Download as pdf or txt

You might also like

- Chapter 4 Exempt SalesDocument23 pagesChapter 4 Exempt SalesHazel Jane Esclamada0% (2)

- Chapter 1 Succession and Transfer Taxes Part 1Document2 pagesChapter 1 Succession and Transfer Taxes Part 1AngieNo ratings yet

- Practice Exercises: Donor'S TaxDocument37 pagesPractice Exercises: Donor'S TaxErica NicolasuraNo ratings yet

- Reviewer Chapter 2Document6 pagesReviewer Chapter 2Ken NavarroNo ratings yet

- Course Financial Management Developer and Their Background: See Assignment / Agreement SectionDocument33 pagesCourse Financial Management Developer and Their Background: See Assignment / Agreement SectionHazel Jane Esclamada100% (1)

- Estate Tax PayableDocument8 pagesEstate Tax PayableHazel Jane Esclamada100% (2)

- Chapter 17 Donor's TaxDocument7 pagesChapter 17 Donor's TaxHazel Jane Esclamada100% (3)

- Chapter 10 Vat Still DueDocument7 pagesChapter 10 Vat Still DueHazel Jane EsclamadaNo ratings yet

- Chapter 9 Input VatDocument10 pagesChapter 9 Input VatHazel Jane EsclamadaNo ratings yet

- Chapter 3 Introduction To Business TaxationDocument27 pagesChapter 3 Introduction To Business TaxationHazel Jane Esclamada100% (1)

- 1caltex Vs Palomar Case DigestDocument3 pages1caltex Vs Palomar Case DigestJunjun50% (2)

- Hindu Succession-Male & FemaleDocument14 pagesHindu Succession-Male & FemaleKumar MangalamNo ratings yet

- FIT All ERC ResolutionNo 18seriesof2014 REPA RESA TemplateDocument26 pagesFIT All ERC ResolutionNo 18seriesof2014 REPA RESA TemplateNikki BalaneNo ratings yet

- Ch10 Donor's TaxDocument9 pagesCh10 Donor's TaxRenelyn FiloteoNo ratings yet

- Toaz - Info Chapter 10 Compensation Income True or False 1 PRDocument22 pagesToaz - Info Chapter 10 Compensation Income True or False 1 PRErna DavidNo ratings yet

- Chapter 10 Tabag - Serrano NotesDocument5 pagesChapter 10 Tabag - Serrano NotesNatalie SerranoNo ratings yet

- Chap. 6 8Document44 pagesChap. 6 82vpsrsmg7jNo ratings yet

- Operating Segment: Intermediate Accounting 3Document51 pagesOperating Segment: Intermediate Accounting 3Trisha Mae AlburoNo ratings yet

- Donor S Tax Exam AnswersDocument6 pagesDonor S Tax Exam AnswersAngela Miles DizonNo ratings yet

- Chapter 6 Deductions From The Gross Estate PDFDocument7 pagesChapter 6 Deductions From The Gross Estate PDFDudz MatienzoNo ratings yet

- Statement of Changes in EquityDocument8 pagesStatement of Changes in EquityGonzalo Jr. RualesNo ratings yet

- Business Tax Chapter 8 ReviewerDocument5 pagesBusiness Tax Chapter 8 ReviewerMurien LimNo ratings yet

- Business Tax ReviewerDocument22 pagesBusiness Tax ReviewereysiNo ratings yet

- TAX Code - Section 109Document3 pagesTAX Code - Section 109Ranin, Manilac Melissa SNo ratings yet

- Intro To Regular Income TaxationDocument2 pagesIntro To Regular Income TaxationhotgirlsummerNo ratings yet

- Exclusions and Inclusions - MANTUANODocument8 pagesExclusions and Inclusions - MANTUANODonita MantuanoNo ratings yet

- Ch06 Introduction To Transfer TaxesDocument9 pagesCh06 Introduction To Transfer TaxesRenelyn FiloteoNo ratings yet

- Taxa2 Quiz3Document14 pagesTaxa2 Quiz3ishinoya keishiNo ratings yet

- Dealings in Property: Lesson 12Document18 pagesDealings in Property: Lesson 12lcNo ratings yet

- Income Tax Banggawan Ch11 CompressDocument10 pagesIncome Tax Banggawan Ch11 CompressRhian BarzanaNo ratings yet

- Transfer and Business Tax 2014 Ballada PDFDocument26 pagesTransfer and Business Tax 2014 Ballada PDFCamzwell Kleinne HalyieNo ratings yet

- Concept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Document12 pagesConcept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Hazel Jane Esclamada100% (1)

- MixDocument32 pagesMixUnnecessary BuyingNo ratings yet

- Draft PH Order On Establishment of Customs Facilities and WarehousesDocument22 pagesDraft PH Order On Establishment of Customs Facilities and WarehousesPortCallsNo ratings yet

- Melanie S. Samsona Business Tax Chapter 7 ExercisesDocument3 pagesMelanie S. Samsona Business Tax Chapter 7 ExercisesMelanie SamsonaNo ratings yet

- Chapter 6 - Introduction To The Value Added TaxDocument8 pagesChapter 6 - Introduction To The Value Added TaxJamaica DavidNo ratings yet

- Chapter 1 Introduction To Business Taxes PDFDocument6 pagesChapter 1 Introduction To Business Taxes PDFDudz Matienzo100% (1)

- Chapter 1 Tax 2Document5 pagesChapter 1 Tax 2Hazel Jane EsclamadaNo ratings yet

- Output TaxDocument15 pagesOutput TaxAmie Jane MirandaNo ratings yet

- Quiz On VAT154623Document5 pagesQuiz On VAT154623Sandy100% (1)

- 7.3 Answer Key Chapter 6 Banggawan 1 PDFDocument4 pages7.3 Answer Key Chapter 6 Banggawan 1 PDFLuca PacioliNo ratings yet

- Rice Company Was Incorporated On January 1Document6 pagesRice Company Was Incorporated On January 1Marjorie PalmaNo ratings yet

- Tax 2 Part 3 Estate TaxDocument25 pagesTax 2 Part 3 Estate TaxShane TorrieNo ratings yet

- May 15 Input VATDocument15 pagesMay 15 Input VATA cNo ratings yet

- Chapter Five: Estate Tax - Gross EstateDocument9 pagesChapter Five: Estate Tax - Gross EstateKai KimNo ratings yet

- Chapter 7: Business Taxes: ProblemsDocument8 pagesChapter 7: Business Taxes: ProblemsAva DoveNo ratings yet

- AssesmentDocument12 pagesAssesmentMaya Keizel A.No ratings yet

- Chapter 9 Other Percentage TaxesDocument56 pagesChapter 9 Other Percentage TaxesKarylle BartolayNo ratings yet

- PDF ch9 Estate Tax - CompressDocument40 pagesPDF ch9 Estate Tax - CompressMary DenizeNo ratings yet

- EffectofObligations PDFDocument0 pagesEffectofObligations PDFÄnne Ü KimberlieNo ratings yet

- Chapter 1: Introduction To Accounting (FAR By: Millan)Document91 pagesChapter 1: Introduction To Accounting (FAR By: Millan)Lovely LimNo ratings yet

- Chapter Four: Introduction To Transfer TaxesDocument9 pagesChapter Four: Introduction To Transfer TaxesKai KimNo ratings yet

- Computaion Pre FinalDocument4 pagesComputaion Pre FinalPaupauNo ratings yet

- Chapter 6 Capital Gains TaxationDocument34 pagesChapter 6 Capital Gains TaxationJason Mables100% (1)

- Tax Term Quiz TheoriesDocument6 pagesTax Term Quiz TheoriesRena Jocelle NalzaroNo ratings yet

- Julia Mae D.S San Juan ACC C301 - 301T Quiz 1 - SolutionDocument3 pagesJulia Mae D.S San Juan ACC C301 - 301T Quiz 1 - SolutionLeona San JuanNo ratings yet

- Estate TaxDocument48 pagesEstate TaxBhosx Kim100% (1)

- LECTURE 10 Dealings in PropertiesDocument33 pagesLECTURE 10 Dealings in PropertiesJeane Mae Boo100% (1)

- Section 1: Payment or PerformanceDocument11 pagesSection 1: Payment or PerformanceNBI ILOCOS REGIONAL OFFICENo ratings yet

- Strategic Tax Management - Week 5Document37 pagesStrategic Tax Management - Week 5Arman DalisayNo ratings yet

- Taxation of IndividualsDocument49 pagesTaxation of IndividualsAnastasha Grey100% (1)

- TAX-301 (VAT-Subject Transactions)Document10 pagesTAX-301 (VAT-Subject Transactions)Edith DalidaNo ratings yet

- Chapter 6 Banggawan RevierwerDocument9 pagesChapter 6 Banggawan RevierwerKyleZapantaNo ratings yet

- Income Tax - Corporations Sample Problems: SolutionsDocument12 pagesIncome Tax - Corporations Sample Problems: SolutionsYellow BelleNo ratings yet

- Chapter 5 Final Income TaxationDocument2 pagesChapter 5 Final Income TaxationBisag AsaNo ratings yet

- Lim Tax 5 Quiz AnswerDocument4 pagesLim Tax 5 Quiz AnswerIvan AnaboNo ratings yet

- Introduction To Transfer Taxation: Pamantasan NG Lungsod NG MuntinlupaDocument23 pagesIntroduction To Transfer Taxation: Pamantasan NG Lungsod NG MuntinlupaRizza Omalin100% (1)

- Tax Reviewer 3 TRANSFER TAXDocument6 pagesTax Reviewer 3 TRANSFER TAXAlliahDataNo ratings yet

- Lecture For Module 1 AutosavedDocument15 pagesLecture For Module 1 AutosavedRoselene LansonNo ratings yet

- Tax SemisDocument50 pagesTax SemisTeam MindanaoNo ratings yet

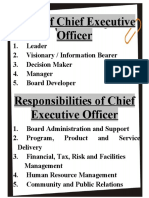

- Report - Roles of CEODocument2 pagesReport - Roles of CEOHazel Jane EsclamadaNo ratings yet

- Introduction To Financial ManagementDocument43 pagesIntroduction To Financial ManagementHazel Jane EsclamadaNo ratings yet

- Photography 3 (Updated)Document28 pagesPhotography 3 (Updated)Hazel Jane EsclamadaNo ratings yet

- Mas 3 Module 1 Fs AnalysisDocument19 pagesMas 3 Module 1 Fs AnalysisHazel Jane EsclamadaNo ratings yet

- Introduction To Donor's TaxDocument7 pagesIntroduction To Donor's TaxHazel Jane EsclamadaNo ratings yet

- MAS-3-Roque - Answer KeyDocument6 pagesMAS-3-Roque - Answer KeyHazel Jane Esclamada100% (1)

- Photography 2Document48 pagesPhotography 2Hazel Jane EsclamadaNo ratings yet

- Topic 4 - EXERCISES6 - Capital Current Liabilities ManagementDocument36 pagesTopic 4 - EXERCISES6 - Capital Current Liabilities ManagementHazel Jane Esclamada100% (1)

- Warranties, Provisions and Contingent LiabilitiesDocument31 pagesWarranties, Provisions and Contingent LiabilitiesHazel Jane EsclamadaNo ratings yet

- What To Do With Perceived Environmental ViolationsDocument15 pagesWhat To Do With Perceived Environmental ViolationsHazel Jane EsclamadaNo ratings yet

- Working Capital FinanceDocument12 pagesWorking Capital FinanceYeoh Mae100% (4)

- Inventory Management: Multiple Choice QuestionsDocument3 pagesInventory Management: Multiple Choice QuestionsHazel Jane Esclamada33% (3)

- MODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Document19 pagesMODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Hazel Jane Esclamada0% (1)

- Topic 3 & 4 - EXERCISES3 - Working Capital Management - TheoriesDocument36 pagesTopic 3 & 4 - EXERCISES3 - Working Capital Management - TheoriesHazel Jane EsclamadaNo ratings yet

- Module Far1 Unit-1 Part-1bDocument5 pagesModule Far1 Unit-1 Part-1bHazel Jane EsclamadaNo ratings yet

- Reclassification: of Financial AssetsDocument15 pagesReclassification: of Financial AssetsHazel Jane EsclamadaNo ratings yet

- Concept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Document12 pagesConcept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Hazel Jane Esclamada100% (1)

- Chapter 1 Tax 2Document5 pagesChapter 1 Tax 2Hazel Jane EsclamadaNo ratings yet

- Module Far1 Unit-1 Part-1c.1Document6 pagesModule Far1 Unit-1 Part-1c.1Hazel Jane EsclamadaNo ratings yet

- Module 2.1 (Property, Plant, and Equipment)Document15 pagesModule 2.1 (Property, Plant, and Equipment)Hazel Jane EsclamadaNo ratings yet

- Topic 4 - Current Liabilities Sample ProblemsDocument8 pagesTopic 4 - Current Liabilities Sample ProblemsHazel Jane EsclamadaNo ratings yet

- Topic 7 Transfer PricingDocument3 pagesTopic 7 Transfer PricingHazel Jane EsclamadaNo ratings yet

- TSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPDocument3 pagesTSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPHazel Jane EsclamadaNo ratings yet

- Walters V Lunt and Another - (1951) 2 All ERDocument3 pagesWalters V Lunt and Another - (1951) 2 All ERSiti Noor Balqis100% (1)

- Directed Energy Weapons (DEW) - Are You A Target of These New WeaponsDocument3 pagesDirected Energy Weapons (DEW) - Are You A Target of These New WeaponsKarl-Heinz-LietzNo ratings yet

- Course Outline-Constitutional History of India (2022)Document14 pagesCourse Outline-Constitutional History of India (2022)Aditya BelsareNo ratings yet

- 2MBA-027 (GBL V Coke)Document8 pages2MBA-027 (GBL V Coke)Anonymous ofr6kiAwNo ratings yet

- 2010 Centralized Bar Operations: San Beda College of LawDocument29 pages2010 Centralized Bar Operations: San Beda College of LawNick Tejada LusticaNo ratings yet

- 2 - Research Paper Not FinalDocument76 pages2 - Research Paper Not FinalJohn Claude Celeste100% (1)

- Team Alias: Gevorgian: LaimantDocument7 pagesTeam Alias: Gevorgian: Laimantbalaj iqbalNo ratings yet

- RFK Jr. Plans To File Lawsuit Against Nevada Over Ballot AccessDocument19 pagesRFK Jr. Plans To File Lawsuit Against Nevada Over Ballot AccessFaris TanyosNo ratings yet

- T1 PERKI - Alexander Veraro Tarigan - 175010100111024Document4 pagesT1 PERKI - Alexander Veraro Tarigan - 175010100111024AlexanderTariganNo ratings yet

- Reply To Response To Motion To Compel Xcentric To Comply With SubpoenaDocument7 pagesReply To Response To Motion To Compel Xcentric To Comply With SubpoenaRipoff ReportNo ratings yet

- AFP National Guideline On Uniform and Standards of Dress PDFDocument43 pagesAFP National Guideline On Uniform and Standards of Dress PDFRah YonetNo ratings yet

- 2 - Us v. Loo Hoe, 36 Phil 867Document1 page2 - Us v. Loo Hoe, 36 Phil 867gerlie22No ratings yet

- Notice To Contractor 3-24-2014 Rev 3 3925-0Document2 pagesNotice To Contractor 3-24-2014 Rev 3 3925-0jubo99No ratings yet

- Essay LW6606 - Marie Mehaudens - IACtHR and Amnesty LawsDocument22 pagesEssay LW6606 - Marie Mehaudens - IACtHR and Amnesty Lawsmarie.mehaudensNo ratings yet

- United States Court of Appeals, Fifth CircuitDocument7 pagesUnited States Court of Appeals, Fifth CircuitScribd Government DocsNo ratings yet

- Application FormDocument4 pagesApplication FormesanogunsNo ratings yet

- Rubi v. Provincial Board of Mindoro (Digest)Document2 pagesRubi v. Provincial Board of Mindoro (Digest)Abi Continuado100% (5)

- LRTA Vs NatividadDocument2 pagesLRTA Vs NatividadVianca Miguel100% (2)

- PIL-Commissioner of Internal Revenue V JOHN GOTAMCO and SONSDocument5 pagesPIL-Commissioner of Internal Revenue V JOHN GOTAMCO and SONSlaw mabaylabayNo ratings yet

- Law On Obligations and Contracts 1Document15 pagesLaw On Obligations and Contracts 1Joefrey Pujadas Baluma0% (1)

- APMSEFCDocument2 pagesAPMSEFCHarinath ReddyNo ratings yet

- Wittenberg Vs Beachwalk: Aka As Homeowners Vs HOA IndustryDocument23 pagesWittenberg Vs Beachwalk: Aka As Homeowners Vs HOA Industry"Buzz" AguirreNo ratings yet

- Yograj Infrastructure LTD VDocument3 pagesYograj Infrastructure LTD VAakash NarangNo ratings yet

- E232 Common Safety Signs: Uses of These SignsDocument8 pagesE232 Common Safety Signs: Uses of These SignsTcer OdahNo ratings yet

- Buenaventura V RamosDocument4 pagesBuenaventura V RamosMiguel CastricionesNo ratings yet

- Contract Act NotesDocument14 pagesContract Act NotesSyed Zohaib RazaNo ratings yet

- United States v. Harry Davidoff, Salvatore Santoro, Frank Manzo, Henry Bono, Jr., Frank Calise, John Russo, Heino Benthin, Pasquale Raucci, Leone Manzo, and William Barone, 845 F.2d 1151, 2d Cir. (1988)Document8 pagesUnited States v. Harry Davidoff, Salvatore Santoro, Frank Manzo, Henry Bono, Jr., Frank Calise, John Russo, Heino Benthin, Pasquale Raucci, Leone Manzo, and William Barone, 845 F.2d 1151, 2d Cir. (1988)Scribd Government DocsNo ratings yet