Week 6-7 Topic: Philippine Architecture Expected Learning OutcomesmarkNo ratings yet

- Jobli Group ResearchDocument22 pagesJobli Group ResearchmarkNo ratings yet

- Solution To AP05 - InvestmentsDocument17 pagesSolution To AP05 - InvestmentsmarkNo ratings yet

- R.A 11032 - Ease of Doing Business and Efficient Government Service Delivey ActDocument17 pagesR.A 11032 - Ease of Doing Business and Efficient Government Service Delivey ActmarkNo ratings yet

- 6870 - FAR First PreboardDocument14 pages6870 - FAR First PreboardZiee00No ratings yet

- Financial Analysis - Chapter 9 - Annisa Nabila Kanti - 155020307121021Document3 pagesFinancial Analysis - Chapter 9 - Annisa Nabila Kanti - 155020307121021Annisa Nabila KantiNo ratings yet

- Balaji TelefilmsDocument23 pagesBalaji TelefilmsShraddha TiwariNo ratings yet

- 01 Long QuizDocument6 pages01 Long Quizgiana riveraNo ratings yet

- List of Banks in EthiopiaDocument20 pagesList of Banks in EthiopiaTewodros2014No ratings yet

- Audit Problems 1 - PPE and IntangiblesDocument10 pagesAudit Problems 1 - PPE and IntangiblesPaula De RuedaNo ratings yet

- Week 05 2022 Topic 5 Lecture Leases Part BDocument19 pagesWeek 05 2022 Topic 5 Lecture Leases Part BErnest LeongNo ratings yet

- Sept 2021 Insight PartiiDocument133 pagesSept 2021 Insight Partiirowan betNo ratings yet

- AccountingDocument6 pagesAccountingGourav SaxenaNo ratings yet

- MCQ-IV Sem Cooperative Management and AdministrationDocument15 pagesMCQ-IV Sem Cooperative Management and Administrationthanish sivakumar100% (1)

- Appreciation and Depreciation Wo AnswersDocument4 pagesAppreciation and Depreciation Wo AnswersZoe BradshawNo ratings yet

- Ebook Cierre Fiscal y ContableDocument125 pagesEbook Cierre Fiscal y ContableAngel RejosNo ratings yet

- Fa 1 CompreDocument16 pagesFa 1 CompreTwainNo ratings yet

- Nisha Readymade 1300000Document12 pagesNisha Readymade 1300000afroz khanNo ratings yet

- Capital Formation in Agriculture PDFDocument17 pagesCapital Formation in Agriculture PDFArya SenapatiNo ratings yet

- Business DeductionsDocument46 pagesBusiness Deductionsdavid.ellis1245No ratings yet

- Owning & Operating of EquipmentDocument52 pagesOwning & Operating of EquipmentIan Louis Steve SantosNo ratings yet

- Internal Control Measures: Page 1 of 7Document7 pagesInternal Control Measures: Page 1 of 7Lucy HeartfiliaNo ratings yet

- AC1011.7.1 Midterm Examinations Questions and AnswersDocument20 pagesAC1011.7.1 Midterm Examinations Questions and AnswersrheaNo ratings yet

- Group4 Cityu8b Assignment Corporate FinanceDocument16 pagesGroup4 Cityu8b Assignment Corporate Financeđức nguyên anhNo ratings yet

- Answer:: Department of Finance and InvestmentDocument3 pagesAnswer:: Department of Finance and Investmentنايف محمد القباتليNo ratings yet

- Fin AcctgDocument9 pagesFin AcctgCarl Angelo0% (1)

- WRD 27e - SE PPT - Ch03 - ADADocument19 pagesWRD 27e - SE PPT - Ch03 - ADANovrissa DianiNo ratings yet

- Finch 11713Document166 pagesFinch 11713Ali ReynoldsNo ratings yet

- Aditya Birla Money SWOTDocument9 pagesAditya Birla Money SWOTGaurav SinghNo ratings yet

- Chap 007Document165 pagesChap 007Certified Public AccountantNo ratings yet

- Accountin & Auditing I & II PDFDocument123 pagesAccountin & Auditing I & II PDFSom DevNo ratings yet

- E TranspharmaDocument7 pagesE TranspharmaLucas Moraes Teixeira SalgadoNo ratings yet