Download as pdf or txt

You might also like

- Chapter 4 Exempt SalesDocument23 pagesChapter 4 Exempt SalesHazel Jane Esclamada0% (2)

- DB Research Short SellingDocument6 pagesDB Research Short SellingMichael SadlerNo ratings yet

- ACYMAG1 Exercise Set #1Document9 pagesACYMAG1 Exercise Set #1123r12f10% (1)

- Accounting For Investments in Debt InstrumentsDocument4 pagesAccounting For Investments in Debt InstrumentsKeahlyn Boticario CapinaNo ratings yet

- L 1Document5 pagesL 1Elizabeth Espinosa ManilagNo ratings yet

- Chapter 17 Donor's TaxDocument7 pagesChapter 17 Donor's TaxHazel Jane Esclamada100% (3)

- Estate Tax PayableDocument8 pagesEstate Tax PayableHazel Jane Esclamada100% (2)

- Course Financial Management Developer and Their Background: See Assignment / Agreement SectionDocument33 pagesCourse Financial Management Developer and Their Background: See Assignment / Agreement SectionHazel Jane Esclamada100% (1)

- Chapter 9 Input VatDocument10 pagesChapter 9 Input VatHazel Jane EsclamadaNo ratings yet

- Chapter 10 Vat Still DueDocument7 pagesChapter 10 Vat Still DueHazel Jane EsclamadaNo ratings yet

- Chapter 3 Introduction To Business TaxationDocument27 pagesChapter 3 Introduction To Business TaxationHazel Jane Esclamada100% (1)

- IMCh 02Document13 pagesIMCh 02Sakub Amin Sick'L'No ratings yet

- Bond Investment - FVOCI: Subject Intermediate Accounting Teacher Dessa Dianna MadridDocument23 pagesBond Investment - FVOCI: Subject Intermediate Accounting Teacher Dessa Dianna MadridJohn Warren MestiolaNo ratings yet

- Week 05 - 02 - Module 11 - Investment in Equity InstrumentsDocument10 pagesWeek 05 - 02 - Module 11 - Investment in Equity Instruments지마리No ratings yet

- Investment PropertyDocument3 pagesInvestment PropertyacyNo ratings yet

- Debt RestructuringDocument4 pagesDebt RestructuringAra BellaNo ratings yet

- Cash Price Equivalent at The Deferred Beyond Normal CreditDocument5 pagesCash Price Equivalent at The Deferred Beyond Normal CreditSharmin ReulaNo ratings yet

- Investment in Equity SecuritiesDocument3 pagesInvestment in Equity Securitiesmiss independentNo ratings yet

- Investment in Equity SecuritiesDocument4 pagesInvestment in Equity SecuritiesElaineJrV-IgotNo ratings yet

- FAR.2906 - PPE-Depreciation and Derecognition.Document4 pagesFAR.2906 - PPE-Depreciation and Derecognition.John Nathan KinglyNo ratings yet

- 0f926440 1614316682621Document20 pages0f926440 1614316682621Abby NavarroNo ratings yet

- GEN 010 For BSA INVESTMENTS IN DEBT SECURITIESDocument7 pagesGEN 010 For BSA INVESTMENTS IN DEBT SECURITIESJoy RadaNo ratings yet

- FAR Handout Investment PropertyDocument4 pagesFAR Handout Investment PropertyPIOLA CAPINANo ratings yet

- Reviewer Borrowing Cost Sec. 1-10Document4 pagesReviewer Borrowing Cost Sec. 1-10imsana minatozakiNo ratings yet

- Assignment 14Document4 pagesAssignment 14Sova ShockdartNo ratings yet

- Gold and Blue Summary Notes - Investment in AssociateDocument6 pagesGold and Blue Summary Notes - Investment in AssociateBryzan Dela CruzNo ratings yet

- Investment in AssociateDocument21 pagesInvestment in AssociateSky SoronoiNo ratings yet

- Unit IA ID. Rematch Unit Drill On Cash and Cash Equivalents Petty Cash Bank Recon Proof of Cash 1Document5 pagesUnit IA ID. Rematch Unit Drill On Cash and Cash Equivalents Petty Cash Bank Recon Proof of Cash 1MARK JHEN SALANGNo ratings yet

- Far Eastern University - Makati: Discussion ProblemsDocument2 pagesFar Eastern University - Makati: Discussion ProblemsMarielle SidayonNo ratings yet

- Pas 16 Property, Plant and EquipmentDocument7 pagesPas 16 Property, Plant and EquipmentElaiza Jane CruzNo ratings yet

- Week 09 - Inventory EstimationsDocument3 pagesWeek 09 - Inventory EstimationsPj ManezNo ratings yet

- Liabilities Part 2Document4 pagesLiabilities Part 2Jay LloydNo ratings yet

- PCOA Module 6 - PAS 23 and 24Document8 pagesPCOA Module 6 - PAS 23 and 24Jan JanNo ratings yet

- 06A Investment in Equity Securities (Financial Assets at FMV, Investment in Associates)Document6 pages06A Investment in Equity Securities (Financial Assets at FMV, Investment in Associates)randomlungs121223No ratings yet

- Financial Instrument - (NEW)Document11 pagesFinancial Instrument - (NEW)AS Gaming100% (1)

- ACT1104-Final Period Quiz No. 6 With AnswerDocument12 pagesACT1104-Final Period Quiz No. 6 With AnswerPj Dela VegaNo ratings yet

- Intermediate Accounting 1Document18 pagesIntermediate Accounting 1Shaina Jane LibiranNo ratings yet

- Derivatives & HedgingDocument10 pagesDerivatives & HedgingKimberly IgnacioNo ratings yet

- Chapter 6 - Teacher's Manual - Ifa Part 1aDocument12 pagesChapter 6 - Teacher's Manual - Ifa Part 1aCharmae Agan CaroroNo ratings yet

- Theory of Accounts - 1Document9 pagesTheory of Accounts - 1Joovs JoovhoNo ratings yet

- Chapter 26 Land and BuildingDocument17 pagesChapter 26 Land and BuildingKendall JennerNo ratings yet

- Chapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Document66 pagesChapter 20 - Effective Interest Method (Amortized Cost, FVOCI, FVPL)Never Letting GoNo ratings yet

- An Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsDocument38 pagesAn Introduction An Introduction: Nature and Scope of Accounting For Government and Non-Profit OrganizationsPhrexilyn PajarilloNo ratings yet

- Asset Standard Initial Measurement Subsequent Measurement Included in Profit or Loss Financial POSITION PresentationDocument3 pagesAsset Standard Initial Measurement Subsequent Measurement Included in Profit or Loss Financial POSITION PresentationDidhane MartinezNo ratings yet

- PrelimsDocument24 pagesPrelimsRhea BadanaNo ratings yet

- Wasting Assets - ProblemsDocument5 pagesWasting Assets - ProblemsMarkNo ratings yet

- Financial Accounting and Reporting - QUIZ 5Document4 pagesFinancial Accounting and Reporting - QUIZ 5JINGLE FULGENCIONo ratings yet

- Cost Accounting & Control (Acecost) Chapter 1: Cost Accounting FundamentalsDocument8 pagesCost Accounting & Control (Acecost) Chapter 1: Cost Accounting FundamentalsXyne FernandezNo ratings yet

- This Study Resource Was: (Stale Check)Document2 pagesThis Study Resource Was: (Stale Check)Lyca Mae CubangbangNo ratings yet

- DepreciationDocument14 pagesDepreciationKris Hazel RentonNo ratings yet

- 8 - Intangible AssetsDocument80 pages8 - Intangible AssetsKRISTINA DENISSE SAN JOSENo ratings yet

- FAFVPL-FAFVOCI IARev RLPDocument2 pagesFAFVPL-FAFVOCI IARev RLPBrian Daniel BayotNo ratings yet

- Midterm Examination AnswersDocument3 pagesMidterm Examination AnswersMilani Joy LazoNo ratings yet

- REVIEWER Intangible AssetsDocument5 pagesREVIEWER Intangible AssetsCarl DionisioNo ratings yet

- Module 12 PAS 36Document6 pagesModule 12 PAS 36Jan JanNo ratings yet

- Chapter 27 MachineryDocument20 pagesChapter 27 MachineryKendall JennerNo ratings yet

- (01I) Lower of Cost and NRVDocument3 pages(01I) Lower of Cost and NRVGabriel Adrian ObungenNo ratings yet

- ACC124 Doubtful-AccountsDocument24 pagesACC124 Doubtful-Accountsジェロスミ プエブラスNo ratings yet

- Discussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument3 pagesDiscussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesNo ratings yet

- Intermediate Accounting Unit4 - Topic4Document8 pagesIntermediate Accounting Unit4 - Topic4Lea Polinar100% (1)

- 16 Property Plant and EquipmentDocument2 pages16 Property Plant and EquipmentRex AdarmeNo ratings yet

- C9 Receivable Financing Discounting of Notes ReceivableDocument24 pagesC9 Receivable Financing Discounting of Notes ReceivableAngelie LaxaNo ratings yet

- Aud Application 2 - Handout 2 Borrowing Cost (UST)Document2 pagesAud Application 2 - Handout 2 Borrowing Cost (UST)RNo ratings yet

- Prac. 1Document15 pagesPrac. 1Lalaine De JesusNo ratings yet

- FAR.3406 PPE-Depreciation and DerecognitionDocument3 pagesFAR.3406 PPE-Depreciation and DerecognitionMonica GarciaNo ratings yet

- Chapter 11 Other Long Term InvestmentsDocument10 pagesChapter 11 Other Long Term InvestmentsChristian Jade Lumasag NavaNo ratings yet

- Reviewer in Intermediate Accounting (Midterm)Document9 pagesReviewer in Intermediate Accounting (Midterm)Czarhiena SantiagoNo ratings yet

- ch21 ReclassificationDocument6 pagesch21 Reclassificationmercyvienho100% (1)

- Chapter 21 - Reclassification of Financial Asset PDFDocument9 pagesChapter 21 - Reclassification of Financial Asset PDFTurksNo ratings yet

- Photography 2Document48 pagesPhotography 2Hazel Jane EsclamadaNo ratings yet

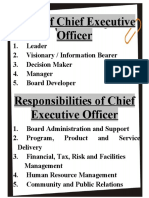

- Report - Roles of CEODocument2 pagesReport - Roles of CEOHazel Jane EsclamadaNo ratings yet

- Mas 3 Module 1 Fs AnalysisDocument19 pagesMas 3 Module 1 Fs AnalysisHazel Jane EsclamadaNo ratings yet

- Introduction To Donor's TaxDocument7 pagesIntroduction To Donor's TaxHazel Jane EsclamadaNo ratings yet

- Introduction To Financial ManagementDocument43 pagesIntroduction To Financial ManagementHazel Jane EsclamadaNo ratings yet

- Photography 3 (Updated)Document28 pagesPhotography 3 (Updated)Hazel Jane EsclamadaNo ratings yet

- Topic 4 - EXERCISES6 - Capital Current Liabilities ManagementDocument36 pagesTopic 4 - EXERCISES6 - Capital Current Liabilities ManagementHazel Jane Esclamada100% (1)

- MAS-3-Roque - Answer KeyDocument6 pagesMAS-3-Roque - Answer KeyHazel Jane Esclamada100% (1)

- Module Far1 Unit-1 Part-1c.1Document6 pagesModule Far1 Unit-1 Part-1c.1Hazel Jane EsclamadaNo ratings yet

- Topic 3 & 4 - EXERCISES3 - Working Capital Management - TheoriesDocument36 pagesTopic 3 & 4 - EXERCISES3 - Working Capital Management - TheoriesHazel Jane EsclamadaNo ratings yet

- TSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPDocument3 pagesTSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPHazel Jane EsclamadaNo ratings yet

- Module Far1 Unit-1 Part-1bDocument5 pagesModule Far1 Unit-1 Part-1bHazel Jane EsclamadaNo ratings yet

- MODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Document19 pagesMODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Hazel Jane Esclamada0% (1)

- Working Capital FinanceDocument12 pagesWorking Capital FinanceYeoh Mae100% (4)

- Inventory Management: Multiple Choice QuestionsDocument3 pagesInventory Management: Multiple Choice QuestionsHazel Jane Esclamada33% (3)

- Warranties, Provisions and Contingent LiabilitiesDocument31 pagesWarranties, Provisions and Contingent LiabilitiesHazel Jane EsclamadaNo ratings yet

- Module 2.1 (Property, Plant, and Equipment)Document15 pagesModule 2.1 (Property, Plant, and Equipment)Hazel Jane EsclamadaNo ratings yet

- Topic 4 - Current Liabilities Sample ProblemsDocument8 pagesTopic 4 - Current Liabilities Sample ProblemsHazel Jane EsclamadaNo ratings yet

- Concept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Document12 pagesConcept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Hazel Jane Esclamada100% (1)

- Introduction To Transfer TaxationDocument6 pagesIntroduction To Transfer TaxationHazel Jane EsclamadaNo ratings yet

- Topic 7 Transfer PricingDocument3 pagesTopic 7 Transfer PricingHazel Jane EsclamadaNo ratings yet

- What To Do With Perceived Environmental ViolationsDocument15 pagesWhat To Do With Perceived Environmental ViolationsHazel Jane EsclamadaNo ratings yet

- Chapter 1 Tax 2Document5 pagesChapter 1 Tax 2Hazel Jane EsclamadaNo ratings yet

- Official Business Plan FormatDocument3 pagesOfficial Business Plan FormatJa FloresNo ratings yet

- HSBC India Global Markets OverviewDocument10 pagesHSBC India Global Markets OverviewKaustubh KambekarNo ratings yet

- Trading CompsDocument8 pagesTrading CompsLeonardoNo ratings yet

- ACCCOB 2 Reflection 4 PDFDocument4 pagesACCCOB 2 Reflection 4 PDFMIGUEL DIEGO PANGILINANNo ratings yet

- The Winning MethodDocument25 pagesThe Winning MethodLeo Nardo Cebua Hinggaray100% (1)

- Corporate Finance Academic Year 2011-2012 TutorialsDocument21 pagesCorporate Finance Academic Year 2011-2012 TutorialsSander Levert100% (1)

- K - StocktonDocument20 pagesK - StocktonDi MitriNo ratings yet

- A Great Automated Trading System - MagicBreakoutDocument14 pagesA Great Automated Trading System - MagicBreakoutminupatel7950No ratings yet

- Equity ReportDocument34 pagesEquity ReportSagarNo ratings yet

- Research-Driven Cardano DEX White Paper v1: MaladexDocument88 pagesResearch-Driven Cardano DEX White Paper v1: MaladexAlan OmriNo ratings yet

- Advanced International Relations Paper 1 by Prof Halima Afridi - CBPBOOKDocument1 pageAdvanced International Relations Paper 1 by Prof Halima Afridi - CBPBOOKFizza KhanNo ratings yet

- Parker Corp Deal Sheet 11-25-20 KGDocument3 pagesParker Corp Deal Sheet 11-25-20 KGjoesphsteelNo ratings yet

- Individual Risk Return ExerciseDocument2 pagesIndividual Risk Return ExerciseAbirMdZaberTauhidNo ratings yet

- S F M - New Syllabus - Study MaterialDocument455 pagesS F M - New Syllabus - Study MaterialTummu SureshNo ratings yet

- Class 5 - Customer LifecycleDocument22 pagesClass 5 - Customer LifecycleAneesh SasidharanNo ratings yet

- Introduction To Malaysian Financial SystemDocument20 pagesIntroduction To Malaysian Financial SystemLim BoonShen100% (4)

- Issue of Shares Question Part 1Document2 pagesIssue of Shares Question Part 1Madhvi Gaur.No ratings yet

- Forex Trading Strategies - Supply and Demand Exposed - Hacking The Forex Market With The ASSARV10 TeaDocument3 pagesForex Trading Strategies - Supply and Demand Exposed - Hacking The Forex Market With The ASSARV10 TeaMichael MarioNo ratings yet

- The Role of Customer Relationship Management in Enhancing Customer LoyaltyDocument83 pagesThe Role of Customer Relationship Management in Enhancing Customer LoyaltyAkash MajjiNo ratings yet

- Other Long-Term Investments: NAME: Piolo Encela Date: 5-11-2020 Professor: Dr. Valcorza Section: BSA 1B ScoreDocument2 pagesOther Long-Term Investments: NAME: Piolo Encela Date: 5-11-2020 Professor: Dr. Valcorza Section: BSA 1B ScoreKrissa Mae LongosNo ratings yet

- Entrepreneurship Finals ReviewerDocument7 pagesEntrepreneurship Finals ReviewerZyrel OtucanNo ratings yet

- NIFTY Options Open Interest AnalysisDocument26 pagesNIFTY Options Open Interest AnalysisindianroadromeoNo ratings yet

- EQIBank - Overview 4Document10 pagesEQIBank - Overview 4royaleliontradingaccNo ratings yet

- Chapter 5Document35 pagesChapter 5ali.view6910No ratings yet

- ACTBFAR Work Text - Chapter 13. - 2T1920 - FormattedDocument7 pagesACTBFAR Work Text - Chapter 13. - 2T1920 - FormattednuggsNo ratings yet

- FMI - Adequacy of The Global Financial Safety Net. Considerations For Fund Toolkit Reform (2017)Document41 pagesFMI - Adequacy of The Global Financial Safety Net. Considerations For Fund Toolkit Reform (2017)Bautista GriffiniNo ratings yet

- Trade Lifecycle 1Document15 pagesTrade Lifecycle 1RamNo ratings yet

- Introduction To Corporate Finance 4Th Edition Booth Test Bank Full Chapter PDFDocument60 pagesIntroduction To Corporate Finance 4Th Edition Booth Test Bank Full Chapter PDFpandoratram2c2100% (12)