Download as pdf or txt

You might also like

- Musical Acoustics PDFDocument26 pagesMusical Acoustics PDFGino Mendoza0% (1)

- Maybury ManualDocument55 pagesMaybury ManualFriends of MayburyNo ratings yet

- Jolly Grammar Programme P1-6Document8 pagesJolly Grammar Programme P1-6Mandy Whorlow100% (3)

- Et Misericordia - Kim Andre ArnesenDocument9 pagesEt Misericordia - Kim Andre ArnesenMaximos KumaNo ratings yet

- List of Documents NBA PfilesDocument48 pagesList of Documents NBA PfilesDr. A. Pathanjali Sastri100% (1)

- Lab2 PDFDocument3 pagesLab2 PDFMd.Arifur RahmanNo ratings yet

- Jan Feb 2023Document2 pagesJan Feb 2023Keshava PrajwalNo ratings yet

- WR1500lpm@16Bar (2E 1J)Document1 pageWR1500lpm@16Bar (2E 1J)NickIrwingNo ratings yet

- NDT CertificatesDocument4 pagesNDT CertificatesrajeshNo ratings yet

- 2011-1 FinalDocument2 pages2011-1 FinalericlesmauricioNo ratings yet

- Performance Certificate - 2023Document13 pagesPerformance Certificate - 2023Brown builderNo ratings yet

- Chemistry PracticalDocument25 pagesChemistry PracticalJeevikaNo ratings yet

- Binder BDocument9 pagesBinder Bapi-298363828No ratings yet

- TL") .I..others: TinineDocument18 pagesTL") .I..others: TinineEzeldeen AgoryNo ratings yet

- IMG_20240710_0001Document4 pagesIMG_20240710_0001tasnimeshakil98No ratings yet

- IMG_20240710_0001Document4 pagesIMG_20240710_0001tasnimeshakil98No ratings yet

- IMG_20240710_0001Document4 pagesIMG_20240710_0001tasnimeshakil98No ratings yet

- FlyHigh 4 Pupils Book FullDocument130 pagesFlyHigh 4 Pupils Book FullHi TalkNo ratings yet

- Img 20240314 0001Document1 pageImg 20240314 0001juliadebienne1No ratings yet

- Sliders 4 - ManualDocument45 pagesSliders 4 - ManualSamia Sannier100% (3)

- Econ JigsawDocument1 pageEcon Jigsawapi-401505926No ratings yet

- Dr. Princy Matlani Appointment LetterDocument2 pagesDr. Princy Matlani Appointment LettersrpyrhlNo ratings yet

- Local PurchaseDocument1 pageLocal PurchaseTheint Theint OoNo ratings yet

- Address:, - .,: Rder IlsDocument3 pagesAddress:, - .,: Rder IlsRohit Parmar (Computer Operator, Bangalore)No ratings yet

- 2-Sig UzuraDocument9 pages2-Sig UzuraOnofrei LiviuNo ratings yet

- c5 Organic Agricuture StandardsDocument11 pagesc5 Organic Agricuture Standardschan nareinNo ratings yet

- I'!.'.' Irr RT :,'FF:"H,:R#.L" Uj Y ( - F FFH ,,'R Ilij:'I,"Ij:.1Y,".T1"'Il' .J . TDocument1 pageI'!.'.' Irr RT :,'FF:"H,:R#.L" Uj Y ( - F FFH ,,'R Ilij:'I,"Ij:.1Y,".T1"'Il' .J . TRaluca SBNo ratings yet

- 'Totortal: 6tvloiflo CDocument14 pages'Totortal: 6tvloiflo CBinura SenavirathnaNo ratings yet

- Pre Intermediate CoursebookDocument162 pagesPre Intermediate CoursebookAlan LNo ratings yet

- ,/' I Ffivnticl: I - C R: R O R C In:P,:Rta'T - Tirc Pro 1 ' PRRRT (,S: . (6) What Do - You Under:Iiancl BF S.$R"GG - F.:Egs - $3!Ult.V ? Librv Is Ihc Process Mil"Uriiill-AnDocument4 pages,/' I Ffivnticl: I - C R: R O R C In:P,:Rta'T - Tirc Pro 1 ' PRRRT (,S: . (6) What Do - You Under:Iiancl BF S.$R"GG - F.:Egs - $3!Ult.V ? Librv Is Ihc Process Mil"Uriiill-AnMeenu GuptaNo ratings yet

- การออกแบบกำแพงกันดินDocument17 pagesการออกแบบกำแพงกันดินSittinan BenNo ratings yet

- T.Olah Sonata (Analiza)Document5 pagesT.Olah Sonata (Analiza)alexavanguNo ratings yet

- Tanzmusik PartiturDocument6 pagesTanzmusik Partiturmischka4No ratings yet

- Manual SediproDocument21 pagesManual SediproBlancaNo ratings yet

- Eureau Inter) Dai, City: ... I R,, I L,:ri Ri U - AuDocument5 pagesEureau Inter) Dai, City: ... I R,, I L,:ri Ri U - Aunathalie velasquezNo ratings yet

- AjmerDocument6 pagesAjmerMakhdoom Syed Hassan BukhariNo ratings yet

- Img PDFDocument2 pagesImg PDFMd Shahed AliNo ratings yet

- Grammar A L (J (S¡//'LLL'F I .I: ? Euasdty B I DNHT, R¡Ir¡RDocument2 pagesGrammar A L (J (S¡//'LLL'F I .I: ? Euasdty B I DNHT, R¡Ir¡RRoss HCHNo ratings yet

- Lemari Es AndiDocument1 pageLemari Es AndiJohn DaneNo ratings yet

- Acf 0 2 Tiie: Arrnex FR:RDocument1 pageAcf 0 2 Tiie: Arrnex FR:RCliff DaquioagNo ratings yet

- HC Part 1Document10 pagesHC Part 1asksankar7857No ratings yet

- Tema I - Miembros A TesionDocument9 pagesTema I - Miembros A TesionAurora JuvenilNo ratings yet

- Img 20210104 0001Document1 pageImg 20210104 0001GeorgeMarcusNo ratings yet

- Img 20230610 0005Document1 pageImg 20230610 0005Print care ServiceNo ratings yet

- ., D. 4it, L : Ttno49iDocument6 pages., D. 4it, L : Ttno49igetachew negaNo ratings yet

- Manjha CLB SPCL Issue PlansDocument14 pagesManjha CLB SPCL Issue PlansAdamaris CruiseNo ratings yet

- Img 0004Document1 pageImg 0004yana rusdianaNo ratings yet

- EXTRACT DA 2, Dapur Hotel, Restoran, Kamar Hotel.Document13 pagesEXTRACT DA 2, Dapur Hotel, Restoran, Kamar Hotel.Zaky Abrallian AdamNo ratings yet

- Ffi&ffii : of As AreDocument7 pagesFfi&ffii : of As AreSwetaMallickNo ratings yet

- Musnad Abu YaAla AlMusali Jild 1Document759 pagesMusnad Abu YaAla AlMusali Jild 1javeria jamilNo ratings yet

- Graded Level 3ADocument11 pagesGraded Level 3ANurul Atikah HashimNo ratings yet

- Img 20200618 0001Document2 pagesImg 20200618 0001Mohammad FalakhuddinNo ratings yet

- 7 UnlockedDocument23 pages7 UnlockedahggggggggmedNo ratings yet

- Sonatina Meridional PonceDocument9 pagesSonatina Meridional PonceCUloNo ratings yet

- Đội VI Trùng 731. 1987Document211 pagesĐội VI Trùng 731. 1987n6skhydysqNo ratings yet

- ,ii - L R:: (F 6f &.I, IDocument1 page,ii - L R:: (F 6f &.I, ISubhash KorumilliNo ratings yet

- Book Menggubah Nyanyian JemaatDocument57 pagesBook Menggubah Nyanyian JemaatharmintoNo ratings yet

- ACFrOgD4nCzzEsuSQpI KTT B2bC7BAyIhNdh1N6ohdH0K09bChNVTpnyVnKHcHE7lg6ny574Du26BeTY2eO OVfPWmvqq9Z878phoY08AiaP9nUytctKCZCsJudj g1PWmlWVhgjAmuDwrv197GDocument1 pageACFrOgD4nCzzEsuSQpI KTT B2bC7BAyIhNdh1N6ohdH0K09bChNVTpnyVnKHcHE7lg6ny574Du26BeTY2eO OVfPWmvqq9Z878phoY08AiaP9nUytctKCZCsJudj g1PWmlWVhgjAmuDwrv197GBia IvascuNo ratings yet

- Deewan e Syedul Bat-Ha Hazrat Abu Talib (As)Document441 pagesDeewan e Syedul Bat-Ha Hazrat Abu Talib (As)Syed-Rizwan RizviNo ratings yet

- Qjnww@#wny: L::::: - IilDocument1 pageQjnww@#wny: L::::: - IilEmdad HamidNo ratings yet

- 757 RokeyaDocument1 page757 RokeyaEmdad HamidNo ratings yet

- Benjamin, Arthur L. Suite For Piano (1927)Document23 pagesBenjamin, Arthur L. Suite For Piano (1927)EwkorngoldNo ratings yet

- Image 034Document5 pagesImage 034زهراء احمد محمدNo ratings yet

- CL2002 15Document1 pageCL2002 15Carlo Garcia, CPANo ratings yet

- Qfiii#': GovernanceDocument12 pagesQfiii#': GovernanceCarlo Garcia, CPANo ratings yet

- CL2001 01Document8 pagesCL2001 01Carlo Garcia, CPANo ratings yet

- Manila: IetificationsDocument4 pagesManila: IetificationsCarlo Garcia, CPANo ratings yet

- Fuil K-Ffi,. w3: ManilaDocument13 pagesFuil K-Ffi,. w3: ManilaCarlo Garcia, CPANo ratings yet

- Man:i1a: in in ofDocument6 pagesMan:i1a: in in ofCarlo Garcia, CPANo ratings yet

- All In: Rates" For AprilDocument1 pageAll In: Rates" For AprilCarlo Garcia, CPANo ratings yet

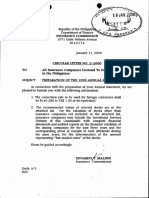

- Republic of Philippines: Department of Finance Insurance Commission 1071 United Nations Avenue ManilaDocument3 pagesRepublic of Philippines: Department of Finance Insurance Commission 1071 United Nations Avenue ManilaCarlo Garcia, CPANo ratings yet

- CL2018 69Document3 pagesCL2018 69Carlo Garcia, CPANo ratings yet

- IASB Agrees Re-Deliberation Plan For Amendments To Ifrs 17: Insurance Accounting AlertDocument9 pagesIASB Agrees Re-Deliberation Plan For Amendments To Ifrs 17: Insurance Accounting AlertCarlo Garcia, CPANo ratings yet

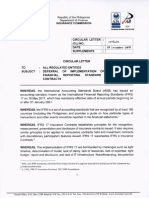

- SEC Memorandum Circular No. 08 S. 2020Document3 pagesSEC Memorandum Circular No. 08 S. 2020Carlo Garcia, CPANo ratings yet

- Ordinary People Summary ChartDocument2 pagesOrdinary People Summary Chartangela_cristiniNo ratings yet

- GIDC Rajju Shroff ROFEL Institute of Management Studies: Subject:-CRVDocument7 pagesGIDC Rajju Shroff ROFEL Institute of Management Studies: Subject:-CRVIranshah MakerNo ratings yet

- TG0012 enDocument24 pagesTG0012 enDhexter VillaNo ratings yet

- A Bravo Delta Lancaster Model Worth 329: 38 Paralle L Paralle LDocument116 pagesA Bravo Delta Lancaster Model Worth 329: 38 Paralle L Paralle LAnonymous 7Je2SSU100% (2)

- Dual-Band Wearable Rectenna For Low-Power RF Energy HarvestingDocument10 pagesDual-Band Wearable Rectenna For Low-Power RF Energy HarvestingbabuNo ratings yet

- Study of Blood Groups and Rhesus Factor in Beta Thalassemia Patients Undergoing Blood TransfusionsDocument6 pagesStudy of Blood Groups and Rhesus Factor in Beta Thalassemia Patients Undergoing Blood TransfusionsOpenaccess Research paperNo ratings yet

- Welspun Linen Customer Price List 2023Document4 pagesWelspun Linen Customer Price List 2023Vipin SharmaNo ratings yet

- GIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedDocument11 pagesGIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedemmanuelNo ratings yet

- The Law of ParkinsonDocument5 pagesThe Law of Parkinsonathanassiadis2890No ratings yet

- The Entrepreneurial and Entrepreneurial Mind: Week #2Document20 pagesThe Entrepreneurial and Entrepreneurial Mind: Week #2Mr.BaiGNo ratings yet

- Analysis of Old Trends in Indian Wine-Making and Need of Expert System in Wine-MakingDocument10 pagesAnalysis of Old Trends in Indian Wine-Making and Need of Expert System in Wine-MakingIJRASETPublicationsNo ratings yet

- Internet Banking Java Project ReportDocument68 pagesInternet Banking Java Project ReportKUMAR NILESH100% (1)

- Whyte Human Rights and The Collateral Damage oDocument16 pagesWhyte Human Rights and The Collateral Damage ojswhy1No ratings yet

- Essay by MariemDocument2 pagesEssay by MariemMatthew MaxwellNo ratings yet

- Security and Privacy Issues: A Survey On Fintech: (Kg71231W, Mqiu, Xs43599N) @pace - EduDocument12 pagesSecurity and Privacy Issues: A Survey On Fintech: (Kg71231W, Mqiu, Xs43599N) @pace - EduthebestNo ratings yet

- Ferdinando Carulli - Op 121, 24 Pieces - 4. Anglaise in A MajorDocument2 pagesFerdinando Carulli - Op 121, 24 Pieces - 4. Anglaise in A MajorOniscoidNo ratings yet

- Term Paper (Dev - Econ-2)Document14 pagesTerm Paper (Dev - Econ-2)acharya.arpan08No ratings yet

- Sap Fico Blueprint-1Document32 pagesSap Fico Blueprint-1Deepak AggarwalNo ratings yet

- Steve Nison - Candlestick Patterns - RezumatDocument22 pagesSteve Nison - Candlestick Patterns - RezumatSIightlyNo ratings yet

- Loi Bayanihan PCR ReviewerDocument15 pagesLoi Bayanihan PCR Reviewerailexcj20No ratings yet

- Data Sheets Ecc I On AdoraDocument23 pagesData Sheets Ecc I On AdoraAlanAvtoNo ratings yet

- LEARNING THEORIES Ausubel's Learning TheoryDocument17 pagesLEARNING THEORIES Ausubel's Learning TheoryCleoNo ratings yet

- William Angelo - Week-7.AssessmentDocument2 pagesWilliam Angelo - Week-7.Assessmentsup shawtyNo ratings yet

- Study Session8Document1 pageStudy Session8MOSESNo ratings yet

- Computer Awareness Topic Wise - TerminologiesDocument15 pagesComputer Awareness Topic Wise - TerminologiesdhirajNo ratings yet

- List Peserta Swab Antigen - 5 Juni 2021Document11 pagesList Peserta Swab Antigen - 5 Juni 2021minhyun hwangNo ratings yet