Download as xlsx, pdf, or txt

You might also like

- Barclays MT199Document2 pagesBarclays MT199Cash monkey100% (1)

- Homework Chapter 12Document28 pagesHomework Chapter 12Trung Kiên NguyễnNo ratings yet

- Be16 P16 2aDocument7 pagesBe16 P16 2aLisa Hammerle ClarkNo ratings yet

- CH 14Document2 pagesCH 14tigger5191100% (1)

- Cash and ReceivablesDocument30 pagesCash and ReceivablesAira Mae Hernandez CabaNo ratings yet

- Chapter 6Document17 pagesChapter 6RB100% (1)

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- Working 3Document6 pagesWorking 3Hà Lê DuyNo ratings yet

- CH 5 LS Practice HW QUIZDocument25 pagesCH 5 LS Practice HW QUIZDenise Jane RoqueNo ratings yet

- OBN - AFBA - Issue 36 (August 2021)Document1 pageOBN - AFBA - Issue 36 (August 2021)Nate TobikNo ratings yet

- Sbi Stock Statement Format in ExcelDocument33 pagesSbi Stock Statement Format in ExcelShadab Malik67% (3)

- Cost Accounting CHPTR 2Document6 pagesCost Accounting CHPTR 2Keisha Lynch75% (4)

- On August 1 2010 Sietens Corporation Had The Following AccountDocument1 pageOn August 1 2010 Sietens Corporation Had The Following AccountAmit PandeyNo ratings yet

- Kisi2 UAS AKM TerjawabDocument8 pagesKisi2 UAS AKM TerjawabBakhtiar AlakadarnyaNo ratings yet

- Tutorial 6 For Instructor PDFDocument5 pagesTutorial 6 For Instructor PDFsherynNo ratings yet

- Problem 2Document4 pagesProblem 2redassdawn100% (1)

- Chapter 7 Supplemental QuestionsDocument7 pagesChapter 7 Supplemental QuestionsDita Ens100% (1)

- Perrt 8 Debt InvestmentDocument2 pagesPerrt 8 Debt InvestmentVidya IntaniNo ratings yet

- Intermediate Accounting Test Bank 3Rd Edition - Test Bank Intermediate Accounting Test Bank 3Rd Edition - Test BankDocument39 pagesIntermediate Accounting Test Bank 3Rd Edition - Test Bank Intermediate Accounting Test Bank 3Rd Edition - Test BankKaren CaelNo ratings yet

- Latihan 7 PAK MaksiDocument3 pagesLatihan 7 PAK MaksiDwi HandariniNo ratings yet

- Tutorial Laporan Arus KasDocument17 pagesTutorial Laporan Arus KasRatna DwiNo ratings yet

- Latihan Accounts ReceivableDocument2 pagesLatihan Accounts ReceivableAlghifary RamadhanNo ratings yet

- Homework Week7Document3 pagesHomework Week7Arista Yuliana SariNo ratings yet

- M REYES Act.2Document2 pagesM REYES Act.2chingchongNo ratings yet

- Working 4Document8 pagesWorking 4Hà Lê DuyNo ratings yet

- Test Canvas: C1: FMGT123Document162 pagesTest Canvas: C1: FMGT123Illion IllionNo ratings yet

- Final Review Jawaban IntermediateDocument33 pagesFinal Review Jawaban Intermediatelukes12No ratings yet

- Chapter 11 Capital Budgeting Cash FlowsDocument33 pagesChapter 11 Capital Budgeting Cash FlowsShahadNo ratings yet

- Kieso Chapter 13Document98 pagesKieso Chapter 13GraceNo ratings yet

- Tugas 6 AKM1 Muhammad Alfarizi 142200278 EA-IDocument9 pagesTugas 6 AKM1 Muhammad Alfarizi 142200278 EA-Imuhammad alfariziNo ratings yet

- IygfigDocument52 pagesIygfigDelfiaNo ratings yet

- Journal Entry at The Step of TransactionDocument4 pagesJournal Entry at The Step of Transactionadmin finishyourtaskNo ratings yet

- CH 14 MCDocument38 pagesCH 14 MCElaine Lingx100% (1)

- Gross Profit MethodDocument25 pagesGross Profit MethoddionirtaNo ratings yet

- Reviewer Mid FinDocument108 pagesReviewer Mid FinIrish Mae DesoyoNo ratings yet

- Zulfitri Handayani - A031191125 (Akkeu P15-3)Document6 pagesZulfitri Handayani - A031191125 (Akkeu P15-3)RismayantiNo ratings yet

- ch11 Kieso IFRS4 SMDocument82 pagesch11 Kieso IFRS4 SM黃炳智No ratings yet

- CH 04Document40 pagesCH 04Melanie SamsonaNo ratings yet

- ACC 221 - Fourth ExaminationDocument5 pagesACC 221 - Fourth ExaminationCharlesNo ratings yet

- Quiz On Partnership LiquidationDocument4 pagesQuiz On Partnership LiquidationTrisha Mae AlburoNo ratings yet

- Ganang Surya Hananta Swara 1901572691 Tugas Personal Ke-4 Minggu 8Document22 pagesGanang Surya Hananta Swara 1901572691 Tugas Personal Ke-4 Minggu 8Vira JilmiNo ratings yet

- Exercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueDocument9 pagesExercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueManuel Magadatu100% (1)

- Week 2 Assessment: Accounting For Business CombinationsDocument12 pagesWeek 2 Assessment: Accounting For Business Combinationstasya salfiraNo ratings yet

- Problem 7 - 22Document3 pagesProblem 7 - 22Jao FloresNo ratings yet

- Kieso Ifrs Testbank ch17Document44 pagesKieso Ifrs Testbank ch17Turan, Jel Therese A.No ratings yet

- Chapter 15 Amended With AnswersDocument6 pagesChapter 15 Amended With AnswersIbn FaridNo ratings yet

- Tugas CH 8 Dan 9Document13 pagesTugas CH 8 Dan 9muhammad alfariziNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument6 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionAIENNA GABRIELLE FABRO100% (1)

- Case 7-20 Contact Global Our Analysis-FinalsDocument11 pagesCase 7-20 Contact Global Our Analysis-FinalsJenny Malabrigo, MBANo ratings yet

- Seiler Co Purchased 6,000,000Document1 pageSeiler Co Purchased 6,000,000Zes ONo ratings yet

- Tugas Advanced Acc. 1Document4 pagesTugas Advanced Acc. 1Astria Arha DillaNo ratings yet

- Fitzgeraldhyne Rappan - A031221038Document2 pagesFitzgeraldhyne Rappan - A031221038Fitzgeraldhyne RappanNo ratings yet

- Soal Bab 15Document5 pagesSoal Bab 15suci monalia putriNo ratings yet

- Chapter 4 CourseDocument15 pagesChapter 4 CourseMagdy KamelNo ratings yet

- Tugas AKM II Minggu 9Document2 pagesTugas AKM II Minggu 9Clarissa NastaniaNo ratings yet

- Midterm Answer KeyDocument6 pagesMidterm Answer Keyazzenethfaye.delacruz.mnlNo ratings yet

- Chapter 10 Intermediate Final RevisionDocument8 pagesChapter 10 Intermediate Final Revisionmagdy kamelNo ratings yet

- Module 13 Present ValueDocument10 pagesModule 13 Present ValueChristine Elaine LamanNo ratings yet

- Financial Assets at Fair Value (Investments) Basic ConceptsDocument2 pagesFinancial Assets at Fair Value (Investments) Basic ConceptsMonica Monica0% (1)

- Chapter 16Document6 pagesChapter 16YasirNo ratings yet

- Exam 1-5Document68 pagesExam 1-5RB100% (1)

- (03A) AR NR Quiz ANSWER KEYDocument8 pages(03A) AR NR Quiz ANSWER KEYKhai Ed PabelicoNo ratings yet

- Chapter 8Document17 pagesChapter 8Jamaica DavidNo ratings yet

- CH 07Document8 pagesCH 07Antonios FahedNo ratings yet

- The Big ShortDocument7 pagesThe Big ShortFrans Jd0% (1)

- Application Form For Education LoanDocument9 pagesApplication Form For Education Loanaakash chauhanNo ratings yet

- PIK Loan: From Wikipedia, The Free EncyclopediaDocument3 pagesPIK Loan: From Wikipedia, The Free Encyclopediacorporateboy36596No ratings yet

- Zenith Bank PLC: Page 1 of 1Document1 pageZenith Bank PLC: Page 1 of 1Wisdom chinecherem Odume INo ratings yet

- Business Account StatementDocument2 pagesBusiness Account StatementRamesh NatarajanNo ratings yet

- 1550244822117Document38 pages1550244822117tawhide_islamicNo ratings yet

- Microfinance in IndiaDocument12 pagesMicrofinance in IndiaRavi KiranNo ratings yet

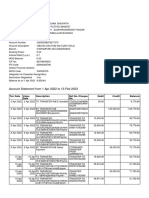

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument2 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balancesandhya kotaNo ratings yet

- Core Banking Solutions FinalDocument7 pagesCore Banking Solutions FinalShashank VarmaNo ratings yet

- CZG GC EGl Qa 6 XW Co XDocument6 pagesCZG GC EGl Qa 6 XW Co XvenkatNo ratings yet

- MCB Bank Report (Final) - ProjectDocument24 pagesMCB Bank Report (Final) - ProjectAbdul RafayNo ratings yet

- Account Statement From 1 Jan 2017 To 30 Jun 2017Document2 pagesAccount Statement From 1 Jan 2017 To 30 Jun 2017Ujjain mpNo ratings yet

- EximDocument3 pagesEximHabibullah ForkanNo ratings yet

- 2012 UCPB Annual ReportDocument81 pages2012 UCPB Annual ReportPat Dela CruzNo ratings yet

- Salary Advance Application FormDocument2 pagesSalary Advance Application FormHAbbuno0% (1)

- Statement 76051387 GBP 2024-01-25 2024-01-25Document3 pagesStatement 76051387 GBP 2024-01-25 2024-01-25qazz68751No ratings yet

- Bill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Document6 pagesBill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Akram YasinNo ratings yet

- Heloc Booklet (CFPB)Document19 pagesHeloc Booklet (CFPB)SweetysNo ratings yet

- Deposit MobiliziationDocument454 pagesDeposit MobiliziationperkisasNo ratings yet

- Opening A Bank Account Leaflet Jan 2018Document6 pagesOpening A Bank Account Leaflet Jan 2018Harry NugrahaNo ratings yet

- Lesson Twelve Quiz: Saving and Investing: True-FalseDocument1 pageLesson Twelve Quiz: Saving and Investing: True-FalseRashed AlawaishehNo ratings yet

- L-5&6 642 ReserveDocument44 pagesL-5&6 642 ReserveNiloy AhmedNo ratings yet

- Institute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingDocument3 pagesInstitute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingTarun GargNo ratings yet

- On Banking SystemDocument17 pagesOn Banking SystemPankajdchaudhari79% (19)

- Bank Reconciliation Roi Book Center 1Document4 pagesBank Reconciliation Roi Book Center 1Shane Nicole DagatanNo ratings yet

- PNB 250821Document1 pagePNB 250821P K MahatoNo ratings yet