Download as xls, pdf, or txt

You might also like

- (Bank of America) Pricing Mortgage-Back SecuritiesDocument22 pages(Bank of America) Pricing Mortgage-Back Securitiesbhartia2512100% (4)

- Chapter 7. Solution To End-of-Chapter Comprehensive/Spreadsheet ProblemDocument5 pagesChapter 7. Solution To End-of-Chapter Comprehensive/Spreadsheet ProblemBen HarrisNo ratings yet

- NNNNN NNNNNNNNN NNNNNNNNNDocument70 pagesNNNNN NNNNNNNNN NNNNNNNNNSheheryar KhanNo ratings yet

- A2 Mbag183004Document22 pagesA2 Mbag183004Hashim EjazNo ratings yet

- A2 Mbag183002Document24 pagesA2 Mbag183002Hashim EjazNo ratings yet

- Bond PricingDocument16 pagesBond PricingAnonymousNo ratings yet

- Price Calculator For Bonds.Document29 pagesPrice Calculator For Bonds.Farjad Rehman100% (1)

- Financial ModelingDocument44 pagesFinancial Modelingaqsarana ranaNo ratings yet

- FIS Duration 20 07 2023Document20 pagesFIS Duration 20 07 2023Vishwajit GoudNo ratings yet

- NPV & IRR TemplateDocument7 pagesNPV & IRR TemplateDimas AriotejoNo ratings yet

- Bond Value IntroductionDocument4 pagesBond Value IntroductionNikhil BajoriaNo ratings yet

- B) Price of Bond When YTM Is 6% 1459.90 Price of BondDocument13 pagesB) Price of Bond When YTM Is 6% 1459.90 Price of BondMasab AsifNo ratings yet

- Chapter 02 Book FM - Simon B-WACCDocument23 pagesChapter 02 Book FM - Simon B-WACCMuhammad Asif Khan KhattakNo ratings yet

- Session 3 Bond and Interes RateDocument26 pagesSession 3 Bond and Interes RateadamobirkNo ratings yet

- The Passive and Active Stances: Bond Portfolio ManagementDocument41 pagesThe Passive and Active Stances: Bond Portfolio ManagementvaibhavNo ratings yet

- UTS MK 15 Sep 18Document14 pagesUTS MK 15 Sep 18Anonymous KyYdMhfaKXNo ratings yet

- Fmi S5Document5 pagesFmi S5Aditi RawatNo ratings yet

- FIS Duration 17 07 2023Document18 pagesFIS Duration 17 07 2023Vishwajit GoudNo ratings yet

- The Immunization Problem: Illustrated For The 30-Year BondDocument18 pagesThe Immunization Problem: Illustrated For The 30-Year BondSyed Ameer Ali ShahNo ratings yet

- Chapter 01Document20 pagesChapter 01Vicky PanditaNo ratings yet

- Chapter 12 Bond Portfolio MGMTDocument32 pagesChapter 12 Bond Portfolio MGMTAanchalNo ratings yet

- NPV - IrrDocument6 pagesNPV - IrrAnonymous jlLBRMAr3ONo ratings yet

- ACN3113 2023 T8 - Financial Instruments (S - P2)Document15 pagesACN3113 2023 T8 - Financial Instruments (S - P2)thchecyainie03No ratings yet

- NPV IrrDocument6 pagesNPV Irrahmad samtidaNo ratings yet

- NPV IrrDocument6 pagesNPV IrrRoni DamanikNo ratings yet

- 4.15 Correct One !!Document6 pages4.15 Correct One !!TarekYehiaNo ratings yet

- 123 - 17-chapter-17-FeasibilityAnalysisDocument21 pages123 - 17-chapter-17-FeasibilityAnalysisHrvoje ErorNo ratings yet

- How To Calculate Present Values: Discounted Cash Flow Analysis (Time Value of Money)Document16 pagesHow To Calculate Present Values: Discounted Cash Flow Analysis (Time Value of Money)cypriancourageNo ratings yet

- Zero-Coupon Bond Bonos de Descuento Puro: Ley Del Precio ÚnicoDocument11 pagesZero-Coupon Bond Bonos de Descuento Puro: Ley Del Precio ÚnicoSebastian MejiaNo ratings yet

- Computing The Present ValueDocument35 pagesComputing The Present ValueSana Naveed FawadNo ratings yet

- Project Finance SpreadsheetDocument30 pagesProject Finance Spreadsheetpamwaka2010No ratings yet

- NPV IrrDocument6 pagesNPV IrrmanjuNo ratings yet

- NPV IrrDocument6 pagesNPV IrrBharath BallalNo ratings yet

- NPV and IRRDocument6 pagesNPV and IRRHelmy WidjajaNo ratings yet

- NPV IrrDocument6 pagesNPV IrrdanielmugaboNo ratings yet

- NPV IrrDocument6 pagesNPV IrrSeno Ilham MaulanaNo ratings yet

- NPV Irr1Document6 pagesNPV Irr1san_lookNo ratings yet

- BANK3011 Workshop Week 4 SolutionsDocument5 pagesBANK3011 Workshop Week 4 SolutionsZahraaNo ratings yet

- NPV IrrDocument6 pagesNPV Irrgouthamireddy75No ratings yet

- WAAC Calculation 07062022 071635pm (AutoRecovered)Document12 pagesWAAC Calculation 07062022 071635pm (AutoRecovered)Saad AteeqNo ratings yet

- 4.15 Correct One !!Document6 pages4.15 Correct One !!TarekYehiaNo ratings yet

- Module 9 - Managing Interest Risk Part 2: 9.2 DurationDocument5 pagesModule 9 - Managing Interest Risk Part 2: 9.2 DurationAnna-Clara MansolahtiNo ratings yet

- Bond Pricing by J MagutaDocument2 pagesBond Pricing by J Magutajonathan magutaNo ratings yet

- NPV IrrDocument6 pagesNPV IrrRobb JackyNo ratings yet

- 0 NPV IrrDocument6 pages0 NPV IrrHimanshu GaurNo ratings yet

- 0 NPV IrrDocument6 pages0 NPV IrrHimanshu GaurNo ratings yet

- NPV IrrDocument6 pagesNPV Irrram persadNo ratings yet

- NPV IrrDocument6 pagesNPV Irrhelmy muktiNo ratings yet

- NPV IrrDocument6 pagesNPV IrrAries LhiNo ratings yet

- NPV IrrDocument6 pagesNPV Irrgidionwidjaja12No ratings yet

- Training Business Case Day 2Document13 pagesTraining Business Case Day 2amritakiranaaNo ratings yet

- Brenda Rianita Hapsari - 12030119130222 - Tugas Bab 17 Dan 18Document9 pagesBrenda Rianita Hapsari - 12030119130222 - Tugas Bab 17 Dan 18Brenda HapsariNo ratings yet

- Costof Equity: We Have Given ThatDocument20 pagesCostof Equity: We Have Given ThatUtkarsh PandeyNo ratings yet

- Totals 19.9 $31,841 $6,368 $3,184 $41,393 Average Value 2.84285714286 $4,549 $910 $455 $5,913 Maximum Value 19.9 $31,841 $6,368 $3,184 $41,393Document4 pagesTotals 19.9 $31,841 $6,368 $3,184 $41,393 Average Value 2.84285714286 $4,549 $910 $455 $5,913 Maximum Value 19.9 $31,841 $6,368 $3,184 $41,393Muhammad UmerNo ratings yet

- Stuti Mehta pgmb2149 FinanceDocument12 pagesStuti Mehta pgmb2149 FinanceStutiNo ratings yet

- Basic Leveraged Lease ExampleDocument13 pagesBasic Leveraged Lease ExampleSyed Ameer Ali ShahNo ratings yet

- Cab AssignmentDocument5 pagesCab AssignmentSonu GuptaNo ratings yet

- Class Questions Excel (1) (CH 10)Document8 pagesClass Questions Excel (1) (CH 10)pahuja ramanpreetNo ratings yet

- Time Value of Money and FormulasDocument5 pagesTime Value of Money and Formulasjanam shahNo ratings yet

- The Investment Detective Answer Q1Document4 pagesThe Investment Detective Answer Q1marco jeffNo ratings yet

- Matrices in Excel: Matrix A (A Row Vector) Matrix B (Square 3 X 3 Matrix) Matrix C (Column Vector)Document14 pagesMatrices in Excel: Matrix A (A Row Vector) Matrix B (Square 3 X 3 Matrix) Matrix C (Column Vector)Syed Ameer Ali ShahNo ratings yet

- Using Excel'S Rand FunctionDocument239 pagesUsing Excel'S Rand FunctionSyed Ameer Ali ShahNo ratings yet

- fm3 Chapter36Document11 pagesfm3 Chapter36Syed Ameer Ali ShahNo ratings yet

- fm3 Chapter35Document21 pagesfm3 Chapter35Syed Ameer Ali ShahNo ratings yet

- Using The Activecelldemo Macro: 5 #Value! 11 #Value!Document16 pagesUsing The Activecelldemo Macro: 5 #Value! 11 #Value!Syed Ameer Ali ShahNo ratings yet

- Excel'S NPV FunctionDocument41 pagesExcel'S NPV FunctionSyed Ameer Ali ShahNo ratings yet

- Using Transpose: A B C D E F G 1 2 3 4Document24 pagesUsing Transpose: A B C D E F G 1 2 3 4Syed Ameer Ali ShahNo ratings yet

- Expected Return On A One-Year Bond With An Adjustment For Default ProbabilityDocument83 pagesExpected Return On A One-Year Bond With An Adjustment For Default ProbabilitySyed Ameer Ali ShahNo ratings yet

- fm3 Chapter27Document79 pagesfm3 Chapter27Syed Ameer Ali ShahNo ratings yet

- The Option To Expand: Black-Scholes Option Pricing FormulaDocument29 pagesThe Option To Expand: Black-Scholes Option Pricing FormulaSyed Ameer Ali ShahNo ratings yet

- The Immunization Problem: Illustrated For The 30-Year BondDocument18 pagesThe Immunization Problem: Illustrated For The 30-Year BondSyed Ameer Ali ShahNo ratings yet

- Underlying Assets and Path-Independent Versus Path-Dependent PayoffsDocument39 pagesUnderlying Assets and Path-Independent Versus Path-Dependent PayoffsSyed Ameer Ali ShahNo ratings yet

- The Unit Circle: For The Quarter Circle and The Pi Experiment, See The Graph BelowDocument36 pagesThe Unit Circle: For The Quarter Circle and The Pi Experiment, See The Graph BelowSyed Ameer Ali ShahNo ratings yet

- Probability of End-Year Portfolio ValueDocument130 pagesProbability of End-Year Portfolio ValueSyed Ameer Ali ShahNo ratings yet

- Black-Scholes Option-Pricing Formula: Data Table: Comparing The Black-Scholes To The Intrinsic ValueDocument47 pagesBlack-Scholes Option-Pricing Formula: Data Table: Comparing The Black-Scholes To The Intrinsic ValueSyed Ameer Ali ShahNo ratings yet

- Black-Scholes Greeks This Spreadsheet Uses The Merton Model For A Continuously Dividend-Paying StockDocument44 pagesBlack-Scholes Greeks This Spreadsheet Uses The Merton Model For A Continuously Dividend-Paying StockSyed Ameer Ali ShahNo ratings yet

- Black-Scholes Option Pricing Formula Applied To General Pills PutDocument25 pagesBlack-Scholes Option Pricing Formula Applied To General Pills PutSyed Ameer Ali ShahNo ratings yet

- Fm3 - Chapter13 (Portfolio Optimization)Document46 pagesFm3 - Chapter13 (Portfolio Optimization)Syed Ameer Ali ShahNo ratings yet

- Binomial Option Pricing in A One-Period Model: Stock Price Bond PriceDocument36 pagesBinomial Option Pricing in A One-Period Model: Stock Price Bond PriceSyed Ameer Ali ShahNo ratings yet

- Call Option Payoff Patterns: Time 0 Time TDocument23 pagesCall Option Payoff Patterns: Time 0 Time TSyed Ameer Ali ShahNo ratings yet

- The Event Study Time Line: Estimation Window Event WindowDocument194 pagesThe Event Study Time Line: Estimation Window Event WindowSyed Ameer Ali ShahNo ratings yet

- Portfolio Optimization Allowing Short Sales: Variance-Covariance Matrix MeansDocument21 pagesPortfolio Optimization Allowing Short Sales: Variance-Covariance Matrix MeansSyed Ameer Ali ShahNo ratings yet

- Calculating The Efficient FrontierDocument31 pagesCalculating The Efficient FrontierSyed Ameer Ali ShahNo ratings yet

- The Gordon Model Cost of EquityDocument165 pagesThe Gordon Model Cost of EquitySyed Ameer Ali ShahNo ratings yet

- Basic Leveraged Lease ExampleDocument13 pagesBasic Leveraged Lease ExampleSyed Ameer Ali ShahNo ratings yet

- Annual Stock Price and Return Data For Six StocksDocument37 pagesAnnual Stock Price and Return Data For Six StocksSyed Ameer Ali ShahNo ratings yet

- Setting Up The Financial Statement ModelDocument45 pagesSetting Up The Financial Statement ModelSyed Ameer Ali ShahNo ratings yet

- How Not To Analyze A LeaseDocument7 pagesHow Not To Analyze A LeaseSyed Ameer Ali ShahNo ratings yet

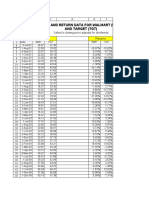

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- PPG CORP. BALANCE SHEETS, 1991-2000 (Million $) : Assets 2000 1999 1998 1997 1996Document47 pagesPPG CORP. BALANCE SHEETS, 1991-2000 (Million $) : Assets 2000 1999 1998 1997 1996Syed Ameer Ali ShahNo ratings yet

- CFTC and Jason AmadaDocument2 pagesCFTC and Jason AmadaJason AmadaNo ratings yet

- FC V23 Sample PaperDocument21 pagesFC V23 Sample PaperJuan_Car100% (1)

- TN TCDNDocument15 pagesTN TCDNLê PhươngNo ratings yet

- FABM2 LESSON 3 Statement of Changes in EquityDocument4 pagesFABM2 LESSON 3 Statement of Changes in EquityArjay CorderoNo ratings yet

- Solution CH 12 - 15Document11 pagesSolution CH 12 - 15Chintya ChrismatinNo ratings yet

- Corporation Problems-1Document18 pagesCorporation Problems-1Avia Chelsy DeangNo ratings yet

- Dividend DecisionsDocument48 pagesDividend DecisionsankitaNo ratings yet

- Moody's Afirmó La Calificación B2 de Argentina y Bajó Su Perspectiva A NegativaDocument6 pagesMoody's Afirmó La Calificación B2 de Argentina y Bajó Su Perspectiva A NegativaCronista.comNo ratings yet

- MK110 Project 3Document4 pagesMK110 Project 3harryNo ratings yet

- Elements of Finance 2Document14 pagesElements of Finance 2asticksNo ratings yet

- Interest Rate and Currency SwapsDocument29 pagesInterest Rate and Currency Swapssheetal221237269No ratings yet

- AFAR 3 - Quiz On Intercompany TransactionsDocument1 pageAFAR 3 - Quiz On Intercompany TransactionsPanda ErarNo ratings yet

- Bond Value and ReturnDocument82 pagesBond Value and Returnbhaskar5377No ratings yet

- Content Marketing BlueprintDocument34 pagesContent Marketing BlueprintJosué Gomes100% (1)

- Four Factor Performance AttributionDocument15 pagesFour Factor Performance AttributionSuraj PadhyNo ratings yet

- Role of Central Bank in ForexDocument5 pagesRole of Central Bank in ForexKrishna Bahadur Thapa100% (2)

- WFE Annual Statistics Guide 2018Document359 pagesWFE Annual Statistics Guide 2018Nico B. ValderramaNo ratings yet

- Different Investment Avenues and Financial Planning For EmergingDocument16 pagesDifferent Investment Avenues and Financial Planning For Emergingfomi89No ratings yet

- PDF Investment Analysis and Portfolio Management 11Th Edition Frank K Reilly Ebook Full ChapterDocument53 pagesPDF Investment Analysis and Portfolio Management 11Th Edition Frank K Reilly Ebook Full Chaptermargaret.redd792100% (2)

- Ft. Lauderdale-Q2 2012 ReportDocument14 pagesFt. Lauderdale-Q2 2012 ReportKen RudominerNo ratings yet

- Chapter 13 Valuing Stock Options: The BSM Model: Fundamentals of Futures and Options Markets, 8e (Hull)Document4 pagesChapter 13 Valuing Stock Options: The BSM Model: Fundamentals of Futures and Options Markets, 8e (Hull)TU Tran AnhNo ratings yet

- Guide To Syndicated Leveraged FinanceDocument11 pagesGuide To Syndicated Leveraged FinanceMrigank Agarwal100% (1)

- Notes On Market Wizards IDocument24 pagesNotes On Market Wizards IAdam HardyNo ratings yet

- BOAT Annual Report - Revenue - FinancialsDocument12 pagesBOAT Annual Report - Revenue - Financialsmaanyaagrawal65No ratings yet

- PS 2 SolutionDocument3 pagesPS 2 Solutionwasp1028100% (1)

- WE - 12 - Exchange Rates and FX MarketsDocument23 pagesWE - 12 - Exchange Rates and FX MarketsKholoud KhaledNo ratings yet

- Va RDocument68 pagesVa RjolienevinNo ratings yet

- Msci Japan IndexDocument3 pagesMsci Japan IndexSimonNo ratings yet

- Citi Bank Fraud Case-Trust On Relationship ManagerDocument12 pagesCiti Bank Fraud Case-Trust On Relationship ManagerChetan PanaraNo ratings yet