Mashoo 1ST ASSIGNMENT OF Financial Regulatry

Mashoo 1ST ASSIGNMENT OF Financial Regulatry

You might also like

- Taxation Grade 12 Daily Assessment Tasks TAHXATIONDocument17 pagesTaxation Grade 12 Daily Assessment Tasks TAHXATIONbohlale.mosala100% (1)

- Chapter 07Document3 pagesChapter 07Suzanna RamizovaNo ratings yet

- Investment Banking OverviewDocument77 pagesInvestment Banking OverviewEmerson De Mello100% (26)

- A simple approach to bond trading: The introductory guide to bond investments and their portfolio managementFrom EverandA simple approach to bond trading: The introductory guide to bond investments and their portfolio managementRating: 5 out of 5 stars5/5 (1)

- What I Learnt as an Analyst: Sharing of Experience in Investment and AnalysisFrom EverandWhat I Learnt as an Analyst: Sharing of Experience in Investment and AnalysisRating: 5 out of 5 stars5/5 (2)

- Shivajirao S. Jondhale Institute of Management Science and Research, AsangaonDocument13 pagesShivajirao S. Jondhale Institute of Management Science and Research, AsangaonROHITNo ratings yet

- Types of Financial Institutions and Their RolesDocument5 pagesTypes of Financial Institutions and Their RolesEmerson Gonzales TañaNo ratings yet

- Chapter - 2 FiDocument10 pagesChapter - 2 Fisitina.at.lunarNo ratings yet

- Financial Institutions TheoryDocument4 pagesFinancial Institutions TheorySandeep Singh SikerwarNo ratings yet

- Name: Hammad Ahmad Roll #: 1626 Section (B) Morning B.BA Semester (4) Introduction - Types of Financial Institutions and Their RolesDocument5 pagesName: Hammad Ahmad Roll #: 1626 Section (B) Morning B.BA Semester (4) Introduction - Types of Financial Institutions and Their RolesHammad AhmadNo ratings yet

- Institutional Interconnectivity: What Is The Difference Between Banking & Insurance?Document21 pagesInstitutional Interconnectivity: What Is The Difference Between Banking & Insurance?Jael CanedoNo ratings yet

- Unit 1Document16 pagesUnit 1Shivam YadavNo ratings yet

- Shivajirao S. Jondhale Institute of Management Science and Research, AsangaonDocument6 pagesShivajirao S. Jondhale Institute of Management Science and Research, AsangaonChetan ChaudhariNo ratings yet

- Investment Banking VivekDocument23 pagesInvestment Banking VivekVivek SinghNo ratings yet

- Fm1-Lps1-Intro Fin MGNT 03Document10 pagesFm1-Lps1-Intro Fin MGNT 03t2691153No ratings yet

- Business Finance Lesson 1 Financial SystemDocument3 pagesBusiness Finance Lesson 1 Financial SystemMatthew SuckNo ratings yet

- LecturesDocument26 pagesLecturesissamessissamess74No ratings yet

- CH 1 FIIMDocument28 pagesCH 1 FIIMMulata KahsayNo ratings yet

- Chapter 4: Financial IntermediationDocument15 pagesChapter 4: Financial IntermediationJhermaine SantiagoNo ratings yet

- CH 1 FIIMDocument28 pagesCH 1 FIIMKume MezgebuNo ratings yet

- Financial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksDocument5 pagesFinancial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksAnamMalikNo ratings yet

- Management For Financial Institutions PDFDocument25 pagesManagement For Financial Institutions PDFEkhlas Jami100% (2)

- FM 03 Financial IntermediationDocument8 pagesFM 03 Financial IntermediationIvy ObligadoNo ratings yet

- Financial EnvironmentDocument7 pagesFinancial Environmenthussainmeeran12No ratings yet

- BFM NotesDocument10 pagesBFM Notesravitejaraviteja11111No ratings yet

- Final Nancy121Document66 pagesFinal Nancy121Sahil SethiNo ratings yet

- Personal Finance-Module 2Document33 pagesPersonal Finance-Module 2Jhaira BarandaNo ratings yet

- What Does Credit Crisis Mean?Document14 pagesWhat Does Credit Crisis Mean?amardeeprocksNo ratings yet

- PROJECT - Financial Industry Sector - ARUNIMA VISWANATH - 21HR30B12Document15 pagesPROJECT - Financial Industry Sector - ARUNIMA VISWANATH - 21HR30B12ARUNIMA VISWANATHNo ratings yet

- DocumentDocument3 pagesDocumentjasvindersinghsagguNo ratings yet

- Debre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceDocument14 pagesDebre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceMikias DegwaleNo ratings yet

- Role of The Investment Bankers in The Financial SystemDocument60 pagesRole of The Investment Bankers in The Financial Systemmanoj_mmm100% (1)

- Ramiro, Lorren - Money MarketsDocument4 pagesRamiro, Lorren - Money Marketslorren ramiroNo ratings yet

- Lesson 4: Lending and Borrowing in The Financial System (Part II)Document6 pagesLesson 4: Lending and Borrowing in The Financial System (Part II)Mark Angelo BustosNo ratings yet

- Revised Project NotesDocument11 pagesRevised Project Notessanjay josephNo ratings yet

- Fin 101Document14 pagesFin 101Nasrullah Khan AbidNo ratings yet

- Financial IntermediationDocument14 pagesFinancial IntermediationKimberly BastesNo ratings yet

- Question 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Document7 pagesQuestion 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Usama KhanNo ratings yet

- FIM Group Assignmen FinalDocument9 pagesFIM Group Assignmen FinalEndeg KelkayNo ratings yet

- Indian Money MarketDocument8 pagesIndian Money MarketRey ArNo ratings yet

- Tien Te Ngan HangDocument2 pagesTien Te Ngan Hangngothiminhhau12a4No ratings yet

- NON BANKING F. INSTITUTIONS - New2Document5 pagesNON BANKING F. INSTITUTIONS - New2Vedy de KinNo ratings yet

- Capital Market Midterm ExamDocument4 pagesCapital Market Midterm ExamJessa Dela Cruz SahagunNo ratings yet

- Financial InstitutionsDocument19 pagesFinancial InstitutionsSunako NakaharaNo ratings yet

- FINANCIAL SYSTEM Role in Economic DevelopmentDocument4 pagesFINANCIAL SYSTEM Role in Economic Developmentrevathi alekhya80% (10)

- Lecture 1Document9 pagesLecture 1Jelani GreerNo ratings yet

- Financial Market in PakistanDocument37 pagesFinancial Market in PakistanNaila Kareem100% (1)

- Finance Is The Study of Funds Management, or The Allocation ofDocument8 pagesFinance Is The Study of Funds Management, or The Allocation ofPushpa BaruaNo ratings yet

- Finance BasicsDocument5 pagesFinance BasicsSneha Satyamoorthy100% (1)

- Unit 2 - Monetary EconomicsDocument20 pagesUnit 2 - Monetary EconomicsDaniel100% (1)

- Role of Financial Institutes in FinanciaDocument18 pagesRole of Financial Institutes in FinanciaI Gusti Ayu Astrid SNo ratings yet

- Act 2Document4 pagesAct 2kyrakeithcamaraNo ratings yet

- GroupDocument10 pagesGroupobayed florianNo ratings yet

- Financial Markets & InstitutionDocument79 pagesFinancial Markets & Institutioncharmilsingh99No ratings yet

- Regulations and Types of FIDocument5 pagesRegulations and Types of FIAbdul AleemNo ratings yet

- Development & Islamic - 4Document4 pagesDevelopment & Islamic - 4polmulitriNo ratings yet

- Fin Ins Chapter 1Document34 pagesFin Ins Chapter 1Mehedi HasanNo ratings yet

- BFI 305 Financing Small Business QPDocument11 pagesBFI 305 Financing Small Business QPministarz1No ratings yet

- Investment Banking..Document5 pagesInvestment Banking..Sachin AyyappasamyNo ratings yet

- University of Mumbai Investment Banking: Project Report by Tejas.S.Kamble ROLLNO:18 T.Y.Bcom - Banking & InsuranceDocument54 pagesUniversity of Mumbai Investment Banking: Project Report by Tejas.S.Kamble ROLLNO:18 T.Y.Bcom - Banking & Insurancetejaskamble45No ratings yet

- Investment Bankers and Scope FinalDocument48 pagesInvestment Bankers and Scope FinalAkash Gupta0% (1)

- LTOM Final Book 1Document72 pagesLTOM Final Book 1Antonette Contreras DomalantaNo ratings yet

- ReportDocument3 pagesReportvayezaNo ratings yet

- BCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateDocument9 pagesBCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateAbinash AgrawalNo ratings yet

- Book Value Per Common ShareDocument2 pagesBook Value Per Common SharepriteechauhanNo ratings yet

- ) ) @Ç!!4Bg!!!lJ6.qD : TotalDocument5 pages) ) @Ç!!4Bg!!!lJ6.qD : Totalchris johnsonNo ratings yet

- Investment AGREEMENTDocument13 pagesInvestment AGREEMENTLyptus PartnersNo ratings yet

- The Manual of Ideas Arnold Van Den Berg 201409Document12 pagesThe Manual of Ideas Arnold Van Den Berg 201409narang.gp5704No ratings yet

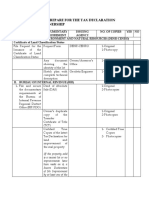

- Draft Requirements For Tax Declaration TranferDocument4 pagesDraft Requirements For Tax Declaration TranfercarmanvernonNo ratings yet

- CDD Aml Handbook 2010Document104 pagesCDD Aml Handbook 2010Salman MohiuddinNo ratings yet

- Debt Financing or Equity FinancingDocument10 pagesDebt Financing or Equity Financingimran hossain ruman100% (1)

- Ambac Industries, Inc. (Formerly American Bosch Arma Corporation) v. Commissioner of Internal Revenue, 487 F.2d 463, 2d Cir. (1973)Document7 pagesAmbac Industries, Inc. (Formerly American Bosch Arma Corporation) v. Commissioner of Internal Revenue, 487 F.2d 463, 2d Cir. (1973)Scribd Government DocsNo ratings yet

- NUST Business School: DerivativesDocument5 pagesNUST Business School: DerivativesAhmad Waqas DarNo ratings yet

- Brown POQDocument4 pagesBrown POQJonas GonzalesNo ratings yet

- A Study of Financial Derivatives (Futures and Options)Document128 pagesA Study of Financial Derivatives (Futures and Options)tanvirNo ratings yet

- Activity 4Document1 pageActivity 4Coleen Joy Sebastian PagalingNo ratings yet

- Lendsqr WorkDocument6 pagesLendsqr WorkitzsleekmayNo ratings yet

- Sol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aYamateNo ratings yet

- Final Exam Review Part 1 AnswersDocument8 pagesFinal Exam Review Part 1 AnswersSavan ParmarNo ratings yet

- Bookshop Business PlanDocument29 pagesBookshop Business PlanAbdullah Al-RafiNo ratings yet

- 3521 MBA (Master of Business Administration)Document58 pages3521 MBA (Master of Business Administration)espeecingNo ratings yet

- UCPB General Insurance Co., Inc. vs. Masagana Telamart, Inc.Document17 pagesUCPB General Insurance Co., Inc. vs. Masagana Telamart, Inc.Jaja Ordinario Quiachon-AbarcaNo ratings yet

- MBA Chp-1 - Introduction To AccountingDocument20 pagesMBA Chp-1 - Introduction To AccountingNitish rajNo ratings yet

- Assessment - Business Immigration - Canada 2021Document4 pagesAssessment - Business Immigration - Canada 2021Adil AhmedNo ratings yet

- Fin329 Chapter 3 - Investment AlternativesDocument30 pagesFin329 Chapter 3 - Investment AlternativesMuhd HisyamuddinNo ratings yet

- Christ (Deemed To Be University) School of Business and Management Assignment BriefDocument5 pagesChrist (Deemed To Be University) School of Business and Management Assignment BriefLatha JosephNo ratings yet

- Cement - 3QFY24 Earnings To Decline by 25%QoQDocument4 pagesCement - 3QFY24 Earnings To Decline by 25%QoQmuhammadghufran1No ratings yet

- As - 22 Accounting For Taxes On IncomeDocument21 pagesAs - 22 Accounting For Taxes On IncomeTACS & CO.No ratings yet

- Customer Journey Non LienDocument9 pagesCustomer Journey Non LienaslamzohaibNo ratings yet

Download as docx, pdf, or txt

You might also like

- Taxation Grade 12 Daily Assessment Tasks TAHXATIONDocument17 pagesTaxation Grade 12 Daily Assessment Tasks TAHXATIONbohlale.mosala100% (1)

- Chapter 07Document3 pagesChapter 07Suzanna RamizovaNo ratings yet

- Investment Banking OverviewDocument77 pagesInvestment Banking OverviewEmerson De Mello100% (26)

- A simple approach to bond trading: The introductory guide to bond investments and their portfolio managementFrom EverandA simple approach to bond trading: The introductory guide to bond investments and their portfolio managementRating: 5 out of 5 stars5/5 (1)

- What I Learnt as an Analyst: Sharing of Experience in Investment and AnalysisFrom EverandWhat I Learnt as an Analyst: Sharing of Experience in Investment and AnalysisRating: 5 out of 5 stars5/5 (2)

- Shivajirao S. Jondhale Institute of Management Science and Research, AsangaonDocument13 pagesShivajirao S. Jondhale Institute of Management Science and Research, AsangaonROHITNo ratings yet

- Types of Financial Institutions and Their RolesDocument5 pagesTypes of Financial Institutions and Their RolesEmerson Gonzales TañaNo ratings yet

- Chapter - 2 FiDocument10 pagesChapter - 2 Fisitina.at.lunarNo ratings yet

- Financial Institutions TheoryDocument4 pagesFinancial Institutions TheorySandeep Singh SikerwarNo ratings yet

- Name: Hammad Ahmad Roll #: 1626 Section (B) Morning B.BA Semester (4) Introduction - Types of Financial Institutions and Their RolesDocument5 pagesName: Hammad Ahmad Roll #: 1626 Section (B) Morning B.BA Semester (4) Introduction - Types of Financial Institutions and Their RolesHammad AhmadNo ratings yet

- Institutional Interconnectivity: What Is The Difference Between Banking & Insurance?Document21 pagesInstitutional Interconnectivity: What Is The Difference Between Banking & Insurance?Jael CanedoNo ratings yet

- Unit 1Document16 pagesUnit 1Shivam YadavNo ratings yet

- Shivajirao S. Jondhale Institute of Management Science and Research, AsangaonDocument6 pagesShivajirao S. Jondhale Institute of Management Science and Research, AsangaonChetan ChaudhariNo ratings yet

- Investment Banking VivekDocument23 pagesInvestment Banking VivekVivek SinghNo ratings yet

- Fm1-Lps1-Intro Fin MGNT 03Document10 pagesFm1-Lps1-Intro Fin MGNT 03t2691153No ratings yet

- Business Finance Lesson 1 Financial SystemDocument3 pagesBusiness Finance Lesson 1 Financial SystemMatthew SuckNo ratings yet

- LecturesDocument26 pagesLecturesissamessissamess74No ratings yet

- CH 1 FIIMDocument28 pagesCH 1 FIIMMulata KahsayNo ratings yet

- Chapter 4: Financial IntermediationDocument15 pagesChapter 4: Financial IntermediationJhermaine SantiagoNo ratings yet

- CH 1 FIIMDocument28 pagesCH 1 FIIMKume MezgebuNo ratings yet

- Financial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksDocument5 pagesFinancial Market in Pakistan: Financial Markets and Their Roles: Commercial BanksAnamMalikNo ratings yet

- Management For Financial Institutions PDFDocument25 pagesManagement For Financial Institutions PDFEkhlas Jami100% (2)

- FM 03 Financial IntermediationDocument8 pagesFM 03 Financial IntermediationIvy ObligadoNo ratings yet

- Financial EnvironmentDocument7 pagesFinancial Environmenthussainmeeran12No ratings yet

- BFM NotesDocument10 pagesBFM Notesravitejaraviteja11111No ratings yet

- Final Nancy121Document66 pagesFinal Nancy121Sahil SethiNo ratings yet

- Personal Finance-Module 2Document33 pagesPersonal Finance-Module 2Jhaira BarandaNo ratings yet

- What Does Credit Crisis Mean?Document14 pagesWhat Does Credit Crisis Mean?amardeeprocksNo ratings yet

- PROJECT - Financial Industry Sector - ARUNIMA VISWANATH - 21HR30B12Document15 pagesPROJECT - Financial Industry Sector - ARUNIMA VISWANATH - 21HR30B12ARUNIMA VISWANATHNo ratings yet

- DocumentDocument3 pagesDocumentjasvindersinghsagguNo ratings yet

- Debre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceDocument14 pagesDebre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceMikias DegwaleNo ratings yet

- Role of The Investment Bankers in The Financial SystemDocument60 pagesRole of The Investment Bankers in The Financial Systemmanoj_mmm100% (1)

- Ramiro, Lorren - Money MarketsDocument4 pagesRamiro, Lorren - Money Marketslorren ramiroNo ratings yet

- Lesson 4: Lending and Borrowing in The Financial System (Part II)Document6 pagesLesson 4: Lending and Borrowing in The Financial System (Part II)Mark Angelo BustosNo ratings yet

- Revised Project NotesDocument11 pagesRevised Project Notessanjay josephNo ratings yet

- Fin 101Document14 pagesFin 101Nasrullah Khan AbidNo ratings yet

- Financial IntermediationDocument14 pagesFinancial IntermediationKimberly BastesNo ratings yet

- Question 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Document7 pagesQuestion 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Usama KhanNo ratings yet

- FIM Group Assignmen FinalDocument9 pagesFIM Group Assignmen FinalEndeg KelkayNo ratings yet

- Indian Money MarketDocument8 pagesIndian Money MarketRey ArNo ratings yet

- Tien Te Ngan HangDocument2 pagesTien Te Ngan Hangngothiminhhau12a4No ratings yet

- NON BANKING F. INSTITUTIONS - New2Document5 pagesNON BANKING F. INSTITUTIONS - New2Vedy de KinNo ratings yet

- Capital Market Midterm ExamDocument4 pagesCapital Market Midterm ExamJessa Dela Cruz SahagunNo ratings yet

- Financial InstitutionsDocument19 pagesFinancial InstitutionsSunako NakaharaNo ratings yet

- FINANCIAL SYSTEM Role in Economic DevelopmentDocument4 pagesFINANCIAL SYSTEM Role in Economic Developmentrevathi alekhya80% (10)

- Lecture 1Document9 pagesLecture 1Jelani GreerNo ratings yet

- Financial Market in PakistanDocument37 pagesFinancial Market in PakistanNaila Kareem100% (1)

- Finance Is The Study of Funds Management, or The Allocation ofDocument8 pagesFinance Is The Study of Funds Management, or The Allocation ofPushpa BaruaNo ratings yet

- Finance BasicsDocument5 pagesFinance BasicsSneha Satyamoorthy100% (1)

- Unit 2 - Monetary EconomicsDocument20 pagesUnit 2 - Monetary EconomicsDaniel100% (1)

- Role of Financial Institutes in FinanciaDocument18 pagesRole of Financial Institutes in FinanciaI Gusti Ayu Astrid SNo ratings yet

- Act 2Document4 pagesAct 2kyrakeithcamaraNo ratings yet

- GroupDocument10 pagesGroupobayed florianNo ratings yet

- Financial Markets & InstitutionDocument79 pagesFinancial Markets & Institutioncharmilsingh99No ratings yet

- Regulations and Types of FIDocument5 pagesRegulations and Types of FIAbdul AleemNo ratings yet

- Development & Islamic - 4Document4 pagesDevelopment & Islamic - 4polmulitriNo ratings yet

- Fin Ins Chapter 1Document34 pagesFin Ins Chapter 1Mehedi HasanNo ratings yet

- BFI 305 Financing Small Business QPDocument11 pagesBFI 305 Financing Small Business QPministarz1No ratings yet

- Investment Banking..Document5 pagesInvestment Banking..Sachin AyyappasamyNo ratings yet

- University of Mumbai Investment Banking: Project Report by Tejas.S.Kamble ROLLNO:18 T.Y.Bcom - Banking & InsuranceDocument54 pagesUniversity of Mumbai Investment Banking: Project Report by Tejas.S.Kamble ROLLNO:18 T.Y.Bcom - Banking & Insurancetejaskamble45No ratings yet

- Investment Bankers and Scope FinalDocument48 pagesInvestment Bankers and Scope FinalAkash Gupta0% (1)

- LTOM Final Book 1Document72 pagesLTOM Final Book 1Antonette Contreras DomalantaNo ratings yet

- ReportDocument3 pagesReportvayezaNo ratings yet

- BCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateDocument9 pagesBCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateAbinash AgrawalNo ratings yet

- Book Value Per Common ShareDocument2 pagesBook Value Per Common SharepriteechauhanNo ratings yet

- ) ) @Ç!!4Bg!!!lJ6.qD : TotalDocument5 pages) ) @Ç!!4Bg!!!lJ6.qD : Totalchris johnsonNo ratings yet

- Investment AGREEMENTDocument13 pagesInvestment AGREEMENTLyptus PartnersNo ratings yet

- The Manual of Ideas Arnold Van Den Berg 201409Document12 pagesThe Manual of Ideas Arnold Van Den Berg 201409narang.gp5704No ratings yet

- Draft Requirements For Tax Declaration TranferDocument4 pagesDraft Requirements For Tax Declaration TranfercarmanvernonNo ratings yet

- CDD Aml Handbook 2010Document104 pagesCDD Aml Handbook 2010Salman MohiuddinNo ratings yet

- Debt Financing or Equity FinancingDocument10 pagesDebt Financing or Equity Financingimran hossain ruman100% (1)

- Ambac Industries, Inc. (Formerly American Bosch Arma Corporation) v. Commissioner of Internal Revenue, 487 F.2d 463, 2d Cir. (1973)Document7 pagesAmbac Industries, Inc. (Formerly American Bosch Arma Corporation) v. Commissioner of Internal Revenue, 487 F.2d 463, 2d Cir. (1973)Scribd Government DocsNo ratings yet

- NUST Business School: DerivativesDocument5 pagesNUST Business School: DerivativesAhmad Waqas DarNo ratings yet

- Brown POQDocument4 pagesBrown POQJonas GonzalesNo ratings yet

- A Study of Financial Derivatives (Futures and Options)Document128 pagesA Study of Financial Derivatives (Futures and Options)tanvirNo ratings yet

- Activity 4Document1 pageActivity 4Coleen Joy Sebastian PagalingNo ratings yet

- Lendsqr WorkDocument6 pagesLendsqr WorkitzsleekmayNo ratings yet

- Sol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Teacher's Manual - Ia Part 1aYamateNo ratings yet

- Final Exam Review Part 1 AnswersDocument8 pagesFinal Exam Review Part 1 AnswersSavan ParmarNo ratings yet

- Bookshop Business PlanDocument29 pagesBookshop Business PlanAbdullah Al-RafiNo ratings yet

- 3521 MBA (Master of Business Administration)Document58 pages3521 MBA (Master of Business Administration)espeecingNo ratings yet

- UCPB General Insurance Co., Inc. vs. Masagana Telamart, Inc.Document17 pagesUCPB General Insurance Co., Inc. vs. Masagana Telamart, Inc.Jaja Ordinario Quiachon-AbarcaNo ratings yet

- MBA Chp-1 - Introduction To AccountingDocument20 pagesMBA Chp-1 - Introduction To AccountingNitish rajNo ratings yet

- Assessment - Business Immigration - Canada 2021Document4 pagesAssessment - Business Immigration - Canada 2021Adil AhmedNo ratings yet

- Fin329 Chapter 3 - Investment AlternativesDocument30 pagesFin329 Chapter 3 - Investment AlternativesMuhd HisyamuddinNo ratings yet

- Christ (Deemed To Be University) School of Business and Management Assignment BriefDocument5 pagesChrist (Deemed To Be University) School of Business and Management Assignment BriefLatha JosephNo ratings yet

- Cement - 3QFY24 Earnings To Decline by 25%QoQDocument4 pagesCement - 3QFY24 Earnings To Decline by 25%QoQmuhammadghufran1No ratings yet

- As - 22 Accounting For Taxes On IncomeDocument21 pagesAs - 22 Accounting For Taxes On IncomeTACS & CO.No ratings yet

- Customer Journey Non LienDocument9 pagesCustomer Journey Non LienaslamzohaibNo ratings yet