AB FMR Assignment

AB FMR Assignment

You might also like

- Solution Manual For Global Investments 6 e 6th Edition Bruno Solnik Dennis McleaveyDocument6 pagesSolution Manual For Global Investments 6 e 6th Edition Bruno Solnik Dennis McleaveyAntonioHallbnoa100% (44)

- Child Rights in India With Reference of Pocso Act: Adnan Belim A21521616003Document106 pagesChild Rights in India With Reference of Pocso Act: Adnan Belim A21521616003Sahida Parveen83% (6)

- Winning On Wall Street (Revised Edition) by Martin ZweigDocument153 pagesWinning On Wall Street (Revised Edition) by Martin ZweigIris Wang100% (6)

- Risk Return Analysis andDocument30 pagesRisk Return Analysis andvishvhomeNo ratings yet

- Performance Evaluation of Elss Schemes of Mutual Funds-Project by ShivaniDocument53 pagesPerformance Evaluation of Elss Schemes of Mutual Funds-Project by Shivanicutepie0671% (7)

- 8 Rgnul National Moot Court Competition, 2019: Before The Hon'Ble Supreme Court of IndiaDocument15 pages8 Rgnul National Moot Court Competition, 2019: Before The Hon'Ble Supreme Court of IndiaSahida Parveen100% (1)

- Corporate Finance Essay 0860103Document3 pagesCorporate Finance Essay 0860103Tuhin ChaturvediNo ratings yet

- Laxmi Soumya - 191239 (Research Report)Document15 pagesLaxmi Soumya - 191239 (Research Report)Laxmi SoumyaNo ratings yet

- Project Report On Mutual FundDocument60 pagesProject Report On Mutual FundBaldeep KaurNo ratings yet

- Welcome To The Mutual Funds Resource CenterDocument6 pagesWelcome To The Mutual Funds Resource CentersivaranjinirathinamNo ratings yet

- Cbi 01 MFS PPT1Document17 pagesCbi 01 MFS PPT1rishi raj modiNo ratings yet

- 31 Comp Study of MfsDocument105 pages31 Comp Study of MfsManisha PattaNo ratings yet

- IntroductionDocument58 pagesIntroductionSumit AgarwalNo ratings yet

- FinalDocument110 pagesFinalMadhur GuptaNo ratings yet

- All About Mutual FundsDocument53 pagesAll About Mutual FundsNilesh GosraniNo ratings yet

- Research Guide Submitted byDocument76 pagesResearch Guide Submitted byGaurav SawlaniNo ratings yet

- Mutual Funds: Learning OutcomesDocument47 pagesMutual Funds: Learning OutcomesPravesh PangeniNo ratings yet

- Chapter 1Document15 pagesChapter 1Aryan KapsNo ratings yet

- Chapter IDocument22 pagesChapter Irahmath faraNo ratings yet

- Intership Report Sem 1 ParaphrasedDocument17 pagesIntership Report Sem 1 Paraphrasedsri vastavNo ratings yet

- Research Proposal: Title of The StudyDocument67 pagesResearch Proposal: Title of The Studyhardikpatel11No ratings yet

- Thakare 1Document50 pagesThakare 1Abhishek MishraNo ratings yet

- Assignment Capital 2Document6 pagesAssignment Capital 2Mohammad ArsalanNo ratings yet

- Mutual FundDocument170 pagesMutual FundPatel UrveshNo ratings yet

- Stock Market TutorialDocument63 pagesStock Market TutorialKaran PatelNo ratings yet

- Introduction On A Study On Investment Avenues in Mutual Funds"Document80 pagesIntroduction On A Study On Investment Avenues in Mutual Funds"Nayana NayuNo ratings yet

- Analysis of Mutual Funds in IndiaDocument78 pagesAnalysis of Mutual Funds in Indiadpk1234No ratings yet

- Performance Evaluation of Mutual Funds" Conducted at EMKAY GLOBAL FINANCIAL SERVICES PRIVATE LTDDocument74 pagesPerformance Evaluation of Mutual Funds" Conducted at EMKAY GLOBAL FINANCIAL SERVICES PRIVATE LTDPrashanth PBNo ratings yet

- Mutual Fund ProjectDocument69 pagesMutual Fund ProjectSatish PenumarthiNo ratings yet

- A Study On Performance of The Indian Mutual Fund IndustryDocument67 pagesA Study On Performance of The Indian Mutual Fund IndustryChethan.sNo ratings yet

- Introduction To The Topic Mutual FundDocument53 pagesIntroduction To The Topic Mutual FundPooja MouliNo ratings yet

- Akash ProjectDocument64 pagesAkash ProjectChethan.sNo ratings yet

- A Project Report On Comparative Analysis Ulip Vs Mutual Funds - NetworthDocument72 pagesA Project Report On Comparative Analysis Ulip Vs Mutual Funds - NetworthNagireddy Kalluri83% (6)

- Introduction of Mutual 22222Document210 pagesIntroduction of Mutual 22222mahaNo ratings yet

- MUtual Funds PPT BasedDocument10 pagesMUtual Funds PPT BasedKARISHMAATA2No ratings yet

- Introduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"Document94 pagesIntroduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"Rocks KiranNo ratings yet

- Mutual FundsDocument35 pagesMutual FundsParul BajajNo ratings yet

- Assignment Capital 2Document6 pagesAssignment Capital 2Mohammad ArsalanNo ratings yet

- A Study of Mutual FundDocument36 pagesA Study of Mutual Fundvijay dhondiyalNo ratings yet

- A Study of Mutual Funds As Perfered Choice of InvestmentDocument36 pagesA Study of Mutual Funds As Perfered Choice of Investmentshlok pathakNo ratings yet

- Finance Project On "Analysis On Performance of Mutual Fund Companies in India"Document94 pagesFinance Project On "Analysis On Performance of Mutual Fund Companies in India"balaji bysani84% (32)

- Analysis of Performance of Franklin India Blue Chip Fund: Title of The ProjectDocument8 pagesAnalysis of Performance of Franklin India Blue Chip Fund: Title of The ProjectPRITAM PATRANo ratings yet

- Project - PORTFOLIO ANALYSIS OF MUTUAL FUNDS IN RELIANCE MONYDocument50 pagesProject - PORTFOLIO ANALYSIS OF MUTUAL FUNDS IN RELIANCE MONYRajendra GawateNo ratings yet

- FinalDocument83 pagesFinalPrajwal SrinivasNo ratings yet

- Introduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"Document96 pagesIntroduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"HarshSuryavanshiNo ratings yet

- Perception of Employees Investment in Mutual Funds - Thanmaie (Final)Document49 pagesPerception of Employees Investment in Mutual Funds - Thanmaie (Final)DivyaNo ratings yet

- ICICI Mutual FundDocument49 pagesICICI Mutual FundkalyanbobbydNo ratings yet

- Chapter 2 (ABSLAMC)Document20 pagesChapter 2 (ABSLAMC)akhilNo ratings yet

- New Black Book PDFDocument73 pagesNew Black Book PDFAmisha VithalaniNo ratings yet

- Chapter-1 Introduction of Mutual Funds: "A Study On Performance of The Indian Mutual Fund Industry"Document67 pagesChapter-1 Introduction of Mutual Funds: "A Study On Performance of The Indian Mutual Fund Industry"ChethanNo ratings yet

- Reliance Growth Fund ProjectDocument69 pagesReliance Growth Fund ProjectVikram GundalaNo ratings yet

- A Project Report On MFDocument76 pagesA Project Report On MFsantoshbansodeNo ratings yet

- A Comparitive Study On Mutual FundsDocument58 pagesA Comparitive Study On Mutual Fundsarjunmba119624No ratings yet

- Objective of The Study Primary ObjectivesDocument6 pagesObjective of The Study Primary ObjectiveszeeiqmarahmedNo ratings yet

- Chapter 1Document15 pagesChapter 1Harry HaranNo ratings yet

- Pooja Project 2Document109 pagesPooja Project 2Rashmitha HonnaiahNo ratings yet

- Mutual Fund Yogesh 2Document24 pagesMutual Fund Yogesh 2Yogesh KumarNo ratings yet

- Summer Training ReportDocument80 pagesSummer Training Reportmanu_1988No ratings yet

- Mutual FundDocument59 pagesMutual FundStephina EdakkalathurNo ratings yet

- Chapter One Introduction To Mutual FundDocument8 pagesChapter One Introduction To Mutual FundanishawalavalkarNo ratings yet

- Report Format For Capstone Project-I - 2Document128 pagesReport Format For Capstone Project-I - 2Ritesh SiNghNo ratings yet

- Content: No Particular Page No 1 2 2 3Document68 pagesContent: No Particular Page No 1 2 2 3amitnpatel1No ratings yet

- Mutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingFrom EverandMutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingNo ratings yet

- Canadian Mutual Funds Investing for Beginners: A Basic Guide for BeginnersFrom EverandCanadian Mutual Funds Investing for Beginners: A Basic Guide for BeginnersNo ratings yet

- Investing Made Easy: Finding the Right Opportunities for YouFrom EverandInvesting Made Easy: Finding the Right Opportunities for YouNo ratings yet

- Final Memo-AppellantDocument37 pagesFinal Memo-AppellantSahida ParveenNo ratings yet

- Icc SynopsisDocument2 pagesIcc SynopsisSahida ParveenNo ratings yet

- RM - AssignmentDocument4 pagesRM - AssignmentSahida ParveenNo ratings yet

- Adnaan Belim LLM (Constitution) 1 SemesterDocument3 pagesAdnaan Belim LLM (Constitution) 1 SemesterSahida ParveenNo ratings yet

- Case AnalysisDocument9 pagesCase AnalysisSahida ParveenNo ratings yet

- Amity University Rajasthan: Cyber Security AssignmentDocument3 pagesAmity University Rajasthan: Cyber Security AssignmentSahida ParveenNo ratings yet

- Adnaan Belim LLM (Constitution) 1 SEM Class TestDocument3 pagesAdnaan Belim LLM (Constitution) 1 SEM Class TestSahida ParveenNo ratings yet

- Amity University Rajasthan: Fundamental Rights, Fundamental Duties and Directive Principles of State PolicyDocument9 pagesAmity University Rajasthan: Fundamental Rights, Fundamental Duties and Directive Principles of State PolicySahida ParveenNo ratings yet

- Bs AssignmentDocument8 pagesBs AssignmentSahida ParveenNo ratings yet

- PIL AssignmentDocument13 pagesPIL AssignmentSahida ParveenNo ratings yet

- Study Questions: (With Answers)Document6 pagesStudy Questions: (With Answers)Sahida ParveenNo ratings yet

- Amity University Rajasthan: Criminal Law Hons. AssignmentDocument9 pagesAmity University Rajasthan: Criminal Law Hons. AssignmentSahida ParveenNo ratings yet

- Amity University RajasthanDocument4 pagesAmity University RajasthanSahida Parveen100% (1)

- Case Analysis M C Mehta V Union of IndiaDocument3 pagesCase Analysis M C Mehta V Union of IndiaSahida ParveenNo ratings yet

- Probation AssignmentDocument5 pagesProbation AssignmentSahida ParveenNo ratings yet

- 18-Tendolkar Committee Report of The Commission of Inquiry On The Administration of Dalmia - Jain CompaniesDocument824 pages18-Tendolkar Committee Report of The Commission of Inquiry On The Administration of Dalmia - Jain CompaniesSahida ParveenNo ratings yet

- Forensic ScienceDocument17 pagesForensic ScienceSahida ParveenNo ratings yet

- Chapter-I: 1.1 GeneralDocument12 pagesChapter-I: 1.1 GeneralSahida ParveenNo ratings yet

- International Trade LawDocument10 pagesInternational Trade LawSahida ParveenNo ratings yet

- Rajasthan JLO EvidenceDocument47 pagesRajasthan JLO EvidenceSahida ParveenNo ratings yet

- Probation and ParoleDocument2 pagesProbation and ParoleSahida Parveen100% (1)

- Amity Unversity Rajasthan: A Critical Study of White Coller Crimes in IndiaDocument6 pagesAmity Unversity Rajasthan: A Critical Study of White Coller Crimes in IndiaSahida ParveenNo ratings yet

- Public International LawDocument14 pagesPublic International LawSahida ParveenNo ratings yet

- Amity University Rajasthan: Probation and Parole AssignmentDocument5 pagesAmity University Rajasthan: Probation and Parole AssignmentSahida ParveenNo ratings yet

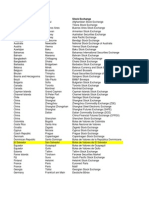

- List of Stock ExchangeDocument15 pagesList of Stock ExchangeTimothy MununuziNo ratings yet

- Early - HTML: Regulations Equity-Based Crowdfunding: Benefits and RisksDocument2 pagesEarly - HTML: Regulations Equity-Based Crowdfunding: Benefits and RisksAbhishek AryaNo ratings yet

- Tool Kit The Cost of CapitalDocument56 pagesTool Kit The Cost of CapitalBrandon FrancomNo ratings yet

- KKR Private Equity Investors, L.P. Annual Report 2006Document84 pagesKKR Private Equity Investors, L.P. Annual Report 2006AsiaBuyoutsNo ratings yet

- Meaning of DematerializationDocument2 pagesMeaning of DematerializationbanksNo ratings yet

- CFA-Chapter 7 Relative ValuationDocument62 pagesCFA-Chapter 7 Relative ValuationNoman MaqsoodNo ratings yet

- Case 2 Version1Document2 pagesCase 2 Version1varatvaiNo ratings yet

- Free Cash Flow Valuation AnswersDocument3 pagesFree Cash Flow Valuation AnswersJenny Chua100% (1)

- Eicher MotorsDocument4 pagesEicher MotorsSubham MazumdarNo ratings yet

- QQQ 2Document2 pagesQQQ 2Dominic angelNo ratings yet

- Corporate Finance: Chapter-8Document16 pagesCorporate Finance: Chapter-8AnongNo ratings yet

- Goldman SECDocument55 pagesGoldman SECZerohedgeNo ratings yet

- Presentation On Summer Training Report of Commodity MarketDocument14 pagesPresentation On Summer Training Report of Commodity MarketSuresh VermaNo ratings yet

- Vaswani Industries Limited IPO ViolationDocument4 pagesVaswani Industries Limited IPO ViolationtenetchatNo ratings yet

- Chap 012Document23 pagesChap 012princearoraNo ratings yet

- Excel Stock and Bond PortfolioDocument7 pagesExcel Stock and Bond Portfolioapi-27174321No ratings yet

- Dividend Policy WGDocument6 pagesDividend Policy WG20BBA137No ratings yet

- The Cyclical Nature of Active & Passive InvestingDocument8 pagesThe Cyclical Nature of Active & Passive Investingmatthew gerlachNo ratings yet

- CA Final SFM New Syllabus Full Chalisa Book by Aaditya Jain SirDocument48 pagesCA Final SFM New Syllabus Full Chalisa Book by Aaditya Jain SirYedu KrishnanNo ratings yet

- Essay On Bombay Stock ExchangeDocument2 pagesEssay On Bombay Stock ExchangeMahadev Techno WorldNo ratings yet

- SHAREKHANDocument63 pagesSHAREKHANShivani GoelNo ratings yet

- Art of Stock Investing Indian Stock MarketDocument10 pagesArt of Stock Investing Indian Stock MarketUmesh Kamath80% (5)

- Tax On Dividend Distribution, Distribution by Way of BuyBackDocument3 pagesTax On Dividend Distribution, Distribution by Way of BuyBackABC 123No ratings yet

- IIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER ADocument88 pagesIIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER AVajir BajiNo ratings yet

- Project On IPODocument24 pagesProject On IPOmysticalmana8100% (2)

- AFS - FormulasDocument2 pagesAFS - FormulasWaqar AhmadNo ratings yet

Download as docx, pdf, or txt

You might also like

- Solution Manual For Global Investments 6 e 6th Edition Bruno Solnik Dennis McleaveyDocument6 pagesSolution Manual For Global Investments 6 e 6th Edition Bruno Solnik Dennis McleaveyAntonioHallbnoa100% (44)

- Child Rights in India With Reference of Pocso Act: Adnan Belim A21521616003Document106 pagesChild Rights in India With Reference of Pocso Act: Adnan Belim A21521616003Sahida Parveen83% (6)

- Winning On Wall Street (Revised Edition) by Martin ZweigDocument153 pagesWinning On Wall Street (Revised Edition) by Martin ZweigIris Wang100% (6)

- Risk Return Analysis andDocument30 pagesRisk Return Analysis andvishvhomeNo ratings yet

- Performance Evaluation of Elss Schemes of Mutual Funds-Project by ShivaniDocument53 pagesPerformance Evaluation of Elss Schemes of Mutual Funds-Project by Shivanicutepie0671% (7)

- 8 Rgnul National Moot Court Competition, 2019: Before The Hon'Ble Supreme Court of IndiaDocument15 pages8 Rgnul National Moot Court Competition, 2019: Before The Hon'Ble Supreme Court of IndiaSahida Parveen100% (1)

- Corporate Finance Essay 0860103Document3 pagesCorporate Finance Essay 0860103Tuhin ChaturvediNo ratings yet

- Laxmi Soumya - 191239 (Research Report)Document15 pagesLaxmi Soumya - 191239 (Research Report)Laxmi SoumyaNo ratings yet

- Project Report On Mutual FundDocument60 pagesProject Report On Mutual FundBaldeep KaurNo ratings yet

- Welcome To The Mutual Funds Resource CenterDocument6 pagesWelcome To The Mutual Funds Resource CentersivaranjinirathinamNo ratings yet

- Cbi 01 MFS PPT1Document17 pagesCbi 01 MFS PPT1rishi raj modiNo ratings yet

- 31 Comp Study of MfsDocument105 pages31 Comp Study of MfsManisha PattaNo ratings yet

- IntroductionDocument58 pagesIntroductionSumit AgarwalNo ratings yet

- FinalDocument110 pagesFinalMadhur GuptaNo ratings yet

- All About Mutual FundsDocument53 pagesAll About Mutual FundsNilesh GosraniNo ratings yet

- Research Guide Submitted byDocument76 pagesResearch Guide Submitted byGaurav SawlaniNo ratings yet

- Mutual Funds: Learning OutcomesDocument47 pagesMutual Funds: Learning OutcomesPravesh PangeniNo ratings yet

- Chapter 1Document15 pagesChapter 1Aryan KapsNo ratings yet

- Chapter IDocument22 pagesChapter Irahmath faraNo ratings yet

- Intership Report Sem 1 ParaphrasedDocument17 pagesIntership Report Sem 1 Paraphrasedsri vastavNo ratings yet

- Research Proposal: Title of The StudyDocument67 pagesResearch Proposal: Title of The Studyhardikpatel11No ratings yet

- Thakare 1Document50 pagesThakare 1Abhishek MishraNo ratings yet

- Assignment Capital 2Document6 pagesAssignment Capital 2Mohammad ArsalanNo ratings yet

- Mutual FundDocument170 pagesMutual FundPatel UrveshNo ratings yet

- Stock Market TutorialDocument63 pagesStock Market TutorialKaran PatelNo ratings yet

- Introduction On A Study On Investment Avenues in Mutual Funds"Document80 pagesIntroduction On A Study On Investment Avenues in Mutual Funds"Nayana NayuNo ratings yet

- Analysis of Mutual Funds in IndiaDocument78 pagesAnalysis of Mutual Funds in Indiadpk1234No ratings yet

- Performance Evaluation of Mutual Funds" Conducted at EMKAY GLOBAL FINANCIAL SERVICES PRIVATE LTDDocument74 pagesPerformance Evaluation of Mutual Funds" Conducted at EMKAY GLOBAL FINANCIAL SERVICES PRIVATE LTDPrashanth PBNo ratings yet

- Mutual Fund ProjectDocument69 pagesMutual Fund ProjectSatish PenumarthiNo ratings yet

- A Study On Performance of The Indian Mutual Fund IndustryDocument67 pagesA Study On Performance of The Indian Mutual Fund IndustryChethan.sNo ratings yet

- Introduction To The Topic Mutual FundDocument53 pagesIntroduction To The Topic Mutual FundPooja MouliNo ratings yet

- Akash ProjectDocument64 pagesAkash ProjectChethan.sNo ratings yet

- A Project Report On Comparative Analysis Ulip Vs Mutual Funds - NetworthDocument72 pagesA Project Report On Comparative Analysis Ulip Vs Mutual Funds - NetworthNagireddy Kalluri83% (6)

- Introduction of Mutual 22222Document210 pagesIntroduction of Mutual 22222mahaNo ratings yet

- MUtual Funds PPT BasedDocument10 pagesMUtual Funds PPT BasedKARISHMAATA2No ratings yet

- Introduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"Document94 pagesIntroduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"Rocks KiranNo ratings yet

- Mutual FundsDocument35 pagesMutual FundsParul BajajNo ratings yet

- Assignment Capital 2Document6 pagesAssignment Capital 2Mohammad ArsalanNo ratings yet

- A Study of Mutual FundDocument36 pagesA Study of Mutual Fundvijay dhondiyalNo ratings yet

- A Study of Mutual Funds As Perfered Choice of InvestmentDocument36 pagesA Study of Mutual Funds As Perfered Choice of Investmentshlok pathakNo ratings yet

- Finance Project On "Analysis On Performance of Mutual Fund Companies in India"Document94 pagesFinance Project On "Analysis On Performance of Mutual Fund Companies in India"balaji bysani84% (32)

- Analysis of Performance of Franklin India Blue Chip Fund: Title of The ProjectDocument8 pagesAnalysis of Performance of Franklin India Blue Chip Fund: Title of The ProjectPRITAM PATRANo ratings yet

- Project - PORTFOLIO ANALYSIS OF MUTUAL FUNDS IN RELIANCE MONYDocument50 pagesProject - PORTFOLIO ANALYSIS OF MUTUAL FUNDS IN RELIANCE MONYRajendra GawateNo ratings yet

- FinalDocument83 pagesFinalPrajwal SrinivasNo ratings yet

- Introduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"Document96 pagesIntroduction of Mutual Funds: "Analysis On Performance of Mutual Fund Companies in India"HarshSuryavanshiNo ratings yet

- Perception of Employees Investment in Mutual Funds - Thanmaie (Final)Document49 pagesPerception of Employees Investment in Mutual Funds - Thanmaie (Final)DivyaNo ratings yet

- ICICI Mutual FundDocument49 pagesICICI Mutual FundkalyanbobbydNo ratings yet

- Chapter 2 (ABSLAMC)Document20 pagesChapter 2 (ABSLAMC)akhilNo ratings yet

- New Black Book PDFDocument73 pagesNew Black Book PDFAmisha VithalaniNo ratings yet

- Chapter-1 Introduction of Mutual Funds: "A Study On Performance of The Indian Mutual Fund Industry"Document67 pagesChapter-1 Introduction of Mutual Funds: "A Study On Performance of The Indian Mutual Fund Industry"ChethanNo ratings yet

- Reliance Growth Fund ProjectDocument69 pagesReliance Growth Fund ProjectVikram GundalaNo ratings yet

- A Project Report On MFDocument76 pagesA Project Report On MFsantoshbansodeNo ratings yet

- A Comparitive Study On Mutual FundsDocument58 pagesA Comparitive Study On Mutual Fundsarjunmba119624No ratings yet

- Objective of The Study Primary ObjectivesDocument6 pagesObjective of The Study Primary ObjectiveszeeiqmarahmedNo ratings yet

- Chapter 1Document15 pagesChapter 1Harry HaranNo ratings yet

- Pooja Project 2Document109 pagesPooja Project 2Rashmitha HonnaiahNo ratings yet

- Mutual Fund Yogesh 2Document24 pagesMutual Fund Yogesh 2Yogesh KumarNo ratings yet

- Summer Training ReportDocument80 pagesSummer Training Reportmanu_1988No ratings yet

- Mutual FundDocument59 pagesMutual FundStephina EdakkalathurNo ratings yet

- Chapter One Introduction To Mutual FundDocument8 pagesChapter One Introduction To Mutual FundanishawalavalkarNo ratings yet

- Report Format For Capstone Project-I - 2Document128 pagesReport Format For Capstone Project-I - 2Ritesh SiNghNo ratings yet

- Content: No Particular Page No 1 2 2 3Document68 pagesContent: No Particular Page No 1 2 2 3amitnpatel1No ratings yet

- Mutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingFrom EverandMutual Funds - The Mutual Fund Retirement Plan For Long - Term Wealth BuildingNo ratings yet

- Canadian Mutual Funds Investing for Beginners: A Basic Guide for BeginnersFrom EverandCanadian Mutual Funds Investing for Beginners: A Basic Guide for BeginnersNo ratings yet

- Investing Made Easy: Finding the Right Opportunities for YouFrom EverandInvesting Made Easy: Finding the Right Opportunities for YouNo ratings yet

- Final Memo-AppellantDocument37 pagesFinal Memo-AppellantSahida ParveenNo ratings yet

- Icc SynopsisDocument2 pagesIcc SynopsisSahida ParveenNo ratings yet

- RM - AssignmentDocument4 pagesRM - AssignmentSahida ParveenNo ratings yet

- Adnaan Belim LLM (Constitution) 1 SemesterDocument3 pagesAdnaan Belim LLM (Constitution) 1 SemesterSahida ParveenNo ratings yet

- Case AnalysisDocument9 pagesCase AnalysisSahida ParveenNo ratings yet

- Amity University Rajasthan: Cyber Security AssignmentDocument3 pagesAmity University Rajasthan: Cyber Security AssignmentSahida ParveenNo ratings yet

- Adnaan Belim LLM (Constitution) 1 SEM Class TestDocument3 pagesAdnaan Belim LLM (Constitution) 1 SEM Class TestSahida ParveenNo ratings yet

- Amity University Rajasthan: Fundamental Rights, Fundamental Duties and Directive Principles of State PolicyDocument9 pagesAmity University Rajasthan: Fundamental Rights, Fundamental Duties and Directive Principles of State PolicySahida ParveenNo ratings yet

- Bs AssignmentDocument8 pagesBs AssignmentSahida ParveenNo ratings yet

- PIL AssignmentDocument13 pagesPIL AssignmentSahida ParveenNo ratings yet

- Study Questions: (With Answers)Document6 pagesStudy Questions: (With Answers)Sahida ParveenNo ratings yet

- Amity University Rajasthan: Criminal Law Hons. AssignmentDocument9 pagesAmity University Rajasthan: Criminal Law Hons. AssignmentSahida ParveenNo ratings yet

- Amity University RajasthanDocument4 pagesAmity University RajasthanSahida Parveen100% (1)

- Case Analysis M C Mehta V Union of IndiaDocument3 pagesCase Analysis M C Mehta V Union of IndiaSahida ParveenNo ratings yet

- Probation AssignmentDocument5 pagesProbation AssignmentSahida ParveenNo ratings yet

- 18-Tendolkar Committee Report of The Commission of Inquiry On The Administration of Dalmia - Jain CompaniesDocument824 pages18-Tendolkar Committee Report of The Commission of Inquiry On The Administration of Dalmia - Jain CompaniesSahida ParveenNo ratings yet

- Forensic ScienceDocument17 pagesForensic ScienceSahida ParveenNo ratings yet

- Chapter-I: 1.1 GeneralDocument12 pagesChapter-I: 1.1 GeneralSahida ParveenNo ratings yet

- International Trade LawDocument10 pagesInternational Trade LawSahida ParveenNo ratings yet

- Rajasthan JLO EvidenceDocument47 pagesRajasthan JLO EvidenceSahida ParveenNo ratings yet

- Probation and ParoleDocument2 pagesProbation and ParoleSahida Parveen100% (1)

- Amity Unversity Rajasthan: A Critical Study of White Coller Crimes in IndiaDocument6 pagesAmity Unversity Rajasthan: A Critical Study of White Coller Crimes in IndiaSahida ParveenNo ratings yet

- Public International LawDocument14 pagesPublic International LawSahida ParveenNo ratings yet

- Amity University Rajasthan: Probation and Parole AssignmentDocument5 pagesAmity University Rajasthan: Probation and Parole AssignmentSahida ParveenNo ratings yet

- List of Stock ExchangeDocument15 pagesList of Stock ExchangeTimothy MununuziNo ratings yet

- Early - HTML: Regulations Equity-Based Crowdfunding: Benefits and RisksDocument2 pagesEarly - HTML: Regulations Equity-Based Crowdfunding: Benefits and RisksAbhishek AryaNo ratings yet

- Tool Kit The Cost of CapitalDocument56 pagesTool Kit The Cost of CapitalBrandon FrancomNo ratings yet

- KKR Private Equity Investors, L.P. Annual Report 2006Document84 pagesKKR Private Equity Investors, L.P. Annual Report 2006AsiaBuyoutsNo ratings yet

- Meaning of DematerializationDocument2 pagesMeaning of DematerializationbanksNo ratings yet

- CFA-Chapter 7 Relative ValuationDocument62 pagesCFA-Chapter 7 Relative ValuationNoman MaqsoodNo ratings yet

- Case 2 Version1Document2 pagesCase 2 Version1varatvaiNo ratings yet

- Free Cash Flow Valuation AnswersDocument3 pagesFree Cash Flow Valuation AnswersJenny Chua100% (1)

- Eicher MotorsDocument4 pagesEicher MotorsSubham MazumdarNo ratings yet

- QQQ 2Document2 pagesQQQ 2Dominic angelNo ratings yet

- Corporate Finance: Chapter-8Document16 pagesCorporate Finance: Chapter-8AnongNo ratings yet

- Goldman SECDocument55 pagesGoldman SECZerohedgeNo ratings yet

- Presentation On Summer Training Report of Commodity MarketDocument14 pagesPresentation On Summer Training Report of Commodity MarketSuresh VermaNo ratings yet

- Vaswani Industries Limited IPO ViolationDocument4 pagesVaswani Industries Limited IPO ViolationtenetchatNo ratings yet

- Chap 012Document23 pagesChap 012princearoraNo ratings yet

- Excel Stock and Bond PortfolioDocument7 pagesExcel Stock and Bond Portfolioapi-27174321No ratings yet

- Dividend Policy WGDocument6 pagesDividend Policy WG20BBA137No ratings yet

- The Cyclical Nature of Active & Passive InvestingDocument8 pagesThe Cyclical Nature of Active & Passive Investingmatthew gerlachNo ratings yet

- CA Final SFM New Syllabus Full Chalisa Book by Aaditya Jain SirDocument48 pagesCA Final SFM New Syllabus Full Chalisa Book by Aaditya Jain SirYedu KrishnanNo ratings yet

- Essay On Bombay Stock ExchangeDocument2 pagesEssay On Bombay Stock ExchangeMahadev Techno WorldNo ratings yet

- SHAREKHANDocument63 pagesSHAREKHANShivani GoelNo ratings yet

- Art of Stock Investing Indian Stock MarketDocument10 pagesArt of Stock Investing Indian Stock MarketUmesh Kamath80% (5)

- Tax On Dividend Distribution, Distribution by Way of BuyBackDocument3 pagesTax On Dividend Distribution, Distribution by Way of BuyBackABC 123No ratings yet

- IIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER ADocument88 pagesIIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER AVajir BajiNo ratings yet

- Project On IPODocument24 pagesProject On IPOmysticalmana8100% (2)

- AFS - FormulasDocument2 pagesAFS - FormulasWaqar AhmadNo ratings yet