Download as pdf or txt

You might also like

- Eco 101 Lecture 1-3 IntroductionDocument10 pagesEco 101 Lecture 1-3 IntroductionSanaullah SiddiqueNo ratings yet

- Micro Econom I ADocument144 pagesMicro Econom I AJose David CeferinoNo ratings yet

- CH 2 Economic ActivitiesDocument16 pagesCH 2 Economic Activitiesshaheduzaman ShahedNo ratings yet

- CH 2 - Economic Activities of Production and TradeDocument15 pagesCH 2 - Economic Activities of Production and TradeSamiul TashbirNo ratings yet

- Economic Activities: Producing and TradingDocument19 pagesEconomic Activities: Producing and TradingMostafa haqueNo ratings yet

- 1 ST Sem EconomicsDocument260 pages1 ST Sem EconomicsM MalikNo ratings yet

- Opportunity Cost: MicroeconomicsDocument5 pagesOpportunity Cost: MicroeconomicsMd RifatNo ratings yet

- Apply Concepts of Production and TradeDocument7 pagesApply Concepts of Production and TradeDaniel ChiarelliNo ratings yet

- The Economic Problem: Chapter Key IdeasDocument7 pagesThe Economic Problem: Chapter Key IdeasTaqsim RajonNo ratings yet

- Lecture NotesDocument101 pagesLecture NotesTariq RahimNo ratings yet

- PA 103: Introduction To Microeconomics: Md. Roni Hossain Lecturer Department of Economics Jahangirnagar UniversityDocument33 pagesPA 103: Introduction To Microeconomics: Md. Roni Hossain Lecturer Department of Economics Jahangirnagar Universitymd jowel khanNo ratings yet

- What Is Economics About? Part OneDocument14 pagesWhat Is Economics About? Part Onesaqib razaNo ratings yet

- ECON 201: Principles of Microconomics I (Micro) : Text: Bradley R. Schiller, "The Economy Today"Document100 pagesECON 201: Principles of Microconomics I (Micro) : Text: Bradley R. Schiller, "The Economy Today"Marielle Aria SantosNo ratings yet

- (SN) II Principles of MicroeconomicsDocument108 pages(SN) II Principles of MicroeconomicsNarmeen RefaiNo ratings yet

- Economics Answers 2Document14 pagesEconomics Answers 2Rakawy Bin RakNo ratings yet

- A. Scarcity: The Nature of Economic Systems: Unit OneDocument25 pagesA. Scarcity: The Nature of Economic Systems: Unit OneShoniqua JohnsonNo ratings yet

- Introduction To Economics - ECO401: VU Lesson 02Document6 pagesIntroduction To Economics - ECO401: VU Lesson 02Susheel KumarNo ratings yet

- UntitledDocument3 pagesUntitledImranNo ratings yet

- T2 The Economic Problem SummaryDocument2 pagesT2 The Economic Problem SummaryCreselda A. De PaduaNo ratings yet

- Week 1 (Chapter 1)Document47 pagesWeek 1 (Chapter 1)Aleksandr KrasavcevNo ratings yet

- Topic 4Document46 pagesTopic 4974374542No ratings yet

- Assignment of Economy PolicyDocument3 pagesAssignment of Economy PolicyLovepreet malhiNo ratings yet

- Name - Eco200: Practice Test 3A Covering Chapters 16, 18-21Document6 pagesName - Eco200: Practice Test 3A Covering Chapters 16, 18-21Thiện ThảoNo ratings yet

- The Economic Problem PDFDocument16 pagesThe Economic Problem PDFKim LamsenNo ratings yet

- Final Exam ReviewDocument19 pagesFinal Exam ReviewJeromy Rech100% (1)

- HW2s Ric HO f11Document10 pagesHW2s Ric HO f11partha_biswas_uiuNo ratings yet

- Economics Assigment: (Type The Company Name) AcerDocument17 pagesEconomics Assigment: (Type The Company Name) AcerMonty WankharNo ratings yet

- Material ManagmentDocument88 pagesMaterial ManagmentFawa TubeNo ratings yet

- Micro Perfect CompetitionDocument9 pagesMicro Perfect CompetitionPriyadarshi BhaskarNo ratings yet

- The Economizing Problem: Scarcity and Choice: Chapter OutlineDocument3 pagesThe Economizing Problem: Scarcity and Choice: Chapter OutlineSyed005No ratings yet

- Amira Saaed Mohamed Mohamed - AAGSB - Economics - Final - Monday - 1G - December2022Document14 pagesAmira Saaed Mohamed Mohamed - AAGSB - Economics - Final - Monday - 1G - December2022Amira MohamedNo ratings yet

- Chapter 2, Comparative Advantage - The Basis For Exchange. DETAILED NOTESDocument11 pagesChapter 2, Comparative Advantage - The Basis For Exchange. DETAILED NOTESRuben JohnNo ratings yet

- Lecture 3Document61 pagesLecture 3Nikoli MajorNo ratings yet

- Downloadfile 1Document7 pagesDownloadfile 1Nayeema HaqueNo ratings yet

- Ecs ExampackDocument103 pagesEcs ExampackCharlize RileyNo ratings yet

- Chapter 05 Inputs & CostsDocument67 pagesChapter 05 Inputs & CostsMark EbrahimNo ratings yet

- ECON 312 Midterm ExamDocument8 pagesECON 312 Midterm ExamDeVryHelpNo ratings yet

- Economics Taxation and Agrarian ReformDocument87 pagesEconomics Taxation and Agrarian ReformKatrine ManaoNo ratings yet

- Economics - Intro - NotesDocument13 pagesEconomics - Intro - NotesAbdur RahmanNo ratings yet

- Production Possibilities and Opportunity CostsDocument9 pagesProduction Possibilities and Opportunity CostsHealthyYOU100% (3)

- Chapter 10 Study QuestionsDocument12 pagesChapter 10 Study QuestionsRasit M. NuriNo ratings yet

- Remedial Take-Home Exam For Introduction To EconomicsDocument2 pagesRemedial Take-Home Exam For Introduction To EconomicsAgZawNo ratings yet

- Economic Models: Trade-Offs and Trade: Krugman/Wells Krugman/Wells EconomicsDocument14 pagesEconomic Models: Trade-Offs and Trade: Krugman/Wells Krugman/Wells EconomicsCarlos VerasNo ratings yet

- Micro One Handout PDFDocument89 pagesMicro One Handout PDFtegegn mogessieNo ratings yet

- Solution: I) Cross Price Elasticity of DemandDocument6 pagesSolution: I) Cross Price Elasticity of DemandMuhammad MubeenNo ratings yet

- HW cH.7Document3 pagesHW cH.7Darin PromthedNo ratings yet

- Economics Lecture 1Document6 pagesEconomics Lecture 1YvonneNo ratings yet

- Engineering Economics Notes 11Document88 pagesEngineering Economics Notes 11Tanmay WakchaureNo ratings yet

- CHAPTER 9: Firm Behavior and Costs of ProductionDocument9 pagesCHAPTER 9: Firm Behavior and Costs of ProductionMuhamamd Asfand YarNo ratings yet

- The Resources Needed To Create Wealth: The History of The Market SystemDocument7 pagesThe Resources Needed To Create Wealth: The History of The Market Systemdorian451No ratings yet

- ChapC15 PDFDocument12 pagesChapC15 PDFRafik RafikNo ratings yet

- Theory of Firm 1Document12 pagesTheory of Firm 1UtkarshaNo ratings yet

- Chapter 1Document35 pagesChapter 1Nidhi HiranwarNo ratings yet

- Chapter 2 - Principles of EconomicsDocument7 pagesChapter 2 - Principles of EconomicsDarius DavidescuNo ratings yet

- Submitted By: Biki Das Class - XI Stream - Commerce Roll No. - 5Document42 pagesSubmitted By: Biki Das Class - XI Stream - Commerce Roll No. - 5Biki DasNo ratings yet

- The Central Problem of Economics and Economic System PDFDocument11 pagesThe Central Problem of Economics and Economic System PDFWong Yu Han Amelia (Yijc)No ratings yet

- Unit 1 Production Possibility Frontier (PPF)Document7 pagesUnit 1 Production Possibility Frontier (PPF)Mohan RajamaniNo ratings yet

- Chapter 21 ECO101 Production and CostDocument17 pagesChapter 21 ECO101 Production and Costxawad13No ratings yet

- Summary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESFrom EverandSummary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESNo ratings yet

- Sparrso RulesDocument5 pagesSparrso RulesOptimistic RiditNo ratings yet

- Part Six Managing International Operations: Chapter Seventeen Global Manufacturing and Supply Chain ManagementDocument32 pagesPart Six Managing International Operations: Chapter Seventeen Global Manufacturing and Supply Chain ManagementOptimistic RiditNo ratings yet

- Direct Investment and Collaborative StrategiesDocument19 pagesDirect Investment and Collaborative StrategiesOptimistic RiditNo ratings yet

- OligopolyDocument2 pagesOligopolyOptimistic RiditNo ratings yet

- Penalty For Unfair Labor PracticesDocument12 pagesPenalty For Unfair Labor PracticesOptimistic RiditNo ratings yet

- Human Resource PlanningDocument10 pagesHuman Resource PlanningOptimistic RiditNo ratings yet

- Class 9 NetworkDocument119 pagesClass 9 NetworkOptimistic RiditNo ratings yet

- Company Act - 1956Document17 pagesCompany Act - 1956Optimistic RiditNo ratings yet

- Introduction DbmsDocument20 pagesIntroduction DbmsOptimistic RiditNo ratings yet

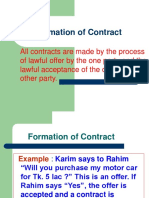

- Formation of Contract-1Document15 pagesFormation of Contract-1Optimistic RiditNo ratings yet

- Munication of Offer and AcceptanceDocument10 pagesMunication of Offer and AcceptanceOptimistic RiditNo ratings yet

- 07.capacity of PartiesDocument6 pages07.capacity of PartiesOptimistic RiditNo ratings yet