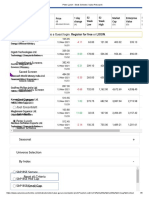

Jay Ushin Limited: Rationale-Press Release

Jay Ushin Limited: Rationale-Press Release

You might also like

- Jeizel Concepcion PR 4-1 To 4-5Document7 pagesJeizel Concepcion PR 4-1 To 4-5Concepcion Family100% (2)

- IOL Chemicals and Pharmaceuticals Limited-07-07-2020Document4 pagesIOL Chemicals and Pharmaceuticals Limited-07-07-2020Jeet SinghNo ratings yet

- Technico Industries LimitedDocument4 pagesTechnico Industries Limitedshankarravi8975No ratings yet

- Press Release Tab India Granites Private LimitedDocument6 pagesPress Release Tab India Granites Private LimitedRavi BabuNo ratings yet

- Super Spinning Mills Limited-09-08-2020Document4 pagesSuper Spinning Mills Limited-09-08-2020Positive ThinkerNo ratings yet

- Ginni Filaments Limited-09!07!2020Document4 pagesGinni Filaments Limited-09!07!2020Saurabh AgarwalNo ratings yet

- Shaily Engineering Plastics Limited-09-25-2019Document4 pagesShaily Engineering Plastics Limited-09-25-2019Ashutosh Gupta100% (1)

- Roots Industries India Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionDocument4 pagesRoots Industries India Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionKarthikeyan RK SwamyNo ratings yet

- PSK Engineering Construction & Co-08-06-2020Document5 pagesPSK Engineering Construction & Co-08-06-2020The JdNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Vinati Organics Limited CARE Rating July 2017Document5 pagesVinati Organics Limited CARE Rating July 2017mgrreddyNo ratings yet

- Akar Auto Industries LimitedDocument5 pagesAkar Auto Industries Limitedkrushna.maneNo ratings yet

- Press Release Vijay Sales (India) Private Limited: Experienced PromotersDocument4 pagesPress Release Vijay Sales (India) Private Limited: Experienced PromoterssriharikosaNo ratings yet

- Emcer Tiles Private LimitedDocument4 pagesEmcer Tiles Private LimitedRudra RoyNo ratings yet

- Filatex India Limited PDFDocument6 pagesFilatex India Limited PDFfatNo ratings yet

- Oriental Rubber Industries Pvt. LTDDocument7 pagesOriental Rubber Industries Pvt. LTDPriya VijiNo ratings yet

- Sunlex Fabrics Private Limited - Care RatingsDocument6 pagesSunlex Fabrics Private Limited - Care RatingsManeet GoyalNo ratings yet

- Prayag Polymers Private LimitedDocument4 pagesPrayag Polymers Private Limitednandinimishra6168No ratings yet

- JCBL India Private LimitedDocument6 pagesJCBL India Private LimitedRAMODSNo ratings yet

- Press Release Jash Engineering LTD.: Details of Instruments/ Facilities in Annexure-1Document6 pagesPress Release Jash Engineering LTD.: Details of Instruments/ Facilities in Annexure-1ArunVenkatachalamNo ratings yet

- Globe Automobiles Private LimitedDocument7 pagesGlobe Automobiles Private LimitedRAMODSNo ratings yet

- Mega Steel IndustriesDocument4 pagesMega Steel IndustrieshseckalpeshNo ratings yet

- Press Release Panoli Intermediates (India) Private Limited: Details of Instruments/ Facilities in Annexure-1Document6 pagesPress Release Panoli Intermediates (India) Private Limited: Details of Instruments/ Facilities in Annexure-1Patel ZeelNo ratings yet

- Pan Healthcare Private Limited (PHCPL) October 12, 2020Document5 pagesPan Healthcare Private Limited (PHCPL) October 12, 2020Sachin DhorajiyaNo ratings yet

- Milestone Gears Private Limited-03-09-2020Document4 pagesMilestone Gears Private Limited-03-09-2020Puneet367No ratings yet

- Press Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1flying400No ratings yet

- Ramani Cars Private Limited 2023Document6 pagesRamani Cars Private Limited 2023Karthikeyan RK SwamyNo ratings yet

- Kanchan Oil Industries LimitedDocument4 pagesKanchan Oil Industries LimitedSam FireNo ratings yet

- Press Release: R B Construction CompanyDocument4 pagesPress Release: R B Construction CompanyRavi BabuNo ratings yet

- AETHER Industries LTD - 2020 Credit RatingDocument5 pagesAETHER Industries LTD - 2020 Credit RatingEast West Strategic ConsultingNo ratings yet

- PR ARCL Organics 31jan22Document7 pagesPR ARCL Organics 31jan22anady135344No ratings yet

- IOL Chemicals and Pharmaceuticals Limited-07!02!2019Document4 pagesIOL Chemicals and Pharmaceuticals Limited-07!02!2019Technical dostNo ratings yet

- Mamta Transformers-R-19102020Document7 pagesMamta Transformers-R-19102020DarshanNo ratings yet

- Press Release Pennar Industries Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Pennar Industries Limited: Details of Instruments/facilities in Annexure-1Radha MohanNo ratings yet

- Epicenter Technologies Private - R - 11082020Document7 pagesEpicenter Technologies Private - R - 11082020Shawn BlazeNo ratings yet

- IIFL Home Finance LimitedDocument6 pagesIIFL Home Finance LimitedSumonto BagchiNo ratings yet

- Best Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionDocument5 pagesBest Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionKarthikeyan RK SwamyNo ratings yet

- Divis Laboratories LimitedDocument7 pagesDivis Laboratories Limiteddivygupta198No ratings yet

- Press Release Deccan Industries: Positive FactorsDocument4 pagesPress Release Deccan Industries: Positive FactorsHARI HARANNo ratings yet

- Press Release Nahar Poly Films LimitedDocument5 pagesPress Release Nahar Poly Films LimitedHarshit SinghNo ratings yet

- Bharat Forge LimitedDocument7 pagesBharat Forge LimitedjagadeeshNo ratings yet

- Press Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionDocument4 pagesPress Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionData CentrumNo ratings yet

- Signode India Financial ReportDocument5 pagesSignode India Financial Reportsaikiran reddyNo ratings yet

- Ganesh Benzoplast LTD (GBL)Document7 pagesGanesh Benzoplast LTD (GBL)Positive ThinkerNo ratings yet

- Myra Hygiene Products Private LimitedDocument7 pagesMyra Hygiene Products Private Limitedanuj7729No ratings yet

- Prime Urban ICRA April 17Document7 pagesPrime Urban ICRA April 17BALMERNo ratings yet

- Care Rating Sterling - Addlife - India - Private - LimitedDocument6 pagesCare Rating Sterling - Addlife - India - Private - Limitedrahul.tibrewalNo ratings yet

- 3F Oil Palm Agrotech Private Limited-02-27-2020 PDFDocument4 pages3F Oil Palm Agrotech Private Limited-02-27-2020 PDFData CentrumNo ratings yet

- Airvision India Private Limited - R - 25082020Document7 pagesAirvision India Private Limited - R - 25082020DarshanNo ratings yet

- Press Release RACL Geartech LTDDocument4 pagesPress Release RACL Geartech LTDSourav DuttaNo ratings yet

- Drools Pet Food Private LimitedDocument6 pagesDrools Pet Food Private Limitedkasimmalnas.ipsNo ratings yet

- La Opala RG LimitedDocument5 pagesLa Opala RG LimitedAshwani KesharwaniNo ratings yet

- Jupiter International LimitedDocument6 pagesJupiter International LimitedRahul syalNo ratings yet

- Press Release Fortune Stones Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Fortune Stones Limited: Details of Instruments/facilities in Annexure-1Ravi BabuNo ratings yet

- Drools Pet Food Private LimitedDocument7 pagesDrools Pet Food Private LimitedramlamacadNo ratings yet

- Press Release Gravita India Limited: Ratings Facilities Amount (Rs. Crore) Ratings Rating ActionDocument7 pagesPress Release Gravita India Limited: Ratings Facilities Amount (Rs. Crore) Ratings Rating ActionhamsNo ratings yet

- Bharat Hotels LimitedDocument7 pagesBharat Hotels LimitedjagadeeshNo ratings yet

- Press Release Amkette Analytics Limited: Details of Instruments/facilities in Annexure-1Document5 pagesPress Release Amkette Analytics Limited: Details of Instruments/facilities in Annexure-1Data CentrumNo ratings yet

- Credit Union Revenues World Summary: Market Values & Financials by CountryFrom EverandCredit Union Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- Aim Paste Handling Guideline Revnf1Document2 pagesAim Paste Handling Guideline Revnf1ravi.youNo ratings yet

- 21 Average True RangeDocument95 pages21 Average True Rangeravi.youNo ratings yet

- Rework Procedure For Your Medical Device - GMP TrendsDocument3 pagesRework Procedure For Your Medical Device - GMP Trendsravi.youNo ratings yet

- Oriental AromatDocument37 pagesOriental Aromatravi.youNo ratings yet

- AlembicDocument37 pagesAlembicravi.youNo ratings yet

- 15 Minute Stock Breakouts, Technical Analysis ScannerDocument8 pages15 Minute Stock Breakouts, Technical Analysis Scannerravi.youNo ratings yet

- Ijprse V1i4 13Document9 pagesIjprse V1i4 13ravi.youNo ratings yet

- Goot CatalogDocument84 pagesGoot Catalogravi.youNo ratings yet

- Power Domiled Alingap DWX-MKG - V7Document16 pagesPower Domiled Alingap DWX-MKG - V7ravi.youNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetravi.youNo ratings yet

- 28 TH Annual Report 2019-20: Manufacturer and ExporterDocument197 pages28 TH Annual Report 2019-20: Manufacturer and Exporterravi.youNo ratings yet

- Heritage FoodsDocument37 pagesHeritage Foodsravi.youNo ratings yet

- New CV Mech MahendraDocument2 pagesNew CV Mech Mahendraravi.youNo ratings yet

- Management Discussion and Analysis: Global Economic Scenario & Outlook A) Macro-Economic ConditionsDocument3 pagesManagement Discussion and Analysis: Global Economic Scenario & Outlook A) Macro-Economic Conditionsravi.youNo ratings yet

- Sector - Industry ( ) DD MMM HH:MM (%) (CR) (CR) Sector - IndustryDocument5 pagesSector - Industry ( ) DD MMM HH:MM (%) (CR) (CR) Sector - Industryravi.youNo ratings yet

- BSE Limited National Stock Exchange of India Limited: Patel Bijal RamjibhaiDocument17 pagesBSE Limited National Stock Exchange of India Limited: Patel Bijal Ramjibhairavi.youNo ratings yet

- 20189616154angel Broking DRHPDocument349 pages20189616154angel Broking DRHPravi.youNo ratings yet

- Apcotex Industries LimitedDocument129 pagesApcotex Industries Limitedravi.youNo ratings yet

- Kirl. FerrousDocument37 pagesKirl. Ferrousravi.youNo ratings yet

- Fertilizernagar-391 750. Vadodara, Gujarat, INDIA. CIN: L99999GJ1962PLC001121Document217 pagesFertilizernagar-391 750. Vadodara, Gujarat, INDIA. CIN: L99999GJ1962PLC001121ravi.youNo ratings yet

- BSE Limited. Phiroze Jeejeebhoy Towers, Mumbai - 400 001Document20 pagesBSE Limited. Phiroze Jeejeebhoy Towers, Mumbai - 400 001ravi.youNo ratings yet

- Investor Presentation - Q2FY2018-19 KiriDocument25 pagesInvestor Presentation - Q2FY2018-19 Kiriravi.youNo ratings yet

- AE Corporate Profile Latest DEC 2017 1Document37 pagesAE Corporate Profile Latest DEC 2017 1ravi.youNo ratings yet

- AccelyaDocument217 pagesAccelyaravi.youNo ratings yet

- GNFCDocument249 pagesGNFCravi.youNo ratings yet

- Racl Gear TechDocument10 pagesRacl Gear Techravi.youNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetravi.youNo ratings yet

- Contract Law 3rd SemDocument16 pagesContract Law 3rd SemAsthaNo ratings yet

- CH 5 - DepositsDocument19 pagesCH 5 - DepositsPrashant ChandaneNo ratings yet

- Picnic Shelter RentalDocument6 pagesPicnic Shelter RentalTony ParkNo ratings yet

- Chapter 9-Rules Governing AcceptanceDocument6 pagesChapter 9-Rules Governing AcceptanceAngelica Joy ManaoisNo ratings yet

- 2017 ACCF111 Semester TestDocument5 pages2017 ACCF111 Semester TestLucas LuluNo ratings yet

- Debt Restructuring Problem 1 (Asset Swap/Dacion en Pago)Document3 pagesDebt Restructuring Problem 1 (Asset Swap/Dacion en Pago)Trice DomingoNo ratings yet

- Afar302 A - PF 1Document4 pagesAfar302 A - PF 1Nicole TeruelNo ratings yet

- HI6026 Final Assessment T3 2021Document11 pagesHI6026 Final Assessment T3 2021adityapatnaik.022No ratings yet

- Case CommentaryDocument7 pagesCase CommentaryHritik KashyapNo ratings yet

- Glossary of Financial Banking TermsDocument3 pagesGlossary of Financial Banking TermsbitocasNo ratings yet

- Balance SheetDocument2 pagesBalance SheetShubham TiwariNo ratings yet

- HDFC Bank LTDDocument2 pagesHDFC Bank LTDKrishna Prasad KanchojuNo ratings yet

- Commodatum ContractDocument3 pagesCommodatum ContractLaura Daniela Restrepo MolinaNo ratings yet

- DISCUSSION ON RECONCILATION AND ERRORS - PrintDocument6 pagesDISCUSSION ON RECONCILATION AND ERRORS - PrintHuyền TrangNo ratings yet

- Tsiyon Sintayehu FinalDocument43 pagesTsiyon Sintayehu Finalsimon solomonNo ratings yet

- Statement of Fees - LT713570010000045404Document3 pagesStatement of Fees - LT713570010000045404Eimantas SipaviciusNo ratings yet

- Dacion en Pago Set 2 - Sales Case DigestDocument9 pagesDacion en Pago Set 2 - Sales Case DigestAbigail TolabingNo ratings yet

- 13 Comm 308 Final Exam (Summer 1, 2012) SolutionsDocument17 pages13 Comm 308 Final Exam (Summer 1, 2012) SolutionsAfafe ElNo ratings yet

- Balance Sheet TemplateDocument8 pagesBalance Sheet TemplateJerarudo BoknoyNo ratings yet

- Before Merger Announced Merger in 2017 Completes Merger in 2019 Approved by Dot in 2020Document3 pagesBefore Merger Announced Merger in 2017 Completes Merger in 2019 Approved by Dot in 2020Sourabh SinghNo ratings yet

- Solved James Smithern Has Asked For A 3 500 Loan From BeardDocument1 pageSolved James Smithern Has Asked For A 3 500 Loan From BeardM Bilal SaleemNo ratings yet

- AccountingDocument26 pagesAccountingMuhammad Jaafar AbinalNo ratings yet

- Poa Revision - Book of Original Entry CSEC REVISIONDocument4 pagesPoa Revision - Book of Original Entry CSEC REVISIONnikeiraawer1No ratings yet

- Chapter 7 - Promissory NotesDocument7 pagesChapter 7 - Promissory NotesIzny KamaliyahNo ratings yet

- Alexander Ramos 211 Wymount Ter BLDG. 4C APT. 211 PROVO, UT 84604-1937 Selecthealth PO BOX 3674 SEATTLE, WA 98124-3674Document2 pagesAlexander Ramos 211 Wymount Ter BLDG. 4C APT. 211 PROVO, UT 84604-1937 Selecthealth PO BOX 3674 SEATTLE, WA 98124-3674alexander ramosNo ratings yet

- BAF3M - Uint 4 Trial Balance 2023Document7 pagesBAF3M - Uint 4 Trial Balance 2023narayanansri2007No ratings yet

- Chapter 8 - Part ADocument22 pagesChapter 8 - Part AKwan Kwok AsNo ratings yet

- Ratio Analysis. Corporate FinanceDocument46 pagesRatio Analysis. Corporate FinanceRadwa MohammedNo ratings yet

- Desrosiers LTD Had The Following Long Term Receivable Account Balances at PDFDocument2 pagesDesrosiers LTD Had The Following Long Term Receivable Account Balances at PDFTaimur TechnologistNo ratings yet

Download as pdf or txt

You might also like

- Jeizel Concepcion PR 4-1 To 4-5Document7 pagesJeizel Concepcion PR 4-1 To 4-5Concepcion Family100% (2)

- IOL Chemicals and Pharmaceuticals Limited-07-07-2020Document4 pagesIOL Chemicals and Pharmaceuticals Limited-07-07-2020Jeet SinghNo ratings yet

- Technico Industries LimitedDocument4 pagesTechnico Industries Limitedshankarravi8975No ratings yet

- Press Release Tab India Granites Private LimitedDocument6 pagesPress Release Tab India Granites Private LimitedRavi BabuNo ratings yet

- Super Spinning Mills Limited-09-08-2020Document4 pagesSuper Spinning Mills Limited-09-08-2020Positive ThinkerNo ratings yet

- Ginni Filaments Limited-09!07!2020Document4 pagesGinni Filaments Limited-09!07!2020Saurabh AgarwalNo ratings yet

- Shaily Engineering Plastics Limited-09-25-2019Document4 pagesShaily Engineering Plastics Limited-09-25-2019Ashutosh Gupta100% (1)

- Roots Industries India Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionDocument4 pagesRoots Industries India Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionKarthikeyan RK SwamyNo ratings yet

- PSK Engineering Construction & Co-08-06-2020Document5 pagesPSK Engineering Construction & Co-08-06-2020The JdNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Vinati Organics Limited CARE Rating July 2017Document5 pagesVinati Organics Limited CARE Rating July 2017mgrreddyNo ratings yet

- Akar Auto Industries LimitedDocument5 pagesAkar Auto Industries Limitedkrushna.maneNo ratings yet

- Press Release Vijay Sales (India) Private Limited: Experienced PromotersDocument4 pagesPress Release Vijay Sales (India) Private Limited: Experienced PromoterssriharikosaNo ratings yet

- Emcer Tiles Private LimitedDocument4 pagesEmcer Tiles Private LimitedRudra RoyNo ratings yet

- Filatex India Limited PDFDocument6 pagesFilatex India Limited PDFfatNo ratings yet

- Oriental Rubber Industries Pvt. LTDDocument7 pagesOriental Rubber Industries Pvt. LTDPriya VijiNo ratings yet

- Sunlex Fabrics Private Limited - Care RatingsDocument6 pagesSunlex Fabrics Private Limited - Care RatingsManeet GoyalNo ratings yet

- Prayag Polymers Private LimitedDocument4 pagesPrayag Polymers Private Limitednandinimishra6168No ratings yet

- JCBL India Private LimitedDocument6 pagesJCBL India Private LimitedRAMODSNo ratings yet

- Press Release Jash Engineering LTD.: Details of Instruments/ Facilities in Annexure-1Document6 pagesPress Release Jash Engineering LTD.: Details of Instruments/ Facilities in Annexure-1ArunVenkatachalamNo ratings yet

- Globe Automobiles Private LimitedDocument7 pagesGlobe Automobiles Private LimitedRAMODSNo ratings yet

- Mega Steel IndustriesDocument4 pagesMega Steel IndustrieshseckalpeshNo ratings yet

- Press Release Panoli Intermediates (India) Private Limited: Details of Instruments/ Facilities in Annexure-1Document6 pagesPress Release Panoli Intermediates (India) Private Limited: Details of Instruments/ Facilities in Annexure-1Patel ZeelNo ratings yet

- Pan Healthcare Private Limited (PHCPL) October 12, 2020Document5 pagesPan Healthcare Private Limited (PHCPL) October 12, 2020Sachin DhorajiyaNo ratings yet

- Milestone Gears Private Limited-03-09-2020Document4 pagesMilestone Gears Private Limited-03-09-2020Puneet367No ratings yet

- Press Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Airo Lam Limited: Details of Instruments/facilities in Annexure-1flying400No ratings yet

- Ramani Cars Private Limited 2023Document6 pagesRamani Cars Private Limited 2023Karthikeyan RK SwamyNo ratings yet

- Kanchan Oil Industries LimitedDocument4 pagesKanchan Oil Industries LimitedSam FireNo ratings yet

- Press Release: R B Construction CompanyDocument4 pagesPress Release: R B Construction CompanyRavi BabuNo ratings yet

- AETHER Industries LTD - 2020 Credit RatingDocument5 pagesAETHER Industries LTD - 2020 Credit RatingEast West Strategic ConsultingNo ratings yet

- PR ARCL Organics 31jan22Document7 pagesPR ARCL Organics 31jan22anady135344No ratings yet

- IOL Chemicals and Pharmaceuticals Limited-07!02!2019Document4 pagesIOL Chemicals and Pharmaceuticals Limited-07!02!2019Technical dostNo ratings yet

- Mamta Transformers-R-19102020Document7 pagesMamta Transformers-R-19102020DarshanNo ratings yet

- Press Release Pennar Industries Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Pennar Industries Limited: Details of Instruments/facilities in Annexure-1Radha MohanNo ratings yet

- Epicenter Technologies Private - R - 11082020Document7 pagesEpicenter Technologies Private - R - 11082020Shawn BlazeNo ratings yet

- IIFL Home Finance LimitedDocument6 pagesIIFL Home Finance LimitedSumonto BagchiNo ratings yet

- Best Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionDocument5 pagesBest Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionKarthikeyan RK SwamyNo ratings yet

- Divis Laboratories LimitedDocument7 pagesDivis Laboratories Limiteddivygupta198No ratings yet

- Press Release Deccan Industries: Positive FactorsDocument4 pagesPress Release Deccan Industries: Positive FactorsHARI HARANNo ratings yet

- Press Release Nahar Poly Films LimitedDocument5 pagesPress Release Nahar Poly Films LimitedHarshit SinghNo ratings yet

- Bharat Forge LimitedDocument7 pagesBharat Forge LimitedjagadeeshNo ratings yet

- Press Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionDocument4 pagesPress Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionData CentrumNo ratings yet

- Signode India Financial ReportDocument5 pagesSignode India Financial Reportsaikiran reddyNo ratings yet

- Ganesh Benzoplast LTD (GBL)Document7 pagesGanesh Benzoplast LTD (GBL)Positive ThinkerNo ratings yet

- Myra Hygiene Products Private LimitedDocument7 pagesMyra Hygiene Products Private Limitedanuj7729No ratings yet

- Prime Urban ICRA April 17Document7 pagesPrime Urban ICRA April 17BALMERNo ratings yet

- Care Rating Sterling - Addlife - India - Private - LimitedDocument6 pagesCare Rating Sterling - Addlife - India - Private - Limitedrahul.tibrewalNo ratings yet

- 3F Oil Palm Agrotech Private Limited-02-27-2020 PDFDocument4 pages3F Oil Palm Agrotech Private Limited-02-27-2020 PDFData CentrumNo ratings yet

- Airvision India Private Limited - R - 25082020Document7 pagesAirvision India Private Limited - R - 25082020DarshanNo ratings yet

- Press Release RACL Geartech LTDDocument4 pagesPress Release RACL Geartech LTDSourav DuttaNo ratings yet

- Drools Pet Food Private LimitedDocument6 pagesDrools Pet Food Private Limitedkasimmalnas.ipsNo ratings yet

- La Opala RG LimitedDocument5 pagesLa Opala RG LimitedAshwani KesharwaniNo ratings yet

- Jupiter International LimitedDocument6 pagesJupiter International LimitedRahul syalNo ratings yet

- Press Release Fortune Stones Limited: Details of Instruments/facilities in Annexure-1Document4 pagesPress Release Fortune Stones Limited: Details of Instruments/facilities in Annexure-1Ravi BabuNo ratings yet

- Drools Pet Food Private LimitedDocument7 pagesDrools Pet Food Private LimitedramlamacadNo ratings yet

- Press Release Gravita India Limited: Ratings Facilities Amount (Rs. Crore) Ratings Rating ActionDocument7 pagesPress Release Gravita India Limited: Ratings Facilities Amount (Rs. Crore) Ratings Rating ActionhamsNo ratings yet

- Bharat Hotels LimitedDocument7 pagesBharat Hotels LimitedjagadeeshNo ratings yet

- Press Release Amkette Analytics Limited: Details of Instruments/facilities in Annexure-1Document5 pagesPress Release Amkette Analytics Limited: Details of Instruments/facilities in Annexure-1Data CentrumNo ratings yet

- Credit Union Revenues World Summary: Market Values & Financials by CountryFrom EverandCredit Union Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- Aim Paste Handling Guideline Revnf1Document2 pagesAim Paste Handling Guideline Revnf1ravi.youNo ratings yet

- 21 Average True RangeDocument95 pages21 Average True Rangeravi.youNo ratings yet

- Rework Procedure For Your Medical Device - GMP TrendsDocument3 pagesRework Procedure For Your Medical Device - GMP Trendsravi.youNo ratings yet

- Oriental AromatDocument37 pagesOriental Aromatravi.youNo ratings yet

- AlembicDocument37 pagesAlembicravi.youNo ratings yet

- 15 Minute Stock Breakouts, Technical Analysis ScannerDocument8 pages15 Minute Stock Breakouts, Technical Analysis Scannerravi.youNo ratings yet

- Ijprse V1i4 13Document9 pagesIjprse V1i4 13ravi.youNo ratings yet

- Goot CatalogDocument84 pagesGoot Catalogravi.youNo ratings yet

- Power Domiled Alingap DWX-MKG - V7Document16 pagesPower Domiled Alingap DWX-MKG - V7ravi.youNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetravi.youNo ratings yet

- 28 TH Annual Report 2019-20: Manufacturer and ExporterDocument197 pages28 TH Annual Report 2019-20: Manufacturer and Exporterravi.youNo ratings yet

- Heritage FoodsDocument37 pagesHeritage Foodsravi.youNo ratings yet

- New CV Mech MahendraDocument2 pagesNew CV Mech Mahendraravi.youNo ratings yet

- Management Discussion and Analysis: Global Economic Scenario & Outlook A) Macro-Economic ConditionsDocument3 pagesManagement Discussion and Analysis: Global Economic Scenario & Outlook A) Macro-Economic Conditionsravi.youNo ratings yet

- Sector - Industry ( ) DD MMM HH:MM (%) (CR) (CR) Sector - IndustryDocument5 pagesSector - Industry ( ) DD MMM HH:MM (%) (CR) (CR) Sector - Industryravi.youNo ratings yet

- BSE Limited National Stock Exchange of India Limited: Patel Bijal RamjibhaiDocument17 pagesBSE Limited National Stock Exchange of India Limited: Patel Bijal Ramjibhairavi.youNo ratings yet

- 20189616154angel Broking DRHPDocument349 pages20189616154angel Broking DRHPravi.youNo ratings yet

- Apcotex Industries LimitedDocument129 pagesApcotex Industries Limitedravi.youNo ratings yet

- Kirl. FerrousDocument37 pagesKirl. Ferrousravi.youNo ratings yet

- Fertilizernagar-391 750. Vadodara, Gujarat, INDIA. CIN: L99999GJ1962PLC001121Document217 pagesFertilizernagar-391 750. Vadodara, Gujarat, INDIA. CIN: L99999GJ1962PLC001121ravi.youNo ratings yet

- BSE Limited. Phiroze Jeejeebhoy Towers, Mumbai - 400 001Document20 pagesBSE Limited. Phiroze Jeejeebhoy Towers, Mumbai - 400 001ravi.youNo ratings yet

- Investor Presentation - Q2FY2018-19 KiriDocument25 pagesInvestor Presentation - Q2FY2018-19 Kiriravi.youNo ratings yet

- AE Corporate Profile Latest DEC 2017 1Document37 pagesAE Corporate Profile Latest DEC 2017 1ravi.youNo ratings yet

- AccelyaDocument217 pagesAccelyaravi.youNo ratings yet

- GNFCDocument249 pagesGNFCravi.youNo ratings yet

- Racl Gear TechDocument10 pagesRacl Gear Techravi.youNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetravi.youNo ratings yet

- Contract Law 3rd SemDocument16 pagesContract Law 3rd SemAsthaNo ratings yet

- CH 5 - DepositsDocument19 pagesCH 5 - DepositsPrashant ChandaneNo ratings yet

- Picnic Shelter RentalDocument6 pagesPicnic Shelter RentalTony ParkNo ratings yet

- Chapter 9-Rules Governing AcceptanceDocument6 pagesChapter 9-Rules Governing AcceptanceAngelica Joy ManaoisNo ratings yet

- 2017 ACCF111 Semester TestDocument5 pages2017 ACCF111 Semester TestLucas LuluNo ratings yet

- Debt Restructuring Problem 1 (Asset Swap/Dacion en Pago)Document3 pagesDebt Restructuring Problem 1 (Asset Swap/Dacion en Pago)Trice DomingoNo ratings yet

- Afar302 A - PF 1Document4 pagesAfar302 A - PF 1Nicole TeruelNo ratings yet

- HI6026 Final Assessment T3 2021Document11 pagesHI6026 Final Assessment T3 2021adityapatnaik.022No ratings yet

- Case CommentaryDocument7 pagesCase CommentaryHritik KashyapNo ratings yet

- Glossary of Financial Banking TermsDocument3 pagesGlossary of Financial Banking TermsbitocasNo ratings yet

- Balance SheetDocument2 pagesBalance SheetShubham TiwariNo ratings yet

- HDFC Bank LTDDocument2 pagesHDFC Bank LTDKrishna Prasad KanchojuNo ratings yet

- Commodatum ContractDocument3 pagesCommodatum ContractLaura Daniela Restrepo MolinaNo ratings yet

- DISCUSSION ON RECONCILATION AND ERRORS - PrintDocument6 pagesDISCUSSION ON RECONCILATION AND ERRORS - PrintHuyền TrangNo ratings yet

- Tsiyon Sintayehu FinalDocument43 pagesTsiyon Sintayehu Finalsimon solomonNo ratings yet

- Statement of Fees - LT713570010000045404Document3 pagesStatement of Fees - LT713570010000045404Eimantas SipaviciusNo ratings yet

- Dacion en Pago Set 2 - Sales Case DigestDocument9 pagesDacion en Pago Set 2 - Sales Case DigestAbigail TolabingNo ratings yet

- 13 Comm 308 Final Exam (Summer 1, 2012) SolutionsDocument17 pages13 Comm 308 Final Exam (Summer 1, 2012) SolutionsAfafe ElNo ratings yet

- Balance Sheet TemplateDocument8 pagesBalance Sheet TemplateJerarudo BoknoyNo ratings yet

- Before Merger Announced Merger in 2017 Completes Merger in 2019 Approved by Dot in 2020Document3 pagesBefore Merger Announced Merger in 2017 Completes Merger in 2019 Approved by Dot in 2020Sourabh SinghNo ratings yet

- Solved James Smithern Has Asked For A 3 500 Loan From BeardDocument1 pageSolved James Smithern Has Asked For A 3 500 Loan From BeardM Bilal SaleemNo ratings yet

- AccountingDocument26 pagesAccountingMuhammad Jaafar AbinalNo ratings yet

- Poa Revision - Book of Original Entry CSEC REVISIONDocument4 pagesPoa Revision - Book of Original Entry CSEC REVISIONnikeiraawer1No ratings yet

- Chapter 7 - Promissory NotesDocument7 pagesChapter 7 - Promissory NotesIzny KamaliyahNo ratings yet

- Alexander Ramos 211 Wymount Ter BLDG. 4C APT. 211 PROVO, UT 84604-1937 Selecthealth PO BOX 3674 SEATTLE, WA 98124-3674Document2 pagesAlexander Ramos 211 Wymount Ter BLDG. 4C APT. 211 PROVO, UT 84604-1937 Selecthealth PO BOX 3674 SEATTLE, WA 98124-3674alexander ramosNo ratings yet

- BAF3M - Uint 4 Trial Balance 2023Document7 pagesBAF3M - Uint 4 Trial Balance 2023narayanansri2007No ratings yet

- Chapter 8 - Part ADocument22 pagesChapter 8 - Part AKwan Kwok AsNo ratings yet

- Ratio Analysis. Corporate FinanceDocument46 pagesRatio Analysis. Corporate FinanceRadwa MohammedNo ratings yet

- Desrosiers LTD Had The Following Long Term Receivable Account Balances at PDFDocument2 pagesDesrosiers LTD Had The Following Long Term Receivable Account Balances at PDFTaimur TechnologistNo ratings yet