Download as docx, pdf, or txt

You might also like

- Exam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersDocument4 pagesExam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersJœ œNo ratings yet

- Internship Report On MCB Bank LimitedDocument40 pagesInternship Report On MCB Bank Limitedbbaahmad89No ratings yet

- Achievements: - Business Internship ReportDocument10 pagesAchievements: - Business Internship ReportSamad AbbasNo ratings yet

- MCB Internship ReportDocument44 pagesMCB Internship Reportbbaahmad89100% (1)

- Muslim Commercial Bank Ltd0200Document37 pagesMuslim Commercial Bank Ltd0200Mir FaisalNo ratings yet

- Internship Report RimshaDocument24 pagesInternship Report RimshaRimsha ButtNo ratings yet

- Internship Report RimshaDocument23 pagesInternship Report RimshaRimsha ButtNo ratings yet

- Vision: Vision Statement Mission StatementDocument7 pagesVision: Vision Statement Mission StatementALINo ratings yet

- AFS PJCTDocument47 pagesAFS PJCTAbdul BasitNo ratings yet

- Acknowledgment: Mustafa Mir " For His Continues, Valuable and Informative Support and Kind PieceDocument14 pagesAcknowledgment: Mustafa Mir " For His Continues, Valuable and Informative Support and Kind Pieceayesha_121No ratings yet

- Executive Summary 1Document82 pagesExecutive Summary 1madihaijazkhanNo ratings yet

- Qdoc - Tips Internship Report On MCBDocument50 pagesQdoc - Tips Internship Report On MCBRaza AliNo ratings yet

- Introduction of MCB: IncorporationDocument11 pagesIntroduction of MCB: IncorporationAli Jameel75% (4)

- MCB Bank Limited Formerly Known As Muslim Commercial Bank Limited Was Incorporated by The Adamjee Group On July 9Document6 pagesMCB Bank Limited Formerly Known As Muslim Commercial Bank Limited Was Incorporated by The Adamjee Group On July 9Imdad Ali JokhioNo ratings yet

- MCB Bank LTDDocument23 pagesMCB Bank LTDAlonefor ChrisleoNo ratings yet

- Sonia Intership ReportDocument32 pagesSonia Intership ReportMubashar HsnNo ratings yet

- Products and ServicesDocument4 pagesProducts and ServicesMalik ZafranNo ratings yet

- Internship Report On MCB Bank LTDDocument66 pagesInternship Report On MCB Bank LTDbbaahmad89No ratings yet

- MCB Project ReportDocument18 pagesMCB Project ReportAyaan Muhammad0% (1)

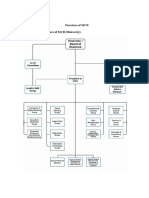

- Organizational Hierarchy of MCBDocument4 pagesOrganizational Hierarchy of MCBSana Javaid100% (3)

- Final MCB ProjectDocument9 pagesFinal MCB ProjectMiShtii BalochNo ratings yet

- MCB IslamicDocument68 pagesMCB IslamicHammad Lali100% (2)

- MCB Presentation For SubmissionDocument79 pagesMCB Presentation For SubmissionAfshan HabibNo ratings yet

- Project On MCB GCUFDocument19 pagesProject On MCB GCUFAmna Goher100% (1)

- Internship ReportDocument21 pagesInternship ReportsoulsisterzNo ratings yet

- Source: MCB Main PortalDocument43 pagesSource: MCB Main PortalFahad IftikharNo ratings yet

- FM ReportDocument7 pagesFM ReportMaryam KamranNo ratings yet

- MCB Report1 Word 2003Document32 pagesMCB Report1 Word 2003luvlieyeNo ratings yet

- Ahmed ReportDocument36 pagesAhmed Reporthassan_shazaibNo ratings yet

- MCB Bank:History: ProfitabilityDocument5 pagesMCB Bank:History: ProfitabilityShaheryar SialNo ratings yet

- Internship Report On MCB Bank LimitedDocument42 pagesInternship Report On MCB Bank Limitedbbaahmad89No ratings yet

- Report - 1862Document23 pagesReport - 1862aqsamumtaz812No ratings yet

- Internship Report MCBDocument22 pagesInternship Report MCBNayab NoumanNo ratings yet

- MCB Bank LTD.: Equation 1Document57 pagesMCB Bank LTD.: Equation 1saragrgNo ratings yet

- RTIAct 2005 Nov 2013Document50 pagesRTIAct 2005 Nov 2013Stalin JoseNo ratings yet

- Full Report RecDocument56 pagesFull Report RecRehan UllahNo ratings yet

- AFS BookletDocument8 pagesAFS Bookletdua.63493No ratings yet

- Shafe Eq AliDocument8 pagesShafe Eq AliZORROALINo ratings yet

- DCB Bank (Development Credit Bank)Document6 pagesDCB Bank (Development Credit Bank)AlexNo ratings yet

- Dena BankDocument25 pagesDena BankJaved ShaikhNo ratings yet

- Banking Law Assigment (Silk Bank)Document6 pagesBanking Law Assigment (Silk Bank)Muzamil AshrafNo ratings yet

- Cia 1 Risk in Financial Services: Risk Management Practices of A Banking CompanyDocument7 pagesCia 1 Risk in Financial Services: Risk Management Practices of A Banking CompanyGoutham ShineNo ratings yet

- Executive SummaryDocument36 pagesExecutive SummaryPooja NirmalNo ratings yet

- MCB Internship ReportDocument30 pagesMCB Internship ReportAdeelBaigNo ratings yet

- Assignment On Historical Background of The City Bank LimitedDocument12 pagesAssignment On Historical Background of The City Bank LimitedAl-Amin SikderNo ratings yet

- Internship Report On MCB Bank Limited: Introduction of Banking Industry What Is Bank?Document55 pagesInternship Report On MCB Bank Limited: Introduction of Banking Industry What Is Bank?Muhammad BurhanNo ratings yet

- Muslim Commercial Bank LimitedDocument3 pagesMuslim Commercial Bank LimitedHaroon Z. ChoudhryNo ratings yet

- Final CHAPTER NO 2Document12 pagesFinal CHAPTER NO 2AliNo ratings yet

- MONIKADocument100 pagesMONIKAFranklin RjamesNo ratings yet

- Project of MCBDocument55 pagesProject of MCBSana JavaidNo ratings yet

- Internship Report On MCB 2009Document85 pagesInternship Report On MCB 2009siaapaNo ratings yet

- BC12010 (M)Document109 pagesBC12010 (M)Life EndNo ratings yet

- Internship Report On MCB BankDocument63 pagesInternship Report On MCB BankMaham ButtNo ratings yet

- NIB Bank's Merger With and Into MCB Bank Comes Into Effect 11 7 2017Document1 pageNIB Bank's Merger With and Into MCB Bank Comes Into Effect 11 7 2017Salman AhmedNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaFrom EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Mastering Trade Lines "A Guide to Building Credit and Financial Success"From EverandMastering Trade Lines "A Guide to Building Credit and Financial Success"No ratings yet

- Financial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeFrom EverandFinancial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeNo ratings yet

- Money and Banking ProjectDocument11 pagesMoney and Banking Projectshahroze ALINo ratings yet

- I Selected The Textile Composite Sector, Which Include Following CompaniesDocument7 pagesI Selected The Textile Composite Sector, Which Include Following Companiesshahroze ALINo ratings yet

- Name: Shahroze Ali Reg # 2183150 Project: FM-2: Date - 1/3/2021Document8 pagesName: Shahroze Ali Reg # 2183150 Project: FM-2: Date - 1/3/2021shahroze ALINo ratings yet

- Name: Shahroze Ali Chohan Reg # 2183150 Question No 1Document4 pagesName: Shahroze Ali Chohan Reg # 2183150 Question No 1shahroze ALINo ratings yet

- Intro Final ProjectDocument13 pagesIntro Final Projectshahroze ALINo ratings yet

- Name: Shahroz Ali Reg# 2183150: Human Resource Management Laws in PakistanDocument3 pagesName: Shahroz Ali Reg# 2183150: Human Resource Management Laws in Pakistanshahroze ALINo ratings yet

- Financial Management II Kiran Naveed: 2183416 Farid Jaleel: 2183364Document4 pagesFinancial Management II Kiran Naveed: 2183416 Farid Jaleel: 2183364shahroze ALINo ratings yet

- ApplyBoard Invoice Template CanadaDocument2 pagesApplyBoard Invoice Template CanadasmangrishNo ratings yet

- 2 Financial AnalysisDocument22 pages2 Financial AnalysisAB11A4-Condor, Joana MieNo ratings yet

- Versprite Envisions 2019: Cybersecurity Through A Geopolitical LensDocument17 pagesVersprite Envisions 2019: Cybersecurity Through A Geopolitical LensTanmay KadamNo ratings yet

- Customer Perception Towards Internet BankingDocument35 pagesCustomer Perception Towards Internet Bankingmajiclover90% (78)

- Management: Notes Prepared by Ar Esra GhalibDocument11 pagesManagement: Notes Prepared by Ar Esra GhalibEsra IrfanNo ratings yet

- Tesfaye FeyisaDocument86 pagesTesfaye FeyisamogesgirmayNo ratings yet

- TV3 AnalysisDocument3 pagesTV3 AnalysishotransangNo ratings yet

- App Builder All SetDocument32 pagesApp Builder All SetArya50% (2)

- Spider Web The Birth of American Anti-Communism (2016)Document369 pagesSpider Web The Birth of American Anti-Communism (2016)Chemical CesiumNo ratings yet

- JIS-B0401-System of Limits and FitsDocument43 pagesJIS-B0401-System of Limits and FitsfatimahNo ratings yet

- Unit 1 Application LetterDocument15 pagesUnit 1 Application Letteryulijuansyah313No ratings yet

- Chapter 1.1 Introduction To Business ManagementDocument48 pagesChapter 1.1 Introduction To Business ManagementRamesh SivaNo ratings yet

- 516-Article Text-8816-2-10-20230331Document17 pages516-Article Text-8816-2-10-20230331vivi irsamNo ratings yet

- A Social Media Crisis Management PlanDocument12 pagesA Social Media Crisis Management PlanEkoda TVNo ratings yet

- Multimodal Transport: Prof. Ashok Advani - Visiting Faculty: IIFT & Jaipuria Institute of Management, NoidaDocument56 pagesMultimodal Transport: Prof. Ashok Advani - Visiting Faculty: IIFT & Jaipuria Institute of Management, NoidaShaivik SharmaNo ratings yet

- The World's Billionaires List - ForbesDocument10 pagesThe World's Billionaires List - ForbesmooninjaNo ratings yet

- Business Strategy 2 - Bus-5571-0Lb - Group #1: Name Student NumberDocument31 pagesBusiness Strategy 2 - Bus-5571-0Lb - Group #1: Name Student NumberArchana NairNo ratings yet

- Digital Marketing by ChatgpxDocument2 pagesDigital Marketing by ChatgpxEdri FauzanNo ratings yet

- AFAR Preboards MergedDocument112 pagesAFAR Preboards Mergedpajarillagavincent15No ratings yet

- International Labour OrganizationDocument14 pagesInternational Labour OrganizationTroeeta Bhuniya100% (1)

- Rahul e BussDocument49 pagesRahul e BussAbhi TiwariNo ratings yet

- Weighing of Stocks and PaymentDocument8 pagesWeighing of Stocks and PaymentPauline Caceres AbayaNo ratings yet

- Cdip 29 Inf 1Document27 pagesCdip 29 Inf 1LOVETH KONNIANo ratings yet

- Pdfanddoc 33163Document74 pagesPdfanddoc 33163Unison Homoeo LaboratoriesNo ratings yet

- M.A. I - Economics Old Exam Question Paper (W.e.f. 2021-22) December 2022Document30 pagesM.A. I - Economics Old Exam Question Paper (W.e.f. 2021-22) December 2022Jelly DukhandeNo ratings yet

- Airport Literature ReviewDocument5 pagesAirport Literature Reviewafmzydxcnojakg100% (1)

- Concha V RubioDocument18 pagesConcha V RubiokamiruhyunNo ratings yet

- Payment of Gratuity ActDocument26 pagesPayment of Gratuity ActAnnie Paul100% (1)

- Supply Chain Management (Haya Ali Kazmi 12487)Document6 pagesSupply Chain Management (Haya Ali Kazmi 12487)HAYA ALI KAZMINo ratings yet