Download as pdf or txt

You might also like

- GST India Pre-Requisites and Solution (3700)Document97 pagesGST India Pre-Requisites and Solution (3700)Kottu Arvind93% (14)

- Fred and Frieda Have Always Wanted To Enter The BlueberryDocument1 pageFred and Frieda Have Always Wanted To Enter The BlueberryAmit PandeyNo ratings yet

- 3 - Chamber of Real Estate & Builder's Association vs. Romulo, G.R. No. 160756, March 9, 2010Document41 pages3 - Chamber of Real Estate & Builder's Association vs. Romulo, G.R. No. 160756, March 9, 2010JedrickJordine MaribojoNo ratings yet

- Human Identification Through The Analysis of Smile PhotographsDocument4 pagesHuman Identification Through The Analysis of Smile PhotographsTiến TrịnhNo ratings yet

- Partnership PRE-MID PersonalDocument12 pagesPartnership PRE-MID PersonalAbigail LicayanNo ratings yet

- Gancayco V Collector (Items Not Deductible)Document5 pagesGancayco V Collector (Items Not Deductible)nichols greenNo ratings yet

- Petitioners Respondents Delos Santos Delos Santos & Delos Santos Virgilio C. Manguera & AssociatesDocument15 pagesPetitioners Respondents Delos Santos Delos Santos & Delos Santos Virgilio C. Manguera & AssociatesGina RothNo ratings yet

- Evidence 3.0Document14 pagesEvidence 3.0Rae ManarNo ratings yet

- Manjoorsa, Krith Mounir, C. Block B ANCHETA v. GUERSEY-DALAYGON GR NO. 139868 (Rule 77)Document1 pageManjoorsa, Krith Mounir, C. Block B ANCHETA v. GUERSEY-DALAYGON GR NO. 139868 (Rule 77)KeithMounirNo ratings yet

- Association of International Shipping Lines VS Sec of Finance GR 222239 15jan2020Document24 pagesAssociation of International Shipping Lines VS Sec of Finance GR 222239 15jan2020CJNo ratings yet

- Court Procedure Omar AminDocument42 pagesCourt Procedure Omar AminJohair MD UmpaNo ratings yet

- 11 Maceda vs. Macaraig, JRDocument35 pages11 Maceda vs. Macaraig, JRshlm bNo ratings yet

- 110 CIR vs. PNB (GR No. 161997, October 25, 2005)Document22 pages110 CIR vs. PNB (GR No. 161997, October 25, 2005)Alfred GarciaNo ratings yet

- AGUSAN WOOD INDUSTRIES v. SECRETARY OF DEPARTMENT OF ENVIRONMENTDocument11 pagesAGUSAN WOOD INDUSTRIES v. SECRETARY OF DEPARTMENT OF ENVIRONMENTsejinmaNo ratings yet

- Journal Entry Voucher: No. Lgu-Labo DateDocument100 pagesJournal Entry Voucher: No. Lgu-Labo DateRenieboy JanabanNo ratings yet

- The Corporation Code of The PhilippinesDocument98 pagesThe Corporation Code of The PhilippinesJ Velasco PeraltaNo ratings yet

- CRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesDocument110 pagesCRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesKyle Ethan AringoNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument9 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledAnonymous lvUVwZMNo ratings yet

- Dick Go Vs CA and SBTCDocument2 pagesDick Go Vs CA and SBTCKaren Patricio LusticaNo ratings yet

- Local Taxation General PrinciplesDocument14 pagesLocal Taxation General PrinciplesRufino Gerard MorenoNo ratings yet

- Visayas Geothermal V CIRDocument2 pagesVisayas Geothermal V CIRGwynneth Grace LasayNo ratings yet

- CIR Vs Isabela Cultural CorporationDocument2 pagesCIR Vs Isabela Cultural CorporationLauren KeiNo ratings yet

- Bertillo - Phil. Guaranty Co. Inc. Vs CIR and CTADocument2 pagesBertillo - Phil. Guaranty Co. Inc. Vs CIR and CTAStella BertilloNo ratings yet

- 82 Supreme Court Reports Annotated: Philippine Petroleum Corp. vs. Municipality of Pililla, RizalDocument10 pages82 Supreme Court Reports Annotated: Philippine Petroleum Corp. vs. Municipality of Pililla, RizalAaron ReyesNo ratings yet

- IIRC ReportDocument59 pagesIIRC ReportOfficial Gazette PHNo ratings yet

- Mejoff vs. Director of PrisonsDocument6 pagesMejoff vs. Director of PrisonsPepper TzuNo ratings yet

- Ulep VsDocument14 pagesUlep VsRochen ShairaNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument6 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledJoyce LapuzNo ratings yet

- Coral Bay Vs CIR Cross Border DoctrineDocument7 pagesCoral Bay Vs CIR Cross Border DoctrineAira Mae P. LayloNo ratings yet

- Vera vs. Fernandez, G.R. No. L-31364, March 30, 1979 (FULL CASE)Document4 pagesVera vs. Fernandez, G.R. No. L-31364, March 30, 1979 (FULL CASE)Sharliemagne B. Bayan100% (1)

- Transport of Goods DigestsDocument67 pagesTransport of Goods DigestsAiden Cyrus TinocoNo ratings yet

- CIR v. Univation Motor Philippines, Inc. G.R. No. 231581, April 10, 2019 FactsDocument4 pagesCIR v. Univation Motor Philippines, Inc. G.R. No. 231581, April 10, 2019 FactsIsabel Claire OcaNo ratings yet

- Systems Plus Computer College Vs Caloocan CityDocument4 pagesSystems Plus Computer College Vs Caloocan CityRachelle DomingoNo ratings yet

- De Castro DoctrinesDocument111 pagesDe Castro DoctrinesarkstersNo ratings yet

- Barba Vs Liceo de CagaynDocument3 pagesBarba Vs Liceo de CagaynPaula GasparNo ratings yet

- Torts and Damages Midterm ReviewerDocument25 pagesTorts and Damages Midterm ReviewerErika-Anne ThereseNo ratings yet

- Deconstructed Codal EvidDocument20 pagesDeconstructed Codal EvidStephanie SerapioNo ratings yet

- CIR vs. PALDocument1 pageCIR vs. PALNeil de CastroNo ratings yet

- CIR v. Tulio (Digest by Madz)Document3 pagesCIR v. Tulio (Digest by Madz)madzarellaNo ratings yet

- Taxation I Reviewer For MidtermDocument23 pagesTaxation I Reviewer For MidtermKaren CueNo ratings yet

- 2019 Bar Review: Taxation Law Chair'S CasesDocument19 pages2019 Bar Review: Taxation Law Chair'S CasesClarisse-joan Bumanglag GarmaNo ratings yet

- Spec Pro Case DigestDocument8 pagesSpec Pro Case DigestCharmie Fuentes AmpalayohanNo ratings yet

- Cancio vs. IsipDocument4 pagesCancio vs. IsipWILHELMINA CUYUGANNo ratings yet

- P.I. Manufacturing v. P.I. Manufacturing SupervisorsDocument14 pagesP.I. Manufacturing v. P.I. Manufacturing SupervisorsChatNo ratings yet

- Deutsche Bank vs. CirDocument1 pageDeutsche Bank vs. CirDee WhyNo ratings yet

- Today's Topics & Notes (Remedial Law Review I)Document35 pagesToday's Topics & Notes (Remedial Law Review I)Miguel Anas Jr.No ratings yet

- Corpo Case DigestDocument8 pagesCorpo Case DigestJasOn EvangelistaNo ratings yet

- Law On Taxation MidtermDocument32 pagesLaw On Taxation Midtermroselleyap20No ratings yet

- A. 5. C. Commissioner of Internal Revenue vs. Bank of The Philippine IslandsDocument3 pagesA. 5. C. Commissioner of Internal Revenue vs. Bank of The Philippine IslandsasdfghjkattNo ratings yet

- Supreme Court of Canada C: Canada V. Glaxosmithkline Inc., 2012 SCC 52, (2012) 3 D: 20121018 D: 33874 B: Her Majesty The QueenDocument39 pagesSupreme Court of Canada C: Canada V. Glaxosmithkline Inc., 2012 SCC 52, (2012) 3 D: 20121018 D: 33874 B: Her Majesty The QueenJm CruzNo ratings yet

- NIRC CodalDocument67 pagesNIRC CodalJo-Al GealonNo ratings yet

- Tax Digest 51 55Document11 pagesTax Digest 51 55glaiNo ratings yet

- Garcia V Pajaro DigestDocument1 pageGarcia V Pajaro DigestOtep Belciña Lumabas100% (1)

- Caltex Philippines v. COA (GR 92585, 8 May 1992)Document29 pagesCaltex Philippines v. COA (GR 92585, 8 May 1992)Cheska VergaraNo ratings yet

- Mangaliag V CatubigDocument1 pageMangaliag V CatubigMiguel CastricionesNo ratings yet

- CIR Vs Burmeisters & Wain Scandinavian GR No. 153205Document9 pagesCIR Vs Burmeisters & Wain Scandinavian GR No. 153205Kimberly SendinNo ratings yet

- Bautista v. Commission On ElectionsDocument25 pagesBautista v. Commission On Electionsryusuki takahashiNo ratings yet

- Tax SparingDocument5 pagesTax Sparingfrancis_asd2003No ratings yet

- R-Civ04 Jurisdiction of The RTCDocument14 pagesR-Civ04 Jurisdiction of The RTCbatasnimatiastigasNo ratings yet

- CIR Vs Fortune Tobacco Corp., GR No. 1677274-75, July 21,2008Document14 pagesCIR Vs Fortune Tobacco Corp., GR No. 1677274-75, July 21,2008Jomari ParejaNo ratings yet

- Tax 1 CasesDocument111 pagesTax 1 CasesJayson Leo VisitacionNo ratings yet

- CIR Vs Fortune TobaccoDocument6 pagesCIR Vs Fortune TobaccoJohnde MartinezNo ratings yet

- NPC AdvisoryOpinionNo. 2017-024Document3 pagesNPC AdvisoryOpinionNo. 2017-024Jay TabuzoNo ratings yet

- Winter Vs NovaritsDocument6 pagesWinter Vs NovaritsJay TabuzoNo ratings yet

- Rollins Ranches, LLC v. WatsonDocument5 pagesRollins Ranches, LLC v. WatsonJay TabuzoNo ratings yet

- NPC AdvisoryOpinionNo. 2017-009Document2 pagesNPC AdvisoryOpinionNo. 2017-009Jay TabuzoNo ratings yet

- How Does The Philippines' Data Privacy Act Compare With The GDPR?Document4 pagesHow Does The Philippines' Data Privacy Act Compare With The GDPR?Jay TabuzoNo ratings yet

- NPC AdvisoryOpinionNo. 2017-005Document3 pagesNPC AdvisoryOpinionNo. 2017-005Jay TabuzoNo ratings yet

- Future Select Vs TremontDocument8 pagesFuture Select Vs TremontJay TabuzoNo ratings yet

- Giorgi Glob. Holdings v. SmulskiDocument3 pagesGiorgi Glob. Holdings v. SmulskiJay TabuzoNo ratings yet

- Kamelgard Vs MacuraDocument9 pagesKamelgard Vs MacuraJay TabuzoNo ratings yet

- 12.hwang V JapanDocument6 pages12.hwang V JapanJay TabuzoNo ratings yet

- 07 Jesner v. Arab BankDocument91 pages07 Jesner v. Arab BankJay TabuzoNo ratings yet

- 11.colvin v. Syrian Arab RepublicDocument19 pages11.colvin v. Syrian Arab RepublicJay TabuzoNo ratings yet

- 10 Bangladesh Bank v. Rizal Commercial Banking Corporation, Et Al.Document25 pages10 Bangladesh Bank v. Rizal Commercial Banking Corporation, Et Al.Jay TabuzoNo ratings yet

- in Re KMHDocument19 pagesin Re KMHJay TabuzoNo ratings yet

- Montinola Vs VillanuevaDocument6 pagesMontinola Vs VillanuevaJay TabuzoNo ratings yet

- Government Vs FrankDocument2 pagesGovernment Vs FrankJay TabuzoNo ratings yet

- Rio Y Compania Vs DatuDocument5 pagesRio Y Compania Vs DatuJay TabuzoNo ratings yet

- Second Division (G.R. NO. 156021, September 23, 2005) : Tinga, J.Document9 pagesSecond Division (G.R. NO. 156021, September 23, 2005) : Tinga, J.Jay TabuzoNo ratings yet

- In RE Matter of Telesforo de Dios Vs Tomas OsmenaDocument5 pagesIn RE Matter of Telesforo de Dios Vs Tomas OsmenaJay TabuzoNo ratings yet

- Current & Saving Account Statement: Vijaya B S/O Belli Karadigodu Siddapur SiddapurDocument13 pagesCurrent & Saving Account Statement: Vijaya B S/O Belli Karadigodu Siddapur SiddapurWipro Foundation KARNo ratings yet

- Income Tax Law & Practice-Lesson - 1 To 12Document250 pagesIncome Tax Law & Practice-Lesson - 1 To 12Space ResearchNo ratings yet

- Tally: Chap-1:-Company Creation & Deletation Create CompanyDocument32 pagesTally: Chap-1:-Company Creation & Deletation Create CompanysananathaniNo ratings yet

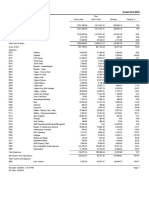

- Income Statement Comparison For The 2 Periods Ended 2/24/2019 Rowes IGADocument2 pagesIncome Statement Comparison For The 2 Periods Ended 2/24/2019 Rowes IGAaribandikNo ratings yet

- Look Back Effect Projet PresentationDocument17 pagesLook Back Effect Projet Presentationapi-242930262No ratings yet

- Contract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)Document3 pagesContract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)JANNNo ratings yet

- Floor Slab Chisling 3rd-5th CertfDocument1 pageFloor Slab Chisling 3rd-5th CertfwendmagegnNo ratings yet

- Concepts in Federal Taxation 2013 20th Edition Murphy Test Bank DownloadDocument141 pagesConcepts in Federal Taxation 2013 20th Edition Murphy Test Bank DownloadDavid Clark100% (23)

- Donation Political PartiesDocument4 pagesDonation Political Partiessockalingam.mNo ratings yet

- Value Added by Subtractive MethodDocument17 pagesValue Added by Subtractive MethodmurtadhoNo ratings yet

- Vat KsaDocument32 pagesVat Ksaabdul mateenNo ratings yet

- Analysis Finance AcctDocument3 pagesAnalysis Finance AcctAsfatin AmranNo ratings yet

- Income Tax Basic Definitions and TermsDocument13 pagesIncome Tax Basic Definitions and TermsshivamNo ratings yet

- Form 12B - Previous Employment Income DetailsDocument2 pagesForm 12B - Previous Employment Income DetailsSachin5586No ratings yet

- Account Statement: Gedung Arthaloka Jl. Jenderal Sudirman Kav 2, Jakarta 10220, IndonesiaDocument50 pagesAccount Statement: Gedung Arthaloka Jl. Jenderal Sudirman Kav 2, Jakarta 10220, Indonesiaalizza nourNo ratings yet

- The Globetrotter'S Guide To: Multi-Currency Travel CardDocument22 pagesThe Globetrotter'S Guide To: Multi-Currency Travel CardRitvikTiwariNo ratings yet

- HMB Ispat Pi 81022Document1 pageHMB Ispat Pi 81022Suman PramanikNo ratings yet

- Limpan Investment Corp V CIRDocument1 pageLimpan Investment Corp V CIRReena MaNo ratings yet

- Cir V. Central Luzon Drug Corporation, GR No. 148512, 2006-06-26Document2 pagesCir V. Central Luzon Drug Corporation, GR No. 148512, 2006-06-26Crisbon ApalisNo ratings yet

- WebsiteDocument17 pagesWebsiteAkansha GuptaNo ratings yet

- The Negotiable Instruments Act, 1881Document55 pagesThe Negotiable Instruments Act, 1881meghna_mg8780% (5)

- En - WRC WhitepaperDocument112 pagesEn - WRC WhitepaperHerdi R FauziNo ratings yet

- Rajesh Patel ITR 04 23Document4 pagesRajesh Patel ITR 04 23The KingNo ratings yet

- BirDocument8 pagesBirDominique VasalloNo ratings yet

- DXBR001900136Document2 pagesDXBR001900136Muhammad WaqasNo ratings yet

- TAxable PurchasesDocument13 pagesTAxable PurchasesLichchhwi foods (i) pvt. ltdNo ratings yet

- Tax Saving Schemes: in Partial Fulfilment of The Requirements For The Award of The Degree inDocument8 pagesTax Saving Schemes: in Partial Fulfilment of The Requirements For The Award of The Degree inMOHAMMED KHAYYUMNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument9 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAnant ParasharNo ratings yet