Download as pdf or txt

You might also like

- 9706 - m24 - QP - 22 - Acc p2 Feb March 24Document20 pages9706 - m24 - QP - 22 - Acc p2 Feb March 24Shaamikh RilwanNo ratings yet

- Euroland Foods Case SolutionDocument5 pagesEuroland Foods Case SolutionAzwimar Putranusa75% (4)

- 2020 Bafs Dse Paper 1 and 2A EngDocument21 pages2020 Bafs Dse Paper 1 and 2A EngwwlNo ratings yet

- Definition of Supply Under GSTDocument8 pagesDefinition of Supply Under GSTRohit Bajpai100% (1)

- Income From SalaryDocument26 pagesIncome From SalaryAkash VisputeNo ratings yet

- New Product DevelopmentDocument18 pagesNew Product DevelopmentSarvar PathanNo ratings yet

- Exempt IncomeDocument18 pagesExempt IncomeSarvar PathanNo ratings yet

- Tuesday 2 June 2020: BusinessDocument20 pagesTuesday 2 June 2020: BusinessAdeeba iqbal100% (2)

- Wealth TaxDocument5 pagesWealth TaxsadathnooriNo ratings yet

- 6 ItcDocument114 pages6 ItcRAUNAQ SHARMANo ratings yet

- Direct Tax Vs Indirect TaxDocument44 pagesDirect Tax Vs Indirect TaxShuchi BhatiaNo ratings yet

- Deduction Under Income TaxDocument57 pagesDeduction Under Income Taxmalayali100No ratings yet

- Tax PPT - DeductionsDocument20 pagesTax PPT - Deductionsjayparekh28No ratings yet

- Reverse Charge Mechanism in GST Regime With ChartDocument14 pagesReverse Charge Mechanism in GST Regime With ChartAnkur ShahNo ratings yet

- Unit 2 - Income From Business or ProfessionDocument13 pagesUnit 2 - Income From Business or ProfessionRakhi DhamijaNo ratings yet

- Chapter 8 - Input Tax Credit - NotesDocument57 pagesChapter 8 - Input Tax Credit - Notesmohd abidNo ratings yet

- GST Registration NotesDocument13 pagesGST Registration NotesNagashree RANo ratings yet

- Numericals On MAT-115JBDocument2 pagesNumericals On MAT-115JBReema Laser100% (1)

- AX Educted at Ource - I: KPPM & AssociatesDocument67 pagesAX Educted at Ource - I: KPPM & AssociatesSaksham JoshiNo ratings yet

- Assessment of Various EntitiesDocument31 pagesAssessment of Various Entitiesinsathi0% (1)

- A Research Paper On Impact of Goods and Service Tax (GST) On Indian Gross Domestic Product (GDP)Document8 pagesA Research Paper On Impact of Goods and Service Tax (GST) On Indian Gross Domestic Product (GDP)archerselevatorsNo ratings yet

- Deduction From Gross Total IncomeDocument29 pagesDeduction From Gross Total Incomegaganhungama007No ratings yet

- 7 - Bcom Benefits of GST To Economy and IndustryDocument13 pages7 - Bcom Benefits of GST To Economy and Industrymnr81No ratings yet

- Concept of Goods & Services Tax ? or Introduction To Goods & Services Tax ? or Explain Goods & Services Tax Act 2017 ?Document2 pagesConcept of Goods & Services Tax ? or Introduction To Goods & Services Tax ? or Explain Goods & Services Tax Act 2017 ?Ranjan BaradurNo ratings yet

- Set of or Carry-11Document11 pagesSet of or Carry-11s4sahithNo ratings yet

- Income Tax Residential Status PDFDocument16 pagesIncome Tax Residential Status PDFNagesha CSNo ratings yet

- Computation of Total IncomeDocument48 pagesComputation of Total IncomeAlphonsaNo ratings yet

- Income From SalaryDocument66 pagesIncome From SalaryShamika LloydNo ratings yet

- Income From Salary (Section 12) : RsDocument8 pagesIncome From Salary (Section 12) : RsKashifNo ratings yet

- Composition Scheme GSTDocument3 pagesComposition Scheme GSTUttiya BasuNo ratings yet

- SalaryDocument29 pagesSalarySarvar PathanNo ratings yet

- Narasimham CommitteeDocument17 pagesNarasimham CommitteeTorsha SahaNo ratings yet

- Basics of Income Tax of India PDFDocument19 pagesBasics of Income Tax of India PDFJai VermaNo ratings yet

- Tax 02Document13 pagesTax 02pj04No ratings yet

- Old Vs New Tax Regime Comparative AnalysisDocument11 pagesOld Vs New Tax Regime Comparative AnalysisAkchu KadNo ratings yet

- Regulation of Certifying AuthoritiesDocument14 pagesRegulation of Certifying AuthoritiesHARSHIT KUMARNo ratings yet

- INCOME TAX AND GST. JURAZ-Module 3Document11 pagesINCOME TAX AND GST. JURAZ-Module 3hisanashanutty2004100% (1)

- CS Professional Programme Tax NotesDocument47 pagesCS Professional Programme Tax NotesRajey Jain100% (2)

- Taxation of Salaried EmployeesDocument39 pagesTaxation of Salaried Employeessailolla30100% (1)

- Introduction Unit of Income TaxDocument5 pagesIntroduction Unit of Income TaxRishabNo ratings yet

- Income From House Property TaxationDocument3 pagesIncome From House Property TaxationAmit Roy100% (1)

- Modes of WindingDocument14 pagesModes of WindingAayushNo ratings yet

- Income From Business or ProfessionDocument7 pagesIncome From Business or ProfessionSwathi JayaprakashNo ratings yet

- Minor Project BcomDocument1 pageMinor Project BcomYash DadheechNo ratings yet

- Composition Scheme SEC 10 - GST PDFDocument20 pagesComposition Scheme SEC 10 - GST PDFTushar SinghNo ratings yet

- Advance RulingDocument16 pagesAdvance Rulingnaggarwal1990No ratings yet

- Chapter 5 Income of Other Persons Included in Assessee S Total IncomeDocument8 pagesChapter 5 Income of Other Persons Included in Assessee S Total IncomeRaj Pati SundiNo ratings yet

- GST NotesDocument22 pagesGST NotesSARATH BABU.YNo ratings yet

- Income Tax Deductions Under Section 80C PDFDocument2 pagesIncome Tax Deductions Under Section 80C PDFArunDanielNo ratings yet

- Chapter 4 - Composition Levy - NotesDocument15 pagesChapter 4 - Composition Levy - Notesmohd abidNo ratings yet

- Profits and Gains of Business or Profession.Document79 pagesProfits and Gains of Business or Profession.Mandira PriyaNo ratings yet

- ExportDocument25 pagesExportBala VinayagamNo ratings yet

- Introduction To Custom Law: Prepared by DR Renu AggarwalDocument13 pagesIntroduction To Custom Law: Prepared by DR Renu AggarwalPramod PrabhasNo ratings yet

- Tax Planning With Respect To Amalgamation and MergersDocument29 pagesTax Planning With Respect To Amalgamation and MergerssadathnooriNo ratings yet

- TCS - in Income TaxDocument8 pagesTCS - in Income TaxrpsinghsikarwarNo ratings yet

- Prof. Ashish R. Chourasiya: Goods & Service Tax: IntroductionDocument36 pagesProf. Ashish R. Chourasiya: Goods & Service Tax: IntroductionAJAY PHENOMNo ratings yet

- Foreign Exchange Management Act 2000Document19 pagesForeign Exchange Management Act 2000Gurvinder AroraNo ratings yet

- Constitutional Validity (Excise Duties, Custom Duties & Service Taxes)Document19 pagesConstitutional Validity (Excise Duties, Custom Duties & Service Taxes)07anshuman100% (2)

- Income From Salary-FinalDocument42 pagesIncome From Salary-FinalPrathibha TiwariNo ratings yet

- Role of Taxation in Equal Distribution of The Economic Resources in A CountryDocument9 pagesRole of Taxation in Equal Distribution of The Economic Resources in A CountrySarada Biswas100% (1)

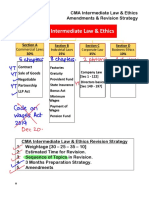

- CMA Intermediate Law & Ethics: Section A 30%Document4 pagesCMA Intermediate Law & Ethics: Section A 30%M RafeeqNo ratings yet

- A Study of Corporate Tax in IndiaDocument27 pagesA Study of Corporate Tax in IndiaKHUSHBOO GOYAL - DMNo ratings yet

- Com.Document24 pagesCom.MALAYALY100% (1)

- Classification of Taxable Income Under Various Heads and Computation of Taxable IncomeDocument4 pagesClassification of Taxable Income Under Various Heads and Computation of Taxable IncomeAnkit Kr MishraNo ratings yet

- Brief History of Banking in IndiaDocument9 pagesBrief History of Banking in IndiaAakriti BhattNo ratings yet

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorFrom EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorNo ratings yet

- E-Way Bill System PDFDocument1 pageE-Way Bill System PDFSarvar PathanNo ratings yet

- Asian Paints (Rakesh Painter)Document2 pagesAsian Paints (Rakesh Painter)Sarvar PathanNo ratings yet

- Mi 4A PRO 80 CM 32 HD Ready LED Smart Android TV With Google Data SaverDocument2 pagesMi 4A PRO 80 CM 32 HD Ready LED Smart Android TV With Google Data SaverSarvar PathanNo ratings yet

- Facility LocationDocument22 pagesFacility LocationSarvar PathanNo ratings yet

- 5b. Capacity PlanningDocument21 pages5b. Capacity PlanningSarvar PathanNo ratings yet

- 1b. Production SystemsDocument13 pages1b. Production SystemsSarvar PathanNo ratings yet

- 1c.OM - Strategy-Rev-2020 - BVRMDocument24 pages1c.OM - Strategy-Rev-2020 - BVRMSarvar PathanNo ratings yet

- Individual Account Opening Form: (Demat + Trading)Document27 pagesIndividual Account Opening Form: (Demat + Trading)Sarvar PathanNo ratings yet

- Salary IllustrationDocument10 pagesSalary IllustrationSarvar Pathan100% (1)

- SalaryDocument29 pagesSalarySarvar PathanNo ratings yet

- Residential Status True or FalseDocument2 pagesResidential Status True or FalseSarvar PathanNo ratings yet

- Acknowledgement of Online Application For Services On Existing DLDocument1 pageAcknowledgement of Online Application For Services On Existing DLSarvar PathanNo ratings yet

- Residential Status MCQDocument6 pagesResidential Status MCQSarvar PathanNo ratings yet

- Residential StatusDocument4 pagesResidential StatusSarvar PathanNo ratings yet

- Important Theory Questions: Tripathi Online EducareDocument1 pageImportant Theory Questions: Tripathi Online EducareSarvar PathanNo ratings yet

- Residential Status FibDocument1 pageResidential Status FibSarvar PathanNo ratings yet

- Income From Other SourcesDocument16 pagesIncome From Other SourcesSarvar PathanNo ratings yet

- Income From Other SourcesDocument10 pagesIncome From Other SourcesSarvar PathanNo ratings yet

- Income From Other Sources IllustrationDocument5 pagesIncome From Other Sources IllustrationSarvar PathanNo ratings yet

- House PropertyDocument17 pagesHouse PropertySarvar PathanNo ratings yet

- House Property 1Document14 pagesHouse Property 1Sarvar Pathan100% (3)

- Capital Gains IllustrationDocument15 pagesCapital Gains IllustrationSarvar PathanNo ratings yet

- DeductionsDocument9 pagesDeductionsSarvar PathanNo ratings yet

- Business IncomeDocument15 pagesBusiness IncomeSarvar PathanNo ratings yet

- Heads of IncomeDocument1 pageHeads of IncomeSarvar PathanNo ratings yet

- Financial Statement:: QuarterlyDocument2 pagesFinancial Statement:: QuarterlyJeraldine RamisoNo ratings yet

- Chapter 3 Ethiopian Tax SystemDocument28 pagesChapter 3 Ethiopian Tax SystemMinaw BelayNo ratings yet

- The Business, Tax, and Financial EnvironmentsDocument58 pagesThe Business, Tax, and Financial EnvironmentsMuhammad Usama IqbalNo ratings yet

- 113.ammonium ChlorideDocument19 pages113.ammonium ChloridetadiyosNo ratings yet

- HR Valuation and AccountingDocument10 pagesHR Valuation and AccountingSanskar YadavNo ratings yet

- Zomato Limited ( Zomato' or Company') - IPO Valuation: "Scaling-Up Challenge"Document7 pagesZomato Limited ( Zomato' or Company') - IPO Valuation: "Scaling-Up Challenge"Rajesh KumarNo ratings yet

- LBR JWB Sesi 2 - CDocument12 pagesLBR JWB Sesi 2 - CAzka RainayokyNo ratings yet

- Financial Accounting GlossaryDocument5 pagesFinancial Accounting GlossaryDheeraj SunthaNo ratings yet

- Financial ReportingDocument103 pagesFinancial ReportingCHARAK RAYNo ratings yet

- Ajanta Pharma PresentatDocument29 pagesAjanta Pharma PresentatBhaskar DasguptaNo ratings yet

- Earning For The Month - April 2023: Jubilant Foodworks LTDDocument1 pageEarning For The Month - April 2023: Jubilant Foodworks LTDnishankithkumarNo ratings yet

- CA Inter FM - Nov 2018 Suggested AnswersDocument14 pagesCA Inter FM - Nov 2018 Suggested Answersrisavey693No ratings yet

- FAR 19MC Provisions Contingent Liabilities and Contingent Assetse 1Document4 pagesFAR 19MC Provisions Contingent Liabilities and Contingent Assetse 1admiral spongebob100% (1)

- Assignment Cover SheetDocument8 pagesAssignment Cover SheetShubashni Sooria Chandra RooNo ratings yet

- ST Andrews Investment Society: SM Prime Holdings, IncDocument5 pagesST Andrews Investment Society: SM Prime Holdings, IncMary EdsylleNo ratings yet

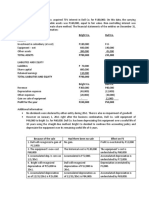

- Ppe ProblemDocument3 pagesPpe ProblemJanuary Ann BeteNo ratings yet

- Ib InfotechDocument3 pagesIb Infotechshivapalle1708No ratings yet

- Accountancy Preparatory ExaminationDocument6 pagesAccountancy Preparatory Examinationclown clNo ratings yet

- Form 15A Licence Under Section 24Document1 pageForm 15A Licence Under Section 24olingirlNo ratings yet

- For Domestic Corporations: 1. Salient Features of The CREATE LawDocument6 pagesFor Domestic Corporations: 1. Salient Features of The CREATE LawJean Tomugdan100% (1)

- Raising Ethical Issues For Icici Bank LTD Ads (Ibn)Document2 pagesRaising Ethical Issues For Icici Bank LTD Ads (Ibn)Asmi KadriNo ratings yet

- Bajaj Holdings & Investments Limited: Holding A Positive GroundDocument7 pagesBajaj Holdings & Investments Limited: Holding A Positive GroundVivek BansalNo ratings yet

- Accounting and Book Keeping NotesDocument15 pagesAccounting and Book Keeping NotesWesley Sang100% (1)

- Josh Tarasoff AmazonDocument7 pagesJosh Tarasoff AmazonDaniel HanasabNo ratings yet

- Spring 2023 Exam CfefdDocument27 pagesSpring 2023 Exam CfefdbenisNo ratings yet

- Capital GainsDocument27 pagesCapital GainsdeepakadhanaNo ratings yet