SPS IIS Conference: Understanding The Link Between Active Share and Future Performance in Equity Portfolios

SPS IIS Conference: Understanding The Link Between Active Share and Future Performance in Equity Portfolios

You might also like

- Moodys - Sample Questions 3Document16 pagesMoodys - Sample Questions 3ivaNo ratings yet

- Hupseng CompletedDocument23 pagesHupseng CompletedHii Nian Tin80% (5)

- Toyota Maintanence Schedule PDFDocument10 pagesToyota Maintanence Schedule PDFcod22050% (2)

- 888 Fourth Lecture CoPDesignGuideDocument8 pages888 Fourth Lecture CoPDesignGuideKaiser KhanNo ratings yet

- Strategic Price NegotiationDocument9 pagesStrategic Price NegotiationMarket Dojo100% (3)

- Delhivery ReportDocument15 pagesDelhivery ReportUdit Narayan KosareNo ratings yet

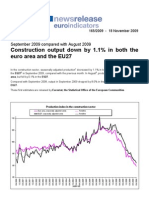

- Construction Output Up by 7.6% in Euro AreaDocument6 pagesConstruction Output Up by 7.6% in Euro AreamlubosNo ratings yet

- Industy Output EU November: - 1,1%Document6 pagesIndusty Output EU November: - 1,1%Frode HaukenesNo ratings yet

- Budget 2009-10: Preview: Expectations A Mirage or RealityDocument11 pagesBudget 2009-10: Preview: Expectations A Mirage or Realityapi-12317095No ratings yet

- Cement Strength Variability: What Can The Customer Expect and How Much Does It Affect Him?Document11 pagesCement Strength Variability: What Can The Customer Expect and How Much Does It Affect Him?musaNo ratings yet

- Sistema ElectricoDocument7 pagesSistema ElectricoJesus BombasNo ratings yet

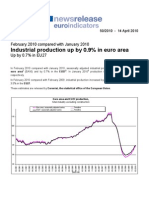

- Industrial Production Up by 0.9% in Euro AreaDocument6 pagesIndustrial Production Up by 0.9% in Euro AreaqtipxNo ratings yet

- EES Presentation Koch PDFDocument67 pagesEES Presentation Koch PDFVaibhav GhildiyalNo ratings yet

- GDP: Growth: Real GDP: Yoy: Select This Link and CLDocument6 pagesGDP: Growth: Real GDP: Yoy: Select This Link and CLadityaNo ratings yet

- Reza SiregarDocument35 pagesReza SiregarKhoirul AnwarNo ratings yet

- 01-04-08 ELECTRIC EQUIPMENT - MCF Global Parts PDFDocument6 pages01-04-08 ELECTRIC EQUIPMENT - MCF Global Parts PDFricardoNo ratings yet

- Fluid Mechanics: Chemical EngineeringDocument143 pagesFluid Mechanics: Chemical EngineeringYADAV VikasNo ratings yet

- The Future of Securitization: 5 Annual Credit Risk ConferenceDocument13 pagesThe Future of Securitization: 5 Annual Credit Risk Conferenceanon-121346No ratings yet

- 1Document3 pages1cafili7634No ratings yet

- Shi CL Asses: Mathematics Trend AnalysisDocument9 pagesShi CL Asses: Mathematics Trend Analysisvinayak kulkarni100% (1)

- Autozone: Case StudyDocument17 pagesAutozone: Case StudyPatcharanan SattayapongNo ratings yet

- Eport Gen Bio Q2Document11 pagesEport Gen Bio Q2Joshua BalmedinaNo ratings yet

- Galactic CompassDocument7 pagesGalactic CompassPedro WinnerNo ratings yet

- Priemysel EUDocument6 pagesPriemysel EUDennik SMENo ratings yet

- Base Metals Q2 2010 - OutlookDocument14 pagesBase Metals Q2 2010 - Outlookkoderi100% (1)

- Msci World Minimum Volatility IndexDocument2 pagesMsci World Minimum Volatility IndexsNo ratings yet

- MWN2020.000 en PDFDocument4 pagesMWN2020.000 en PDFadrianNo ratings yet

- ACSR 795KCMIL - Short Circuit WithstandDocument1 pageACSR 795KCMIL - Short Circuit WithstandsohaibazamNo ratings yet

- Practice U3O1 Part 2 # 2Document9 pagesPractice U3O1 Part 2 # 2lachykoumisNo ratings yet

- TP UAT DefectReport 140623Document288 pagesTP UAT DefectReport 140623Priya VNo ratings yet

- TP UAT DefectReport 150623Document313 pagesTP UAT DefectReport 150623Priya VNo ratings yet

- Final 1Document3 pagesFinal 1Taye YohannesNo ratings yet

- المقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern intellectual approach to marketing strategy 'with reference to resource and competencies theory'Document15 pagesالمقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern intellectual approach to marketing strategy 'with reference to resource and competencies theory'teNo ratings yet

- المقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern Intellectual Approach to Marketing Strategy 'With Reference to Resource and Competencies Theory'Document15 pagesالمقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern Intellectual Approach to Marketing Strategy 'With Reference to Resource and Competencies Theory'teNo ratings yet

- Social Sciences: A Comparison of Tablet-Based and Paper-Based Survey Data Collection in Conservation ProjectsDocument8 pagesSocial Sciences: A Comparison of Tablet-Based and Paper-Based Survey Data Collection in Conservation ProjectsAffan ElahiNo ratings yet

- TP UAT DefectReport 200623Document338 pagesTP UAT DefectReport 200623Priya VNo ratings yet

- TP UAT DefectReport 210623Document333 pagesTP UAT DefectReport 210623Priya VNo ratings yet

- Sample Quality Control Chart TemplateDocument8 pagesSample Quality Control Chart TemplatecervantessejNo ratings yet

- RE Workshop - Paper - Akram&ShaddadDocument21 pagesRE Workshop - Paper - Akram&Shaddadsafiya alaminNo ratings yet

- Materi TPB 1 - IntroductionDocument18 pagesMateri TPB 1 - IntroductionFadhilNo ratings yet

- Odisha SpeechDocument16 pagesOdisha SpeechHari SahooNo ratings yet

- Life Cycle Management Advant OCS and Master - HardwareDocument2 pagesLife Cycle Management Advant OCS and Master - HardwarekanbouchNo ratings yet

- 13 Chapter 5Document44 pages13 Chapter 5anju sureshNo ratings yet

- Ce Ulei Folosesc La Toyota Corolla VersoDocument4 pagesCe Ulei Folosesc La Toyota Corolla VersovladutuNo ratings yet

- Msci Us Broad Market Index (Usd) : Cumulative Index Performance - Net Returns Annual PerformanceDocument2 pagesMsci Us Broad Market Index (Usd) : Cumulative Index Performance - Net Returns Annual PerformancePrayogoNo ratings yet

- Nyse MS 2002Document28 pagesNyse MS 2002Gautam TandonNo ratings yet

- Hex WorldDocument117 pagesHex WorldCatastrioNo ratings yet

- National Travel Survey: 2010: Driving Licence Holding and Vehicle AvailabilityDocument4 pagesNational Travel Survey: 2010: Driving Licence Holding and Vehicle AvailabilitygirnetvaleriuNo ratings yet

- Pack 3 Books in 1 - Flash Cards Pictures and Words English French: 220 Learning Cards with first words to Learn French the easy wayFrom EverandPack 3 Books in 1 - Flash Cards Pictures and Words English French: 220 Learning Cards with first words to Learn French the easy wayNo ratings yet

- FOXBORO IA - Series - Lifecycle - Product - Phase - ListingDocument26 pagesFOXBORO IA - Series - Lifecycle - Product - Phase - Listingtricucha priyantoNo ratings yet

- Methode Install Roof Yane672Document2 pagesMethode Install Roof Yane672ardhikiraNo ratings yet

- Bangladesh - Still Resilient: - On The GroundDocument6 pagesBangladesh - Still Resilient: - On The GroundanmolshardaNo ratings yet

- Age Matters in ShippingDocument15 pagesAge Matters in ShippingmekulaNo ratings yet

- 5 Ascarya Rev FinDocument15 pages5 Ascarya Rev FinSisca WiryawanNo ratings yet

- United States Patent: Malik Et AlDocument13 pagesUnited States Patent: Malik Et Alkat78904No ratings yet

- DF-601 Parts ManDocument30 pagesDF-601 Parts ManKaren SantacruzNo ratings yet

- Analyse The Relationship Between Government Spending and Investment Spending For The US Economy in The Past 20 YearsDocument7 pagesAnalyse The Relationship Between Government Spending and Investment Spending For The US Economy in The Past 20 YearsNeil VictorNo ratings yet

- Pack 3 Books in 1 - Flash Cards Pictures and Words English Spanish: 200 Cards - Spanish vocabulary learning flash cards with pictures for beginnersFrom EverandPack 3 Books in 1 - Flash Cards Pictures and Words English Spanish: 200 Cards - Spanish vocabulary learning flash cards with pictures for beginnersNo ratings yet

- Penanda Hardskill N Core Abilities 2018Document1 pagePenanda Hardskill N Core Abilities 2018Hanif HazirinNo ratings yet

- DummyApp GanttDocument1 pageDummyApp Gantt21bcm002No ratings yet

- Case Study - LÓrealDocument4 pagesCase Study - LÓrealAndrea BrozosNo ratings yet

- Dividend DecisionsDocument36 pagesDividend DecisionsMohammed ZakriyaNo ratings yet

- Pack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersFrom EverandPack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersNo ratings yet

- A_moral_house_divided_How_idealized_family_models_Document31 pagesA_moral_house_divided_How_idealized_family_models_lchristoffNo ratings yet

- Securitisation, Shadow Banking and The Value of Financial InnovationDocument35 pagesSecuritisation, Shadow Banking and The Value of Financial InnovationlchristoffNo ratings yet

- 2 Eiopa 20 500 Pepp Draft RtssDocument36 pages2 Eiopa 20 500 Pepp Draft RtsslchristoffNo ratings yet

- SSRN Id3209429Document15 pagesSSRN Id3209429lchristoffNo ratings yet

- From Money To Data: Book ReviewsDocument1 pageFrom Money To Data: Book ReviewslchristoffNo ratings yet

- Te Connectivity 2012 Annual ReportDocument177 pagesTe Connectivity 2012 Annual ReportNguyễn Trọng VinhNo ratings yet

- Chapter 18 - Bonds - Analysis and StrategyDocument11 pagesChapter 18 - Bonds - Analysis and Strategyumer1650% (1)

- Administrative Coordinator Secours IslamiqueDocument11 pagesAdministrative Coordinator Secours IslamiqueAnonymous hEH9lqENo ratings yet

- IPA Institute Webinar 7 Deadly Sins Industrial MegaprojectsDocument31 pagesIPA Institute Webinar 7 Deadly Sins Industrial MegaprojectsXuxu Too100% (1)

- Introduction To Business 16 BUS101: Chapter 21: Accounting FundamentalsDocument11 pagesIntroduction To Business 16 BUS101: Chapter 21: Accounting Fundamentalsnahidul202No ratings yet

- Balochistan Glass LimitedDocument9 pagesBalochistan Glass Limitedarifking29No ratings yet

- Case Study - So What Is It WorthDocument7 pagesCase Study - So What Is It WorthJohn Aldridge Chew100% (1)

- Mob I ReportDocument50 pagesMob I ReportYasmin AruniNo ratings yet

- BAII Plus Professional TutorialDocument22 pagesBAII Plus Professional TutorialOladipupo Mayowa PaulNo ratings yet

- SAP Share Matching Plan India Guide To Taxation: Acquisition and Transfer of SharesDocument2 pagesSAP Share Matching Plan India Guide To Taxation: Acquisition and Transfer of SharesAbhijeet KumarNo ratings yet

- Singapore Stock PulseDocument12 pagesSingapore Stock Pulsemngb6499No ratings yet

- Pas 16 Property, Plant and EquipmentDocument2 pagesPas 16 Property, Plant and Equipmentamber_harthartNo ratings yet

- Difference Between IPO and Secondary OfferingDocument2 pagesDifference Between IPO and Secondary OfferingUsman Khan100% (1)

- Reliance Industries LTD.: Assignment 2Document27 pagesReliance Industries LTD.: Assignment 2Vishal RajNo ratings yet

- Excel Cash Book Extra RowsDocument28 pagesExcel Cash Book Extra RowsppjobNo ratings yet

- Alankit Assignments LTD.: Project Report ONDocument84 pagesAlankit Assignments LTD.: Project Report ONmannuNo ratings yet

- Investment Options Through Hedge FundDocument17 pagesInvestment Options Through Hedge FundMahesh KempegowdaNo ratings yet

- DailySocial Indonesia S Tech Startup Report 2016 PDFDocument75 pagesDailySocial Indonesia S Tech Startup Report 2016 PDFwaladNo ratings yet

- MCQ For ManagementDocument2 pagesMCQ For ManagementPhaul Quicktrack100% (1)

- STR 581 Capstone Final Exam Part Two Latest Question AnswersDocument12 pagesSTR 581 Capstone Final Exam Part Two Latest Question AnswersaarenaddisonNo ratings yet

- Inter Brand Valuation Method - by Freddy GuevaraDocument10 pagesInter Brand Valuation Method - by Freddy GuevaraRohith GirishNo ratings yet

- CH - 17 - 11e Keown & TitmanTKM - Financial Forecasting Planning & Budgeting L-6Document47 pagesCH - 17 - 11e Keown & TitmanTKM - Financial Forecasting Planning & Budgeting L-6Adeel RanaNo ratings yet

- Sample MBA Admissions EssaysDocument4 pagesSample MBA Admissions EssayshelvadjianNo ratings yet

- Form For Registratio of Subscribers CS S1Document9 pagesForm For Registratio of Subscribers CS S1sanjeetvermaNo ratings yet

- Yg EntertainmentDocument3 pagesYg EntertainmentNura Syazana Diyana HalmiNo ratings yet

- Ccris BNM BookletDocument11 pagesCcris BNM BookletMuhamad AzmirNo ratings yet

Download as pdf or txt

You might also like

- Moodys - Sample Questions 3Document16 pagesMoodys - Sample Questions 3ivaNo ratings yet

- Hupseng CompletedDocument23 pagesHupseng CompletedHii Nian Tin80% (5)

- Toyota Maintanence Schedule PDFDocument10 pagesToyota Maintanence Schedule PDFcod22050% (2)

- 888 Fourth Lecture CoPDesignGuideDocument8 pages888 Fourth Lecture CoPDesignGuideKaiser KhanNo ratings yet

- Strategic Price NegotiationDocument9 pagesStrategic Price NegotiationMarket Dojo100% (3)

- Delhivery ReportDocument15 pagesDelhivery ReportUdit Narayan KosareNo ratings yet

- Construction Output Up by 7.6% in Euro AreaDocument6 pagesConstruction Output Up by 7.6% in Euro AreamlubosNo ratings yet

- Industy Output EU November: - 1,1%Document6 pagesIndusty Output EU November: - 1,1%Frode HaukenesNo ratings yet

- Budget 2009-10: Preview: Expectations A Mirage or RealityDocument11 pagesBudget 2009-10: Preview: Expectations A Mirage or Realityapi-12317095No ratings yet

- Cement Strength Variability: What Can The Customer Expect and How Much Does It Affect Him?Document11 pagesCement Strength Variability: What Can The Customer Expect and How Much Does It Affect Him?musaNo ratings yet

- Sistema ElectricoDocument7 pagesSistema ElectricoJesus BombasNo ratings yet

- Industrial Production Up by 0.9% in Euro AreaDocument6 pagesIndustrial Production Up by 0.9% in Euro AreaqtipxNo ratings yet

- EES Presentation Koch PDFDocument67 pagesEES Presentation Koch PDFVaibhav GhildiyalNo ratings yet

- GDP: Growth: Real GDP: Yoy: Select This Link and CLDocument6 pagesGDP: Growth: Real GDP: Yoy: Select This Link and CLadityaNo ratings yet

- Reza SiregarDocument35 pagesReza SiregarKhoirul AnwarNo ratings yet

- 01-04-08 ELECTRIC EQUIPMENT - MCF Global Parts PDFDocument6 pages01-04-08 ELECTRIC EQUIPMENT - MCF Global Parts PDFricardoNo ratings yet

- Fluid Mechanics: Chemical EngineeringDocument143 pagesFluid Mechanics: Chemical EngineeringYADAV VikasNo ratings yet

- The Future of Securitization: 5 Annual Credit Risk ConferenceDocument13 pagesThe Future of Securitization: 5 Annual Credit Risk Conferenceanon-121346No ratings yet

- 1Document3 pages1cafili7634No ratings yet

- Shi CL Asses: Mathematics Trend AnalysisDocument9 pagesShi CL Asses: Mathematics Trend Analysisvinayak kulkarni100% (1)

- Autozone: Case StudyDocument17 pagesAutozone: Case StudyPatcharanan SattayapongNo ratings yet

- Eport Gen Bio Q2Document11 pagesEport Gen Bio Q2Joshua BalmedinaNo ratings yet

- Galactic CompassDocument7 pagesGalactic CompassPedro WinnerNo ratings yet

- Priemysel EUDocument6 pagesPriemysel EUDennik SMENo ratings yet

- Base Metals Q2 2010 - OutlookDocument14 pagesBase Metals Q2 2010 - Outlookkoderi100% (1)

- Msci World Minimum Volatility IndexDocument2 pagesMsci World Minimum Volatility IndexsNo ratings yet

- MWN2020.000 en PDFDocument4 pagesMWN2020.000 en PDFadrianNo ratings yet

- ACSR 795KCMIL - Short Circuit WithstandDocument1 pageACSR 795KCMIL - Short Circuit WithstandsohaibazamNo ratings yet

- Practice U3O1 Part 2 # 2Document9 pagesPractice U3O1 Part 2 # 2lachykoumisNo ratings yet

- TP UAT DefectReport 140623Document288 pagesTP UAT DefectReport 140623Priya VNo ratings yet

- TP UAT DefectReport 150623Document313 pagesTP UAT DefectReport 150623Priya VNo ratings yet

- Final 1Document3 pagesFinal 1Taye YohannesNo ratings yet

- المقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern intellectual approach to marketing strategy 'with reference to resource and competencies theory'Document15 pagesالمقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern intellectual approach to marketing strategy 'with reference to resource and competencies theory'teNo ratings yet

- المقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern Intellectual Approach to Marketing Strategy 'With Reference to Resource and Competencies Theory'Document15 pagesالمقاربة الفكرية الحديثة للإستراتيجية التسويقية 'مع الاشارة إلى نظرية الموارد والكفاءات' Modern Intellectual Approach to Marketing Strategy 'With Reference to Resource and Competencies Theory'teNo ratings yet

- Social Sciences: A Comparison of Tablet-Based and Paper-Based Survey Data Collection in Conservation ProjectsDocument8 pagesSocial Sciences: A Comparison of Tablet-Based and Paper-Based Survey Data Collection in Conservation ProjectsAffan ElahiNo ratings yet

- TP UAT DefectReport 200623Document338 pagesTP UAT DefectReport 200623Priya VNo ratings yet

- TP UAT DefectReport 210623Document333 pagesTP UAT DefectReport 210623Priya VNo ratings yet

- Sample Quality Control Chart TemplateDocument8 pagesSample Quality Control Chart TemplatecervantessejNo ratings yet

- RE Workshop - Paper - Akram&ShaddadDocument21 pagesRE Workshop - Paper - Akram&Shaddadsafiya alaminNo ratings yet

- Materi TPB 1 - IntroductionDocument18 pagesMateri TPB 1 - IntroductionFadhilNo ratings yet

- Odisha SpeechDocument16 pagesOdisha SpeechHari SahooNo ratings yet

- Life Cycle Management Advant OCS and Master - HardwareDocument2 pagesLife Cycle Management Advant OCS and Master - HardwarekanbouchNo ratings yet

- 13 Chapter 5Document44 pages13 Chapter 5anju sureshNo ratings yet

- Ce Ulei Folosesc La Toyota Corolla VersoDocument4 pagesCe Ulei Folosesc La Toyota Corolla VersovladutuNo ratings yet

- Msci Us Broad Market Index (Usd) : Cumulative Index Performance - Net Returns Annual PerformanceDocument2 pagesMsci Us Broad Market Index (Usd) : Cumulative Index Performance - Net Returns Annual PerformancePrayogoNo ratings yet

- Nyse MS 2002Document28 pagesNyse MS 2002Gautam TandonNo ratings yet

- Hex WorldDocument117 pagesHex WorldCatastrioNo ratings yet

- National Travel Survey: 2010: Driving Licence Holding and Vehicle AvailabilityDocument4 pagesNational Travel Survey: 2010: Driving Licence Holding and Vehicle AvailabilitygirnetvaleriuNo ratings yet

- Pack 3 Books in 1 - Flash Cards Pictures and Words English French: 220 Learning Cards with first words to Learn French the easy wayFrom EverandPack 3 Books in 1 - Flash Cards Pictures and Words English French: 220 Learning Cards with first words to Learn French the easy wayNo ratings yet

- FOXBORO IA - Series - Lifecycle - Product - Phase - ListingDocument26 pagesFOXBORO IA - Series - Lifecycle - Product - Phase - Listingtricucha priyantoNo ratings yet

- Methode Install Roof Yane672Document2 pagesMethode Install Roof Yane672ardhikiraNo ratings yet

- Bangladesh - Still Resilient: - On The GroundDocument6 pagesBangladesh - Still Resilient: - On The GroundanmolshardaNo ratings yet

- Age Matters in ShippingDocument15 pagesAge Matters in ShippingmekulaNo ratings yet

- 5 Ascarya Rev FinDocument15 pages5 Ascarya Rev FinSisca WiryawanNo ratings yet

- United States Patent: Malik Et AlDocument13 pagesUnited States Patent: Malik Et Alkat78904No ratings yet

- DF-601 Parts ManDocument30 pagesDF-601 Parts ManKaren SantacruzNo ratings yet

- Analyse The Relationship Between Government Spending and Investment Spending For The US Economy in The Past 20 YearsDocument7 pagesAnalyse The Relationship Between Government Spending and Investment Spending For The US Economy in The Past 20 YearsNeil VictorNo ratings yet

- Pack 3 Books in 1 - Flash Cards Pictures and Words English Spanish: 200 Cards - Spanish vocabulary learning flash cards with pictures for beginnersFrom EverandPack 3 Books in 1 - Flash Cards Pictures and Words English Spanish: 200 Cards - Spanish vocabulary learning flash cards with pictures for beginnersNo ratings yet

- Penanda Hardskill N Core Abilities 2018Document1 pagePenanda Hardskill N Core Abilities 2018Hanif HazirinNo ratings yet

- DummyApp GanttDocument1 pageDummyApp Gantt21bcm002No ratings yet

- Case Study - LÓrealDocument4 pagesCase Study - LÓrealAndrea BrozosNo ratings yet

- Dividend DecisionsDocument36 pagesDividend DecisionsMohammed ZakriyaNo ratings yet

- Pack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersFrom EverandPack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersNo ratings yet

- A_moral_house_divided_How_idealized_family_models_Document31 pagesA_moral_house_divided_How_idealized_family_models_lchristoffNo ratings yet

- Securitisation, Shadow Banking and The Value of Financial InnovationDocument35 pagesSecuritisation, Shadow Banking and The Value of Financial InnovationlchristoffNo ratings yet

- 2 Eiopa 20 500 Pepp Draft RtssDocument36 pages2 Eiopa 20 500 Pepp Draft RtsslchristoffNo ratings yet

- SSRN Id3209429Document15 pagesSSRN Id3209429lchristoffNo ratings yet

- From Money To Data: Book ReviewsDocument1 pageFrom Money To Data: Book ReviewslchristoffNo ratings yet

- Te Connectivity 2012 Annual ReportDocument177 pagesTe Connectivity 2012 Annual ReportNguyễn Trọng VinhNo ratings yet

- Chapter 18 - Bonds - Analysis and StrategyDocument11 pagesChapter 18 - Bonds - Analysis and Strategyumer1650% (1)

- Administrative Coordinator Secours IslamiqueDocument11 pagesAdministrative Coordinator Secours IslamiqueAnonymous hEH9lqENo ratings yet

- IPA Institute Webinar 7 Deadly Sins Industrial MegaprojectsDocument31 pagesIPA Institute Webinar 7 Deadly Sins Industrial MegaprojectsXuxu Too100% (1)

- Introduction To Business 16 BUS101: Chapter 21: Accounting FundamentalsDocument11 pagesIntroduction To Business 16 BUS101: Chapter 21: Accounting Fundamentalsnahidul202No ratings yet

- Balochistan Glass LimitedDocument9 pagesBalochistan Glass Limitedarifking29No ratings yet

- Case Study - So What Is It WorthDocument7 pagesCase Study - So What Is It WorthJohn Aldridge Chew100% (1)

- Mob I ReportDocument50 pagesMob I ReportYasmin AruniNo ratings yet

- BAII Plus Professional TutorialDocument22 pagesBAII Plus Professional TutorialOladipupo Mayowa PaulNo ratings yet

- SAP Share Matching Plan India Guide To Taxation: Acquisition and Transfer of SharesDocument2 pagesSAP Share Matching Plan India Guide To Taxation: Acquisition and Transfer of SharesAbhijeet KumarNo ratings yet

- Singapore Stock PulseDocument12 pagesSingapore Stock Pulsemngb6499No ratings yet

- Pas 16 Property, Plant and EquipmentDocument2 pagesPas 16 Property, Plant and Equipmentamber_harthartNo ratings yet

- Difference Between IPO and Secondary OfferingDocument2 pagesDifference Between IPO and Secondary OfferingUsman Khan100% (1)

- Reliance Industries LTD.: Assignment 2Document27 pagesReliance Industries LTD.: Assignment 2Vishal RajNo ratings yet

- Excel Cash Book Extra RowsDocument28 pagesExcel Cash Book Extra RowsppjobNo ratings yet

- Alankit Assignments LTD.: Project Report ONDocument84 pagesAlankit Assignments LTD.: Project Report ONmannuNo ratings yet

- Investment Options Through Hedge FundDocument17 pagesInvestment Options Through Hedge FundMahesh KempegowdaNo ratings yet

- DailySocial Indonesia S Tech Startup Report 2016 PDFDocument75 pagesDailySocial Indonesia S Tech Startup Report 2016 PDFwaladNo ratings yet

- MCQ For ManagementDocument2 pagesMCQ For ManagementPhaul Quicktrack100% (1)

- STR 581 Capstone Final Exam Part Two Latest Question AnswersDocument12 pagesSTR 581 Capstone Final Exam Part Two Latest Question AnswersaarenaddisonNo ratings yet

- Inter Brand Valuation Method - by Freddy GuevaraDocument10 pagesInter Brand Valuation Method - by Freddy GuevaraRohith GirishNo ratings yet

- CH - 17 - 11e Keown & TitmanTKM - Financial Forecasting Planning & Budgeting L-6Document47 pagesCH - 17 - 11e Keown & TitmanTKM - Financial Forecasting Planning & Budgeting L-6Adeel RanaNo ratings yet

- Sample MBA Admissions EssaysDocument4 pagesSample MBA Admissions EssayshelvadjianNo ratings yet

- Form For Registratio of Subscribers CS S1Document9 pagesForm For Registratio of Subscribers CS S1sanjeetvermaNo ratings yet

- Yg EntertainmentDocument3 pagesYg EntertainmentNura Syazana Diyana HalmiNo ratings yet

- Ccris BNM BookletDocument11 pagesCcris BNM BookletMuhamad AzmirNo ratings yet