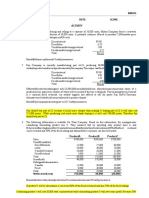

Part A - JW Sports Supplies Cost Categorization and Calculation

Part A - JW Sports Supplies Cost Categorization and Calculation

You might also like

- JW SPORT SuppliesDocument5 pagesJW SPORT SuppliesVishvesh Soni100% (4)

- Columbia 2017 PDFDocument190 pagesColumbia 2017 PDFN100% (3)

- Michael Porters Model For Industry and Competitor AnalysisDocument9 pagesMichael Porters Model For Industry and Competitor AnalysisbagumaNo ratings yet

- Economic Nationalism - Claro M. RectoDocument58 pagesEconomic Nationalism - Claro M. RectoGabriel Achacoso Mon76% (17)

- Problem 2-14 Product Cost Sunk Cost Direct LaborDocument8 pagesProblem 2-14 Product Cost Sunk Cost Direct LaborarijitmajeeNo ratings yet

- UTS AkutansiDocument24 pagesUTS AkutansiAbraham KristiyonoNo ratings yet

- Problem Unit 4Document7 pagesProblem Unit 4meenasaratha100% (1)

- General Discussion Absorption Costing Variable Costing: FixedDocument4 pagesGeneral Discussion Absorption Costing Variable Costing: FixedHassan KhanNo ratings yet

- 05 Activity 3Document1 page05 Activity 3Reikenh SalesNo ratings yet

- Day 4 (My)Document11 pagesDay 4 (My)Jhilmil JeswaniNo ratings yet

- Variable Costing April Revenues 8,400,000Document10 pagesVariable Costing April Revenues 8,400,000Hiền NguyễnNo ratings yet

- Finals Unit 4 Exercise - Variable and Absorption CostingDocument2 pagesFinals Unit 4 Exercise - Variable and Absorption CostingMelo RiegoNo ratings yet

- Quiz No. 4 - Variable and Absorption CostingDocument2 pagesQuiz No. 4 - Variable and Absorption CostingRio Cyrel CelleroNo ratings yet

- Chapter 9 - Alwi Syahnur Nasution - 120104160048Document6 pagesChapter 9 - Alwi Syahnur Nasution - 120104160048Nugrah LesmanaNo ratings yet

- Narsee Monjee Institute of Management StudiesDocument8 pagesNarsee Monjee Institute of Management StudiesSHIVANGI AGRAWALNo ratings yet

- Accounting Chapter 06 Full SolutionDocument15 pagesAccounting Chapter 06 Full SolutionAsadullahil GalibNo ratings yet

- Chapter 10 SCMDocument15 pagesChapter 10 SCMAliyah Francine Gojo CruzNo ratings yet

- Variable and Absorption CostingDocument52 pagesVariable and Absorption CostingcruzchristophertangaNo ratings yet

- Ch8 PDFDocument11 pagesCh8 PDFGiang NguyenNo ratings yet

- Cost Accounting - ABC Vs Variable CostingDocument3 pagesCost Accounting - ABC Vs Variable CostingJaycel Yam-Yam VerancesNo ratings yet

- Problems On Pricing DecisionsDocument15 pagesProblems On Pricing Decisionschintan desaiNo ratings yet

- Problems On Pricing DecisionsDocument15 pagesProblems On Pricing DecisionsMae-shane SagayoNo ratings yet

- Assignment 2 - CMADocument9 pagesAssignment 2 - CMAVivek SharanNo ratings yet

- MAS.05 Drill Variable and Absorption CostingDocument5 pagesMAS.05 Drill Variable and Absorption Costingace ender zeroNo ratings yet

- Chapter 11 SCMDocument22 pagesChapter 11 SCMAliyah Francine Gojo CruzNo ratings yet

- Grand Test - Question PaperDocument3 pagesGrand Test - Question PaperWaseim khan Barik zaiNo ratings yet

- Accounting Act6Document2 pagesAccounting Act6Eren YeagerNo ratings yet

- Static Budgets and Performance Reports Static Budgets Are Prepared For A SingleDocument6 pagesStatic Budgets and Performance Reports Static Budgets Are Prepared For A SingleAbisheNo ratings yet

- Institute of Cost and Management Accountants of PakistanDocument11 pagesInstitute of Cost and Management Accountants of PakistanAsad RiazNo ratings yet

- Variable and Absorption Costing Problems Without SolutionsDocument4 pagesVariable and Absorption Costing Problems Without SolutionsMeca CorpuzNo ratings yet

- Flexible and Static Budgets ReviewerDocument13 pagesFlexible and Static Budgets ReviewerLilac heartNo ratings yet

- Budgeting and Budgetary ControlDocument2 pagesBudgeting and Budgetary ControlpalkeeNo ratings yet

- Jose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyDocument6 pagesJose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyBernadette CaduyacNo ratings yet

- Costing Systems - Lessons ExamplesDocument15 pagesCosting Systems - Lessons ExamplesNicolasNo ratings yet

- CMA-II BookDocument38 pagesCMA-II BookmaxsuzsxoxoNo ratings yet

- 5 Job CostingDocument22 pages5 Job CostingAbimanyu Shenil0% (1)

- Tut 8 - Management AccountingDocument29 pagesTut 8 - Management AccountingTao LoheNo ratings yet

- Problem 3 4 Chapter 14Document6 pagesProblem 3 4 Chapter 14freaann03No ratings yet

- MAE RevisionDocument57 pagesMAE RevisionsaloniNo ratings yet

- Departmental PEQDocument38 pagesDepartmental PEQRishikaNo ratings yet

- CostconDocument33 pagesCostconDanica VillaganteNo ratings yet

- Abc1 - FinalDocument7 pagesAbc1 - FinalSakshi ShardaNo ratings yet

- FINAL Acctg7Document5 pagesFINAL Acctg7Romcel FlorendoNo ratings yet

- Alvaro, Fernel Jean C. AE212-1741 TTHS 3-5PM Exercise 8-2. Joint Cost AllocationDocument4 pagesAlvaro, Fernel Jean C. AE212-1741 TTHS 3-5PM Exercise 8-2. Joint Cost AllocationNhel AlvaroNo ratings yet

- CAC Computations Chap 4 1 20Document9 pagesCAC Computations Chap 4 1 20rochelle lagmayNo ratings yet

- Marginal Costing .. Feb 2020: Q. 1 Denton Company (Rupees in '000') 20x4 20x5Document5 pagesMarginal Costing .. Feb 2020: Q. 1 Denton Company (Rupees in '000') 20x4 20x5신두No ratings yet

- ProblemsDocument11 pagesProblemsMohamed RefaayNo ratings yet

- Variableabsorption CostingDocument77 pagesVariableabsorption Costingandrea arapocNo ratings yet

- Byproduct Mission MCQDocument3 pagesByproduct Mission MCQRohit ThandarNo ratings yet

- Act.4-8 Ae23Document6 pagesAct.4-8 Ae23Damian Sheila MaeNo ratings yet

- Exercises Absorption and Variable CostingPAUL ANTHONY DE JESUSDocument4 pagesExercises Absorption and Variable CostingPAUL ANTHONY DE JESUSMeng DanNo ratings yet

- 1.2.1 Assignments - Cost Concepts and Classifications (Answers and Solutions)Document8 pages1.2.1 Assignments - Cost Concepts and Classifications (Answers and Solutions)Roselyn LumbaoNo ratings yet

- Marwa Year 1 Using Marginal Costing ApproachDocument6 pagesMarwa Year 1 Using Marginal Costing ApproachMak PussNo ratings yet

- DepartmentalDocument17 pagesDepartmentalPapiya DeyNo ratings yet

- Tutorial 1 - Topic 4 - OAR - QDocument6 pagesTutorial 1 - Topic 4 - OAR - QJong HannahNo ratings yet

- 8 33 PricingDocument1 page8 33 Pricinganonymous.me0201No ratings yet

- Ae 212 Exercise 8Document4 pagesAe 212 Exercise 8Nhel AlvaroNo ratings yet

- CMA Garrison SuggestedSolutions Chap2Document12 pagesCMA Garrison SuggestedSolutions Chap2PIYUSH SINGHNo ratings yet

- Group AssignmentDocument7 pagesGroup Assignmentsaidkhatib368No ratings yet

- Master Question (Mixed With Process Costing) - Q ADocument3 pagesMaster Question (Mixed With Process Costing) - Q AMuaaz NayyarNo ratings yet

- SVKM'S Nmims Anil Surendra Modi School of Commerce Batch: 2018 - 2021 Academic Year: 2020 - 2021 Subject: Management Accounting Date: 5 January 2021Document24 pagesSVKM'S Nmims Anil Surendra Modi School of Commerce Batch: 2018 - 2021 Academic Year: 2020 - 2021 Subject: Management Accounting Date: 5 January 2021Madhuram SharmaNo ratings yet

- Bio Coal EstimateDocument1 pageBio Coal EstimateDhananjay KulkarniNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Financial Ratio Analysis of Square Pharmaceuticals Limited: Asif AhmedDocument24 pagesFinancial Ratio Analysis of Square Pharmaceuticals Limited: Asif AhmedMD. MUNTASIR MAMUN SHOVONNo ratings yet

- Topic 11 - Open-Economy Macroeconomics - Basic Concepts.Document36 pagesTopic 11 - Open-Economy Macroeconomics - Basic Concepts.Trung Hai TrieuNo ratings yet

- Quiz Module 1 FINALDocument4 pagesQuiz Module 1 FINALeia aieNo ratings yet

- Tax Invoice: Agarwal Impex 21-22/745 5-Feb-2022Document2 pagesTax Invoice: Agarwal Impex 21-22/745 5-Feb-2022bhola.vilesh7No ratings yet

- Final CompilationDocument85 pagesFinal CompilationRakesh KushwahaNo ratings yet

- Ajax Fiori-R-07092017Document7 pagesAjax Fiori-R-07092017parimal.rodeNo ratings yet

- SMO 105 Group Course Work Group 4I "Bright Future Food LLC" (Shavelle Lee Vasca, Ming Yang, Shuo Chen) Market Entry Strategies and RationaleDocument3 pagesSMO 105 Group Course Work Group 4I "Bright Future Food LLC" (Shavelle Lee Vasca, Ming Yang, Shuo Chen) Market Entry Strategies and Rationaleshavelle leevascaNo ratings yet

- Melihat Sisi Pengusaha Sosial Dengan Bottle Refill Station Sebagai Solusi Pengendalian Kemasan Sekali Pakai Untuk Kelestarian LingkunganDocument18 pagesMelihat Sisi Pengusaha Sosial Dengan Bottle Refill Station Sebagai Solusi Pengendalian Kemasan Sekali Pakai Untuk Kelestarian LingkunganCuters TresnoNo ratings yet

- Tle EntrepreneurshipDocument2 pagesTle EntrepreneurshipMark Anthony LibecoNo ratings yet

- Digital Marketing PPT - 2021 - ConsellingDocument32 pagesDigital Marketing PPT - 2021 - ConsellingDolly DharmshaktuNo ratings yet

- Contoh Studi Kasus ZachmanDocument15 pagesContoh Studi Kasus Zachmanindra sunardiNo ratings yet

- Kuaishou Technology Announces Fourth Quarter and Full Year 2021 Financial ResultsDocument4 pagesKuaishou Technology Announces Fourth Quarter and Full Year 2021 Financial Resultsmuhamad.ariapujaNo ratings yet

- MANG6296 AssignmentDocument28 pagesMANG6296 Assignmentxu zhenchuanNo ratings yet

- Investment Decision - IciciDocument8 pagesInvestment Decision - Icicimohammed khayyumNo ratings yet

- BCG NBFC Sector Update H1FY24Document48 pagesBCG NBFC Sector Update H1FY24ashi.reportsNo ratings yet

- Dayton Hudson Corporation Conscience and ControlDocument15 pagesDayton Hudson Corporation Conscience and Controlsajal sazzadNo ratings yet

- Corp Law Yash TiwariDocument30 pagesCorp Law Yash TiwariMani YadavNo ratings yet

- Hsieh Mcconnell DonationsDocument9 pagesHsieh Mcconnell DonationsResourcesNo ratings yet

- Support To Operational PlanDocument2 pagesSupport To Operational PlanreshadNo ratings yet

- Module 5 BankingDocument42 pagesModule 5 Bankingg.prasanna saiNo ratings yet

- HRM Project Ultra Tech CementDocument51 pagesHRM Project Ultra Tech CementRoy Yadav100% (1)

- Razelle Ann B. Dapilaga 11 Abm, Peter DruckerDocument3 pagesRazelle Ann B. Dapilaga 11 Abm, Peter DruckerJasmine ActaNo ratings yet

- Whitepaper 2Document8 pagesWhitepaper 2Minhayati BklNo ratings yet

- Price List OGOship Logistics 2022 DE-SOL ENDocument17 pagesPrice List OGOship Logistics 2022 DE-SOL ENDraganaNo ratings yet

- Rangga Fakhrurriza - Kelompok 6 Konflik Dan NegosiasiDocument6 pagesRangga Fakhrurriza - Kelompok 6 Konflik Dan NegosiasiRangga FakhrurrizaKls AAkt 2021No ratings yet

- Presentation On Government BudgetingDocument2 pagesPresentation On Government BudgetingSherry Gonzales ÜNo ratings yet

- China Pastry Bread Mfg. Industry Profile Cic1411Document8 pagesChina Pastry Bread Mfg. Industry Profile Cic1411AllChinaReports.comNo ratings yet

Download as pdf or txt

You might also like

- JW SPORT SuppliesDocument5 pagesJW SPORT SuppliesVishvesh Soni100% (4)

- Columbia 2017 PDFDocument190 pagesColumbia 2017 PDFN100% (3)

- Michael Porters Model For Industry and Competitor AnalysisDocument9 pagesMichael Porters Model For Industry and Competitor AnalysisbagumaNo ratings yet

- Economic Nationalism - Claro M. RectoDocument58 pagesEconomic Nationalism - Claro M. RectoGabriel Achacoso Mon76% (17)

- Problem 2-14 Product Cost Sunk Cost Direct LaborDocument8 pagesProblem 2-14 Product Cost Sunk Cost Direct LaborarijitmajeeNo ratings yet

- UTS AkutansiDocument24 pagesUTS AkutansiAbraham KristiyonoNo ratings yet

- Problem Unit 4Document7 pagesProblem Unit 4meenasaratha100% (1)

- General Discussion Absorption Costing Variable Costing: FixedDocument4 pagesGeneral Discussion Absorption Costing Variable Costing: FixedHassan KhanNo ratings yet

- 05 Activity 3Document1 page05 Activity 3Reikenh SalesNo ratings yet

- Day 4 (My)Document11 pagesDay 4 (My)Jhilmil JeswaniNo ratings yet

- Variable Costing April Revenues 8,400,000Document10 pagesVariable Costing April Revenues 8,400,000Hiền NguyễnNo ratings yet

- Finals Unit 4 Exercise - Variable and Absorption CostingDocument2 pagesFinals Unit 4 Exercise - Variable and Absorption CostingMelo RiegoNo ratings yet

- Quiz No. 4 - Variable and Absorption CostingDocument2 pagesQuiz No. 4 - Variable and Absorption CostingRio Cyrel CelleroNo ratings yet

- Chapter 9 - Alwi Syahnur Nasution - 120104160048Document6 pagesChapter 9 - Alwi Syahnur Nasution - 120104160048Nugrah LesmanaNo ratings yet

- Narsee Monjee Institute of Management StudiesDocument8 pagesNarsee Monjee Institute of Management StudiesSHIVANGI AGRAWALNo ratings yet

- Accounting Chapter 06 Full SolutionDocument15 pagesAccounting Chapter 06 Full SolutionAsadullahil GalibNo ratings yet

- Chapter 10 SCMDocument15 pagesChapter 10 SCMAliyah Francine Gojo CruzNo ratings yet

- Variable and Absorption CostingDocument52 pagesVariable and Absorption CostingcruzchristophertangaNo ratings yet

- Ch8 PDFDocument11 pagesCh8 PDFGiang NguyenNo ratings yet

- Cost Accounting - ABC Vs Variable CostingDocument3 pagesCost Accounting - ABC Vs Variable CostingJaycel Yam-Yam VerancesNo ratings yet

- Problems On Pricing DecisionsDocument15 pagesProblems On Pricing Decisionschintan desaiNo ratings yet

- Problems On Pricing DecisionsDocument15 pagesProblems On Pricing DecisionsMae-shane SagayoNo ratings yet

- Assignment 2 - CMADocument9 pagesAssignment 2 - CMAVivek SharanNo ratings yet

- MAS.05 Drill Variable and Absorption CostingDocument5 pagesMAS.05 Drill Variable and Absorption Costingace ender zeroNo ratings yet

- Chapter 11 SCMDocument22 pagesChapter 11 SCMAliyah Francine Gojo CruzNo ratings yet

- Grand Test - Question PaperDocument3 pagesGrand Test - Question PaperWaseim khan Barik zaiNo ratings yet

- Accounting Act6Document2 pagesAccounting Act6Eren YeagerNo ratings yet

- Static Budgets and Performance Reports Static Budgets Are Prepared For A SingleDocument6 pagesStatic Budgets and Performance Reports Static Budgets Are Prepared For A SingleAbisheNo ratings yet

- Institute of Cost and Management Accountants of PakistanDocument11 pagesInstitute of Cost and Management Accountants of PakistanAsad RiazNo ratings yet

- Variable and Absorption Costing Problems Without SolutionsDocument4 pagesVariable and Absorption Costing Problems Without SolutionsMeca CorpuzNo ratings yet

- Flexible and Static Budgets ReviewerDocument13 pagesFlexible and Static Budgets ReviewerLilac heartNo ratings yet

- Budgeting and Budgetary ControlDocument2 pagesBudgeting and Budgetary ControlpalkeeNo ratings yet

- Jose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyDocument6 pagesJose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyBernadette CaduyacNo ratings yet

- Costing Systems - Lessons ExamplesDocument15 pagesCosting Systems - Lessons ExamplesNicolasNo ratings yet

- CMA-II BookDocument38 pagesCMA-II BookmaxsuzsxoxoNo ratings yet

- 5 Job CostingDocument22 pages5 Job CostingAbimanyu Shenil0% (1)

- Tut 8 - Management AccountingDocument29 pagesTut 8 - Management AccountingTao LoheNo ratings yet

- Problem 3 4 Chapter 14Document6 pagesProblem 3 4 Chapter 14freaann03No ratings yet

- MAE RevisionDocument57 pagesMAE RevisionsaloniNo ratings yet

- Departmental PEQDocument38 pagesDepartmental PEQRishikaNo ratings yet

- CostconDocument33 pagesCostconDanica VillaganteNo ratings yet

- Abc1 - FinalDocument7 pagesAbc1 - FinalSakshi ShardaNo ratings yet

- FINAL Acctg7Document5 pagesFINAL Acctg7Romcel FlorendoNo ratings yet

- Alvaro, Fernel Jean C. AE212-1741 TTHS 3-5PM Exercise 8-2. Joint Cost AllocationDocument4 pagesAlvaro, Fernel Jean C. AE212-1741 TTHS 3-5PM Exercise 8-2. Joint Cost AllocationNhel AlvaroNo ratings yet

- CAC Computations Chap 4 1 20Document9 pagesCAC Computations Chap 4 1 20rochelle lagmayNo ratings yet

- Marginal Costing .. Feb 2020: Q. 1 Denton Company (Rupees in '000') 20x4 20x5Document5 pagesMarginal Costing .. Feb 2020: Q. 1 Denton Company (Rupees in '000') 20x4 20x5신두No ratings yet

- ProblemsDocument11 pagesProblemsMohamed RefaayNo ratings yet

- Variableabsorption CostingDocument77 pagesVariableabsorption Costingandrea arapocNo ratings yet

- Byproduct Mission MCQDocument3 pagesByproduct Mission MCQRohit ThandarNo ratings yet

- Act.4-8 Ae23Document6 pagesAct.4-8 Ae23Damian Sheila MaeNo ratings yet

- Exercises Absorption and Variable CostingPAUL ANTHONY DE JESUSDocument4 pagesExercises Absorption and Variable CostingPAUL ANTHONY DE JESUSMeng DanNo ratings yet

- 1.2.1 Assignments - Cost Concepts and Classifications (Answers and Solutions)Document8 pages1.2.1 Assignments - Cost Concepts and Classifications (Answers and Solutions)Roselyn LumbaoNo ratings yet

- Marwa Year 1 Using Marginal Costing ApproachDocument6 pagesMarwa Year 1 Using Marginal Costing ApproachMak PussNo ratings yet

- DepartmentalDocument17 pagesDepartmentalPapiya DeyNo ratings yet

- Tutorial 1 - Topic 4 - OAR - QDocument6 pagesTutorial 1 - Topic 4 - OAR - QJong HannahNo ratings yet

- 8 33 PricingDocument1 page8 33 Pricinganonymous.me0201No ratings yet

- Ae 212 Exercise 8Document4 pagesAe 212 Exercise 8Nhel AlvaroNo ratings yet

- CMA Garrison SuggestedSolutions Chap2Document12 pagesCMA Garrison SuggestedSolutions Chap2PIYUSH SINGHNo ratings yet

- Group AssignmentDocument7 pagesGroup Assignmentsaidkhatib368No ratings yet

- Master Question (Mixed With Process Costing) - Q ADocument3 pagesMaster Question (Mixed With Process Costing) - Q AMuaaz NayyarNo ratings yet

- SVKM'S Nmims Anil Surendra Modi School of Commerce Batch: 2018 - 2021 Academic Year: 2020 - 2021 Subject: Management Accounting Date: 5 January 2021Document24 pagesSVKM'S Nmims Anil Surendra Modi School of Commerce Batch: 2018 - 2021 Academic Year: 2020 - 2021 Subject: Management Accounting Date: 5 January 2021Madhuram SharmaNo ratings yet

- Bio Coal EstimateDocument1 pageBio Coal EstimateDhananjay KulkarniNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Financial Ratio Analysis of Square Pharmaceuticals Limited: Asif AhmedDocument24 pagesFinancial Ratio Analysis of Square Pharmaceuticals Limited: Asif AhmedMD. MUNTASIR MAMUN SHOVONNo ratings yet

- Topic 11 - Open-Economy Macroeconomics - Basic Concepts.Document36 pagesTopic 11 - Open-Economy Macroeconomics - Basic Concepts.Trung Hai TrieuNo ratings yet

- Quiz Module 1 FINALDocument4 pagesQuiz Module 1 FINALeia aieNo ratings yet

- Tax Invoice: Agarwal Impex 21-22/745 5-Feb-2022Document2 pagesTax Invoice: Agarwal Impex 21-22/745 5-Feb-2022bhola.vilesh7No ratings yet

- Final CompilationDocument85 pagesFinal CompilationRakesh KushwahaNo ratings yet

- Ajax Fiori-R-07092017Document7 pagesAjax Fiori-R-07092017parimal.rodeNo ratings yet

- SMO 105 Group Course Work Group 4I "Bright Future Food LLC" (Shavelle Lee Vasca, Ming Yang, Shuo Chen) Market Entry Strategies and RationaleDocument3 pagesSMO 105 Group Course Work Group 4I "Bright Future Food LLC" (Shavelle Lee Vasca, Ming Yang, Shuo Chen) Market Entry Strategies and Rationaleshavelle leevascaNo ratings yet

- Melihat Sisi Pengusaha Sosial Dengan Bottle Refill Station Sebagai Solusi Pengendalian Kemasan Sekali Pakai Untuk Kelestarian LingkunganDocument18 pagesMelihat Sisi Pengusaha Sosial Dengan Bottle Refill Station Sebagai Solusi Pengendalian Kemasan Sekali Pakai Untuk Kelestarian LingkunganCuters TresnoNo ratings yet

- Tle EntrepreneurshipDocument2 pagesTle EntrepreneurshipMark Anthony LibecoNo ratings yet

- Digital Marketing PPT - 2021 - ConsellingDocument32 pagesDigital Marketing PPT - 2021 - ConsellingDolly DharmshaktuNo ratings yet

- Contoh Studi Kasus ZachmanDocument15 pagesContoh Studi Kasus Zachmanindra sunardiNo ratings yet

- Kuaishou Technology Announces Fourth Quarter and Full Year 2021 Financial ResultsDocument4 pagesKuaishou Technology Announces Fourth Quarter and Full Year 2021 Financial Resultsmuhamad.ariapujaNo ratings yet

- MANG6296 AssignmentDocument28 pagesMANG6296 Assignmentxu zhenchuanNo ratings yet

- Investment Decision - IciciDocument8 pagesInvestment Decision - Icicimohammed khayyumNo ratings yet

- BCG NBFC Sector Update H1FY24Document48 pagesBCG NBFC Sector Update H1FY24ashi.reportsNo ratings yet

- Dayton Hudson Corporation Conscience and ControlDocument15 pagesDayton Hudson Corporation Conscience and Controlsajal sazzadNo ratings yet

- Corp Law Yash TiwariDocument30 pagesCorp Law Yash TiwariMani YadavNo ratings yet

- Hsieh Mcconnell DonationsDocument9 pagesHsieh Mcconnell DonationsResourcesNo ratings yet

- Support To Operational PlanDocument2 pagesSupport To Operational PlanreshadNo ratings yet

- Module 5 BankingDocument42 pagesModule 5 Bankingg.prasanna saiNo ratings yet

- HRM Project Ultra Tech CementDocument51 pagesHRM Project Ultra Tech CementRoy Yadav100% (1)

- Razelle Ann B. Dapilaga 11 Abm, Peter DruckerDocument3 pagesRazelle Ann B. Dapilaga 11 Abm, Peter DruckerJasmine ActaNo ratings yet

- Whitepaper 2Document8 pagesWhitepaper 2Minhayati BklNo ratings yet

- Price List OGOship Logistics 2022 DE-SOL ENDocument17 pagesPrice List OGOship Logistics 2022 DE-SOL ENDraganaNo ratings yet

- Rangga Fakhrurriza - Kelompok 6 Konflik Dan NegosiasiDocument6 pagesRangga Fakhrurriza - Kelompok 6 Konflik Dan NegosiasiRangga FakhrurrizaKls AAkt 2021No ratings yet

- Presentation On Government BudgetingDocument2 pagesPresentation On Government BudgetingSherry Gonzales ÜNo ratings yet

- China Pastry Bread Mfg. Industry Profile Cic1411Document8 pagesChina Pastry Bread Mfg. Industry Profile Cic1411AllChinaReports.comNo ratings yet