Download as pdf or txt

You might also like

- Workday Integration Ebook PDFDocument20 pagesWorkday Integration Ebook PDFdavidprasad100% (4)

- SummeryAssignmentEPMDocument64 pagesSummeryAssignmentEPMreadqwertyNo ratings yet

- New Century Clinic Chapter1Document4 pagesNew Century Clinic Chapter1chandini100% (2)

- Eric Roberts CaseDocument12 pagesEric Roberts CaseSteveNo ratings yet

- $203 Billion and Counting: Total Debt For State and Local Retirement Benefits in IllinoisDocument35 pages$203 Billion and Counting: Total Debt For State and Local Retirement Benefits in IllinoisIllinois PolicyNo ratings yet

- 2020 CRF Data BulletinDocument26 pages2020 CRF Data BulletinWKYTNo ratings yet

- handbook-AutoPlus - January 2020.cleanDocument79 pageshandbook-AutoPlus - January 2020.cleanJeff BakerNo ratings yet

- PAGES 239-242 Exercise 1: Required: For Each Misstatement, List An Internal Control That Should Prevent ItDocument12 pagesPAGES 239-242 Exercise 1: Required: For Each Misstatement, List An Internal Control That Should Prevent ItRia PaulaNo ratings yet

- Benefits Administration - 1Document34 pagesBenefits Administration - 1vivek_sharma13No ratings yet

- Insights Home Based Vs Host PayDocument4 pagesInsights Home Based Vs Host PayPratap Reddy100% (1)

- See Chapter 20 of 48 U.S. CodeDocument4 pagesSee Chapter 20 of 48 U.S. CodeMetro Puerto RicoNo ratings yet

- Cares Act Funds 058ec425199fbDocument3 pagesCares Act Funds 058ec425199fbVickie LarsenNo ratings yet

- American Rescue Plan One-Pager 1Document1 pageAmerican Rescue Plan One-Pager 1api-551507435No ratings yet

- McKee ARPA Down PaymentDocument12 pagesMcKee ARPA Down PaymentNBC 10 WJARNo ratings yet

- Office of The City AdministratorDocument6 pagesOffice of The City AdministratorSusie CambriaNo ratings yet

- Jag FaqsDocument33 pagesJag FaqsOrdnaz Iluye OdidrasNo ratings yet

- Ortgaging: UR UtureDocument5 pagesOrtgaging: UR UturereasonorgNo ratings yet

- 05 - 14 - 2020 CRF Mills Delegation LetterDocument4 pages05 - 14 - 2020 CRF Mills Delegation LetterNEWS CENTER MaineNo ratings yet

- April Fools MN House Week in ReviewDocument6 pagesApril Fools MN House Week in ReviewquantataNo ratings yet

- House Hearing, 112TH Congress - Social Security's Payment AccuracyDocument110 pagesHouse Hearing, 112TH Congress - Social Security's Payment AccuracyScribd Government DocsNo ratings yet

- Keller Spring 2010 NewsletterDocument4 pagesKeller Spring 2010 NewsletterPAHouseGOPNo ratings yet

- Lania Boone InfoDocument8 pagesLania Boone InfoTyler EstepNo ratings yet

- 2010 Albany BudgetDocument187 pages2010 Albany BudgettulocalpoliticsNo ratings yet

- Budget UpdateDocument1 pageBudget UpdateSteve CouncilNo ratings yet

- Livingston County Adopted Budget (2023)Document401 pagesLivingston County Adopted Budget (2023)Watertown Daily TimesNo ratings yet

- Report of Investigation RichwoodDocument189 pagesReport of Investigation RichwoodAnna MooreNo ratings yet

- States Fall Short On Help For HousingDocument14 pagesStates Fall Short On Help For HousingForeclosure FraudNo ratings yet

- Livingston County 2024 Proposed BudgetDocument395 pagesLivingston County 2024 Proposed BudgetThe Livingston County NewsNo ratings yet

- MainePigletBook 2007Document19 pagesMainePigletBook 2007Maine Policy InstituteNo ratings yet

- Binder - LL - SecDocument23 pagesBinder - LL - SecMy-Acts Of-SeditionNo ratings yet

- HHRG 117 Ba00 Wstate Yellenj 20210323Document12 pagesHHRG 117 Ba00 Wstate Yellenj 20210323Joseph Adinolfi Jr.No ratings yet

- Corrections Marginal CostDocument19 pagesCorrections Marginal CostWDIV/ClickOnDetroitNo ratings yet

- An Open Letter To Kentucky LegislatorsDocument3 pagesAn Open Letter To Kentucky LegislatorsWKMS NewsNo ratings yet

- T Rident: Municipal ResearchDocument4 pagesT Rident: Municipal Researchapi-245850635No ratings yet

- DMR Transportation Press ReleaseDocument2 pagesDMR Transportation Press ReleaseBrandon Michael ChewNo ratings yet

- Veto Letter Dayton To DaudtDocument5 pagesVeto Letter Dayton To DaudtGoMNNo ratings yet

- The $21 Billion State Budget: South Carolina's Three Spending CategoriesDocument25 pagesThe $21 Billion State Budget: South Carolina's Three Spending CategoriesSteve CouncilNo ratings yet

- LAO Re Brown Initiative 1-11-12Document7 pagesLAO Re Brown Initiative 1-11-12smf 4LAKidsNo ratings yet

- Baltimore Case StudyDocument5 pagesBaltimore Case StudyShane MastroNo ratings yet

- Riverside County FY 2020-21 First Quarter Budget ReportDocument50 pagesRiverside County FY 2020-21 First Quarter Budget ReportThe Press-Enterprise / pressenterprise.comNo ratings yet

- Wastebook 2011Document98 pagesWastebook 2011FedSmith Inc.No ratings yet

- Digging OutDocument12 pagesDigging OutCrains Chicago BusinessNo ratings yet

- State Budget RequestDocument12 pagesState Budget RequestDevon Louise KesslerNo ratings yet

- Build America Bond Subsidies May Be CutDocument3 pagesBuild America Bond Subsidies May Be CutCOASTNo ratings yet

- House Hearing, 110TH Congress - Budgeting To Fight Waste, Fraud and AbuseDocument76 pagesHouse Hearing, 110TH Congress - Budgeting To Fight Waste, Fraud and AbuseScribd Government DocsNo ratings yet

- Legal Covid CARES Act Complaint To Idaho Governor Brad LittleDocument39 pagesLegal Covid CARES Act Complaint To Idaho Governor Brad LittleR.No ratings yet

- Stimulus Contractors Who Cheat On Their Taxes: What Happened?Document98 pagesStimulus Contractors Who Cheat On Their Taxes: What Happened?Scribd Government DocsNo ratings yet

- Running Out of Other People's Money: It's The Entitlements, StupidDocument4 pagesRunning Out of Other People's Money: It's The Entitlements, StupidLatinos Ready To VoteNo ratings yet

- War Supplemental Summary House Ammt.6.30.10Document5 pagesWar Supplemental Summary House Ammt.6.30.10StimulatingBroadband.comNo ratings yet

- Holtzeakin Testimony 4oct2011Document12 pagesHoltzeakin Testimony 4oct2011Committee For a Responsible Federal BudgetNo ratings yet

- American Rescue Plan Frequently Asked QuestionsDocument42 pagesAmerican Rescue Plan Frequently Asked QuestionsAnonymous GF8PPILW5No ratings yet

- Hud-Oig 2012-FW-1013Document38 pagesHud-Oig 2012-FW-1013Texas WatchdogNo ratings yet

- 2020-09-01.PPP Interim ReportDocument10 pages2020-09-01.PPP Interim ReportMeilin TompkinsNo ratings yet

- U.S. Department of Housing and Urban DevelopmentDocument16 pagesU.S. Department of Housing and Urban DevelopmentSarah LehrNo ratings yet

- El2010 20Document4 pagesEl2010 20arborjimbNo ratings yet

- Budget Letter To Gov CooperDocument1 pageBudget Letter To Gov CooperLauren HorschNo ratings yet

- Federal Funding BriefDocument6 pagesFederal Funding BriefNick ReismanNo ratings yet

- Governor Withholding ReportDocument4 pagesGovernor Withholding ReportColumbia Daily TribuneNo ratings yet

- Usa Debt Crisis Republicans ViewDocument6 pagesUsa Debt Crisis Republicans ViewAmit Kumar RoyNo ratings yet

- Keller Audit 4.5 PDFDocument25 pagesKeller Audit 4.5 PDFJason LopezNo ratings yet

- Federal Budget Sequestration 101: Perspectives Through The County LensDocument31 pagesFederal Budget Sequestration 101: Perspectives Through The County LenslaedcpdfsNo ratings yet

- State of Minnesota: Office of Governor Mark DaytonDocument2 pagesState of Minnesota: Office of Governor Mark DaytonRachel E. Stassen-BergerNo ratings yet

- House Hearing, 112TH Congress - Transparency and Funding of State and Local Pension PlansDocument128 pagesHouse Hearing, 112TH Congress - Transparency and Funding of State and Local Pension PlansScribd Government DocsNo ratings yet

- Press Release: Alameda County Supervisor Keith Carson, Fifth DistrictDocument2 pagesPress Release: Alameda County Supervisor Keith Carson, Fifth DistrictlocalonNo ratings yet

- Hidden Spending: The Politics of Federal Credit ProgramsFrom EverandHidden Spending: The Politics of Federal Credit ProgramsNo ratings yet

- Chancellor's Council Executive Committee Letter To RegentsDocument3 pagesChancellor's Council Executive Committee Letter To RegentsSteveNo ratings yet

- Final Suggested Dallas City Charter Amendments ListDocument19 pagesFinal Suggested Dallas City Charter Amendments ListSteveNo ratings yet

- BLM Research DictatesDocument1 pageBLM Research DictatesSteveNo ratings yet

- Nelson Tweet On Self DefenseDocument1 pageNelson Tweet On Self DefenseSteveNo ratings yet

- CTCL Conflict PolicyDocument1 pageCTCL Conflict PolicySteveNo ratings yet

- RSC 2023 Budget Final VersionDocument122 pagesRSC 2023 Budget Final VersionSteveNo ratings yet

- AB-935 CalifDocument4 pagesAB-935 CalifSteveNo ratings yet

- Greater East Texas Community Action ProgramDocument11 pagesGreater East Texas Community Action ProgramSteveNo ratings yet

- Southeast Alabama Community Action CaseDocument2 pagesSoutheast Alabama Community Action CaseSteveNo ratings yet

- Alabama LawsuitDocument8 pagesAlabama LawsuitSteveNo ratings yet

- Nelson Deposition 2018, Iowa UniversityDocument93 pagesNelson Deposition 2018, Iowa UniversitySteveNo ratings yet

- Google Review, AuxinDocument1 pageGoogle Review, AuxinSteveNo ratings yet

- Nsta LetterDocument2 pagesNsta LetterSteveNo ratings yet

- Lithium US ExportsDocument1 pageLithium US ExportsSteveNo ratings yet

- DOT EmailDocument1 pageDOT EmailSteveNo ratings yet

- K12 ClimateActionPlanDocument80 pagesK12 ClimateActionPlanSteveNo ratings yet

- Eyond A Ond: - by Nicolás Antonio Jiménez / Photos by Gesi SchillingDocument4 pagesEyond A Ond: - by Nicolás Antonio Jiménez / Photos by Gesi SchillingSteveNo ratings yet

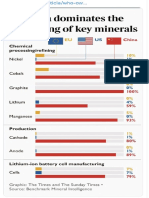

- China DominatesDocument1 pageChina DominatesSteveNo ratings yet

- BLM Oil and Gas Leases Complaint 29 June 2022Document63 pagesBLM Oil and Gas Leases Complaint 29 June 2022SteveNo ratings yet

- Directions For Green Bay Elections WorkersDocument1 pageDirections For Green Bay Elections WorkersSteveNo ratings yet

- Engaging Voters On Facebook WebinarDocument31 pagesEngaging Voters On Facebook WebinarSteveNo ratings yet

- Fort Worth ISDDocument224 pagesFort Worth ISDSteveNo ratings yet

- Voter NavigatorsDocument2 pagesVoter NavigatorsSteveNo ratings yet

- Curing BallotsDocument2 pagesCuring BallotsSteveNo ratings yet

- Freedom of Information Act (Foia) Response: S M Department of Technology, Management & BudgetDocument4 pagesFreedom of Information Act (Foia) Response: S M Department of Technology, Management & BudgetSteveNo ratings yet

- New Mexico Liberty, January 2006Document10 pagesNew Mexico Liberty, January 2006Mike BlessingNo ratings yet

- Assignment#1: Natchapha 6143241826 Phornprakaikaew 6143284826Document7 pagesAssignment#1: Natchapha 6143241826 Phornprakaikaew 6143284826Minnie NatchaphaNo ratings yet

- APM Employment HandbookDocument40 pagesAPM Employment HandbookShakeel MirzaNo ratings yet

- Sample HCM Resume 1Document5 pagesSample HCM Resume 1Courtney FordNo ratings yet

- D2 Accounting For LabourDocument13 pagesD2 Accounting For LabourNkatlehiseng MabuselaNo ratings yet

- Cost Accounting: Labor: Controlling and Accounting For CostsDocument37 pagesCost Accounting: Labor: Controlling and Accounting For CostsNuraini Meina RatriNo ratings yet

- Planning: Stoney-Wilson Business ConsultingDocument5 pagesPlanning: Stoney-Wilson Business Consultingarnel tanggaroNo ratings yet

- Payslipreport cm24804 Id PDFDocument1 pagePayslipreport cm24804 Id PDFSyarifah SyarifahNo ratings yet

- HR and Payroll ManagementDocument8 pagesHR and Payroll ManagementAmit Anand100% (1)

- Financial Reporting Using OBIEEDocument44 pagesFinancial Reporting Using OBIEEAmit Sharma67% (3)

- Prescribed Barangay FormsDocument53 pagesPrescribed Barangay FormsSeth Cabrera100% (1)

- Payroll/Personnel System Overview (PPSO) : ProceduresDocument41 pagesPayroll/Personnel System Overview (PPSO) : ProceduresCymond CubaNo ratings yet

- Internal Control of Pancharatna ParadiseDocument10 pagesInternal Control of Pancharatna Paradiseprabhu_bala100% (1)

- Sap Us TaxationDocument274 pagesSap Us TaxationKRISHNA RAONo ratings yet

- Set PoliciesDocument5 pagesSet Policiesbloop carrotNo ratings yet

- Chapter 14 SolutionsDocument35 pagesChapter 14 SolutionsAnik Kumar MallickNo ratings yet

- Implementing OTM (US)Document36 pagesImplementing OTM (US)allextrastodoNo ratings yet

- Jadwal Shifting JULI - AGUSTUS 2020Document10 pagesJadwal Shifting JULI - AGUSTUS 2020Ahmad Tio Handini IINo ratings yet

- Tiendaan Delivery Partner AgreementDocument3 pagesTiendaan Delivery Partner Agreementmarvene paladoNo ratings yet

- SAPayslipDocument1 pageSAPayslipmomen rababahNo ratings yet

- 318c - TaxationDocument24 pages318c - TaxationdashanNo ratings yet

- Building A Market Based Pay StructureDocument20 pagesBuilding A Market Based Pay StructureMaha SiddiquiNo ratings yet

- REGULAR EMPLOYMENT CONTRACT - Liggayu (SIGNED)Document2 pagesREGULAR EMPLOYMENT CONTRACT - Liggayu (SIGNED)D LNo ratings yet