Download as docx, pdf, or txt

You might also like

- Case Study - Waste ManagementDocument4 pagesCase Study - Waste ManagementLuke MazarelloNo ratings yet

- Internal Audit Key Performance Indicators (KPIs)Document15 pagesInternal Audit Key Performance Indicators (KPIs)Oumayma Niz100% (1)

- SM Chapter 04Document135 pagesSM Chapter 04mas aziz100% (1)

- Chapter 1 - An Introduction To Assurance and Financial Statement AuditingDocument7 pagesChapter 1 - An Introduction To Assurance and Financial Statement AuditingBlake Crusius0% (1)

- Leopard (Working Sep-2022) CPR Tax Month Dec-2022Document1 pageLeopard (Working Sep-2022) CPR Tax Month Dec-2022AnaassNo ratings yet

- It 2023072601012252139Document1 pageIt 2023072601012252139M.TayyabNo ratings yet

- 1.JIAP ObservationsDocument70 pages1.JIAP ObservationsHamid AliNo ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document1 pageIncome Tax Department: Computerized Payment Receipt (CPR - It)Mian EnterprisesNo ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document1 pageIncome Tax Department: Computerized Payment Receipt (CPR - It)naeem1990No ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document2 pagesIncome Tax Department: Computerized Payment Receipt (CPR - It)Mian EnterprisesNo ratings yet

- In0878 GlobalDocument1 pageIn0878 Globalanshag631No ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1thalapathytimes65No ratings yet

- PNB Turner Road KSKDocument1 pagePNB Turner Road KSKlipinaren99No ratings yet

- Annual Budget 2020 TagaytyaDocument168 pagesAnnual Budget 2020 TagaytyaKakam PwetNo ratings yet

- This Is An Auto-Generated Purchase Order Based On Online Tender DecisionDocument2 pagesThis Is An Auto-Generated Purchase Order Based On Online Tender DecisiondycmmgncrNo ratings yet

- This Is An Auto-Generated Purchase Order Based On Online Tender DecisionDocument3 pagesThis Is An Auto-Generated Purchase Order Based On Online Tender DecisionvivekNo ratings yet

- Tax Invoice: F-14, Ground Floor, Sector-9, Noida-201301 GSTIN/UIN: 09ABCCS0954K1Z2 State Name: Uttar Pradesh, Code: 09Document1 pageTax Invoice: F-14, Ground Floor, Sector-9, Noida-201301 GSTIN/UIN: 09ABCCS0954K1Z2 State Name: Uttar Pradesh, Code: 09VIDYANAND THAKURNo ratings yet

- Tax Invoice P K EnterprisesDocument2 pagesTax Invoice P K EnterprisesSanjay LoyalkaNo ratings yet

- AC GST Tax InvoiceDocument1 pageAC GST Tax InvoiceSh'JilNo ratings yet

- AC GST Tax Invoice PDFDocument1 pageAC GST Tax Invoice PDFPriyanshu PalNo ratings yet

- Larsen & Toubro Limited, ConstructionDocument3 pagesLarsen & Toubro Limited, ConstructionandrewgeorgecherianNo ratings yet

- AC GST Tax InvoiceDocument1 pageAC GST Tax InvoiceSuganthi RavindrenNo ratings yet

- Tax Invoice: Singh Computer SC/SM/0058/23-24 00564 Dt. 15-Apr-23 15-Apr-23Document1 pageTax Invoice: Singh Computer SC/SM/0058/23-24 00564 Dt. 15-Apr-23 15-Apr-23rkassociates.bizNo ratings yet

- This Is An Auto-Generated Purchase Order Based On Online Tender DecisionDocument2 pagesThis Is An Auto-Generated Purchase Order Based On Online Tender DecisionTUff LabNo ratings yet

- Subal Consruction GST Invoice 7Document4 pagesSubal Consruction GST Invoice 7smn.ussharNo ratings yet

- Screenshot 2022-10-18 at 3.10.59 PMDocument4 pagesScreenshot 2022-10-18 at 3.10.59 PMbilalahmed333No ratings yet

- Report of Disbursement (ROD)Document2 pagesReport of Disbursement (ROD)amender22No ratings yet

- 1 2uvdz21Document1 page1 2uvdz21diptajyotiroyNo ratings yet

- AC GST Tax InvoiceDocument1 pageAC GST Tax InvoicearunavNo ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1vighnarthaagency2255No ratings yet

- Digitally Signed by Manoj Agarwal Date: 2023.11.07 16:12:12 +05'30'Document13 pagesDigitally Signed by Manoj Agarwal Date: 2023.11.07 16:12:12 +05'30'unstableskNo ratings yet

- 08-10 Annex-BDocument5 pages08-10 Annex-BNakul DhawanNo ratings yet

- SBC GDocument2 pagesSBC GsujaraghupsNo ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1Rakesh SinghNo ratings yet

- Ecr Loa 24Document14 pagesEcr Loa 24sanojcad123No ratings yet

- Pending Bill StatusDocument5 pagesPending Bill StatusSanu RajNo ratings yet

- Address:-MRO-CIDCO Mansarovar Station, Navi Mumbai - 410209, Maharashtra, IndiaDocument4 pagesAddress:-MRO-CIDCO Mansarovar Station, Navi Mumbai - 410209, Maharashtra, IndiaNikhil PatilNo ratings yet

- Exemption Certificate Us 159 (1) 153Document2 pagesExemption Certificate Us 159 (1) 153ijazaslam.huaweiNo ratings yet

- BFCS 009 2022 23Document4 pagesBFCS 009 2022 23Pintu Raj DasNo ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document2 pagesIncome Tax Department: Computerized Payment Receipt (CPR - It)Mian EnterprisesNo ratings yet

- AC GST Tax InvoiceDocument1 pageAC GST Tax Invoiceanbu.jerome01No ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1lakshay122333No ratings yet

- Report OutputDocument3 pagesReport OutputRishabh KapoorNo ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1prasannaNo ratings yet

- Order 2971112Document2 pagesOrder 2971112Zeeshan KhanNo ratings yet

- Fcipl Invoice Czika19200009495Document1 pageFcipl Invoice Czika19200009495sudhakar sudhakarNo ratings yet

- Office of The Inland Revenue and Customs (South), Karachi: Director General AuditDocument14 pagesOffice of The Inland Revenue and Customs (South), Karachi: Director General AuditHamid AliNo ratings yet

- Project/Estimate Detail Report (GST)Document8 pagesProject/Estimate Detail Report (GST)Ravi SahuNo ratings yet

- Tax Invoice: M/S. Panakala & Co., Chartered Accountants Prop.: C.A K Panakala Rao Indian Bank-Bill ToDocument1 pageTax Invoice: M/S. Panakala & Co., Chartered Accountants Prop.: C.A K Panakala Rao Indian Bank-Bill Tomanoj mohanNo ratings yet

- Tax Invoice: Singh Computer SC/SM/0032/23-24 00536 Dt. 8-Apr-23 8-Apr-23Document1 pageTax Invoice: Singh Computer SC/SM/0032/23-24 00536 Dt. 8-Apr-23 8-Apr-23rkassociates.bizNo ratings yet

- RailwayDocument1 pageRailwaypises97155No ratings yet

- 14231101105456PODocument3 pages14231101105456PONOTOFIRE PVT. LTD.No ratings yet

- AC GST Tax InvoiceDocument1 pageAC GST Tax Invoiceபைசல் ஹNo ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1SuriyaprakashNo ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1Varun GoswamiNo ratings yet

- AC GST Tax InvoiceDocument1 pageAC GST Tax InvoiceHarikrishna BNo ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1s.suresh k.swaminathanNo ratings yet

- This Is An Auto-Generated Purchase Order Based On Online Tender DecisionDocument3 pagesThis Is An Auto-Generated Purchase Order Based On Online Tender Decisionmitzz39No ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1saradhishiva1No ratings yet

- IT2023070701011262401Document2 pagesIT2023070701011262401Naseem HameedNo ratings yet

- AC GST Tax Invoice 1Document1 pageAC GST Tax Invoice 1KarthikStarkNo ratings yet

- Sales RDRL 6222 23-24Document1 pageSales RDRL 6222 23-24sourav.dey.bcom24No ratings yet

- Bill Details SpecimenDocument1 pageBill Details SpecimenJ.J. AnandNo ratings yet

- Building Inspection Service Revenues World Summary: Market Values & Financials by CountryFrom EverandBuilding Inspection Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- 1.JIAP ObservationsDocument70 pages1.JIAP ObservationsHamid AliNo ratings yet

- AIR UAB West Wharf 2018-19Document7 pagesAIR UAB West Wharf 2018-19Hamid AliNo ratings yet

- Air Crto Khi 17.10.18Document27 pagesAir Crto Khi 17.10.18Hamid AliNo ratings yet

- Office of The Inland Revenue and Customs (South), Karachi: Director General AuditDocument14 pagesOffice of The Inland Revenue and Customs (South), Karachi: Director General AuditHamid AliNo ratings yet

- Coa C2001-004Document2 pagesCoa C2001-004bolNo ratings yet

- Capstone ProjectDocument11 pagesCapstone ProjectHezekiah TalaraNo ratings yet

- Ricy Annual Report 2014Document118 pagesRicy Annual Report 2014Farida SetiawatiNo ratings yet

- Bcom 203Document134 pagesBcom 203Dharmesh GoyalNo ratings yet

- 2017 Annual Report KiaDocument74 pages2017 Annual Report Kiakavitha kalasudhanNo ratings yet

- Ch09 Break-Even Point and Cost-Volume Profit AnalysisDocument19 pagesCh09 Break-Even Point and Cost-Volume Profit AnalysisZaira PangesfanNo ratings yet

- Budget Process PakistanDocument68 pagesBudget Process PakistanMomin Qureshi75% (4)

- Chapter 35 001Document8 pagesChapter 35 001Grace Ann Aceveda QuinioNo ratings yet

- Summary of Standards of Auditing (SA) Issued by Institute of Chartered Accountants of IndiaDocument43 pagesSummary of Standards of Auditing (SA) Issued by Institute of Chartered Accountants of IndiaParthasarathi MishraNo ratings yet

- BSTDB Financial Statements For 2020Document72 pagesBSTDB Financial Statements For 2020Isabela VelicariaNo ratings yet

- Multiple Choice Questions ITDocument3 pagesMultiple Choice Questions ITKim CarpioNo ratings yet

- Resume Sample For Quantity SurveyorDocument5 pagesResume Sample For Quantity Surveyorc2znbtts100% (1)

- ConstitutionDocument20 pagesConstitutionfsyNo ratings yet

- SBL ListDocument5 pagesSBL ListrNo ratings yet

- 9706 s06 QP 1Document12 pages9706 s06 QP 1roukaiya_peerkhanNo ratings yet

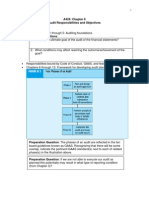

- A424: Chapter 6 Audit Responsibilities and Objectives Preparation QuestionsDocument8 pagesA424: Chapter 6 Audit Responsibilities and Objectives Preparation QuestionsNovah Mae Begaso SamarNo ratings yet

- Credit Administration, MeasurementDocument11 pagesCredit Administration, Measurementmentor_muhaxheriNo ratings yet

- Bot ContractDocument18 pagesBot ContractideyNo ratings yet

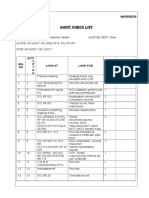

- Audit Check List: Acti V IT Y N O Look at Look For Sampl Size Objective EvidenceDocument2 pagesAudit Check List: Acti V IT Y N O Look at Look For Sampl Size Objective EvidencemaheshNo ratings yet

- Context of Organization REV 01Document13 pagesContext of Organization REV 01cibelle100% (2)

- International Auditing and Assurance Standards Board: 2020 EditionDocument102 pagesInternational Auditing and Assurance Standards Board: 2020 EditionSanket BaraiNo ratings yet

- Inspection Manual IDRA (Eng)Document24 pagesInspection Manual IDRA (Eng)Auishee BaruaNo ratings yet

- Enron Scandal - Wikipedia, The Free EncyclopediaDocument31 pagesEnron Scandal - Wikipedia, The Free Encyclopediazhyldyz_88No ratings yet

- Name: - Score: - Block: - DateDocument8 pagesName: - Score: - Block: - DateLEONARDO BAÑAGANo ratings yet

- 1000 Guide To Global Grants en PDFDocument40 pages1000 Guide To Global Grants en PDFAnusha LihalaNo ratings yet

- SIMS Exim ManagementDocument56 pagesSIMS Exim ManagementRounaq DharNo ratings yet