Download as docx, pdf, or txt

You might also like

- IGCSE Business Studies Revision NotesDocument11 pagesIGCSE Business Studies Revision NotesWambui Kahende100% (3)

- Candle Business Startup Budget Sheet CS 2022Document8 pagesCandle Business Startup Budget Sheet CS 2022Andrei FilipNo ratings yet

- Spring Strawberry Salad With ChickenDocument3 pagesSpring Strawberry Salad With Chickenkaku0% (1)

- Chef 1320 E-Portfolio AssignmentDocument1 pageChef 1320 E-Portfolio Assignmentapi-310791920No ratings yet

- Poultry Calculator EXAMPLEDocument14 pagesPoultry Calculator EXAMPLEArshad Rashid ShahNo ratings yet

- Pig Calculation Tables: Date Batch Nr. Number of PigletsDocument7 pagesPig Calculation Tables: Date Batch Nr. Number of PigletsUrs SchaffnerNo ratings yet

- 08 11 December 2018 Questions and AnswersDocument26 pages08 11 December 2018 Questions and AnswersMae TomeldenNo ratings yet

- Chapter 14 - A Manager's Guide To Government in The MarketplaceDocument29 pagesChapter 14 - A Manager's Guide To Government in The MarketplaceMae TomeldenNo ratings yet

- Quiz 3Document33 pagesQuiz 3Arup DeyNo ratings yet

- Summer Internship/ Project WorkDocument45 pagesSummer Internship/ Project WorkAshwini PatelNo ratings yet

- Bill Ackman's Ira Sohn JCP PresentationDocument64 pagesBill Ackman's Ira Sohn JCP PresentationJohnCarney100% (1)

- Sol ch16Document12 pagesSol ch16Mae CruzNo ratings yet

- Ne Malai - 7 - Exercise CalculationDocument30 pagesNe Malai - 7 - Exercise CalculationNemalai VitalNo ratings yet

- Module 9 Problems - MrnakDocument9 pagesModule 9 Problems - MrnakJenny MrnakNo ratings yet

- EXERCICE Cost Accounting 16-16Document3 pagesEXERCICE Cost Accounting 16-16Amanda VeronikaNo ratings yet

- ACCT3203 Week 3 Tutorial Questions Joint Products S2 2022: Product Separable Costs Sales ValueDocument7 pagesACCT3203 Week 3 Tutorial Questions Joint Products S2 2022: Product Separable Costs Sales ValueJingwen YangNo ratings yet

- 3341 Chapter 16 ProblemsDocument11 pages3341 Chapter 16 ProblemsGrace Love Yzyry LuNo ratings yet

- ACCT303 Chapter 16Document40 pagesACCT303 Chapter 16Cừu Ngây NgôNo ratings yet

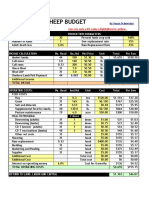

- 2013 Sample Sheep Budget: Annual LambingDocument10 pages2013 Sample Sheep Budget: Annual LambingGeros dienosNo ratings yet

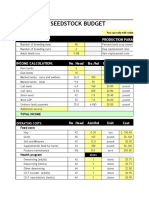

- 2016 Sheep Seedstock Budget: Annual LambingDocument8 pages2016 Sheep Seedstock Budget: Annual LambingGeros dienosNo ratings yet

- 2016 Wool Sheep Enterprise Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentDocument19 pages2016 Wool Sheep Enterprise Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentGeros dienosNo ratings yet

- Budget For 100 Conventional BroilersDocument3 pagesBudget For 100 Conventional BroilersMary Jessah LumbabNo ratings yet

- Sample Dairy Beef BudgetDocument2 pagesSample Dairy Beef BudgetUniversity of Bohol Professional StudiesNo ratings yet

- Production and Operation Management-PARDUCHO, NICOLE S.A-Course Requirement 2Document11 pagesProduction and Operation Management-PARDUCHO, NICOLE S.A-Course Requirement 2NicoleParduchoNo ratings yet

- 2013 Sample Meat Goat Budget: Annual KiddingDocument6 pages2013 Sample Meat Goat Budget: Annual KiddingGeros dienosNo ratings yet

- Sample Fryer Rabbit Budget PDFDocument2 pagesSample Fryer Rabbit Budget PDFGrace NacionalNo ratings yet

- This Template Is Not Capable of Detailed Financial AnalysisDocument35 pagesThis Template Is Not Capable of Detailed Financial AnalysisAlexNo ratings yet

- 954017mppu v1.1 Processing OnlyDocument8 pages954017mppu v1.1 Processing OnlyNareshNo ratings yet

- MD Meat Goat Seedstock Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentDocument19 pagesMD Meat Goat Seedstock Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentGeros dienosNo ratings yet

- Assumptions/Data: Unit Price Unit Variable CostDocument7 pagesAssumptions/Data: Unit Price Unit Variable CostHannan yusuf KhanNo ratings yet

- 2016 Goat Seedstock Budget: Annual KiddingDocument8 pages2016 Goat Seedstock Budget: Annual KiddingGeros dienosNo ratings yet

- Spring Strawberry Salad With ChickenDocument3 pagesSpring Strawberry Salad With Chicken19071 AVIK AGGARWALNo ratings yet

- Agriculture Sba Karakay PunalDocument2 pagesAgriculture Sba Karakay PunalKarakay PunalNo ratings yet

- Honey Bee: Southwest British Columbia Small-Scale Farm Enterprise BudgetDocument3 pagesHoney Bee: Southwest British Columbia Small-Scale Farm Enterprise Budgetbello2011No ratings yet

- SRC & Yield - WastageDocument6 pagesSRC & Yield - WastageAMAN MIGLANINo ratings yet

- Jawaban Akuntansi 3 KelompokDocument14 pagesJawaban Akuntansi 3 KelompokJason sean cNo ratings yet

- CostAcc CaseCh06 ADocument3 pagesCostAcc CaseCh06 ANhư TrầnNo ratings yet

- Deadweight Loss Formula Excel TemplateDocument7 pagesDeadweight Loss Formula Excel TemplateMustafa Ricky Pramana SeNo ratings yet

- CVPDocument9 pagesCVPClei UbandoNo ratings yet

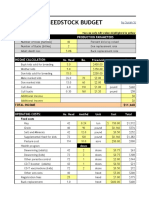

- 2016 Sheep Seedstock Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentDocument19 pages2016 Sheep Seedstock Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentGeros dienosNo ratings yet

- Designation Basic Salary House Rent Medical Allowance: MHR Corp Salary SheetDocument16 pagesDesignation Basic Salary House Rent Medical Allowance: MHR Corp Salary SheetMehedi HasanNo ratings yet

- Acquisitions) For A Discussion of This AnalysisDocument12 pagesAcquisitions) For A Discussion of This AnalysishamadeenooNo ratings yet

- Sample Dairy Heifer Budget Small Breeds ConfinedDocument2 pagesSample Dairy Heifer Budget Small Breeds ConfinedUniversity of Bohol Professional StudiesNo ratings yet

- PC - ExampleDocument6 pagesPC - Exampleaiaklearn1No ratings yet

- Target - 320+87+114 (521) /2 261Document4 pagesTarget - 320+87+114 (521) /2 261sneha patelNo ratings yet

- Expenses: Event Budget Muffin Top Beside Knutsford ExpressDocument2 pagesExpenses: Event Budget Muffin Top Beside Knutsford ExpressHjort HenryNo ratings yet

- Marjorie Bse 4a EconomicsDocument25 pagesMarjorie Bse 4a Economics062691No ratings yet

- RD FinancialDocument42 pagesRD FinancialAmranul HaqueNo ratings yet

- 2017 Meat Goat Enterprise Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentDocument19 pages2017 Meat Goat Enterprise Budget: Assumptions Income Feed Costs Veterinary Costs Other Expenses Capital InvestmentGeros dienosNo ratings yet

- BROILERSDocument2 pagesBROILERSthatolicious49No ratings yet

- Total Investment: Selling Price Amazon Fee Landing Cost Referral % Referral FBA Fee Storage Total Fee Product FrieghtDocument4 pagesTotal Investment: Selling Price Amazon Fee Landing Cost Referral % Referral FBA Fee Storage Total Fee Product FrieghtSyed AsadNo ratings yet

- How To Calculate Markup PercentageDocument12 pagesHow To Calculate Markup PercentageAlma SarciaNo ratings yet

- Health Benefits CostsDocument3 pagesHealth Benefits CostsCharll Dezon AbaNo ratings yet

- Mayo Lusong Meat ProcessingDocument4 pagesMayo Lusong Meat ProcessingRonnie ManaoNo ratings yet

- Latihan Cost Volume Profit Analysis (01) : Source of Variable CostDocument9 pagesLatihan Cost Volume Profit Analysis (01) : Source of Variable CostechaaaxxNo ratings yet

- Latihan Cost Volume Profit Analysis (01) : Source of Variable CostDocument9 pagesLatihan Cost Volume Profit Analysis (01) : Source of Variable CostechaaaxxNo ratings yet

- Production CostingDocument1 pageProduction CostingMAV MacaleNo ratings yet

- ICE #3 - Break Even and Pricing (Semester 3)Document4 pagesICE #3 - Break Even and Pricing (Semester 3)Ava Farjad100% (1)

- Joint Products & by Products - 2440011362 - Rogger SeptryaDocument2 pagesJoint Products & by Products - 2440011362 - Rogger SeptryaRogger SeptryaNo ratings yet

- FINANCIAL FEASIB - Start Up CostsDocument2 pagesFINANCIAL FEASIB - Start Up Costs2B MASIGLAT, CRIZEL JOY Y.No ratings yet

- Inventories: Discussion QuestionsDocument8 pagesInventories: Discussion QuestionsJNo ratings yet

- Joint CostingDocument38 pagesJoint CostingHassan MohiuddinNo ratings yet

- Goat RaisingDocument2 pagesGoat RaisingBENJIELITO EMPENADONo ratings yet

- Republic of The Philippines: Sorsogon National High School Sorsogon CityDocument2 pagesRepublic of The Philippines: Sorsogon National High School Sorsogon CityCYRIL DOMENSNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- QuizDocument2 pagesQuizMae TomeldenNo ratings yet

- Ch1.6 Distribution of Discrete R.V.: Binomial DistributionDocument4 pagesCh1.6 Distribution of Discrete R.V.: Binomial DistributionMae TomeldenNo ratings yet

- Econ 25 PrelimsDocument6 pagesEcon 25 PrelimsMae TomeldenNo ratings yet

- Taste Sample Number Squash Seed Coffee Commercial Coffee D DDocument3 pagesTaste Sample Number Squash Seed Coffee Commercial Coffee D DMae TomeldenNo ratings yet

- Review of Related LiteratureDocument5 pagesReview of Related LiteratureMae Tomelden100% (1)

- Squash Seeds FinalDocument9 pagesSquash Seeds FinalMae TomeldenNo ratings yet

- Bus Math 42 Prelims Test Formula: Chi-Square TableDocument1 pageBus Math 42 Prelims Test Formula: Chi-Square TableMae TomeldenNo ratings yet

- Color Sample Number Squash Seed Coffee Commercial Coffee D DDocument3 pagesColor Sample Number Squash Seed Coffee Commercial Coffee D DMae TomeldenNo ratings yet

- ReferencesDocument3 pagesReferencesMae TomeldenNo ratings yet

- Hapter 1: Introduction and Background of The StudyDocument11 pagesHapter 1: Introduction and Background of The StudyMae Tomelden100% (2)

- Chapter 1: Introduction and Background of The Study: Page - 1Document129 pagesChapter 1: Introduction and Background of The Study: Page - 1Mae TomeldenNo ratings yet

- Squash Seeds FinalDocument19 pagesSquash Seeds FinalMae TomeldenNo ratings yet

- No Garage No Car Position PaperDocument12 pagesNo Garage No Car Position PaperMae TomeldenNo ratings yet

- January 2019: Sun Mon Tue Wed Thu Fri SatDocument1 pageJanuary 2019: Sun Mon Tue Wed Thu Fri SatMae TomeldenNo ratings yet

- Case Study1 (GM Bailout)Document2 pagesCase Study1 (GM Bailout)Mae TomeldenNo ratings yet

- Actual Market Day SWOT AnalysisDocument1 pageActual Market Day SWOT AnalysisMae TomeldenNo ratings yet

- Medical CertificateDocument1 pageMedical CertificateMae TomeldenNo ratings yet

- February 2019 : Sun Mon Tue Wed Thu Fri SatDocument1 pageFebruary 2019 : Sun Mon Tue Wed Thu Fri SatMae TomeldenNo ratings yet

- BPCLDocument184 pagesBPCLYogesh Puneeth VNo ratings yet

- Furniture & Homeware - Indonesia - Statista Market ForecastDocument13 pagesFurniture & Homeware - Indonesia - Statista Market ForecastSales InteriorquNo ratings yet

- First Exam (ch.1-5) PDFDocument43 pagesFirst Exam (ch.1-5) PDFOmar HosnyNo ratings yet

- Introduction To Transaction ProcessingDocument6 pagesIntroduction To Transaction ProcessingmafeNo ratings yet

- Management ProjectDocument21 pagesManagement ProjectShivam KapoorNo ratings yet

- Generally Accepted Accounting PrinciplesDocument29 pagesGenerally Accepted Accounting Principlesarpit vora100% (2)

- Mett International Pty LTD Financial Forecast 3 Year SummaryDocument134 pagesMett International Pty LTD Financial Forecast 3 Year SummaryJamilexNo ratings yet

- HLL Vs Itc Big Fight 300805 SskiDocument35 pagesHLL Vs Itc Big Fight 300805 Sskimohit_rawatNo ratings yet

- Industry Analysis of Banking SectorDocument20 pagesIndustry Analysis of Banking Sectorusefulthomas67No ratings yet

- FInancial Management MidtermDocument5 pagesFInancial Management MidtermJosella McKay SantosNo ratings yet

- GudiyattamDocument211 pagesGudiyattamMadhan Manoharan100% (1)

- Advanced Financial Accounting and Reporting 14 - NGAS: Straight Problems Problem 1Document6 pagesAdvanced Financial Accounting and Reporting 14 - NGAS: Straight Problems Problem 1Jem ValmonteNo ratings yet

- Financial Ratio Analysis Infosys PresentationDocument44 pagesFinancial Ratio Analysis Infosys PresentationSushanth VarmaNo ratings yet

- APC Ch1solDocument7 pagesAPC Ch1solAnonymous LusWvyNo ratings yet

- ReflectionDocument3 pagesReflectionsonpatz678No ratings yet

- CH - Depatmental Accounting: Fill in The BlanksDocument4 pagesCH - Depatmental Accounting: Fill in The BlanksSardar Gurpreet Singh100% (1)

- Company Financial Analysis Project: Nke - Nyse Nike IncDocument37 pagesCompany Financial Analysis Project: Nke - Nyse Nike IncAliceJohnNo ratings yet

- Business Proposal g1Document18 pagesBusiness Proposal g1Sarah Mel Gwyneth DequitoNo ratings yet

- Interim Financial ReportingDocument17 pagesInterim Financial ReportingAlexa LeeNo ratings yet

- Chap 7Document27 pagesChap 7Joanne Chau100% (1)

- Practice CF Scooter KeyDocument4 pagesPractice CF Scooter KeyAllie LinNo ratings yet

- FAR SampleDocument3 pagesFAR SampleAt Least Know This CPANo ratings yet

- Chapter 13Document2 pagesChapter 13Fatima Nicetas Rabang AlonzoNo ratings yet

- Tally-9 0Document35 pagesTally-9 0Řohan DhakalNo ratings yet

- ExampleDocument2 pagesExampleandrew_yardy2623No ratings yet

- T6 Lecture Note For Chapter 1 To 5Document42 pagesT6 Lecture Note For Chapter 1 To 5Mahbubul Karim ShahinNo ratings yet