Download as docx, pdf, or txt

You might also like

- Accntncy MCQs For SAS CAGDocument12 pagesAccntncy MCQs For SAS CAGDeepak Kumar PandaNo ratings yet

- CA Inter Income Tax AY 2020-21 Material by RSN SirDocument404 pagesCA Inter Income Tax AY 2020-21 Material by RSN SirAbNo ratings yet

- 80 Auditing Assurance MCQ'S: © Ca WorldDocument14 pages80 Auditing Assurance MCQ'S: © Ca WorldZain Butt50% (2)

- Account MCQ PDFDocument93 pagesAccount MCQ PDFsunil kalura100% (1)

- Information Technology LawDocument232 pagesInformation Technology LawMeenal LutherNo ratings yet

- ITAD Ruling No 018-09Document11 pagesITAD Ruling No 018-09Peggy SalazarNo ratings yet

- Taxatio MCQDocument10 pagesTaxatio MCQAtif KhanNo ratings yet

- MCQ Module 1Document4 pagesMCQ Module 1mohanraokp2279No ratings yet

- MCQ'S - 1 To 50Document12 pagesMCQ'S - 1 To 50varunendra pandeyNo ratings yet

- Chapter 1 Mcqs On Income Tax Rates and Basic Concept of Income TaxDocument27 pagesChapter 1 Mcqs On Income Tax Rates and Basic Concept of Income TaxSatheesh KannaNo ratings yet

- MCQ - Unit 2Document15 pagesMCQ - Unit 2Niraj PandeyNo ratings yet

- It MCQDocument31 pagesIt MCQbigbulleye6078No ratings yet

- Income Tax MCQ With Answers PDFDocument19 pagesIncome Tax MCQ With Answers PDFAman Pandit100% (1)

- MCQ On Direct TaxDocument3 pagesMCQ On Direct TaxVarsha SinhaNo ratings yet

- BusinessenvioronmentDocument28 pagesBusinessenvioronmentshamsnpalamNo ratings yet

- Goods and Services Tax (Question Bank For Internal)Document14 pagesGoods and Services Tax (Question Bank For Internal)rupalNo ratings yet

- Mcqs On Basic Concept of Income Tax, Residential Status & Exempt IncomeDocument6 pagesMcqs On Basic Concept of Income Tax, Residential Status & Exempt IncomePradeep SethyNo ratings yet

- Account's MCQDocument7 pagesAccount's MCQMohitTagotraNo ratings yet

- NPO MCQ QuestionDocument5 pagesNPO MCQ QuestionBikash SahooNo ratings yet

- MCQ-Financial Account-SEM VDocument52 pagesMCQ-Financial Account-SEM VVishnuNadarNo ratings yet

- Income Tax MCQ 1Document9 pagesIncome Tax MCQ 1mohammedumair100% (3)

- MCQ 2 EpmDocument3 pagesMCQ 2 EpmCharu Lata0% (1)

- MCQ On Rti ActDocument4 pagesMCQ On Rti ActmuthuNo ratings yet

- GST MCQ S Ca Shiva Teja PDFDocument172 pagesGST MCQ S Ca Shiva Teja PDFGiri SukumarNo ratings yet

- Xii Mcqs CH - 11 Redemption of DebenturesDocument4 pagesXii Mcqs CH - 11 Redemption of DebenturesJoanna GarciaNo ratings yet

- Public Economics MCQs LongDocument18 pagesPublic Economics MCQs Longrkhadke1100% (1)

- Goods-And-Services-Tax-Gst Solved MCQs (Set-4)Document8 pagesGoods-And-Services-Tax-Gst Solved MCQs (Set-4)Ayushi BhardwajNo ratings yet

- Corporate Accounting Solved Mcqs Set 15Document6 pagesCorporate Accounting Solved Mcqs Set 15Bhupendra Gocher0% (1)

- Audit Mcqs 150 MergedDocument188 pagesAudit Mcqs 150 MergedKadam KartikeshNo ratings yet

- GST MCQ Are in Question Bank - Chapter WISE .. Custom MCQ'SDocument26 pagesGST MCQ Are in Question Bank - Chapter WISE .. Custom MCQ'SAman jainNo ratings yet

- Unit 1: Indian Financial System: Multiple Choice QuestionsDocument31 pagesUnit 1: Indian Financial System: Multiple Choice QuestionsNisha PariharNo ratings yet

- Ncert Books PDF: General Financial Rules 2017: WORKSDocument3 pagesNcert Books PDF: General Financial Rules 2017: WORKSRISHABH TOMARNo ratings yet

- Goods and Services Tax: Multiple Choice QuestionsDocument20 pagesGoods and Services Tax: Multiple Choice QuestionsDhruti AthaNo ratings yet

- Goods-And-Services-Tax-Gst Solved MCQs (Set-1)Document8 pagesGoods-And-Services-Tax-Gst Solved MCQs (Set-1)Ayushi BhardwajNo ratings yet

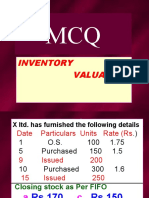

- MCQ Inventory Valuation LBSIMDocument49 pagesMCQ Inventory Valuation LBSIMSumit SharmaNo ratings yet

- MCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23Document10 pagesMCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23NikiNo ratings yet

- Income Tax MCQ Compilation PDFDocument76 pagesIncome Tax MCQ Compilation PDFjesurajajoseph100% (1)

- Taxation MCQsDocument114 pagesTaxation MCQsKishan makvanaNo ratings yet

- Fiscal Policy (Multiple Choice Questions)Document16 pagesFiscal Policy (Multiple Choice Questions)NickNo ratings yet

- Non-Profit Organisations Accounts MCQS: A) B) C) D)Document5 pagesNon-Profit Organisations Accounts MCQS: A) B) C) D)Anonymous EZxKXzNo ratings yet

- T.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Document13 pagesT.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Kadam KartikeshNo ratings yet

- Cost Accounting Objective (MCQ)Document243 pagesCost Accounting Objective (MCQ)mirjapur0% (1)

- MCQ - Law 1 PDFDocument160 pagesMCQ - Law 1 PDFBharathNo ratings yet

- Pension Procedure MCQ S Set-1Document6 pagesPension Procedure MCQ S Set-1Atiq33% (3)

- Cost Sem 5 ObjectiveDocument16 pagesCost Sem 5 Objectivesimran Keswani0% (1)

- MCQ - BasicDocument22 pagesMCQ - BasicLalitNo ratings yet

- Xii Mcqs CH - 10 Issue of DebenturesDocument4 pagesXii Mcqs CH - 10 Issue of DebenturesJoanna GarciaNo ratings yet

- MCQsDocument16 pagesMCQsShreyansh Chopra100% (1)

- SET-1 Public Procurement Rule - 2004 MCQ'sDocument3 pagesSET-1 Public Procurement Rule - 2004 MCQ'sFalak HanifNo ratings yet

- Cma Inter MCQ Booklet Financial Accounting Paper 5Document175 pagesCma Inter MCQ Booklet Financial Accounting Paper 5DGGI BPL Group1No ratings yet

- Mcs QDocument52 pagesMcs QNabeel GondalNo ratings yet

- CRV Goodwill MCQDocument9 pagesCRV Goodwill MCQMital ParmarNo ratings yet

- Sem5 MCQ MangACCDocument8 pagesSem5 MCQ MangACCShirowa ManishNo ratings yet

- Public Finance MCQDocument23 pagesPublic Finance MCQHarshit Tripathi100% (1)

- MCQ's On EconomicsDocument43 pagesMCQ's On Economicsआई सी एस इंस्टीट्यूटNo ratings yet

- Top Senior Auditor Solved MCQs Past PapersDocument12 pagesTop Senior Auditor Solved MCQs Past PapersAli100% (1)

- Dnyansagar Arts and Commerce College, Balewadi, Pune45Document24 pagesDnyansagar Arts and Commerce College, Balewadi, Pune45PrasadNo ratings yet

- Chapter 3 MCQs On DepreciationDocument14 pagesChapter 3 MCQs On DepreciationGrace StylesNo ratings yet

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxDocument25 pagesChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxSonu KumarNo ratings yet

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxDocument25 pagesChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxSonu KumarNo ratings yet

- Direct Tax: Multiple Choice QuestionsDocument27 pagesDirect Tax: Multiple Choice QuestionsAyushman PatnaikNo ratings yet

- Name R.Kishorekumar R.NO RA1931201040210Document19 pagesName R.Kishorekumar R.NO RA1931201040210Kishore KumarNo ratings yet

- Direct Tax MCQDocument320 pagesDirect Tax MCQRam Iyer100% (1)

- Assault On Science and History: - Amar FarooquiDocument22 pagesAssault On Science and History: - Amar FarooquiMeenal LutherNo ratings yet

- Startling Similarity Between Hindu Flood Legend of Manu and The Biblical Account of Noah - Ancient OriginsDocument6 pagesStartling Similarity Between Hindu Flood Legend of Manu and The Biblical Account of Noah - Ancient OriginsMeenal LutherNo ratings yet

- The Man in The Red Underpants: A. R. GreenDocument48 pagesThe Man in The Red Underpants: A. R. GreenMeenal LutherNo ratings yet

- RTI - ManualDocument22 pagesRTI - ManualMeenal LutherNo ratings yet

- Prophet Muhammad Pbuh in Bhavishya Purana. - Know The Truth. - PDFDocument6 pagesProphet Muhammad Pbuh in Bhavishya Purana. - Know The Truth. - PDFMeenal LutherNo ratings yet

- Shepherd CrisisDocument11 pagesShepherd CrisisMeenal LutherNo ratings yet

- Liontree HR Consultants: Strategic Recruitment ConsulantsDocument10 pagesLiontree HR Consultants: Strategic Recruitment ConsulantsMeenal LutherNo ratings yet

- Market Research India - Branded Furniture Market in India 2009Document30 pagesMarket Research India - Branded Furniture Market in India 2009Meenal LutherNo ratings yet

- Accounting TaxationDocument2 pagesAccounting TaxationAia Sophia SindacNo ratings yet

- Oman Investment GuideDocument19 pagesOman Investment GuideTreeSix SolutionsNo ratings yet

- Bir Ruling (Da 576 06)Document26 pagesBir Ruling (Da 576 06)Rieland CuevasNo ratings yet

- 1702 June 2011Document18 pages1702 June 2011fatmaaleahNo ratings yet

- 29 CIR v. CADocument2 pages29 CIR v. CARem SerranoNo ratings yet

- Payslip For The Month of June 2022: Kotak Mahindra Bank LTDDocument1 pagePayslip For The Month of June 2022: Kotak Mahindra Bank LTDshubham choure100% (1)

- Chapter 5Document7 pagesChapter 5yebegashetNo ratings yet

- Brochure Filing A Tax Return in The NetherlandsDocument8 pagesBrochure Filing A Tax Return in The Netherlandssonazinus6847No ratings yet

- Department of Labor: mw4f 76761 7Document1 pageDepartment of Labor: mw4f 76761 7USA_DepartmentOfLaborNo ratings yet

- 16-Limpan Investment Corp. v. CIR G.R. No. L-21570 July 26, 1966Document4 pages16-Limpan Investment Corp. v. CIR G.R. No. L-21570 July 26, 1966Jopan SJNo ratings yet

- Quiz 2 - Income Tax Concepts and ComplianceDocument3 pagesQuiz 2 - Income Tax Concepts and ComplianceDela cruz, Hainrich (Hain)No ratings yet

- 2017 Bar Exams Questions in Mercantile LawDocument29 pages2017 Bar Exams Questions in Mercantile LawGeeAgayamPastorNo ratings yet

- Taxation - Business and ProfessionDocument45 pagesTaxation - Business and ProfessionSanah Bijlani67% (3)

- Tax Law Class NotesDocument126 pagesTax Law Class NotesANAND GEO 1850508No ratings yet

- 1617 3 CoursesDocument318 pages1617 3 Coursesbena omerNo ratings yet

- Question Analysis ICAB Application Level TAXATION-II (Syllabus Weight Based)Document68 pagesQuestion Analysis ICAB Application Level TAXATION-II (Syllabus Weight Based)Optimal Management SolutionNo ratings yet

- CIR v. Marubeni Corp., GR No. 137377, 18 December 2001Document14 pagesCIR v. Marubeni Corp., GR No. 137377, 18 December 2001Ygh E SargeNo ratings yet

- ING Bank N.V. vs. CIR, 763 SCRA 359 (2015)Document2 pagesING Bank N.V. vs. CIR, 763 SCRA 359 (2015)Anonymous MikI28PkJc100% (2)

- Income Taxation DrillsDocument10 pagesIncome Taxation DrillsResty VillaroelNo ratings yet

- 1702 QDocument3 pages1702 Qappipinnim50% (2)

- ZICA Accountancy Programme Students Handbook PDFDocument72 pagesZICA Accountancy Programme Students Handbook PDFAgnes Henderson Mwendela100% (1)

- Chapter 14Document40 pagesChapter 14Ivo_NichtNo ratings yet

- AMERICAN College of Tecnolg Course Business Research Method Factors That Influence Business Income Taxpayers Compliance in EthiopiaDocument29 pagesAMERICAN College of Tecnolg Course Business Research Method Factors That Influence Business Income Taxpayers Compliance in EthiopiaBewuket MazieNo ratings yet

- Standard DeductionDocument58 pagesStandard DeductionJoseph Gabriel EstrellaNo ratings yet

- TAXATIONDocument33 pagesTAXATIONSsentongo NazilNo ratings yet

- Annual Income Tax Return: II014 Income From Profession-Graduated IT Rates II013 Mixed Income-Graduated IT RatesDocument1 pageAnnual Income Tax Return: II014 Income From Profession-Graduated IT Rates II013 Mixed Income-Graduated IT Ratesmary grace villasenorNo ratings yet

- Prelim Take Home ExamDocument11 pagesPrelim Take Home ExamPATATASNo ratings yet

- ACCOUNTING 2 - ProblemsDocument6 pagesACCOUNTING 2 - ProblemsJasmin NoblezaNo ratings yet