Download as pdf or txt

You might also like

- ChargeBack Order ABH-122009-CO101 PDFDocument2 pagesChargeBack Order ABH-122009-CO101 PDFAllen-nelson of the Boisjoli family100% (2)

- BC BondDocument1 pageBC Bondtaylor falcone100% (2)

- Claim On The NameDocument1 pageClaim On The NamepattyobornNo ratings yet

- HHIADocument4 pagesHHIAKeith Alden100% (6)

- Documentary Schedule SamplesDocument2 pagesDocumentary Schedule Samplesgalal2720006810No ratings yet

- W 8ben FormDocument2 pagesW 8ben FormrichblackNo ratings yet

- Wakefit Water Proof Terry Cotton Mattress ProtectorDocument1 pageWakefit Water Proof Terry Cotton Mattress ProtectorArunNo ratings yet

- Main Wire Transfer FormDocument2 pagesMain Wire Transfer FormThierry Nhamo100% (1)

- Certified Mail #: RE: Account #4447962301858167Document1 pageCertified Mail #: RE: Account #4447962301858167DEVNo ratings yet

- Basic Surrender and UnderstandingDocument3 pagesBasic Surrender and Understandingddrazen11No ratings yet

- BC Bond John Doe TemplateDocument1 pageBC Bond John Doe TemplateDarioNo ratings yet

- Final DeterminationDocument1 pageFinal DeterminationtonyNo ratings yet

- H H I A: OLD Armless AND Ndemnity Greement No. 05091989QNWHHIA Non Negotiable Between The PartiesDocument4 pagesH H I A: OLD Armless AND Ndemnity Greement No. 05091989QNWHHIA Non Negotiable Between The PartiesQueenNicole Williams100% (1)

- Recording Cover Sheet PDFDocument1 pageRecording Cover Sheet PDFSalaam Bey®No ratings yet

- Offset & Discharge BondDocument6 pagesOffset & Discharge Bondtrust2386No ratings yet

- Cover Letter: Notice To Principal Is Notice To Agent Notice To Agent Is Notice To PrincipalDocument2 pagesCover Letter: Notice To Principal Is Notice To Agent Notice To Agent Is Notice To PrincipalSultana Latisah ElBeyNo ratings yet

- Northridge HOA Affidavit of UCC1 Financing Statement Lien Macn-R00154noaDocument8 pagesNorthridge HOA Affidavit of UCC1 Financing Statement Lien Macn-R00154noaDiane Peeples ElNo ratings yet

- Notice of StandingDocument1 pageNotice of StandingGee PennNo ratings yet

- October 24 2018: Copies: Secretary of The Treasury John Snow, 1500 Pennsylvania Avenue NW, Washington D.C. 20220Document2 pagesOctober 24 2018: Copies: Secretary of The Treasury John Snow, 1500 Pennsylvania Avenue NW, Washington D.C. 20220Sultana Latisah ElBeyNo ratings yet

- 8 NEW UCC 1 Sample Text 1-15-11Document1 page8 NEW UCC 1 Sample Text 1-15-11party24100% (2)

- Bond Kapready TREASURY - OdtDocument1 pageBond Kapready TREASURY - OdtThomas campbellNo ratings yet

- Proof of Delivery COVER LETTERDocument1 pageProof of Delivery COVER LETTERBen Hill100% (1)

- Setoff BondDocument2 pagesSetoff BondCarolina Baltazar Edwards100% (5)

- Universal Sovereign Affidavit of Fact Notice of Default VANGUARD CORPORATION 9-7-22Document3 pagesUniversal Sovereign Affidavit of Fact Notice of Default VANGUARD CORPORATION 9-7-22stonsome100% (1)

- 2009 2410488 607793 U 20090914 PuuscanDocument25 pages2009 2410488 607793 U 20090914 Puuscan:Nanya-Ahk:Heru-El(R)(C)TM100% (1)

- 1-5c List of Collateral - Rdw09221985loc0001Document5 pages1-5c List of Collateral - Rdw09221985loc0001RICHARDDWASHINGTONNo ratings yet

- Death Certificate Template 23Document1 pageDeath Certificate Template 23Luke ElbertNo ratings yet

- Indemnity BondDocument5 pagesIndemnity Bondtrust2386No ratings yet

- Fidelity BondDocument2 pagesFidelity BondBhushan Paralkar100% (1)

- The Note Sample KaronDocument1 pageThe Note Sample KaronYarod YisraelNo ratings yet

- Letter of Credit FormDocument3 pagesLetter of Credit Formwidyarahmadesbita100% (1)

- Power of AttorneytempDocument3 pagesPower of Attorneytemplyocco1100% (1)

- United States Post Office Creditor BondDocument14 pagesUnited States Post Office Creditor BondSia Meri Rah El100% (3)

- Sf181 Government Ethnicity FormDocument1 pageSf181 Government Ethnicity FormQreus One100% (1)

- Registered Mail # RB XXX XXX XXX Us: in Camera Civilian Due Process RequiredDocument2 pagesRegistered Mail # RB XXX XXX XXX Us: in Camera Civilian Due Process RequiredDUTCH551400No ratings yet

- W8Ben With US Mailing (FILLABLE)Document2 pagesW8Ben With US Mailing (FILLABLE)Veronica Mtz100% (1)

- Sample Fraud Private Bond PDFDocument1 pageSample Fraud Private Bond PDFBrien JeffersonNo ratings yet

- Empire Ucc1 Fillable Form1 Straw Lien Ucc1 Kimki ElDocument1 pageEmpire Ucc1 Fillable Form1 Straw Lien Ucc1 Kimki Elkimki makita elNo ratings yet

- Actual &V Constructive Legal NoticeDocument2 pagesActual &V Constructive Legal NoticeDarrell Wilson100% (2)

- v888 Request by An Individual For Information About A Vehicle PDFDocument2 pagesv888 Request by An Individual For Information About A Vehicle PDFmxckcxzlm.c,0% (1)

- DT 2008 990Document53 pagesDT 2008 990shimeralumNo ratings yet

- T + R999999999-Affidavavid of The National Trust 01-17-22signed and FingerprintedDocument2 pagesT + R999999999-Affidavavid of The National Trust 01-17-22signed and Fingerprintedakil kemnebi easley elNo ratings yet

- Blakely Amended Motion For Bond Pending SentencingDocument2 pagesBlakely Amended Motion For Bond Pending SentencingFOX54 News Huntsville100% (1)

- CBV Collections Notice of Demand To Cease and Desist To All CreditorsDocument3 pagesCBV Collections Notice of Demand To Cease and Desist To All CreditorskrystalmarienymannNo ratings yet

- Fom 91Document1 pageFom 91Dave EatonNo ratings yet

- Macn-A000130710 - All Debtor U.S. Corporations, Affiavit - No Bills Are DueDocument3 pagesMacn-A000130710 - All Debtor U.S. Corporations, Affiavit - No Bills Are Duetheodore moses antoine bey100% (1)

- Affidavit of Corporate Death PenaltyDocument2 pagesAffidavit of Corporate Death PenaltyAmir Hassan El100% (2)

- TCUs TRUST CAPITAL UNITS BLUE BORDER EDITABLE1Document1 pageTCUs TRUST CAPITAL UNITS BLUE BORDER EDITABLE1Kevin100% (1)

- TREASURY Creditor BOND Tymon WillisDocument13 pagesTREASURY Creditor BOND Tymon Willisakua vitae elNo ratings yet

- Property ListDocument4 pagesProperty ListMichael Kovach100% (1)

- COVID19 Estate LetterDocument22 pagesCOVID19 Estate Letter:Nikolaj: Færch.100% (1)

- Florida Name Change Petition and OrderDocument5 pagesFlorida Name Change Petition and OrderRocketLawyerNo ratings yet

- Miller Et Al V Homecomings FinDocument22 pagesMiller Et Al V Homecomings FinA. CampbellNo ratings yet

- 1-5d Non Negotiable Security Agmt - RDW09221985NNSA0001Document1 page1-5d Non Negotiable Security Agmt - RDW09221985NNSA0001RICHARDDWASHINGTONNo ratings yet

- Notice of Intent To LienDocument2 pagesNotice of Intent To LienDemetrius BeyNo ratings yet

- UCC11Document2 pagesUCC11stdlns134410No ratings yet

- Constitution of the State of Minnesota — 1876 VersionFrom EverandConstitution of the State of Minnesota — 1876 VersionNo ratings yet

- The Constitutional Case for Religious Exemptions from Federal Vaccine MandatesFrom EverandThe Constitutional Case for Religious Exemptions from Federal Vaccine MandatesNo ratings yet

- Constitution of the State of Minnesota — 1974 VersionFrom EverandConstitution of the State of Minnesota — 1974 VersionNo ratings yet

- PWC Tax Memorandum 2013 PDFDocument64 pagesPWC Tax Memorandum 2013 PDFMuhammad Sohail MalikNo ratings yet

- Pagcor Vs BirDocument2 pagesPagcor Vs BirMarie ChieloNo ratings yet

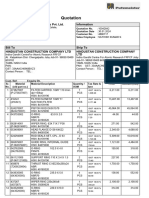

- Quotation: Putzmeister Concrete Machines Pvt. Ltd. InformationDocument4 pagesQuotation: Putzmeister Concrete Machines Pvt. Ltd. InformationsathishNo ratings yet

- Zillion TV CorporationDocument1 pageZillion TV Corporationmdaniels1901No ratings yet

- Accounting For Capital Project FundsDocument8 pagesAccounting For Capital Project FundsMeklit AlemNo ratings yet

- ShaferDocument29 pagesShaferFrederick BartlettNo ratings yet

- Capital Gains TaxDocument9 pagesCapital Gains TaxPmbNo ratings yet

- Arrears Relief Calculator For W.B.govt Employees 2Document4 pagesArrears Relief Calculator For W.B.govt Employees 2Rana BiswasNo ratings yet

- Starting A Business in The UK As A ForeignerDocument8 pagesStarting A Business in The UK As A ForeignerThe SmartMove2UkNo ratings yet

- Difference Between Trust and SocietyDocument2 pagesDifference Between Trust and SocietyNancy GirdherNo ratings yet

- Mali ResumeDocument2 pagesMali Resumeshashikantpatil24No ratings yet

- Salary Slip (31692490 April, 2017)Document1 pageSalary Slip (31692490 April, 2017)Muhamm Jamshed Zarrar50% (2)

- Intermediate Accounting III ReviewerDocument3 pagesIntermediate Accounting III ReviewerRenalyn PascuaNo ratings yet

- Income From HPDocument8 pagesIncome From HPNidaNo ratings yet

- Hindware Chimney InvoiceDocument1 pageHindware Chimney InvoiceSayantan GhoshNo ratings yet

- Deutsche Bank Ag Manila Branch v. CirDocument3 pagesDeutsche Bank Ag Manila Branch v. Circhappy_leigh118No ratings yet

- Ms - Dhanshree Babanrao Wankhede Sbi 21-22Document1 pageMs - Dhanshree Babanrao Wankhede Sbi 21-22Dhanshree WankhedeNo ratings yet

- 621213320531883RPOSDocument2 pages621213320531883RPOSSIVA KRISHNA PRASAD ARJANo ratings yet

- Aditya Techno Fab EngineeringDocument1 pageAditya Techno Fab Engineeringdherendra chhadodiNo ratings yet

- Chapter 3 Agriculture Allowance StudntDocument22 pagesChapter 3 Agriculture Allowance StudntCharmaine Deirdre DaveNo ratings yet

- Tax Code Declaration: 1 Your DetailsDocument4 pagesTax Code Declaration: 1 Your DetailsAmy YoungNo ratings yet

- Invoice 39618325Document1 pageInvoice 39618325sam huangNo ratings yet

- Tax AssignmentDocument6 pagesTax AssignmentCarlos Takudzwa MudzengerereNo ratings yet

- Challenges of Tax Administration EvidenceDocument69 pagesChallenges of Tax Administration EvidenceJohn Bates Blankson0% (1)

- Kenya The Finance Bill 2024Document7 pagesKenya The Finance Bill 2024victor namwetakoNo ratings yet

- Muestra MASDocument132 pagesMuestra MASJohaderNo ratings yet

- Coral Bay Nickel v. CIR PDFDocument10 pagesCoral Bay Nickel v. CIR PDFLiz KawiNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Nitesh MamgainNo ratings yet

- Factors Influencing Tax EvasionDocument59 pagesFactors Influencing Tax EvasionLyka Trisha Uy SagoliliNo ratings yet