Download as xlsx, pdf, or txt

You might also like

- Chapter 18 TestbankDocument44 pagesChapter 18 TestbankHuu LuatNo ratings yet

- Bookkeeping ActivitesDocument23 pagesBookkeeping ActivitesRose Darnayla55% (11)

- RESA FAR PreWeek (B43)Document10 pagesRESA FAR PreWeek (B43)MellaniNo ratings yet

- Introduction To Business Processes: Multiple Choice QuestionsDocument162 pagesIntroduction To Business Processes: Multiple Choice QuestionsHuu Luat100% (1)

- BUSI 353 S18 Assignment 6 SOLUTIONDocument4 pagesBUSI 353 S18 Assignment 6 SOLUTIONTanNo ratings yet

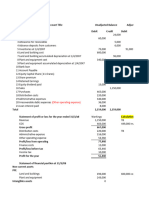

- Total Current Assets $1,405,000 $1,206,000Document2 pagesTotal Current Assets $1,405,000 $1,206,000Renz Barrientos0% (1)

- Advanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Document21 pagesAdvanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Uyên Nguyễn Hoàng ThanhNo ratings yet

- Bba 122 Fai 11 AnswerDocument12 pagesBba 122 Fai 11 AnswerTomi Wayne Malenga100% (1)

- Assets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedDocument6 pagesAssets.: (Vi) Due To Lack of Information, Depreciation Has Not Been Provided On FixedMehul Gupta100% (1)

- Guiding Cfs Lecture PracticeDocument25 pagesGuiding Cfs Lecture PracticeThanh UyênNo ratings yet

- Financial Accounting 2nd AssignmentDocument4 pagesFinancial Accounting 2nd AssignmentedwardfangthuNo ratings yet

- Direct Method - Ocf:: 1/ Sales - AR - Cash Aim? Sales ARDocument23 pagesDirect Method - Ocf:: 1/ Sales - AR - Cash Aim? Sales ARThu Anh NguyenNo ratings yet

- Tuto 6Document6 pagesTuto 6WEI QUAN LEENo ratings yet

- ACT320 Assignment ProjectDocument11 pagesACT320 Assignment ProjectMd. Shakil Ahmed 1620890630No ratings yet

- Case 3.7Document7 pagesCase 3.7Thái SơnNo ratings yet

- Liabilities 31.03.20X1 Rs. 31.03.20X 2 Rs. Assets 31.03.20X 1 Rs. 31.03.20X2 RsDocument3 pagesLiabilities 31.03.20X1 Rs. 31.03.20X 2 Rs. Assets 31.03.20X 1 Rs. 31.03.20X2 RsAmit GodaraNo ratings yet

- CHP 4Document16 pagesCHP 4Beenish JafriNo ratings yet

- Fund Flow Statement: by Dr. Aleem AnsariDocument18 pagesFund Flow Statement: by Dr. Aleem AnsariPRIYAL GUPTANo ratings yet

- Solvay Adv Acc Case 5B (Fiat Lux) - Solution Consolidation Entries Step Acquisition VersionDocument5 pagesSolvay Adv Acc Case 5B (Fiat Lux) - Solution Consolidation Entries Step Acquisition VersionlolaNo ratings yet

- CACell Intermediate Account Full Book-201-250Document50 pagesCACell Intermediate Account Full Book-201-250kalyanikamineniNo ratings yet

- Answer Key Chapter 2 BCDocument18 pagesAnswer Key Chapter 2 BCMerel Rose FloresNo ratings yet

- Tampoa Ae211 Unit 1 Assessment ProblemsDocument12 pagesTampoa Ae211 Unit 1 Assessment ProblemsJahna Kay TampoaNo ratings yet

- FFS & CFSDocument3 pagesFFS & CFSJEBA SCHULZ JNo ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- Applied Auditing-Prelim FinalDocument3 pagesApplied Auditing-Prelim FinalDominic E. BoticarioNo ratings yet

- Week11 Example QuestionDocument2 pagesWeek11 Example Questiongohhs_aaron100% (1)

- Final PB FAR Batch 7 Sept 2023Document38 pagesFinal PB FAR Batch 7 Sept 2023Leo M. SalibioNo ratings yet

- 4-02 - 03 - Andika Fivaldi - Latihan Soal Pertemuan 7Document9 pages4-02 - 03 - Andika Fivaldi - Latihan Soal Pertemuan 7Andika FivaldiNo ratings yet

- Tutorial 3 - Cash Flow Statement (Solutions)Document5 pagesTutorial 3 - Cash Flow Statement (Solutions)swayam palNo ratings yet

- GROUP PROJECT REPORT 1 AmsyarDocument24 pagesGROUP PROJECT REPORT 1 AmsyarAmmarNo ratings yet

- Solution To Q1 Summer 2022Document2 pagesSolution To Q1 Summer 2022dgornik021No ratings yet

- Direct Method - Ocf:: 1/ Sales - AR - Cash Aim? Sales ARDocument4 pagesDirect Method - Ocf:: 1/ Sales - AR - Cash Aim? Sales ARHermione GrangerNo ratings yet

- Multiple Choice ProblemsDocument17 pagesMultiple Choice ProblemsDieter LudwigNo ratings yet

- DSR Mock Test - 1 - Ca FoundationDocument5 pagesDSR Mock Test - 1 - Ca Foundationmaskguy001No ratings yet

- CFAB Chapter12 Full GuidanceDocument74 pagesCFAB Chapter12 Full GuidanceNgân Lê Trần BảoNo ratings yet

- CPA 1 - Financial Acconting Sep 2022Document10 pagesCPA 1 - Financial Acconting Sep 2022Asaba GloriaNo ratings yet

- Solutions and Notes (FAR Review)Document6 pagesSolutions and Notes (FAR Review)Corin Ahmed CorinNo ratings yet

- Cash Flows PAS7Document10 pagesCash Flows PAS7Jenyl Mae NobleNo ratings yet

- Cfs Direct Method - IaDocument35 pagesCfs Direct Method - IaCanny TrầnNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document14 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- Cash and Cash Equivalents Problem 4Document2 pagesCash and Cash Equivalents Problem 4Carel Joy AndalajaoNo ratings yet

- Chap 12 NotesDocument3 pagesChap 12 NotesrbarronsolutionsNo ratings yet

- 1314F-TP5-P9-R1 - 2001660713 - NADIA ANIYA SUDRAJAT - MergeDocument9 pages1314F-TP5-P9-R1 - 2001660713 - NADIA ANIYA SUDRAJAT - MergeLala Lala LalaNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document15 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- Felix Fernando - C13-Q2Document3 pagesFelix Fernando - C13-Q2Steve IdnNo ratings yet

- CFS - 18 Oct 2022Document11 pagesCFS - 18 Oct 2022Kartik SujanNo ratings yet

- CPAR 95 FAR FINAL PB ANSWER KEYDocument7 pagesCPAR 95 FAR FINAL PB ANSWER KEYcaryljoycemaceda3No ratings yet

- June 2009 Fa4a1Document9 pagesJune 2009 Fa4a1ksakala58No ratings yet

- Perpetual Bank: ReceivablesDocument13 pagesPerpetual Bank: ReceivablesYes ChannelNo ratings yet

- Akuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Document2 pagesAkuntansi Keuangan Menengah 2 Asistensi - Tim Asdos Akm 2Muhamad Rizal DinyatNo ratings yet

- Advance Financial Accounting and ReportingDocument25 pagesAdvance Financial Accounting and ReportingEmma Mariz GarciaNo ratings yet

- RIL Excel Sheet FRADocument56 pagesRIL Excel Sheet FRAAditi AgrawalNo ratings yet

- Chapter 08 - Bank and CashDocument13 pagesChapter 08 - Bank and CashMkhonto XuluNo ratings yet

- Bos 28432 CP 10Document45 pagesBos 28432 CP 10hiral dattaniNo ratings yet

- 04 Branch AccountsDocument23 pages04 Branch Accountslasix47725No ratings yet

- 04 Branch Accounts PQ SolDocument24 pages04 Branch Accounts PQ Soltyagivansh1200No ratings yet

- Homework Answer (Quiz 1-2 Revision)Document7 pagesHomework Answer (Quiz 1-2 Revision)Kccc siniNo ratings yet

- ACCT101 9n10 SCFDocument17 pagesACCT101 9n10 SCFVedanshi BihaniNo ratings yet

- Ghi BaiDocument42 pagesGhi BaiPhạm Như HậuNo ratings yet

- Adv Acc Prep 2024Document3 pagesAdv Acc Prep 2024Suhail AhmedNo ratings yet

- Statement of CashflowDocument9 pagesStatement of CashflowOwen Lustre50% (2)

- Statement of CFDocument1 pageStatement of CFnr1520122No ratings yet

- AKL 2 Jawban Lat UTSDocument14 pagesAKL 2 Jawban Lat UTSSUGYANTO SUGYANTONo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Process Costing EgDocument8 pagesProcess Costing EgHuu LuatNo ratings yet

- This Study Resource Was: Chapter 04 TestbankDocument4 pagesThis Study Resource Was: Chapter 04 TestbankHuu LuatNo ratings yet

- Test Bank 1Document3 pagesTest Bank 1Huu LuatNo ratings yet

- Test Bank 2Document7 pagesTest Bank 2Huu LuatNo ratings yet

- Budgeting Systems: Langfield-Smith, Thorne, Smith, Hilton Management Accounting, 7eDocument32 pagesBudgeting Systems: Langfield-Smith, Thorne, Smith, Hilton Management Accounting, 7eHuu LuatNo ratings yet

- Standard Costs For Control: Direct Material and Direct LabourDocument33 pagesStandard Costs For Control: Direct Material and Direct LabourHuu LuatNo ratings yet

- Standard Costs For Control: Flexible Budgets and Manufacturing OverheadDocument29 pagesStandard Costs For Control: Flexible Budgets and Manufacturing OverheadHuu LuatNo ratings yet

- General Journal Date Account Titles and Explanation Debit CreditDocument17 pagesGeneral Journal Date Account Titles and Explanation Debit CreditHuu LuatNo ratings yet

- Net Income 38000 Non Cash ItemsDocument8 pagesNet Income 38000 Non Cash ItemsHuu LuatNo ratings yet

- Opening Trial Balance Debit CreditDocument41 pagesOpening Trial Balance Debit CreditHuu LuatNo ratings yet

- Receivables Study Guide Solutions Fill-in-the-Blank EquationsDocument19 pagesReceivables Study Guide Solutions Fill-in-the-Blank EquationsPelin CanikliNo ratings yet

- Nov 2019 Paper 2A Questions EngDocument10 pagesNov 2019 Paper 2A Questions EngTerry MaNo ratings yet

- Ratio Analysis: Categories of RatiosDocument7 pagesRatio Analysis: Categories of RatiosAhmad vlogsNo ratings yet

- Pakistan State Oil:: WebsiteDocument5 pagesPakistan State Oil:: WebsiteAreeba FatimaNo ratings yet

- Accounting 12 Chapter 8Document30 pagesAccounting 12 Chapter 8cecilia capiliNo ratings yet

- Accounting For Decision Making Mid TermDocument5 pagesAccounting For Decision Making Mid Termumer12No ratings yet

- ROE Disaggregation Exercise - P&GDocument3 pagesROE Disaggregation Exercise - P&GPepe GeoNo ratings yet

- Ge Acctg 7Document5 pagesGe Acctg 7ezraelydanNo ratings yet

- Textbook Accounting Carl Warren Ebook All Chapter PDFDocument34 pagesTextbook Accounting Carl Warren Ebook All Chapter PDFbethany.sauders576100% (19)

- FIN201 Term Paper 1Document34 pagesFIN201 Term Paper 1Mahbub Rahman NionNo ratings yet

- CHAPTER 2 PartnershipDocument17 pagesCHAPTER 2 PartnershipLAZARO, Jaspher S.No ratings yet

- Lembar Ukk Ud AbadiDocument62 pagesLembar Ukk Ud Abadibayufitriani3956% (18)

- Project in FinanceDocument177 pagesProject in FinanceJoyce Ann Agdippa BarcelonaNo ratings yet

- 1810 AFAR Home Office Branch and Agency TransactionDocument9 pages1810 AFAR Home Office Branch and Agency TransactionMina Valencia100% (1)

- Intacc2 M2 Ass2Document14 pagesIntacc2 M2 Ass2Rosette SANTOSNo ratings yet

- Test Bank ACC101ng NDocument92 pagesTest Bank ACC101ng NTrọng MinhNo ratings yet

- Final Exam AC 1 2 Answer KeyDocument7 pagesFinal Exam AC 1 2 Answer KeyBill VilladolidNo ratings yet

- FABM Week 6 - Financial RatioDocument35 pagesFABM Week 6 - Financial Ratiovmin친구No ratings yet

- Xii Acc 23.08.23 Study MaterialDocument92 pagesXii Acc 23.08.23 Study MaterialkaranbhattxsNo ratings yet

- 1922 B.com B.com Batchno 247Document66 pages1922 B.com B.com Batchno 247Mukesh SoniNo ratings yet

- Balance Sheet of WiproDocument3 pagesBalance Sheet of Wiproishit9No ratings yet

- Second Term Exam-2070 Particulars Debit (RS.) Credit (RS.)Document8 pagesSecond Term Exam-2070 Particulars Debit (RS.) Credit (RS.)ragedskullNo ratings yet

- MC Questions For FOA IIDocument9 pagesMC Questions For FOA IIGrace SustiguerNo ratings yet

- MRF PNL BalanaceDocument2 pagesMRF PNL BalanaceRupesh DhindeNo ratings yet

- Bookkeeping To Trial Balance 10Document15 pagesBookkeeping To Trial Balance 10elelwaniNo ratings yet

- Quarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterDocument3 pagesQuarter 1st Quarter 2nd Quarter 3rd Quarter 4th QuarterKelvin Jay Sebastian SaplaNo ratings yet

- (A) and (C)Document6 pages(A) and (C)nickNo ratings yet