Download as pdf or txt

You might also like

- Manny Pacquiao Tax Case DigestDocument3 pagesManny Pacquiao Tax Case Digestbigbird1021780% (1)

- PLDT v. Davao City Case DigestDocument1 pagePLDT v. Davao City Case DigestFlorence Rosete100% (3)

- Bir Ruling Da 095 05Document2 pagesBir Ruling Da 095 05RB BalanayNo ratings yet

- Air Canada v. CIR DigestDocument2 pagesAir Canada v. CIR Digestpinkblush717100% (4)

- Domingo vs. Garlitos Case DigestDocument1 pageDomingo vs. Garlitos Case DigestAdhara CelerianNo ratings yet

- 106 Cir Vs Cta GR No 106611 July 21 1994 DigestDocument1 page106 Cir Vs Cta GR No 106611 July 21 1994 Digestjayinthelongrun33% (3)

- CIR Vs Eastern TelecommunicationsDocument1 pageCIR Vs Eastern TelecommunicationsLizzy WayNo ratings yet

- Used Actually, Directly and Exclusively For Educational Purposes Shall Be Exempt From Taxes and DutiesDocument2 pagesUsed Actually, Directly and Exclusively For Educational Purposes Shall Be Exempt From Taxes and DutiesJasper Alon100% (2)

- Camp John Hay Development Corp. v. CBAA, 706 SCRA 547 - THE LIFEBLOOD DOCTRINE - DigestDocument2 pagesCamp John Hay Development Corp. v. CBAA, 706 SCRA 547 - THE LIFEBLOOD DOCTRINE - DigestKate Garo100% (1)

- 28 Municipality of Cainta Vs City of PasigDocument2 pages28 Municipality of Cainta Vs City of Pasighigoremso giensdks100% (3)

- Annual Tax and Interest Statement: See Reverse Side For Additional InformationDocument2 pagesAnnual Tax and Interest Statement: See Reverse Side For Additional InformationtclippertNo ratings yet

- PAL v. CIR (GR 198759)Document2 pagesPAL v. CIR (GR 198759)Erica Gana100% (1)

- Mitsubishi v. CIRDocument2 pagesMitsubishi v. CIRSophiaFrancescaEspinosa100% (1)

- CIR V Pilipinas ShellDocument4 pagesCIR V Pilipinas ShellCedric Enriquez100% (2)

- Ing Bank v. CIR / G.R. No. 167679 / July 22, 2015Document1 pageIng Bank v. CIR / G.R. No. 167679 / July 22, 2015Mini U. Soriano100% (1)

- (Digest) CIR v. Pineda, 21 SCRA 105Document2 pages(Digest) CIR v. Pineda, 21 SCRA 105Homer SimpsonNo ratings yet

- 3M PhilippinesDocument2 pages3M PhilippinesKarl Vincent Raso100% (1)

- 117 Luzon Stevedoring Co. vs. CTADocument1 page117 Luzon Stevedoring Co. vs. CTACleinJonTiuNo ratings yet

- Valley Trading Co v. CFI of IsabelaDocument1 pageValley Trading Co v. CFI of IsabelaArahbells100% (2)

- BIR Ruling (DA-287-07) May 8, 2007Document3 pagesBIR Ruling (DA-287-07) May 8, 2007Raiya AngelaNo ratings yet

- China Banking Corporation v. CIRDocument2 pagesChina Banking Corporation v. CIRRaymond Cheng80% (5)

- 35 GR 175772 Mitsubishi vs. CIRDocument2 pages35 GR 175772 Mitsubishi vs. CIRJoshua Erik Madria100% (1)

- 010 CELAJE Secretary of Finance V LazatinDocument1 page010 CELAJE Secretary of Finance V LazatinJosh CelajeNo ratings yet

- M. Construction and Interpretation I. Cir vs. Puregold Duty Free, Inc. G.R. NO. 202789, JUNE 22, 2015Document3 pagesM. Construction and Interpretation I. Cir vs. Puregold Duty Free, Inc. G.R. NO. 202789, JUNE 22, 2015Marry LasherasNo ratings yet

- 11 NDC V CIRDocument3 pages11 NDC V CIRTricia MontoyaNo ratings yet

- Diaz Vs Secretary of FinanceDocument3 pagesDiaz Vs Secretary of FinanceJoshua Shin100% (5)

- CIR Vs Toledo DigestDocument2 pagesCIR Vs Toledo DigestClar Napa100% (2)

- Valley Trading vs. Court of First Instance of Isabela Branch IIDocument3 pagesValley Trading vs. Court of First Instance of Isabela Branch IISarah BuendiaNo ratings yet

- Commissioner of Internal Revenue V. Lancaster Philippines, Inc. FactsDocument11 pagesCommissioner of Internal Revenue V. Lancaster Philippines, Inc. FactsJun Bill CercadoNo ratings yet

- Case Digest CIR v. DashDocument2 pagesCase Digest CIR v. DashLIERANo ratings yet

- BIR Ruling No. 006-00Document2 pagesBIR Ruling No. 006-00glg-phNo ratings yet

- Coca Cola vs. CIRDocument1 pageCoca Cola vs. CIRmenlyn100% (4)

- Tax-Digest 1-5Document16 pagesTax-Digest 1-5Royalhighness18No ratings yet

- 2008 BIR - Ruling - DA 128 08 - 20180320 1159 1heemgd PDFDocument2 pages2008 BIR - Ruling - DA 128 08 - 20180320 1159 1heemgd PDFAleezah Gertrude RaymundoNo ratings yet

- Republic V Aquafresh SeafoodDocument2 pagesRepublic V Aquafresh SeafoodRia Evita RevitaNo ratings yet

- Misamis Oriental Vs CEPALCO, 181 SCRA 38Document2 pagesMisamis Oriental Vs CEPALCO, 181 SCRA 38Ron LaurelNo ratings yet

- China Banking Corporation Vs CIRDocument3 pagesChina Banking Corporation Vs CIRMiaNo ratings yet

- CIR Vs Seagate, GR 153866Document3 pagesCIR Vs Seagate, GR 153866Mar Develos100% (1)

- 25 (Tono) CBK Power Company V Commissioner of Internal RevenueDocument2 pages25 (Tono) CBK Power Company V Commissioner of Internal RevenueKaye Dominique TonoNo ratings yet

- Phil Guaranty V CIR DigestDocument2 pagesPhil Guaranty V CIR DigestMaria Reylan Garcia100% (2)

- Bdo V CirDocument5 pagesBdo V CirAnselmo Rodiel IVNo ratings yet

- Figuerres v. CADocument3 pagesFiguerres v. CAkathrynmaydevezaNo ratings yet

- Chamber of Real Estate and Builders' Assoc. Vs Hon. Exec. Sec. Alberto RomuloDocument2 pagesChamber of Real Estate and Builders' Assoc. Vs Hon. Exec. Sec. Alberto RomuloRhea Mae Lasay-Sumpiao100% (1)

- John Hay Sez v. Lim, 414 Scra 356Document1 pageJohn Hay Sez v. Lim, 414 Scra 356Scrib LawNo ratings yet

- Case 1 Tridharma Marketing Corp. Vs CTA and CIRDocument2 pagesCase 1 Tridharma Marketing Corp. Vs CTA and CIRlenvfNo ratings yet

- Phil. Guaranty Co. v. CIRDocument2 pagesPhil. Guaranty Co. v. CIRIshNo ratings yet

- Atlas Vs CIRDocument2 pagesAtlas Vs CIRRoyalhighness18No ratings yet

- Cir V Gotamco DigestDocument1 pageCir V Gotamco DigestDee LMNo ratings yet

- Philippine Acetylene Co. Inc vs. CirDocument2 pagesPhilippine Acetylene Co. Inc vs. Cirbrendamanganaan100% (1)

- 022 Cir vs. Marubeni Corporation GR No. 137377Document1 page022 Cir vs. Marubeni Corporation GR No. 137377Anonymous MikI28PkJcNo ratings yet

- Smart Vs Malvar Case Digest G.R. No. 204429 February 18, 2014 (Regulatory Purpose)Document2 pagesSmart Vs Malvar Case Digest G.R. No. 204429 February 18, 2014 (Regulatory Purpose)Pre AvanzNo ratings yet

- CIR Vs CTA DigestDocument2 pagesCIR Vs CTA DigestAbilene Joy Dela Cruz83% (6)

- TaxDocument7 pagesTaxArvi April NarzabalNo ratings yet

- Philippine Ports Authority v. The City of DavaoDocument2 pagesPhilippine Ports Authority v. The City of DavaoAlyk Tumayan Calion100% (2)

- PLDT V CirDocument1 pagePLDT V CirDirect LukeNo ratings yet

- Taganito Mining Corporation v. Commissioner of Internal RevenueDocument2 pagesTaganito Mining Corporation v. Commissioner of Internal RevenueRoland MarananNo ratings yet

- Digest Bir Ruling 30-00, 19-01Document3 pagesDigest Bir Ruling 30-00, 19-01Jonathan Ocampo BajetaNo ratings yet

- Philippine Airlines V CIRDocument1 pagePhilippine Airlines V CIRZ FNo ratings yet

- Pal vs. CirDocument2 pagesPal vs. CirKarla BeeNo ratings yet

- Philippine Airlines V CIRDocument5 pagesPhilippine Airlines V CIRBettina Rayos del SolNo ratings yet

- Philippine Airlines v. CIR: SummaryDocument4 pagesPhilippine Airlines v. CIR: SummaryL-Shy KïmNo ratings yet

- Philippine Airlines v. CIR: SummaryDocument4 pagesPhilippine Airlines v. CIR: SummaryUnicorns Are RealNo ratings yet

- Hatch IndictmentDocument29 pagesHatch IndictmentMNRNo ratings yet

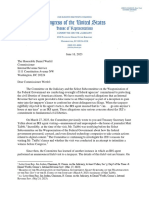

- Jim Jordan Letter To IRS Re: "Highly Concerning" Targeting of TaxpayerDocument4 pagesJim Jordan Letter To IRS Re: "Highly Concerning" Targeting of TaxpayerFedSmith Inc.No ratings yet

- 65 Mitsubishi Co Vs CIRDocument25 pages65 Mitsubishi Co Vs CIRLimberge Paul CorpuzNo ratings yet

- Foreign Trusts, 1998 PDFDocument15 pagesForeign Trusts, 1998 PDFTwonNo ratings yet

- Scam Artists Will Say AnythingDocument3 pagesScam Artists Will Say AnythingRichard100% (1)

- Taxrev Smi-Ed v. CirDocument26 pagesTaxrev Smi-Ed v. CirLudica OjaNo ratings yet

- Atty. Cabaniero Tax QuestionsDocument9 pagesAtty. Cabaniero Tax QuestionsYen Yen NicolasNo ratings yet

- Limpan Investment Corp v. CIR, 17 SCRA 703Document2 pagesLimpan Investment Corp v. CIR, 17 SCRA 703Gabriel Hernandez100% (1)

- Tax Controversies Practice and ProcedureDocument61 pagesTax Controversies Practice and Proceduremelissa.barlowe306100% (46)

- RMC No. 65-2016 PDFDocument3 pagesRMC No. 65-2016 PDFlavyne56No ratings yet

- BIR Citizen - S Charter 2021 EditionDocument999 pagesBIR Citizen - S Charter 2021 EditionRosalie FeraerNo ratings yet

- Effect of Tax Auditing Does The Deterent DeterDocument8 pagesEffect of Tax Auditing Does The Deterent DeterAgnes EvelinaNo ratings yet

- Irs Form 1023Document30 pagesIrs Form 1023Steve Majerus-Collins0% (1)

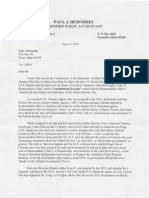

- Letter From Mr. Paul DesfossesDocument2 pagesLetter From Mr. Paul DesfossesPhilHart0% (1)

- Cases JloDocument10 pagesCases JloOwen DefuntaronNo ratings yet

- STL Irr+ (29 09 10)Document13 pagesSTL Irr+ (29 09 10)opa.pmsdNo ratings yet

- Tax Updates by Atty. LumberaDocument68 pagesTax Updates by Atty. Lumberaavery03No ratings yet

- A Survey of Taxation Law Bar Questions 2009 To 2019Document142 pagesA Survey of Taxation Law Bar Questions 2009 To 2019Jessy FrancisNo ratings yet

- APJARBA 2015 1 004 Awareness On BIR E Filing and Payment SystemDocument9 pagesAPJARBA 2015 1 004 Awareness On BIR E Filing and Payment Systemjovelyn labordoNo ratings yet

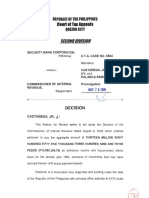

- Coon of Tax Appeals: Second DivisionDocument19 pagesCoon of Tax Appeals: Second DivisionpierremartinreyesNo ratings yet

- Comm. of Customs vs. PH Phosphate FertilizerDocument3 pagesComm. of Customs vs. PH Phosphate FertilizerMara VinluanNo ratings yet

- Pimentel v. Aguirre, Et Al.Document2 pagesPimentel v. Aguirre, Et Al.Noreenesse Santos100% (1)

- 2-dfdDocument15 pages2-dfdjjjj_123No ratings yet

- Uniform Bonding Code (Part 1)Document19 pagesUniform Bonding Code (Part 1)Paschal James BloiseNo ratings yet

- Tambunting Pawnshop Vs CIRDocument10 pagesTambunting Pawnshop Vs CIRMayr TeruelNo ratings yet

- Philex Mining Corporation v. CIRDocument3 pagesPhilex Mining Corporation v. CIRAila AmpNo ratings yet

- Claim For Refund and Request For AbatementDocument1 pageClaim For Refund and Request For AbatementIRSNo ratings yet

- Power Sector Assets and Liabilities Management Corporation, v. Commissioner of InternalDocument4 pagesPower Sector Assets and Liabilities Management Corporation, v. Commissioner of InternalewnesssNo ratings yet