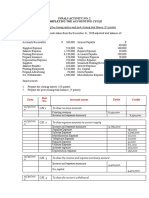

Activity 7 Adjusting Entries and Accounting Policy

Activity 7 Adjusting Entries and Accounting Policy

You might also like

- Activity 8 JournalizingDocument6 pagesActivity 8 Journalizingdra_gon86% (14)

- Madelyn Rialubin Travel Agency Adjusting Entries AdjustedDocument5 pagesMadelyn Rialubin Travel Agency Adjusting Entries AdjustedJustine Almodiel100% (1)

- Quiz 1Document8 pagesQuiz 1Lyca Mae Cubangbang67% (3)

- Comprehensive Problem 23Document29 pagesComprehensive Problem 23Nicole Fidelson100% (2)

- Problem 15 - Group 5Document9 pagesProblem 15 - Group 5Francine TorresNo ratings yet

- Adjusting Entries Exercises - EditedDocument4 pagesAdjusting Entries Exercises - EditedCINDY LIAN CABILLON100% (2)

- Closing Entries (Step 7) & Post Closing Trial Balance (Step 8)Document1 pageClosing Entries (Step 7) & Post Closing Trial Balance (Step 8)Eunice Villacacan33% (3)

- Work Sheet Moises Dondoyano Information SystemDocument1 pageWork Sheet Moises Dondoyano Information SystemRJ DAVE DURUHA100% (5)

- ACT1101, PRB, Midterm, Wit Ans KeyDocument5 pagesACT1101, PRB, Midterm, Wit Ans KeyDyen100% (1)

- ASPL3 Activity 3-6 DoneDocument7 pagesASPL3 Activity 3-6 DoneConcepcion Family33% (3)

- Journal (Remedios Palaganas)Document2 pagesJournal (Remedios Palaganas)Mika CunananNo ratings yet

- Accounting ProblemsDocument3 pagesAccounting ProblemsKeitheia Quidlat67% (3)

- Problem 7 - Group 1Document8 pagesProblem 7 - Group 1Francine Torres100% (4)

- Illustrative Problem Worksheet ADocument6 pagesIllustrative Problem Worksheet AJoy Santos33% (3)

- Chapter 2 JournalizingDocument21 pagesChapter 2 Journalizingkakao100% (1)

- Problem-5 - AFCAR Chapter 3Document9 pagesProblem-5 - AFCAR Chapter 3kakao100% (1)

- Accounting HomeworkDocument6 pagesAccounting HomeworkGavin Ramos100% (2)

- Ebin Belderol TB and WorksheetDocument11 pagesEbin Belderol TB and WorksheetMarielle Ebin100% (3)

- Account Classification Normal Balance Income Statement / Balance Sheet ColumnDocument13 pagesAccount Classification Normal Balance Income Statement / Balance Sheet ColumnRhoda Claire M. Gansobin86% (7)

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- Exercises II - Adjusting TransactionsDocument2 pagesExercises II - Adjusting TransactionsJowjie TV80% (5)

- Laurent e Answer KeyDocument4 pagesLaurent e Answer KeyZee Santisas86% (7)

- Worksheet PalaganasDocument38 pagesWorksheet PalaganasMomo HiraiNo ratings yet

- MODULE-5 Ac 5 inDocument14 pagesMODULE-5 Ac 5 inBlesh Macusi75% (4)

- Requiring Lawyers To Submit Suspicious Transaction Reports PDFDocument13 pagesRequiring Lawyers To Submit Suspicious Transaction Reports PDFGeorge CarmonaNo ratings yet

- Deviations and Non Conformances SOP PDFDocument1 pageDeviations and Non Conformances SOP PDFAlinaNo ratings yet

- Adjusting Entries Christine Gamba CargoDocument5 pagesAdjusting Entries Christine Gamba Cargoelma wagwag100% (2)

- ACC111 Activity 22Document8 pagesACC111 Activity 22Triquesha Marriette Romero Rabi100% (1)

- ACTIVITY NO1and2Document5 pagesACTIVITY NO1and2Patricia Nicole Barrios100% (1)

- Rosalie Balhag CleanersDocument1 pageRosalie Balhag CleanersDominique Abrajano100% (1)

- Catherine Viesca Outdoor Ad Concepts Journal Entries January - December 2020Document4 pagesCatherine Viesca Outdoor Ad Concepts Journal Entries January - December 2020Jamycka Antolin100% (1)

- Travel Agency RubisomethingDocument12 pagesTravel Agency RubisomethingItsRenz YTNo ratings yet

- Pamantasan NG Lungsod NG Valenzuela: Financial Accounting and Reporting I (FAR I)Document5 pagesPamantasan NG Lungsod NG Valenzuela: Financial Accounting and Reporting I (FAR I)Mariane Manangan100% (2)

- AlisuagDocument5 pagesAlisuagAgatha Alcid100% (1)

- EDocument17 pagesEMark Cyphrysse Masiglat67% (3)

- Journal Entries: Edgar DetoyaDocument17 pagesJournal Entries: Edgar DetoyaAntonNo ratings yet

- Total: Adjusting EntriesDocument8 pagesTotal: Adjusting EntriesLj BesaNo ratings yet

- Dr. Nick Marasigan AccountsDocument11 pagesDr. Nick Marasigan AccountsNicole SarmientoNo ratings yet

- C3 - Problem 17 - Correcting A Trial BalanceDocument2 pagesC3 - Problem 17 - Correcting A Trial BalanceLorence John Imperial0% (1)

- Marichu Fornolles Novelties Transactions in December 2020: Date Particulars DebitDocument4 pagesMarichu Fornolles Novelties Transactions in December 2020: Date Particulars DebitHannah Pearl Flores Villar100% (1)

- Eva Cammayo Supply Company Journal Entry May 2021 Agnes Ramos Company Journal Entry May 2021Document7 pagesEva Cammayo Supply Company Journal Entry May 2021 Agnes Ramos Company Journal Entry May 2021Stephen ReloxNo ratings yet

- Accounting Problem 5Document8 pagesAccounting Problem 5Carlo AniNo ratings yet

- Noel Hungria, Adjusting EntriesDocument1 pageNoel Hungria, Adjusting EntriesFeiya Liu100% (2)

- Mads Rialubin Travel Agency WORKSHEET FS TRIAL BALANCEDocument3 pagesMads Rialubin Travel Agency WORKSHEET FS TRIAL BALANCEJowe Ringor Casignia100% (1)

- Exercise 3 Adjusting Entries - Service BusinessDocument2 pagesExercise 3 Adjusting Entries - Service BusinessMarc Viduya75% (4)

- Problem #3: Teresita Nacion Publishers Trial BalanceDocument4 pagesProblem #3: Teresita Nacion Publishers Trial BalanceRhea Sismo-anNo ratings yet

- Nelson Daganta CashDocument10 pagesNelson Daganta CashDan RioNo ratings yet

- Marasigan TransactionDocument20 pagesMarasigan TransactionE.D.J100% (2)

- Teresita Buenaflor ShoesDocument30 pagesTeresita Buenaflor ShoesHannah Pearl Flores Villar100% (1)

- John Bala Company Worksheet: Unadjusted Trial Balance DebitDocument9 pagesJohn Bala Company Worksheet: Unadjusted Trial Balance DebitJekoeNo ratings yet

- ACCA101 Leah May SantiagoDocument9 pagesACCA101 Leah May SantiagoNicole FidelsonNo ratings yet

- Teresita Buenaflor Shoes Worksheet 1 RegineDocument24 pagesTeresita Buenaflor Shoes Worksheet 1 RegineBaby Babe100% (1)

- Elegant Home Decors Worksheet For The Year Ended December 31,20ADocument8 pagesElegant Home Decors Worksheet For The Year Ended December 31,20AChloe CatalunaNo ratings yet

- Noel Hungria, Adjusting EntriesDocument1 pageNoel Hungria, Adjusting EntriesFeiya Liu100% (4)

- Jackielyn Magpantay Chart of AccountsDocument9 pagesJackielyn Magpantay Chart of AccountsIgnite NightNo ratings yet

- Acctgchap 2Document15 pagesAcctgchap 2Anjelika ViescaNo ratings yet

- Journalizing Posting and Preparing A Trial BalanceDocument38 pagesJournalizing Posting and Preparing A Trial BalanceJules Beltran100% (3)

- Acctg Assginment 4 Adjusting EntriesDocument3 pagesAcctg Assginment 4 Adjusting EntriesDaisy Marie A. RoselNo ratings yet

- N MarasiganDocument16 pagesN MarasiganMarikris Cadiente100% (1)

- Financial Statement Worksheet DetoyaDocument8 pagesFinancial Statement Worksheet Detoyasharon emailNo ratings yet

- Adjusting Entries For Bad DebtsDocument6 pagesAdjusting Entries For Bad DebtsKristine IvyNo ratings yet

- ACCTG1 PrefinalsDocument23 pagesACCTG1 PrefinalsJAN RAY CUISON VISPERAS100% (1)

- DDA 1 Niaga C Materials - 4th MeetingDocument32 pagesDDA 1 Niaga C Materials - 4th MeetingZenalina Hadi PutriNo ratings yet

- Explain The Purpose of DerivativesDocument5 pagesExplain The Purpose of DerivativesBlesh MacusiNo ratings yet

- Date Account Title and Explanation Debit Credit: Ref. NoDocument7 pagesDate Account Title and Explanation Debit Credit: Ref. NoBlesh MacusiNo ratings yet

- Name: Joana Marie Bueno Score: - Course/Section: BSA 1-2 Date Submitted: 1/17/2020Document12 pagesName: Joana Marie Bueno Score: - Course/Section: BSA 1-2 Date Submitted: 1/17/2020Blesh MacusiNo ratings yet

- Far Format Journal Posting Balance SheetDocument4 pagesFar Format Journal Posting Balance SheetBlesh MacusiNo ratings yet

- Dasmarinas Duplicators VDocument29 pagesDasmarinas Duplicators VBlesh MacusiNo ratings yet

- Mechyr1 Chapter 10::: Forces and MotionDocument31 pagesMechyr1 Chapter 10::: Forces and MotionAgrata PouloseNo ratings yet

- Compressed Gas Emergency Response Containment VesselsDocument4 pagesCompressed Gas Emergency Response Containment VesselsTzu Huan PengNo ratings yet

- NatwestDocument1 pageNatwestVinay SinghNo ratings yet

- Request For Copy of Tax ReturnDocument2 pagesRequest For Copy of Tax ReturnAsjsjsjsNo ratings yet

- Murder in Baldurs Gate Events SupplementDocument8 pagesMurder in Baldurs Gate Events SupplementDavid L Kriegel100% (3)

- The Courage To Be Happy - Augusto Boal, Legislative Theatre, and The 7th International (1146376)Document11 pagesThe Courage To Be Happy - Augusto Boal, Legislative Theatre, and The 7th International (1146376)Ashwini JayaramanNo ratings yet

- Biography of Abdul Hai HabibiDocument3 pagesBiography of Abdul Hai Habibisanakhan100% (1)

- Mano Marz Ul MautDocument12 pagesMano Marz Ul Mautdynamo vjNo ratings yet

- TFC Prospectus PDFDocument99 pagesTFC Prospectus PDFMehboobElaheiNo ratings yet

- Balane SheetDocument33 pagesBalane SheetOswinda GomesNo ratings yet

- Yogesh P Assignment PDFDocument2 pagesYogesh P Assignment PDFಯೋಗೇಶ್ ಪಿNo ratings yet

- Manila Fashions v. NLRCDocument5 pagesManila Fashions v. NLRCAlyssa MateoNo ratings yet

- TDS Byk-065 enDocument2 pagesTDS Byk-065 enrazamehdi3No ratings yet

- Revised Budget M Annual 2008Document390 pagesRevised Budget M Annual 2008FaisalNo ratings yet

- Chapter-1 The French Revolution: France During The Late 18 CenturyDocument33 pagesChapter-1 The French Revolution: France During The Late 18 CenturyNodiaNo ratings yet

- Citric Acid SDS11350 PDFDocument7 pagesCitric Acid SDS11350 PDFSyafiq Mohd NohNo ratings yet

- Compromise Agreement - AguinaldoDocument6 pagesCompromise Agreement - AguinaldoPatrice Noelle RamirezNo ratings yet

- Investigation On Instagram Android-Based Using Digital Forensics Research Workshop FrameworkDocument8 pagesInvestigation On Instagram Android-Based Using Digital Forensics Research Workshop FrameworkOnur KaraagacNo ratings yet

- Financial Accounting (International) : Fundamentals Pilot Paper - Knowledge ModuleDocument19 pagesFinancial Accounting (International) : Fundamentals Pilot Paper - Knowledge ModuleNguyen Thi Phuong ThuyNo ratings yet

- Deteksi Potensi Fraud Dengan Analisis Benford Law - APCI - HandoutDocument27 pagesDeteksi Potensi Fraud Dengan Analisis Benford Law - APCI - Handoutayassaras9No ratings yet

- Ervin Leon Edwards LawsuitDocument25 pagesErvin Leon Edwards Lawsuittom clearyNo ratings yet

- BWV45 - Es Ist Dir Gesagt, Mensch, Was Gut IstDocument54 pagesBWV45 - Es Ist Dir Gesagt, Mensch, Was Gut IstLegalSheetsNo ratings yet

- Mullahs On A BusDocument36 pagesMullahs On A BusAlphaaliy BabamuhalyNo ratings yet

- AD0-E551 Adobe Marketo Engage Business Practitioner ProfessionalDocument2 pagesAD0-E551 Adobe Marketo Engage Business Practitioner ProfessionalTushar Wagh0% (1)

- Panchayat BengalDocument5 pagesPanchayat Bengalapi-3711789No ratings yet

- English Sa11Document11 pagesEnglish Sa11Muhammadakbar Al AsgarNo ratings yet

- Accounting Fact SheetDocument1 pageAccounting Fact SheetSergio OlarteNo ratings yet

- 15-June-2020 Secretary-General Report On CAAC EngDocument38 pages15-June-2020 Secretary-General Report On CAAC EngsofiabloemNo ratings yet

Download as docx, pdf, or txt

You might also like

- Activity 8 JournalizingDocument6 pagesActivity 8 Journalizingdra_gon86% (14)

- Madelyn Rialubin Travel Agency Adjusting Entries AdjustedDocument5 pagesMadelyn Rialubin Travel Agency Adjusting Entries AdjustedJustine Almodiel100% (1)

- Quiz 1Document8 pagesQuiz 1Lyca Mae Cubangbang67% (3)

- Comprehensive Problem 23Document29 pagesComprehensive Problem 23Nicole Fidelson100% (2)

- Problem 15 - Group 5Document9 pagesProblem 15 - Group 5Francine TorresNo ratings yet

- Adjusting Entries Exercises - EditedDocument4 pagesAdjusting Entries Exercises - EditedCINDY LIAN CABILLON100% (2)

- Closing Entries (Step 7) & Post Closing Trial Balance (Step 8)Document1 pageClosing Entries (Step 7) & Post Closing Trial Balance (Step 8)Eunice Villacacan33% (3)

- Work Sheet Moises Dondoyano Information SystemDocument1 pageWork Sheet Moises Dondoyano Information SystemRJ DAVE DURUHA100% (5)

- ACT1101, PRB, Midterm, Wit Ans KeyDocument5 pagesACT1101, PRB, Midterm, Wit Ans KeyDyen100% (1)

- ASPL3 Activity 3-6 DoneDocument7 pagesASPL3 Activity 3-6 DoneConcepcion Family33% (3)

- Journal (Remedios Palaganas)Document2 pagesJournal (Remedios Palaganas)Mika CunananNo ratings yet

- Accounting ProblemsDocument3 pagesAccounting ProblemsKeitheia Quidlat67% (3)

- Problem 7 - Group 1Document8 pagesProblem 7 - Group 1Francine Torres100% (4)

- Illustrative Problem Worksheet ADocument6 pagesIllustrative Problem Worksheet AJoy Santos33% (3)

- Chapter 2 JournalizingDocument21 pagesChapter 2 Journalizingkakao100% (1)

- Problem-5 - AFCAR Chapter 3Document9 pagesProblem-5 - AFCAR Chapter 3kakao100% (1)

- Accounting HomeworkDocument6 pagesAccounting HomeworkGavin Ramos100% (2)

- Ebin Belderol TB and WorksheetDocument11 pagesEbin Belderol TB and WorksheetMarielle Ebin100% (3)

- Account Classification Normal Balance Income Statement / Balance Sheet ColumnDocument13 pagesAccount Classification Normal Balance Income Statement / Balance Sheet ColumnRhoda Claire M. Gansobin86% (7)

- Nerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Document3 pagesNerissa Mae L. Santos Activity On Completing The Accounting Cycle 1Mica Mae Correa100% (1)

- Exercises II - Adjusting TransactionsDocument2 pagesExercises II - Adjusting TransactionsJowjie TV80% (5)

- Laurent e Answer KeyDocument4 pagesLaurent e Answer KeyZee Santisas86% (7)

- Worksheet PalaganasDocument38 pagesWorksheet PalaganasMomo HiraiNo ratings yet

- MODULE-5 Ac 5 inDocument14 pagesMODULE-5 Ac 5 inBlesh Macusi75% (4)

- Requiring Lawyers To Submit Suspicious Transaction Reports PDFDocument13 pagesRequiring Lawyers To Submit Suspicious Transaction Reports PDFGeorge CarmonaNo ratings yet

- Deviations and Non Conformances SOP PDFDocument1 pageDeviations and Non Conformances SOP PDFAlinaNo ratings yet

- Adjusting Entries Christine Gamba CargoDocument5 pagesAdjusting Entries Christine Gamba Cargoelma wagwag100% (2)

- ACC111 Activity 22Document8 pagesACC111 Activity 22Triquesha Marriette Romero Rabi100% (1)

- ACTIVITY NO1and2Document5 pagesACTIVITY NO1and2Patricia Nicole Barrios100% (1)

- Rosalie Balhag CleanersDocument1 pageRosalie Balhag CleanersDominique Abrajano100% (1)

- Catherine Viesca Outdoor Ad Concepts Journal Entries January - December 2020Document4 pagesCatherine Viesca Outdoor Ad Concepts Journal Entries January - December 2020Jamycka Antolin100% (1)

- Travel Agency RubisomethingDocument12 pagesTravel Agency RubisomethingItsRenz YTNo ratings yet

- Pamantasan NG Lungsod NG Valenzuela: Financial Accounting and Reporting I (FAR I)Document5 pagesPamantasan NG Lungsod NG Valenzuela: Financial Accounting and Reporting I (FAR I)Mariane Manangan100% (2)

- AlisuagDocument5 pagesAlisuagAgatha Alcid100% (1)

- EDocument17 pagesEMark Cyphrysse Masiglat67% (3)

- Journal Entries: Edgar DetoyaDocument17 pagesJournal Entries: Edgar DetoyaAntonNo ratings yet

- Total: Adjusting EntriesDocument8 pagesTotal: Adjusting EntriesLj BesaNo ratings yet

- Dr. Nick Marasigan AccountsDocument11 pagesDr. Nick Marasigan AccountsNicole SarmientoNo ratings yet

- C3 - Problem 17 - Correcting A Trial BalanceDocument2 pagesC3 - Problem 17 - Correcting A Trial BalanceLorence John Imperial0% (1)

- Marichu Fornolles Novelties Transactions in December 2020: Date Particulars DebitDocument4 pagesMarichu Fornolles Novelties Transactions in December 2020: Date Particulars DebitHannah Pearl Flores Villar100% (1)

- Eva Cammayo Supply Company Journal Entry May 2021 Agnes Ramos Company Journal Entry May 2021Document7 pagesEva Cammayo Supply Company Journal Entry May 2021 Agnes Ramos Company Journal Entry May 2021Stephen ReloxNo ratings yet

- Accounting Problem 5Document8 pagesAccounting Problem 5Carlo AniNo ratings yet

- Noel Hungria, Adjusting EntriesDocument1 pageNoel Hungria, Adjusting EntriesFeiya Liu100% (2)

- Mads Rialubin Travel Agency WORKSHEET FS TRIAL BALANCEDocument3 pagesMads Rialubin Travel Agency WORKSHEET FS TRIAL BALANCEJowe Ringor Casignia100% (1)

- Exercise 3 Adjusting Entries - Service BusinessDocument2 pagesExercise 3 Adjusting Entries - Service BusinessMarc Viduya75% (4)

- Problem #3: Teresita Nacion Publishers Trial BalanceDocument4 pagesProblem #3: Teresita Nacion Publishers Trial BalanceRhea Sismo-anNo ratings yet

- Nelson Daganta CashDocument10 pagesNelson Daganta CashDan RioNo ratings yet

- Marasigan TransactionDocument20 pagesMarasigan TransactionE.D.J100% (2)

- Teresita Buenaflor ShoesDocument30 pagesTeresita Buenaflor ShoesHannah Pearl Flores Villar100% (1)

- John Bala Company Worksheet: Unadjusted Trial Balance DebitDocument9 pagesJohn Bala Company Worksheet: Unadjusted Trial Balance DebitJekoeNo ratings yet

- ACCA101 Leah May SantiagoDocument9 pagesACCA101 Leah May SantiagoNicole FidelsonNo ratings yet

- Teresita Buenaflor Shoes Worksheet 1 RegineDocument24 pagesTeresita Buenaflor Shoes Worksheet 1 RegineBaby Babe100% (1)

- Elegant Home Decors Worksheet For The Year Ended December 31,20ADocument8 pagesElegant Home Decors Worksheet For The Year Ended December 31,20AChloe CatalunaNo ratings yet

- Noel Hungria, Adjusting EntriesDocument1 pageNoel Hungria, Adjusting EntriesFeiya Liu100% (4)

- Jackielyn Magpantay Chart of AccountsDocument9 pagesJackielyn Magpantay Chart of AccountsIgnite NightNo ratings yet

- Acctgchap 2Document15 pagesAcctgchap 2Anjelika ViescaNo ratings yet

- Journalizing Posting and Preparing A Trial BalanceDocument38 pagesJournalizing Posting and Preparing A Trial BalanceJules Beltran100% (3)

- Acctg Assginment 4 Adjusting EntriesDocument3 pagesAcctg Assginment 4 Adjusting EntriesDaisy Marie A. RoselNo ratings yet

- N MarasiganDocument16 pagesN MarasiganMarikris Cadiente100% (1)

- Financial Statement Worksheet DetoyaDocument8 pagesFinancial Statement Worksheet Detoyasharon emailNo ratings yet

- Adjusting Entries For Bad DebtsDocument6 pagesAdjusting Entries For Bad DebtsKristine IvyNo ratings yet

- ACCTG1 PrefinalsDocument23 pagesACCTG1 PrefinalsJAN RAY CUISON VISPERAS100% (1)

- DDA 1 Niaga C Materials - 4th MeetingDocument32 pagesDDA 1 Niaga C Materials - 4th MeetingZenalina Hadi PutriNo ratings yet

- Explain The Purpose of DerivativesDocument5 pagesExplain The Purpose of DerivativesBlesh MacusiNo ratings yet

- Date Account Title and Explanation Debit Credit: Ref. NoDocument7 pagesDate Account Title and Explanation Debit Credit: Ref. NoBlesh MacusiNo ratings yet

- Name: Joana Marie Bueno Score: - Course/Section: BSA 1-2 Date Submitted: 1/17/2020Document12 pagesName: Joana Marie Bueno Score: - Course/Section: BSA 1-2 Date Submitted: 1/17/2020Blesh MacusiNo ratings yet

- Far Format Journal Posting Balance SheetDocument4 pagesFar Format Journal Posting Balance SheetBlesh MacusiNo ratings yet

- Dasmarinas Duplicators VDocument29 pagesDasmarinas Duplicators VBlesh MacusiNo ratings yet

- Mechyr1 Chapter 10::: Forces and MotionDocument31 pagesMechyr1 Chapter 10::: Forces and MotionAgrata PouloseNo ratings yet

- Compressed Gas Emergency Response Containment VesselsDocument4 pagesCompressed Gas Emergency Response Containment VesselsTzu Huan PengNo ratings yet

- NatwestDocument1 pageNatwestVinay SinghNo ratings yet

- Request For Copy of Tax ReturnDocument2 pagesRequest For Copy of Tax ReturnAsjsjsjsNo ratings yet

- Murder in Baldurs Gate Events SupplementDocument8 pagesMurder in Baldurs Gate Events SupplementDavid L Kriegel100% (3)

- The Courage To Be Happy - Augusto Boal, Legislative Theatre, and The 7th International (1146376)Document11 pagesThe Courage To Be Happy - Augusto Boal, Legislative Theatre, and The 7th International (1146376)Ashwini JayaramanNo ratings yet

- Biography of Abdul Hai HabibiDocument3 pagesBiography of Abdul Hai Habibisanakhan100% (1)

- Mano Marz Ul MautDocument12 pagesMano Marz Ul Mautdynamo vjNo ratings yet

- TFC Prospectus PDFDocument99 pagesTFC Prospectus PDFMehboobElaheiNo ratings yet

- Balane SheetDocument33 pagesBalane SheetOswinda GomesNo ratings yet

- Yogesh P Assignment PDFDocument2 pagesYogesh P Assignment PDFಯೋಗೇಶ್ ಪಿNo ratings yet

- Manila Fashions v. NLRCDocument5 pagesManila Fashions v. NLRCAlyssa MateoNo ratings yet

- TDS Byk-065 enDocument2 pagesTDS Byk-065 enrazamehdi3No ratings yet

- Revised Budget M Annual 2008Document390 pagesRevised Budget M Annual 2008FaisalNo ratings yet

- Chapter-1 The French Revolution: France During The Late 18 CenturyDocument33 pagesChapter-1 The French Revolution: France During The Late 18 CenturyNodiaNo ratings yet

- Citric Acid SDS11350 PDFDocument7 pagesCitric Acid SDS11350 PDFSyafiq Mohd NohNo ratings yet

- Compromise Agreement - AguinaldoDocument6 pagesCompromise Agreement - AguinaldoPatrice Noelle RamirezNo ratings yet

- Investigation On Instagram Android-Based Using Digital Forensics Research Workshop FrameworkDocument8 pagesInvestigation On Instagram Android-Based Using Digital Forensics Research Workshop FrameworkOnur KaraagacNo ratings yet

- Financial Accounting (International) : Fundamentals Pilot Paper - Knowledge ModuleDocument19 pagesFinancial Accounting (International) : Fundamentals Pilot Paper - Knowledge ModuleNguyen Thi Phuong ThuyNo ratings yet

- Deteksi Potensi Fraud Dengan Analisis Benford Law - APCI - HandoutDocument27 pagesDeteksi Potensi Fraud Dengan Analisis Benford Law - APCI - Handoutayassaras9No ratings yet

- Ervin Leon Edwards LawsuitDocument25 pagesErvin Leon Edwards Lawsuittom clearyNo ratings yet

- BWV45 - Es Ist Dir Gesagt, Mensch, Was Gut IstDocument54 pagesBWV45 - Es Ist Dir Gesagt, Mensch, Was Gut IstLegalSheetsNo ratings yet

- Mullahs On A BusDocument36 pagesMullahs On A BusAlphaaliy BabamuhalyNo ratings yet

- AD0-E551 Adobe Marketo Engage Business Practitioner ProfessionalDocument2 pagesAD0-E551 Adobe Marketo Engage Business Practitioner ProfessionalTushar Wagh0% (1)

- Panchayat BengalDocument5 pagesPanchayat Bengalapi-3711789No ratings yet

- English Sa11Document11 pagesEnglish Sa11Muhammadakbar Al AsgarNo ratings yet

- Accounting Fact SheetDocument1 pageAccounting Fact SheetSergio OlarteNo ratings yet

- 15-June-2020 Secretary-General Report On CAAC EngDocument38 pages15-June-2020 Secretary-General Report On CAAC EngsofiabloemNo ratings yet