Download as docx, pdf, or txt

You might also like

- Share and Share CapitalDocument6 pagesShare and Share CapitalDanish KhattarNo ratings yet

- Maneesh Capstone 2 FinalDocument45 pagesManeesh Capstone 2 FinalRakesh SinghNo ratings yet

- Enterprise and Venture CapitalDocument336 pagesEnterprise and Venture CapitalvadymkochNo ratings yet

- SAP Best Practice Design - S4HANA 1709 Transfer Prices.v1Document71 pagesSAP Best Practice Design - S4HANA 1709 Transfer Prices.v1DipomoySaha100% (1)

- Company Share Capital 2020Document26 pagesCompany Share Capital 2020Levin makokhaNo ratings yet

- Fa Unit 4Document13 pagesFa Unit 4VTNo ratings yet

- What Are Preferred SharesDocument9 pagesWhat Are Preferred SharesMariam LatifNo ratings yet

- BMS CL Unit 4Document30 pagesBMS CL Unit 4RKS KRNo ratings yet

- Share CapitalDocument4 pagesShare Capital20AH419 Talukdar DebanjanaNo ratings yet

- Share CapitalDocument17 pagesShare Capitalzydeco.14No ratings yet

- FINMAN 102 Module-IIDocument27 pagesFINMAN 102 Module-IIzehra我No ratings yet

- Kinds of Shares Legal AspectsDocument12 pagesKinds of Shares Legal AspectsAhmad Nadeem MohammadiNo ratings yet

- Share 3Document19 pagesShare 3manishchaudhary3537No ratings yet

- Issue of SharesDocument19 pagesIssue of SharesBhupender Singh Kaushal100% (16)

- Meaning:: Difference Between Equity Shares and Preference SharesDocument7 pagesMeaning:: Difference Between Equity Shares and Preference SharesAnkita ModiNo ratings yet

- Chapter-4 Capital Market and Mone Market InstrumentsDocument24 pagesChapter-4 Capital Market and Mone Market InstrumentsaswinecebeNo ratings yet

- CL PB SLD8Document79 pagesCL PB SLD8Pooja ChatleyNo ratings yet

- L35 - 36share Capital and Its AlterationDocument27 pagesL35 - 36share Capital and Its AlterationSudhanshu Kumar SinghNo ratings yet

- Legal Aspect of Business AssignmentDocument25 pagesLegal Aspect of Business AssignmentUBSHimanshu KumarNo ratings yet

- Course Code: COM-405 Course Title: Credit Hours: 3 (3-0) : Introduction To Business FinanceDocument20 pagesCourse Code: COM-405 Course Title: Credit Hours: 3 (3-0) : Introduction To Business FinanceSajjad AhmadNo ratings yet

- Co. Ltd. 1901) : Hare AND Hare ApitalDocument16 pagesCo. Ltd. 1901) : Hare AND Hare ApitalNavya BhandariNo ratings yet

- EquityDocument17 pagesEquityItronix MohaliNo ratings yet

- Issue of SharesDocument16 pagesIssue of SharesAdan HoodaNo ratings yet

- Shares & DebenturesDocument7 pagesShares & DebenturesKARISHMA RAJNo ratings yet

- Shares and Share CapitalDocument16 pagesShares and Share Capitalvamsibu100% (2)

- Share CapDocument29 pagesShare CapRabbikaNo ratings yet

- FM AssignmentDocument25 pagesFM Assignmentsamy7541No ratings yet

- Share Capital & TypesDocument13 pagesShare Capital & TypesHarvinder Singh100% (1)

- Extra Reading Lecture 02Document17 pagesExtra Reading Lecture 02iragouldNo ratings yet

- Equity Share and Its TypesDocument4 pagesEquity Share and Its TypeslakshmibabymaniNo ratings yet

- Share, Capital & BorrowingDocument26 pagesShare, Capital & BorrowingshahneelahmedNo ratings yet

- Amity University Rajasthan: Brief Description On SharesDocument7 pagesAmity University Rajasthan: Brief Description On SharesSahida ParveenNo ratings yet

- Unit 2 - Part 2Document19 pagesUnit 2 - Part 2Ridhima AggarwalNo ratings yet

- Preference SharesDocument7 pagesPreference Sharesmayuresh bariNo ratings yet

- Types of SharesDocument13 pagesTypes of SharesGaurav GuptaNo ratings yet

- Classes of Share and Corporate CapitalDocument2 pagesClasses of Share and Corporate CapitalChristian NavalesNo ratings yet

- Final AssignmentDocument51 pagesFinal AssignmentNaveeda RiazNo ratings yet

- Shares: Meaning and Nature of SharesDocument9 pagesShares: Meaning and Nature of SharesNeenaNo ratings yet

- Additional Paid-In CapitalDocument5 pagesAdditional Paid-In CapitalBR Lake City LHRNo ratings yet

- Materi PPT Bing SharesDocument3 pagesMateri PPT Bing SharesSyifa UrrohmahNo ratings yet

- Materi PPT Bing SharesDocument3 pagesMateri PPT Bing SharesSyifa UrrohmahNo ratings yet

- Shareholders Rights, Dividend Payment andDocument16 pagesShareholders Rights, Dividend Payment andSachin PatilNo ratings yet

- Financial Accounting Class: Bba Ii Submitted To: Sir Ghulam Mustafa Shaikh Submitted By: Sarah Khan Chandio Registration No: 0911120Document5 pagesFinancial Accounting Class: Bba Ii Submitted To: Sir Ghulam Mustafa Shaikh Submitted By: Sarah Khan Chandio Registration No: 0911120wajid2345No ratings yet

- Share and Types of ShareDocument10 pagesShare and Types of Sharesivaramjayaprakash26No ratings yet

- FM Unit 4 - Dr. Anuradha HDocument46 pagesFM Unit 4 - Dr. Anuradha HBsdk TmkcNo ratings yet

- Shares: Presentation BY Mahender VijaypalDocument24 pagesShares: Presentation BY Mahender VijaypalHemant AgarwalNo ratings yet

- HSC SP Q.8. Answer The FollowingDocument11 pagesHSC SP Q.8. Answer The FollowingTanya SinghNo ratings yet

- MBA 3.5-4th-BUSA4140-10Document16 pagesMBA 3.5-4th-BUSA4140-10Salman AliNo ratings yet

- A Project Report On: Factor-AnalysisDocument53 pagesA Project Report On: Factor-Analysisswati_poddarNo ratings yet

- Preference SharesDocument3 pagesPreference SharesDipti AryaNo ratings yet

- Share MarketDocument48 pagesShare MarketHariharan SamyNo ratings yet

- Types of SecuritiesDocument12 pagesTypes of SecuritiesgauravNo ratings yet

- ASSIGNMENT OF SHARES - Qodir - 02 - 22feb2021Document3 pagesASSIGNMENT OF SHARES - Qodir - 02 - 22feb2021Boss SyihabNo ratings yet

- Budget PDFDocument55 pagesBudget PDFMONIKA R PSGRKCWNo ratings yet

- Shares and Its Types - IndiaDocument2 pagesShares and Its Types - IndiaGaurav TiwariNo ratings yet

- Introduction To SHARESDocument6 pagesIntroduction To SHARESShristi thakurNo ratings yet

- Sources of FinanceDocument29 pagesSources of FinanceVJ FirozNo ratings yet

- Sources of FinanceDocument7 pagesSources of FinanceVJ FirozNo ratings yet

- Share CapitalDocument3 pagesShare Capitalsarath cmNo ratings yet

- PM CH - ViDocument31 pagesPM CH - ViTemesgen DibaNo ratings yet

- Dividend Investing for Beginners & DummiesFrom EverandDividend Investing for Beginners & DummiesRating: 5 out of 5 stars5/5 (1)

- Stocks: An Essential Guide To Investing In The Stock Market And Learning The Sophisticated Investor Money Making SystemFrom EverandStocks: An Essential Guide To Investing In The Stock Market And Learning The Sophisticated Investor Money Making SystemRating: 5 out of 5 stars5/5 (3)

- Foreign Exchange Regulation ActDocument3 pagesForeign Exchange Regulation ActHIMANSHU DARGANNo ratings yet

- Sales & Retail MGMTDocument31 pagesSales & Retail MGMTHIMANSHU DARGANNo ratings yet

- Role of Indian Ethos in ManagerialDocument5 pagesRole of Indian Ethos in ManagerialHIMANSHU DARGANNo ratings yet

- Personal Selling Part 2Document9 pagesPersonal Selling Part 2HIMANSHU DARGANNo ratings yet

- BAILMENTDocument15 pagesBAILMENTHIMANSHU DARGANNo ratings yet

- Personal Selling Part 1Document26 pagesPersonal Selling Part 1HIMANSHU DARGAN100% (1)

- PACKAGINGDocument4 pagesPACKAGINGHIMANSHU DARGANNo ratings yet

- Media PlanningDocument5 pagesMedia PlanningHIMANSHU DARGANNo ratings yet

- Methods For Setting Advertising BudgetDocument11 pagesMethods For Setting Advertising BudgetHIMANSHU DARGANNo ratings yet

- Types of Production SystemDocument4 pagesTypes of Production SystemHIMANSHU DARGANNo ratings yet

- Four Types of Production: Page Contents Example of Unit Type of ProductionDocument3 pagesFour Types of Production: Page Contents Example of Unit Type of ProductionHIMANSHU DARGANNo ratings yet

- UNIT IV Material ManagementDocument3 pagesUNIT IV Material ManagementHIMANSHU DARGANNo ratings yet

- Product DesignDocument2 pagesProduct DesignHIMANSHU DARGANNo ratings yet

- DIRECTIN1Document20 pagesDIRECTIN1HIMANSHU DARGANNo ratings yet

- Forecasting: Forecasting Is A Process of Predicting or Estimating The Future Based On Past and Present DataDocument5 pagesForecasting: Forecasting Is A Process of Predicting or Estimating The Future Based On Past and Present DataHIMANSHU DARGANNo ratings yet

- Regional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerDocument2 pagesRegional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerCynthia ChandlerNo ratings yet

- Bermuda Segregated Accounts Companies-BDADocument15 pagesBermuda Segregated Accounts Companies-BDADecimusBlueNo ratings yet

- A Complete Set of Financial Statements ComprisesDocument9 pagesA Complete Set of Financial Statements Comprisesۦۦۦۦۦ ۦۦ ۦۦۦNo ratings yet

- FWD: Nesl - Request To Authenticate: Nesliu@Nesl - Co.InDocument2 pagesFWD: Nesl - Request To Authenticate: Nesliu@Nesl - Co.InSagar GuptaNo ratings yet

- Microfinance in India - A Tool For Poverty ReductionDocument20 pagesMicrofinance in India - A Tool For Poverty ReductionVijay KumarNo ratings yet

- Entrepreneurship and Business Ownership: COMM 1010: Business in A Global ContextDocument15 pagesEntrepreneurship and Business Ownership: COMM 1010: Business in A Global ContextAbeer ArifNo ratings yet

- Most Common Forms of Negotiable InstrumentDocument4 pagesMost Common Forms of Negotiable InstrumentJeanne CalalinNo ratings yet

- Company Set Up and OrganizationDocument11 pagesCompany Set Up and OrganizationAtikah JembariNo ratings yet

- FI - Fall 2020 - PPT Slides - IntroductionDocument27 pagesFI - Fall 2020 - PPT Slides - IntroductionBabar MairajNo ratings yet

- IC AvailmentForm Mar2019 NC PDFDocument1 pageIC AvailmentForm Mar2019 NC PDFVerghie Ariza FloresNo ratings yet

- BAM - OCT 2021 - 2pagesDocument2 pagesBAM - OCT 2021 - 2pagesTincho PreitiNo ratings yet

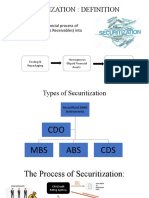

- SECURITIZATIONDocument5 pagesSECURITIZATIONASHISH KUMARNo ratings yet

- Nature of A PartnershipDocument27 pagesNature of A PartnershipschafieqahNo ratings yet

- A Study On Regestration and Taxation Services of Lal & AssociatesDocument43 pagesA Study On Regestration and Taxation Services of Lal & AssociatesSOURAV GOYALNo ratings yet

- Practice Question 2 RPGT & RPC Oct 2022Document1 pagePractice Question 2 RPGT & RPC Oct 2022FeahRafeah KikiNo ratings yet

- Dozier Industries (A)Document8 pagesDozier Industries (A)Ayaz Ul HaqNo ratings yet

- Adobe Scan 14 Apr 2023Document1 pageAdobe Scan 14 Apr 2023srii21rohithNo ratings yet

- Analisis Laporan Keuangan Untuk Menilai Kinerja Keuangan Perusahaan PT. Ultrajaya Milk Industry, TBKDocument6 pagesAnalisis Laporan Keuangan Untuk Menilai Kinerja Keuangan Perusahaan PT. Ultrajaya Milk Industry, TBKMeirza FazriyahNo ratings yet

- Partnership - Principles of AccountingDocument9 pagesPartnership - Principles of AccountingAbdulla MaseehNo ratings yet

- Residential StatusDocument8 pagesResidential StatusUthra PandianNo ratings yet

- Assignment # 4Document4 pagesAssignment # 4Butt ArhamNo ratings yet

- FSA Vertical FormatDocument10 pagesFSA Vertical FormatMayank BahetiNo ratings yet

- Unit 4Document3 pagesUnit 4Mukul KumarNo ratings yet

- Almeda vs. CADocument7 pagesAlmeda vs. CAAnonymous oDPxEkdNo ratings yet

- Investment Appraisal-Fm AccaDocument11 pagesInvestment Appraisal-Fm AccaCorrinaNo ratings yet

- Financial and Monetary System of BangladeshDocument24 pagesFinancial and Monetary System of BangladeshM.g. Mostofa OheeNo ratings yet

- Engro's Annual Report 2008Document189 pagesEngro's Annual Report 2008shahidamin1100% (2)