Download as pdf or txt

You might also like

- Group B&D - Case 19 - Fonderia PresentationDocument24 pagesGroup B&D - Case 19 - Fonderia PresentationVinithi Thongkampala100% (2)

- Case 26 Rockboro Group ADocument27 pagesCase 26 Rockboro Group AKanoknad KalaphakdeeNo ratings yet

- Rockboro Machine Tools Corporation Case QuestionsDocument1 pageRockboro Machine Tools Corporation Case QuestionsMasumiNo ratings yet

- Case Report "Stryker: In-Sourcing PCBS"Document2 pagesCase Report "Stryker: In-Sourcing PCBS"Vishakha ChopraNo ratings yet

- Case 7Document3 pagesCase 7Shaarang BeganiNo ratings yet

- Case Study On Gainesboro Machine Tools CorporationDocument13 pagesCase Study On Gainesboro Machine Tools Corporationemehmehmeh86% (7)

- Eastboro Case SolutionDocument22 pagesEastboro Case Solutionuddindjm100% (2)

- Individual Case Writing AssignmentDocument6 pagesIndividual Case Writing Assignmentapi-273010008No ratings yet

- OM Scott Case AnalysisDocument20 pagesOM Scott Case AnalysissushilkhannaNo ratings yet

- Submitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Document3 pagesSubmitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Aurva BhardwajNo ratings yet

- Massachusetts Financial Services Case AnalysisDocument4 pagesMassachusetts Financial Services Case AnalysisNayan Manik Tripura100% (2)

- T.1 Bahasa Inggris NiagaDocument2 pagesT.1 Bahasa Inggris NiagaNovi Risa0% (2)

- Introduction of Volkswagen Do Brasil Driving Strategy With The Balanced Scorecard Case Solutio1Document3 pagesIntroduction of Volkswagen Do Brasil Driving Strategy With The Balanced Scorecard Case Solutio1Pepito PerezNo ratings yet

- Rockboro Machine Tools Corporation: Source: Author EstimatesDocument10 pagesRockboro Machine Tools Corporation: Source: Author EstimatesMasumi0% (2)

- Dividend Policy Case (Gainesboro Machine Tools) - Session 2-Group 8Document19 pagesDividend Policy Case (Gainesboro Machine Tools) - Session 2-Group 8api-2001200071% (7)

- Envy Rides Case DecisionDocument4 pagesEnvy Rides Case DecisionMikey MadRatNo ratings yet

- Target Corporation: Ackman Versus The Board: FM2 Case Study AnalysisDocument6 pagesTarget Corporation: Ackman Versus The Board: FM2 Case Study AnalysisSuman MandalNo ratings yet

- Anagene - Final Case AssignmentDocument19 pagesAnagene - Final Case AssignmentSantiago Fernandez Moreno100% (1)

- Solutions To Chapters 7 and 8 Problem SetsDocument21 pagesSolutions To Chapters 7 and 8 Problem SetsMuhammad Hasnain100% (1)

- Group B&D Case 19 FonderiaDocument12 pagesGroup B&D Case 19 FonderiaVinithi ThongkampalaNo ratings yet

- This Study Resource Was: Group 9 - M&M Pizza Case StudyDocument2 pagesThis Study Resource Was: Group 9 - M&M Pizza Case StudyAsma AyedNo ratings yet

- Case Study 4 Winfield Refuse Management, Inc.: Raising Debt vs. EquityDocument5 pagesCase Study 4 Winfield Refuse Management, Inc.: Raising Debt vs. EquityAditya DashNo ratings yet

- Case 26 Assignment AnalysisDocument1 pageCase 26 Assignment AnalysisNiyanthesh Reddy50% (2)

- Buckeye Bank CaseDocument7 pagesBuckeye Bank CasePulkit Mathur0% (2)

- Facebook IPO Valuation AnalysisDocument13 pagesFacebook IPO Valuation AnalysisMegha BepariNo ratings yet

- Hill Country Snack Foods CoDocument9 pagesHill Country Snack Foods CoZjiajiajiajiaPNo ratings yet

- Hill CountryDocument8 pagesHill CountryAtif Raza AkbarNo ratings yet

- Final Case Study G M Machine Tools CorpDocument5 pagesFinal Case Study G M Machine Tools CorpShadab Akhter100% (1)

- Rockboro CaseDocument4 pagesRockboro CaseVan Arloe YuNo ratings yet

- Vers Hire Company Study CaseDocument11 pagesVers Hire Company Study CaseAradhysta SvarnabhumiNo ratings yet

- Eastboro Machine Tools CorporationDocument32 pagesEastboro Machine Tools Corporationrifki100% (2)

- Overview of The Problem:: 0%, 20%, 40% Dividend Payout Along With Residual Payout PolicyDocument2 pagesOverview of The Problem:: 0%, 20%, 40% Dividend Payout Along With Residual Payout PolicyJhonSteveNo ratings yet

- Case 25 Gainesboro-Exh8Document1 pageCase 25 Gainesboro-Exh8odie99No ratings yet

- Case Bidding For Antamina: This Study Resource Was Shared ViaDocument6 pagesCase Bidding For Antamina: This Study Resource Was Shared ViaRishavLakraNo ratings yet

- This Study Resource WasDocument7 pagesThis Study Resource WasmdNo ratings yet

- Jetblue: Relevant Sustainability Leadership (A) : Situational AnalysisDocument1 pageJetblue: Relevant Sustainability Leadership (A) : Situational AnalysisShivani KarkeraNo ratings yet

- Session 10 Simulation Questions PDFDocument6 pagesSession 10 Simulation Questions PDFVAIBHAV WADHWA0% (1)

- Accounting For The IphoneDocument9 pagesAccounting For The IphoneFatihahZainalLim100% (1)

- Stanley Black & Decker IncDocument6 pagesStanley Black & Decker IncNitesh RajNo ratings yet

- Sealed Air CorporationDocument4 pagesSealed Air CorporationValdemar Miguel SilvaNo ratings yet

- Case #7 Butler LumberDocument2 pagesCase #7 Butler LumberBianca UcheNo ratings yet

- LinearDocument6 pagesLinearjackedup211No ratings yet

- New Heritage Doll Company Capital BudgetDocument5 pagesNew Heritage Doll Company Capital BudgetCarlosNo ratings yet

- Sec6 Group13 SimulationDocument5 pagesSec6 Group13 SimulationAvinashDeshpande1989100% (1)

- Sealed Air Corporation's Leveraged Recapitalization (A)Document7 pagesSealed Air Corporation's Leveraged Recapitalization (A)Jyoti GuptaNo ratings yet

- Eastboro Case Write Up For Presentation1Document4 pagesEastboro Case Write Up For Presentation1Paula Elaine ThorpeNo ratings yet

- Sealed Air CorporationDocument7 pagesSealed Air CorporationMeenal MalhotraNo ratings yet

- Case Nike - Cost of Capital Fix 1Document9 pagesCase Nike - Cost of Capital Fix 1Yousania RatuNo ratings yet

- How Does The Internal Market For Innovation at Nypro FunctionDocument2 pagesHow Does The Internal Market For Innovation at Nypro Functionprerna004No ratings yet

- Linear Technology Payout Policy Case 3Document4 pagesLinear Technology Payout Policy Case 3Amrinder SinghNo ratings yet

- FM Project Archroma FinalDocument10 pagesFM Project Archroma FinalRameen Nadeem IqbalNo ratings yet

- Star RiverDocument8 pagesStar Riverjack stauberNo ratings yet

- Deconstructing Roe: Improving Efficiency An Important Parameter While Investing in CompaniesDocument5 pagesDeconstructing Roe: Improving Efficiency An Important Parameter While Investing in CompaniesAkshit GuptaNo ratings yet

- Turn Around Strategy For Avon ProductsDocument10 pagesTurn Around Strategy For Avon ProductsEmmanuel Kibaya OmbiroNo ratings yet

- Gainesboro CaseDocument16 pagesGainesboro Caseapi-402685925No ratings yet

- Financial Performance Evaluation Using RATIO ANALYSISDocument31 pagesFinancial Performance Evaluation Using RATIO ANALYSISGurvinder Arora100% (1)

- Final Project On Engro FinalDocument27 pagesFinal Project On Engro FinalKamran GulNo ratings yet

- Flash Memory IncDocument3 pagesFlash Memory IncAhsan IqbalNo ratings yet

- Fin201 Final Assignment ReportDocument13 pagesFin201 Final Assignment ReportAasif26No ratings yet

- Tata Motors Ratio AnalysisDocument12 pagesTata Motors Ratio AnalysisVasu AgarwalNo ratings yet

- Salesforce Fy 2023 Annual ReportDocument132 pagesSalesforce Fy 2023 Annual ReportsergioNo ratings yet

- Monzon, Jessa Marie M. Law 3E Special ProceedingsDocument4 pagesMonzon, Jessa Marie M. Law 3E Special ProceedingsRonna Faith MonzonNo ratings yet

- Assignment 4.2 Accounting For Income TaxDocument2 pagesAssignment 4.2 Accounting For Income TaxMon RamNo ratings yet

- MujiDocument5 pagesMujiHương PhanNo ratings yet

- Who Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)Document294 pagesWho Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)dev guptaNo ratings yet

- Kaizen 5W 1H PDFDocument20 pagesKaizen 5W 1H PDFSUBA NANTINI A/P M.SUBRAMANIAMNo ratings yet

- Inferno Flipkart MarketingReportDocument21 pagesInferno Flipkart MarketingReportRaghav BanthiaNo ratings yet

- Web Class8Document19 pagesWeb Class8Christos MaiNo ratings yet

- Furniture Brochure 2021Document8 pagesFurniture Brochure 2021Haider QadriNo ratings yet

- Development of Capital Markets in ZambiaDocument9 pagesDevelopment of Capital Markets in ZambiaBernard SimwanzaNo ratings yet

- Project Investment Appraisal Process PDFDocument24 pagesProject Investment Appraisal Process PDFsowra vsahaNo ratings yet

- Chap006-Intercompany Transfers of Services and Non Current AssetsDocument41 pagesChap006-Intercompany Transfers of Services and Non Current Assets_casals100% (4)

- Australian Super BrochureDocument4 pagesAustralian Super Brochurehail capiralNo ratings yet

- Unit 8. English Daily Test For Grade 5Document3 pagesUnit 8. English Daily Test For Grade 5NINGSIHNo ratings yet

- Safe OP - Working Machinery On Slopes: General Safety Rules and GuidanceDocument2 pagesSafe OP - Working Machinery On Slopes: General Safety Rules and Guidanceminov minovitchNo ratings yet

- Chap 5 - Contract PerformanceDocument35 pagesChap 5 - Contract PerformancePhương TrươngNo ratings yet

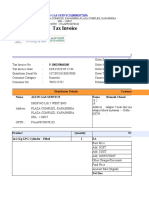

- Tax Invoice: JATIN GAS SERVICE (0000107209)Document4 pagesTax Invoice: JATIN GAS SERVICE (0000107209)RiseNo ratings yet

- Portugal Real Estate Market Research - 19 AprilDocument5 pagesPortugal Real Estate Market Research - 19 AprilTamNo ratings yet

- Handout CHE F343Document3 pagesHandout CHE F343Aryan ShuklaNo ratings yet

- Business Proposal Nutela Cupcake: The Fisher Valley College Taguig CityDocument26 pagesBusiness Proposal Nutela Cupcake: The Fisher Valley College Taguig CityMarlon RaquelNo ratings yet

- 5a - FreddyDocument29 pages5a - Freddyaliona.simon.ousviatsevNo ratings yet

- Basics of Accounting: By: Dr. Bhupendra Singh HadaDocument84 pagesBasics of Accounting: By: Dr. Bhupendra Singh HadaAryanSinghNo ratings yet

- Om FinalDocument37 pagesOm FinalAkliluNo ratings yet

- Black Book AjayDocument59 pagesBlack Book AjayMarshall CountyNo ratings yet

- Chapter 6 - Principles Products Services of IFDocument54 pagesChapter 6 - Principles Products Services of IFYaaga DharsiniNo ratings yet

- Increasing Productivity Through Implementation of 5S Methodology in A Manufacturing Industry: A Case StudyDocument7 pagesIncreasing Productivity Through Implementation of 5S Methodology in A Manufacturing Industry: A Case StudyGCOERC TEAM 5SNo ratings yet

- BQ Prime-RBI - S - Restrictions - On - Deferred - Consideration - Ready - For - Covid - 19Document8 pagesBQ Prime-RBI - S - Restrictions - On - Deferred - Consideration - Ready - For - Covid - 19Aryan StarkNo ratings yet

- Business Model Canvas Key Partners Key Activities Value Propositions Customer Relationships Customer SegmentsDocument2 pagesBusiness Model Canvas Key Partners Key Activities Value Propositions Customer Relationships Customer SegmentsLuqman SyahbudinNo ratings yet

- RI Annexure Editable-1Document6 pagesRI Annexure Editable-1pranay jambhaleNo ratings yet

- Project Final Submission (Ajith)Document136 pagesProject Final Submission (Ajith)Amal SunnyNo ratings yet