Download as docx, pdf, or txt

You might also like

- Economics: Market ScenariosDocument3 pagesEconomics: Market ScenariosOsiris HernandezNo ratings yet

- Chapter 1 - Financial Reporting and Accounting Standards - Intermediate Accounting - IFRS Edition, 2nd EditionDocument41 pagesChapter 1 - Financial Reporting and Accounting Standards - Intermediate Accounting - IFRS Edition, 2nd EditionWihl Mathew ZalatarNo ratings yet

- Bsbfim601 Manage Finances Monitor and Review BudgetDocument7 pagesBsbfim601 Manage Finances Monitor and Review BudgetAli Butt100% (7)

- Individual AssignmentDocument6 pagesIndividual AssignmentFurkanNo ratings yet

- The Rise of The Deferred Tax Assets in JapanDocument57 pagesThe Rise of The Deferred Tax Assets in Japanpaliacho77No ratings yet

- 12 - Summary and ConclusionDocument13 pages12 - Summary and ConclusionJanak SinghNo ratings yet

- Ifrs Japan GaapDocument54 pagesIfrs Japan Gaapaqua01No ratings yet

- Effect of Creative Accounting On Shareholders Wealth Among Listed Deposited Banks in NigeriaDocument52 pagesEffect of Creative Accounting On Shareholders Wealth Among Listed Deposited Banks in Nigeriaadewale abiodunNo ratings yet

- ACC 805 Public Sector Accountig-Course Outline June 2021Document2 pagesACC 805 Public Sector Accountig-Course Outline June 2021Kehinde OjoNo ratings yet

- IPSAS BriefDocument8 pagesIPSAS BriefAshfaque LarikNo ratings yet

- AS Dita - IfRS As A Guide To Overcome Challenges in International AccountingDocument9 pagesAS Dita - IfRS As A Guide To Overcome Challenges in International AccountingYor AdeNo ratings yet

- KB Agt Nina 752 1671184347 681 PDFDocument10 pagesKB Agt Nina 752 1671184347 681 PDFHero PratikNo ratings yet

- A Study of Recent Accounting Trends in India's Corporate Sector With Special Reference To International Financial Reporting StandardsDocument9 pagesA Study of Recent Accounting Trends in India's Corporate Sector With Special Reference To International Financial Reporting StandardsManagement Journal for Advanced ResearchNo ratings yet

- E - Content On IFRSDocument20 pagesE - Content On IFRSPranit Satyavan NaikNo ratings yet

- Research Group ADocument7 pagesResearch Group ATedros BelaynehNo ratings yet

- Effect of Creative Accounting On Shareholders Wealth Among Listed Deposited Banks in NigeriaDocument40 pagesEffect of Creative Accounting On Shareholders Wealth Among Listed Deposited Banks in Nigeriaadewale abiodunNo ratings yet

- Book-Tax Income Differences and Major Determining FactorsDocument11 pagesBook-Tax Income Differences and Major Determining FactorsFbsdf SdvsNo ratings yet

- Accounting in China: I. Legal FrameworkDocument5 pagesAccounting in China: I. Legal Frameworkdev_thecoolboyNo ratings yet

- Chapter One: Globalization and Trade Liberalization HaveDocument7 pagesChapter One: Globalization and Trade Liberalization HaveImmanuel Billie AllenNo ratings yet

- Professional Pronouncement On Public Sector Accounting, Economic and Financial ImplicationDocument53 pagesProfessional Pronouncement On Public Sector Accounting, Economic and Financial ImplicationGodfrey MosesNo ratings yet

- Chapter One Accounting Principles and Professional PracticeDocument22 pagesChapter One Accounting Principles and Professional PracticeHussen Abdulkadir100% (1)

- International Public Sector Accounting Standards and Financial Reporting in Nigeria: Answers To Implementation QuestionsDocument5 pagesInternational Public Sector Accounting Standards and Financial Reporting in Nigeria: Answers To Implementation QuestionsIOSRjournalNo ratings yet

- The Effect of International Public Sector Accounting Standard (IPSAS) Implementation and Public Financial Management in NigeriaDocument10 pagesThe Effect of International Public Sector Accounting Standard (IPSAS) Implementation and Public Financial Management in NigeriaaijbmNo ratings yet

- Far 600 Q&aDocument41 pagesFar 600 Q&aRaja AinNo ratings yet

- Economic Development in Japan - FinalDocument9 pagesEconomic Development in Japan - FinalstanomjuguuNo ratings yet

- COMPARISON OF IFRS AND GAAP REPORTONG STANDARDS Case Study On Abay BankDocument29 pagesCOMPARISON OF IFRS AND GAAP REPORTONG STANDARDS Case Study On Abay BanknigusNo ratings yet

- Toring J. BibliographyDocument7 pagesToring J. BibliographyJessa Dela Rosa ToringNo ratings yet

- Financiarización y DesigualdadDocument27 pagesFinanciarización y DesigualdadArturo Martínez BareaNo ratings yet

- An OLS Approach To Modelling The Determinants of Private Investment in GhanaDocument26 pagesAn OLS Approach To Modelling The Determinants of Private Investment in GhanaMirza MustafaNo ratings yet

- Week 1 Accounting For Governmental Standards and GAAP Hierarchy - ACTG343Document10 pagesWeek 1 Accounting For Governmental Standards and GAAP Hierarchy - ACTG343Marilou Arcillas PanisalesNo ratings yet

- Cafr in Case of The Governmental AccountingDocument7 pagesCafr in Case of The Governmental Accountingmanita jainNo ratings yet

- Cafr in Case of The Governmental AccountingDocument7 pagesCafr in Case of The Governmental Accountingmanita jainNo ratings yet

- AssignmentDocument15 pagesAssignmentAngieNo ratings yet

- CFA - Diversity of Financial Acc. PracticesDocument16 pagesCFA - Diversity of Financial Acc. PracticesDhea Nanda ChristaliaNo ratings yet

- Must Read BOPDocument22 pagesMust Read BOPAnushkaa DattaNo ratings yet

- Impact of International Public Sector Accounting Standards On Financial Statements in NigeriaDocument10 pagesImpact of International Public Sector Accounting Standards On Financial Statements in NigeriaEmmanuel OlanrewajuNo ratings yet

- Determinants of Tax Revenue - A Case of Nigeria - Ishola & OthersDocument10 pagesDeterminants of Tax Revenue - A Case of Nigeria - Ishola & Otherspriyanthikadilrukshi05No ratings yet

- Lover Rings - LSC - Accounting For Business - Accounting ConceptsDocument5 pagesLover Rings - LSC - Accounting For Business - Accounting ConceptsNazmul AlamNo ratings yet

- Peran Akuntansi Dalam Meningkatkan Kesadaran Permasalahan Keuangan Negara Indonesia (Autorecovered)Document7 pagesPeran Akuntansi Dalam Meningkatkan Kesadaran Permasalahan Keuangan Negara Indonesia (Autorecovered)dewaedison0No ratings yet

- Japan AccountingDocument14 pagesJapan AccountingAzure Pear HaNo ratings yet

- Revenue Recognition Paradox: A Review of IAS 18 and IFRS 15: SSRN Electronic Journal January 2016Document26 pagesRevenue Recognition Paradox: A Review of IAS 18 and IFRS 15: SSRN Electronic Journal January 2016JohnNo ratings yet

- Requirements For Reaching Accounting Harmonization: Research ArticleDocument8 pagesRequirements For Reaching Accounting Harmonization: Research Article*iNo ratings yet

- Sistemul Contabil JaponezDocument28 pagesSistemul Contabil JaponezLina MandarinaNo ratings yet

- 9097-32810-3-PB PDFDocument16 pages9097-32810-3-PB PDFRenaNo ratings yet

- Chapter OneDocument56 pagesChapter OneKamal MoyerNo ratings yet

- The Causes and Implication of Delayed Passage of 2018 Budget On The Nigerias Economic Recovery and Growth PlanDocument6 pagesThe Causes and Implication of Delayed Passage of 2018 Budget On The Nigerias Economic Recovery and Growth PlanIJAR JOURNALNo ratings yet

- Final Seminar 4Document20 pagesFinal Seminar 4Sumit GuptaNo ratings yet

- Pawlose SorsaDocument17 pagesPawlose SorsaBarnababas BeyeneNo ratings yet

- Interim Financial Reporting & Compliance With SEBIs Guidelines The Case of India's Financial Industry - GIBS Bangalore - Top B-School in BangaloreDocument10 pagesInterim Financial Reporting & Compliance With SEBIs Guidelines The Case of India's Financial Industry - GIBS Bangalore - Top B-School in BangalorePradeep KhadariaNo ratings yet

- Group 1 - International Accounting Comparative Accounting The Americas and AsiaDocument23 pagesGroup 1 - International Accounting Comparative Accounting The Americas and AsiaAlmaliyana BasyaibanNo ratings yet

- LESSON 1 Introduction To Accounting LectureDocument3 pagesLESSON 1 Introduction To Accounting LectureACCOUNTING STRESSNo ratings yet

- Pertemuan 10 - Utama Disclosure Evidence MUDocument5 pagesPertemuan 10 - Utama Disclosure Evidence MUroroewiNo ratings yet

- Full Download Book International Financial Management Second Custom Edition For University of Groningen PDFDocument41 pagesFull Download Book International Financial Management Second Custom Edition For University of Groningen PDFjanet.conaway420100% (24)

- Fundamental of Accounting: Bestari Dwi HandayaniDocument9 pagesFundamental of Accounting: Bestari Dwi Handayaniferonikalarasati100% (1)

- Adoption of International Financial Reporting Standards in Bangladesh: Benefits and ChallengesDocument16 pagesAdoption of International Financial Reporting Standards in Bangladesh: Benefits and ChallengesSheikh RubelNo ratings yet

- The Adaptability of Accrual Accounting in The Public SectorDocument15 pagesThe Adaptability of Accrual Accounting in The Public Sectoriyika4real8671No ratings yet

- Economics - II Project - Sumant Meena (217055) & Himanshu Cheeta (217089)Document31 pagesEconomics - II Project - Sumant Meena (217055) & Himanshu Cheeta (217089)Himanshu CheetaNo ratings yet

- FRA MaterialDocument35 pagesFRA Materialelitesquad9432No ratings yet

- The Corporate Tax Planning and Financial Performance of Systemically Important Banks in NigeriaDocument13 pagesThe Corporate Tax Planning and Financial Performance of Systemically Important Banks in NigeriaMohammad Rakibul IslamNo ratings yet

- A Study On The Impact of International Financial Reporting Standards Convergence On Indian Corporate SectorDocument8 pagesA Study On The Impact of International Financial Reporting Standards Convergence On Indian Corporate SectorKiran KumarNo ratings yet

- Guide to Management Accounting CCC (Cash Conversion Cycle) for ManagersFrom EverandGuide to Management Accounting CCC (Cash Conversion Cycle) for ManagersNo ratings yet

- Guide to Management Accounting CCC for managers-Cash Conversion Cycle_2020 EditionFrom EverandGuide to Management Accounting CCC for managers-Cash Conversion Cycle_2020 EditionNo ratings yet

- Advanced Financial Accounting: AssetsDocument2 pagesAdvanced Financial Accounting: AssetsPrabavathi KarunanithiNo ratings yet

- Advance Financial Accounting: BMAF 33104Document11 pagesAdvance Financial Accounting: BMAF 33104Prabavathi KarunanithiNo ratings yet

- 376Cbs Advanced Financial Accounting & Reporting Business Combinations Example Sheet 3 - SolutionsDocument10 pages376Cbs Advanced Financial Accounting & Reporting Business Combinations Example Sheet 3 - SolutionsPrabavathi KarunanithiNo ratings yet

- Advanced Financial Accounting: AssetsDocument9 pagesAdvanced Financial Accounting: AssetsPrabavathi KarunanithiNo ratings yet

- Alpha + Subs OnlyDocument8 pagesAlpha + Subs OnlyPrabavathi KarunanithiNo ratings yet

- Assignment #1 March 2020 Semester: Advanced Financial AccountingDocument11 pagesAssignment #1 March 2020 Semester: Advanced Financial AccountingPrabavathi KarunanithiNo ratings yet

- Example Sheet 2 AfaDocument4 pagesExample Sheet 2 AfaPrabavathi KarunanithiNo ratings yet

- Assignment March 2020 Semester: 1222 WordsDocument12 pagesAssignment March 2020 Semester: 1222 WordsPrabavathi KarunanithiNo ratings yet

- Statement of HE Mahinda Rajapakse, The Prime Minister and Finance Minister of Sri Lanka On The World Accreditation Day 2021Document2 pagesStatement of HE Mahinda Rajapakse, The Prime Minister and Finance Minister of Sri Lanka On The World Accreditation Day 2021Adaderana OnlineNo ratings yet

- Chapter 5. An Introduction Investment Appraisal TechniquesDocument10 pagesChapter 5. An Introduction Investment Appraisal TechniquesHastings KapalaNo ratings yet

- Brochure Timberline Collection RESTL100Document20 pagesBrochure Timberline Collection RESTL100Orlando MunozNo ratings yet

- 3rd Term Lesson Note For Ss2 On EconomicsDocument24 pages3rd Term Lesson Note For Ss2 On Economicslukajoy082No ratings yet

- Menegaki and Damigos 2018 A Review On Current Situation and Challenges of Construction and Demolition Waste ManagementDocument19 pagesMenegaki and Damigos 2018 A Review On Current Situation and Challenges of Construction and Demolition Waste ManagementBurak BulutNo ratings yet

- The Lemons MarketDocument20 pagesThe Lemons Marketshahin317No ratings yet

- R PosDocument2 pagesR PosAvinash Chandra MishraNo ratings yet

- (Clean) CREATE MORE Act - Plenary Substitute Bill - Asof30jan2024Document32 pages(Clean) CREATE MORE Act - Plenary Substitute Bill - Asof30jan2024marlon.rondainNo ratings yet

- Introduction and Types of BanksDocument7 pagesIntroduction and Types of BanksshahzaibNo ratings yet

- Consultancy Contract Awards 2018Document17 pagesConsultancy Contract Awards 2018kamogelo MolalaNo ratings yet

- Fin 358: Chapter 1: Introduction To Investment - Erimalida YaziDocument10 pagesFin 358: Chapter 1: Introduction To Investment - Erimalida YaziHannaJoyCarlaMendozaNo ratings yet

- Topic 7-ValuationDocument36 pagesTopic 7-ValuationK60 Nguyễn Ngọc Quế AnhNo ratings yet

- 2020 Landfill Capacity Calculation Work SheetDocument4 pages2020 Landfill Capacity Calculation Work SheetLYNo ratings yet

- PNB v. San Miguel Corporation DigestDocument1 pagePNB v. San Miguel Corporation DigestAprilNo ratings yet

- 19Th Century Philippines: As Rizal'S ContextDocument17 pages19Th Century Philippines: As Rizal'S ContextMisor FireNo ratings yet

- Moahllah Mohammad Khel, P/O Yarhussain Village Yarhussain, TEHSIL RAZZAR, Swabi Swabi Liaqat Ali KhanDocument4 pagesMoahllah Mohammad Khel, P/O Yarhussain Village Yarhussain, TEHSIL RAZZAR, Swabi Swabi Liaqat Ali Khanzahid khanNo ratings yet

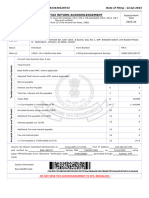

- Indian Income Tax Return Acknowledgement: Acknowledgement Number:438523430120723 Date of Filing: 12-Jul-2023Document1 pageIndian Income Tax Return Acknowledgement: Acknowledgement Number:438523430120723 Date of Filing: 12-Jul-2023kambojnaresh693No ratings yet

- Good Man Wave TheoryDocument20 pagesGood Man Wave TheorySantoso Adiputra Mulyadi100% (2)

- Pengaruh Infrastruktur Publik Terhadap Pertumbuhan Ekonomi Di Kota LangsaDocument8 pagesPengaruh Infrastruktur Publik Terhadap Pertumbuhan Ekonomi Di Kota LangsaanneNo ratings yet

- Brezhnev: Domestic and Foreign Policies Study Guide: SummaryDocument2 pagesBrezhnev: Domestic and Foreign Policies Study Guide: SummaryebhartneyNo ratings yet

- Math108x Document w04GroupAssignmentBudgeting ADocument16 pagesMath108x Document w04GroupAssignmentBudgeting AMatthew MacaballugNo ratings yet

- Plaridel Bypass DPWHDocument2 pagesPlaridel Bypass DPWHHenson CoNo ratings yet

- FX MKT Insights Jun2010 Rosenberg PDFDocument27 pagesFX MKT Insights Jun2010 Rosenberg PDFsuksesNo ratings yet

- SetcDocument3 pagesSetcsindhusmNo ratings yet

- Baby Doge: WhitepaperDocument14 pagesBaby Doge: WhitepaperReezQeyNo ratings yet

- List of Suppliers 2022Document7 pagesList of Suppliers 2022Fatma AhmedNo ratings yet

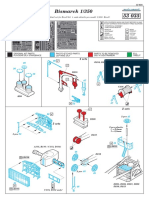

- 1-350 Bismarck For RevellDocument12 pages1-350 Bismarck For RevellDoru SicoeNo ratings yet

- Pob TestDocument5 pagesPob Testselina fraserNo ratings yet