Download as pdf or txt

You might also like

- Introduction To Islamic Fintech - Mufti Faraz AdamDocument165 pagesIntroduction To Islamic Fintech - Mufti Faraz AdamAini Khairiyah SharakalNo ratings yet

- Forensic and Investigative AccountingDocument51 pagesForensic and Investigative AccountingNarendra Sengupta100% (5)

- Video Lesson Chapter 7 Fabm2 Journal and LedgerDocument27 pagesVideo Lesson Chapter 7 Fabm2 Journal and LedgerRon louise Pereyra100% (8)

- CH - 9 Assessing The Risk of Material MisstatementDocument14 pagesCH - 9 Assessing The Risk of Material MisstatementOmar C100% (2)

- Auditing: Prsentation On Frauds and Errors in AuditingDocument8 pagesAuditing: Prsentation On Frauds and Errors in AuditingABHINAV KHURANANo ratings yet

- Chapter 17Document21 pagesChapter 17Talia AdaNo ratings yet

- PPT3-Recoqnizing The Symptoms of FraudDocument21 pagesPPT3-Recoqnizing The Symptoms of FraudSintia LieNo ratings yet

- Errors & FraudsDocument27 pagesErrors & FraudsmostakNo ratings yet

- Module 4ADocument6 pagesModule 4Aashley.cyang1988No ratings yet

- Kwentahan Tayo Basic Internal ControlsDocument27 pagesKwentahan Tayo Basic Internal ControlsMary Ann RosilNo ratings yet

- Cash and Internal Control: Ani Wilujeng Suryani, PHDDocument47 pagesCash and Internal Control: Ani Wilujeng Suryani, PHDRoby RohmadNo ratings yet

- CH 7Document32 pagesCH 7Савелий СмирновNo ratings yet

- Fraud Detection: No Name Matric NumberDocument51 pagesFraud Detection: No Name Matric NumberRiri MorganaNo ratings yet

- Topic 7 Internal ControlDocument41 pagesTopic 7 Internal ControlKevin LoboNo ratings yet

- Module - IV Errors, Frauds and MisstatementsDocument25 pagesModule - IV Errors, Frauds and MisstatementsMeenakshi RajakumarNo ratings yet

- Unit IDocument17 pagesUnit IThiri PhwayNo ratings yet

- Material Auditing1 5Document86 pagesMaterial Auditing1 5Akshat RanaNo ratings yet

- Auditing and Fraud Prevention: What Is Fraud and How Can You Protect Your Organization?Document12 pagesAuditing and Fraud Prevention: What Is Fraud and How Can You Protect Your Organization?Bambang HaryadiNo ratings yet

- Audit of CashDocument15 pagesAudit of CashZelalem Hassen100% (1)

- Ethical Issues in Accounting: Course Code: ACT 4102Document16 pagesEthical Issues in Accounting: Course Code: ACT 4102Tanvir Ahmed100% (1)

- CH 08Document33 pagesCH 08Kushal VyasNo ratings yet

- Objectivesofauditing 200715072549Document18 pagesObjectivesofauditing 200715072549hitaler.raazNo ratings yet

- Types of Accounting ErrorsDocument8 pagesTypes of Accounting ErrorsHassleBustNo ratings yet

- Part 7 Fundamentals of Accountanct 1Document30 pagesPart 7 Fundamentals of Accountanct 1mang tomasNo ratings yet

- Auditing and Corporate GovernanceDocument13 pagesAuditing and Corporate Governancesuraj agarwalNo ratings yet

- ACCT 3109 - AuditingDocument41 pagesACCT 3109 - AuditingChung CFNo ratings yet

- Lecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringDocument24 pagesLecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- Albrecht Chap 02Document31 pagesAlbrecht Chap 02Aze NutzNo ratings yet

- Chapter 2 Audit of CashDocument11 pagesChapter 2 Audit of Cashadinew abeyNo ratings yet

- Internal Control and CashDocument8 pagesInternal Control and CashHassleBustNo ratings yet

- Chapter 8 MBA 65Document40 pagesChapter 8 MBA 65Al Rashedin KawserNo ratings yet

- Week 4: Ledgers and Trial BalanceDocument23 pagesWeek 4: Ledgers and Trial BalanceIris NguNo ratings yet

- Auditors ResponisbilityDocument5 pagesAuditors ResponisbilityGigi LuceroNo ratings yet

- 02 Red FlagDocument25 pages02 Red Flagcasaurabhmittal2006No ratings yet

- Fraud IndicatorsDocument26 pagesFraud IndicatorsIena SharinaNo ratings yet

- Unit 1 Meaning and Definition of AuditingDocument88 pagesUnit 1 Meaning and Definition of AuditingsdfghjkNo ratings yet

- Acctsys Unit 3Document15 pagesAcctsys Unit 3Mutya TimbangNo ratings yet

- Corpgov - Chapter 14-17Document22 pagesCorpgov - Chapter 14-17AlexanNo ratings yet

- CB Review Modules 3 and 4Document175 pagesCB Review Modules 3 and 4Glemhar RodriguezNo ratings yet

- Jonah Beker - A Class 11Document5 pagesJonah Beker - A Class 11Liza NinalgaNo ratings yet

- Auditing NotesDocument73 pagesAuditing Notesvivekrawatsingh9084No ratings yet

- 02 Red FlagDocument25 pages02 Red FlagArif AhmedNo ratings yet

- Untitled Presentation - KeyDocument15 pagesUntitled Presentation - Keysexy samuelNo ratings yet

- AA - MC.U3COM2107048 Forensic Accounting and Fraud Management Module 05 Assignment 05Document3 pagesAA - MC.U3COM2107048 Forensic Accounting and Fraud Management Module 05 Assignment 05Thurai MuruganNo ratings yet

- BCom 6th Sem - AuditingDocument46 pagesBCom 6th Sem - AuditingJibin Samuel100% (1)

- The Five Letter F Word: Fraud in The Hospitality Industry: Topics For DiscussionDocument21 pagesThe Five Letter F Word: Fraud in The Hospitality Industry: Topics For Discussionmohamed12345No ratings yet

- Chapter 4 Audit Responsibility, EvidenceDocument17 pagesChapter 4 Audit Responsibility, EvidenceYitera SisayNo ratings yet

- Group 4: Module 12: Errors and Irregularities in The Transaction Cycles of The Business EntityDocument35 pagesGroup 4: Module 12: Errors and Irregularities in The Transaction Cycles of The Business EntityApril Joy ObedozaNo ratings yet

- Bcs Midterms ReviewerDocument22 pagesBcs Midterms ReviewerJustine Jean PerezNo ratings yet

- Can Ethical Culture Prevent FraudsDocument8 pagesCan Ethical Culture Prevent FraudsRaj MohanNo ratings yet

- Objectives of AuditingDocument22 pagesObjectives of AuditingArjun M JimmyNo ratings yet

- Overtrading and UndertradingDocument2 pagesOvertrading and UndertradingYee TanNo ratings yet

- Overtrading and UndertradingDocument2 pagesOvertrading and UndertradingYee TanNo ratings yet

- Errors and FraudDocument25 pagesErrors and Fraudmiam67830No ratings yet

- Audch 2Document13 pagesAudch 2kitababekele26No ratings yet

- BOOKKEEPINGDocument6 pagesBOOKKEEPINGsserugo dodovicNo ratings yet

- Mod 5 - AuditingDocument51 pagesMod 5 - AuditingInchara S Dept of MBANo ratings yet

- Accounting: THE Language of BusinessDocument53 pagesAccounting: THE Language of BusinessBAM ZAHARDNo ratings yet

- Acc114a Fraud and ErrorDocument8 pagesAcc114a Fraud and Errorsophia lorreine chattoNo ratings yet

- Chapter 14 Fraud and ErrorDocument7 pagesChapter 14 Fraud and ErrorAlexanNo ratings yet

- Forensic Accounting: Dr. Lynn H. Clements Cpa Cfe CR - Fa Cma CFMDocument14 pagesForensic Accounting: Dr. Lynn H. Clements Cpa Cfe CR - Fa Cma CFMRalph Santos0% (1)

- Fraud Detection and PreventionDocument5 pagesFraud Detection and PreventionIrsani KurniatiNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Bosco Bizcon DraftDocument50 pagesBosco Bizcon DraftShubh Khattry100% (1)

- The Us China Trade Relationship During The Biden Adminsitration PDFDocument7 pagesThe Us China Trade Relationship During The Biden Adminsitration PDFWilliam WulffNo ratings yet

- Peraturan Salinan TranskripDocument2 pagesPeraturan Salinan TranskripWan Muhammad AriefNo ratings yet

- Return and Refund PolicyDocument4 pagesReturn and Refund PolicyChishty Shai NomaniNo ratings yet

- (Financial Accounting & Reporting 2) : Lecture AidDocument19 pages(Financial Accounting & Reporting 2) : Lecture AidMay Grethel Joy PeranteNo ratings yet

- Pricing IntricaciesDocument35 pagesPricing IntricaciesRadhaNo ratings yet

- Resume - Sanchit GoyalDocument1 pageResume - Sanchit GoyaltompaulmarottickalNo ratings yet

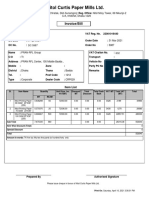

- Nitol Curtis Paper Mills LTD.: Invoice/BillDocument1 pageNitol Curtis Paper Mills LTD.: Invoice/BillMd. Tanvir RahmanNo ratings yet

- Accounts Project Yamini JainDocument57 pagesAccounts Project Yamini Jainbabaraligour234No ratings yet

- "Kuraloane Fab Tech Private Limited" at BangaloreDocument23 pages"Kuraloane Fab Tech Private Limited" at BangaloreCHANDAN CHANDUNo ratings yet

- Module 3 QUALITY MANAGEMENTDocument17 pagesModule 3 QUALITY MANAGEMENTThippesh GNNo ratings yet

- Null 8Document4 pagesNull 8Baqar BaigNo ratings yet

- Design and Fabrication of Grain Separator Using Solar Energy Project Reference No: 38S0809Document4 pagesDesign and Fabrication of Grain Separator Using Solar Energy Project Reference No: 38S0809roronoa zoroNo ratings yet

- 3 8 2021 Ae00007406537cgbDocument2 pages3 8 2021 Ae00007406537cgbAshley GreenNo ratings yet

- Full Name: Example 1 No Summary Statement and Education Listed After ExperienceDocument3 pagesFull Name: Example 1 No Summary Statement and Education Listed After ExperienceGarimaBhandariNo ratings yet

- Lecture 5 Farming System Components-Cropping SystemsDocument31 pagesLecture 5 Farming System Components-Cropping SystemsTabasum BhatNo ratings yet

- Working Capital Management: Investment Decision Financing DecisionDocument41 pagesWorking Capital Management: Investment Decision Financing DecisionMazen SalahNo ratings yet

- 8215 Almagtome 2019 E R1Document21 pages8215 Almagtome 2019 E R1Gabriela LFNo ratings yet

- 3.13 Pirovano v. Dela Rama Steamship Co., 96 P 335Document19 pages3.13 Pirovano v. Dela Rama Steamship Co., 96 P 335Sam ConcepcionNo ratings yet

- Vocabulary For MeetingsDocument3 pagesVocabulary For MeetingsMarcia OhtaNo ratings yet

- Brealey 9 e IPPTCh 07Document44 pagesBrealey 9 e IPPTCh 07haidarNo ratings yet

- SKF Spectraseal: Sealing Solutions For Extreme Application ChallengesDocument5 pagesSKF Spectraseal: Sealing Solutions For Extreme Application ChallengesmiguelNo ratings yet

- Market Positioning Assignment PDFDocument5 pagesMarket Positioning Assignment PDFazar emraanNo ratings yet

- R12.2.10 TOI Implement - and - Use Cost Management - Cost Management Command CenterDocument27 pagesR12.2.10 TOI Implement - and - Use Cost Management - Cost Management Command CenterPrasannaNo ratings yet

- DDD Dodd: D CDDD DDocument2 pagesDDD Dodd: D CDDD DPRINCE KUMARNo ratings yet

- LogisticsDocument15 pagesLogisticsAbdiNo ratings yet

- Linear ProgrammingDocument3 pagesLinear ProgrammingthinkiitNo ratings yet