Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Accrued Expenses: Practice Question # 1Document4 pagesAccrued Expenses: Practice Question # 1Shoaib AslamNo ratings yet

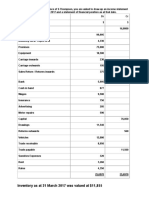

- Inventory As at 31 March 2017 Was Valued at $11,855Document2 pagesInventory As at 31 March 2017 Was Valued at $11,855Shoaib AslamNo ratings yet

- Scan 0002Document1 pageScan 0002Shoaib AslamNo ratings yet

- Solution: 14.8 Advantages and Uses of Control AccountsDocument1 pageSolution: 14.8 Advantages and Uses of Control AccountsShoaib AslamNo ratings yet

- Control Accounts: Example 5Document1 pageControl Accounts: Example 5Shoaib AslamNo ratings yet

- Sample of Revision Plan - 10-cDocument3 pagesSample of Revision Plan - 10-cShoaib AslamNo ratings yet

- As Level Accounting Topic 1 OddDocument45 pagesAs Level Accounting Topic 1 OddShoaib AslamNo ratings yet

- Time Table IX M CrimsonDocument2 pagesTime Table IX M CrimsonShoaib AslamNo ratings yet

- Principles of Accounts: GCE Ordinary Level (2017) (Syllabus 7175)Document48 pagesPrinciples of Accounts: GCE Ordinary Level (2017) (Syllabus 7175)Shoaib AslamNo ratings yet

- RTP Group 1Document129 pagesRTP Group 1sandhya vNo ratings yet

- S1.16 - Receivable Financing - StudentDocument8 pagesS1.16 - Receivable Financing - StudentCyndy Villapando100% (1)

- Indigo ProspectusDocument557 pagesIndigo Prospectusvbt999123yahoo100% (1)

- On IFRS, US GAAP and Indian GAAPDocument64 pagesOn IFRS, US GAAP and Indian GAAPrishipath100% (1)

- FR MCQs - Ind AS Puzzlers - Module 1Document8 pagesFR MCQs - Ind AS Puzzlers - Module 1CA8512No ratings yet

- InventoriesDocument64 pagesInventoriesJoey WassigNo ratings yet

- Business Finance 1st WeekDocument11 pagesBusiness Finance 1st WeekErleNo ratings yet

- 3.6 ExercisesDocument8 pages3.6 ExercisesGeorgios MilitsisNo ratings yet

- SOCPA IFRS Transition ProjectDocument51 pagesSOCPA IFRS Transition ProjectArslan Zafar0% (1)

- DSP Mutual FundDocument5 pagesDSP Mutual FundSarika AroteNo ratings yet

- Executive Compensation in World's Largest Corporations Increases by 5.5%Document2 pagesExecutive Compensation in World's Largest Corporations Increases by 5.5%Dumitru ErhanNo ratings yet

- IOI Properties Group Berhad Annual Report 2016 (Front Cover - Page 29)Document31 pagesIOI Properties Group Berhad Annual Report 2016 (Front Cover - Page 29)Jamuna BatumalaiNo ratings yet

- UTS Aplikasi Manajemen Keuangan Take HomeDocument10 pagesUTS Aplikasi Manajemen Keuangan Take HomeRifan Herwandi FauziNo ratings yet

- FAR 3MC The Conceptual Framework of Financial ReportingDocument4 pagesFAR 3MC The Conceptual Framework of Financial ReportingJoy Dhemple LambacoNo ratings yet

- Income Taxation NotesDocument15 pagesIncome Taxation NotesJustin Andre SiguanNo ratings yet

- Test 1-Unit-18 (SV)Document8 pagesTest 1-Unit-18 (SV)Phan Ha MyNo ratings yet

- Accounting For Receivables: Both AR and NR Are Called Trade ReceivablesDocument7 pagesAccounting For Receivables: Both AR and NR Are Called Trade ReceivablesKhaled Abo YousefNo ratings yet

- Financial RatiosDocument1 pageFinancial RatiosJEANNo ratings yet

- Pami Equity Index Fund: Value of P5,000 Invested Since InceptionDocument1 pagePami Equity Index Fund: Value of P5,000 Invested Since InceptionNoah BrionesNo ratings yet

- Profile of Sonali BankDocument24 pagesProfile of Sonali BankRahi RebaNo ratings yet

- Public Alert Unregistered Soliciting EntitiesDocument9 pagesPublic Alert Unregistered Soliciting EntitiesForkLogNo ratings yet

- Capital Budgeting: An Insight ToDocument26 pagesCapital Budgeting: An Insight Torjrahuljain100% (2)

- Problem Set 1 Answer KeyDocument8 pagesProblem Set 1 Answer KeyVicNo ratings yet

- Mauboussin - Does The M&a Boom Mean Anything For The MarketDocument6 pagesMauboussin - Does The M&a Boom Mean Anything For The MarketRob72081No ratings yet

- PT Metro Healthcare Indonesia TBK 31 December 2022Document91 pagesPT Metro Healthcare Indonesia TBK 31 December 2022Fanniya Dyah PrameswariNo ratings yet

- FNSACC507 7 Task 2 - Case Study and Practical AssessmentDocument3 pagesFNSACC507 7 Task 2 - Case Study and Practical AssessmentnattyNo ratings yet

- Bentuk Bentuk Badan Usaha-1Document28 pagesBentuk Bentuk Badan Usaha-1y_fihartiniNo ratings yet

- Pamantasan NG CabuyaoDocument2 pagesPamantasan NG CabuyaoHhhhhNo ratings yet

- American International University - Bangladesh: Q $45,000 Q Jewelry StoreDocument5 pagesAmerican International University - Bangladesh: Q $45,000 Q Jewelry StoreWahidul Alam SrijonNo ratings yet

- Income Statement and Financial PerformanceDocument29 pagesIncome Statement and Financial PerformancePetrinaNo ratings yet