Download as docx, pdf, or txt

You might also like

- LIC Receipt PDFDocument2 pagesLIC Receipt PDFRahul Kumar73% (33)

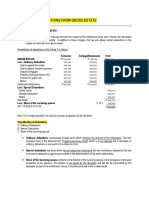

- Module 1 - Deductions From Gross EstateDocument68 pagesModule 1 - Deductions From Gross EstateKat Miranda100% (1)

- Sample Interim Payment ApplicationDocument1 pageSample Interim Payment ApplicationKasun Dulanjana100% (1)

- Chapter Exercises DeductionsDocument11 pagesChapter Exercises DeductionsShaine KeefeNo ratings yet

- Deductions From Gross EstateDocument31 pagesDeductions From Gross EstateXin Zhao50% (2)

- Chapter 7Document7 pagesChapter 7张心怡No ratings yet

- 15gift and Estate Tax - Katzenstein - Fall 2002Document95 pages15gift and Estate Tax - Katzenstein - Fall 2002proveitwasmeNo ratings yet

- Deductions From Gross EstateDocument20 pagesDeductions From Gross EstateJamaica David100% (2)

- DEDUCTIONSDocument21 pagesDEDUCTIONSlet me live in peaceNo ratings yet

- Module 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Document35 pagesModule 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Venice Marie ArroyoNo ratings yet

- Chapter 14Document13 pagesChapter 14Team MindanaoNo ratings yet

- M5 - Deductions From Gross Estate - Students'Document33 pagesM5 - Deductions From Gross Estate - Students'micaella pasionNo ratings yet

- AEC 215 Week 3 HandoutsDocument7 pagesAEC 215 Week 3 HandoutsKeith Chea Pace CobradorNo ratings yet

- Deductions From Gross EstateDocument55 pagesDeductions From Gross EstateMa Aragil Valentine JomocNo ratings yet

- TRAIN On ESTATE TAXATIONDocument6 pagesTRAIN On ESTATE TAXATIONCanapi AmerahNo ratings yet

- Deduction From The Gross EstateDocument6 pagesDeduction From The Gross EstateEmma Mariz GarciaNo ratings yet

- Taxation Review Atty Lock-Transfer Tax ClaveriacadDocument8 pagesTaxation Review Atty Lock-Transfer Tax Claveriacadamor claveriaNo ratings yet

- Deductions From Gross EstateDocument3 pagesDeductions From Gross EstateMark Lawrence YusiNo ratings yet

- 03 Deductions From Gross EstateDocument4 pages03 Deductions From Gross Estatelemvin121003No ratings yet

- Module 2 - Estate TaxDocument14 pagesModule 2 - Estate TaxHaidee Flavier SabidoNo ratings yet

- Deductions From Gross EstateDocument31 pagesDeductions From Gross EstateKristabel MicutuanNo ratings yet

- Deductions On Gross Estate Part 1Document19 pagesDeductions On Gross Estate Part 1Angel Clarisse JariolNo ratings yet

- Deductions From Gross EstateDocument112 pagesDeductions From Gross EstateLuna CakesNo ratings yet

- Tax2 - Estate Tax - Deductions AllowedDocument31 pagesTax2 - Estate Tax - Deductions AllowedMelady Sison CequeñaNo ratings yet

- Ordinary DeductionDocument1 pageOrdinary DeductionXhaNo ratings yet

- Estate Taxation Net Distrubatable Estate Versus Net Taxable EstateDocument10 pagesEstate Taxation Net Distrubatable Estate Versus Net Taxable EstateNaja MadineNo ratings yet

- U1.3 Introduction To Income Taxation 2 U1.4 Tax Accounting MethodsDocument17 pagesU1.3 Introduction To Income Taxation 2 U1.4 Tax Accounting Methodsfrancis dungcaNo ratings yet

- ReviewerDocument4 pagesReviewerQueen Juliana G. TambaoanNo ratings yet

- Itemized Deductions - Taxes Paid 2021Document2 pagesItemized Deductions - Taxes Paid 2021Finn KevinNo ratings yet

- Chapter 13 REGULAR ALLOWABLE ITEMIZED DEDUCTIONSDocument3 pagesChapter 13 REGULAR ALLOWABLE ITEMIZED DEDUCTIONSAlyssa BerangberangNo ratings yet

- Taxation 2 Review AssessmentDocument11 pagesTaxation 2 Review AssessmentaverellabrasaldoNo ratings yet

- Session 6 Exercise DrillDocument3 pagesSession 6 Exercise DrillAbigail Ann PasiliaoNo ratings yet

- EstateDocument6 pagesEstateMarjorie IsonNo ratings yet

- Allowable Dedcutions From Gross EstateDocument51 pagesAllowable Dedcutions From Gross EstatefredNo ratings yet

- TAXATION 2 Chapter 4 Estate Tax Deductions From Gross EstateDocument8 pagesTAXATION 2 Chapter 4 Estate Tax Deductions From Gross EstateKim Cristian MaañoNo ratings yet

- Tax Lectures TranscribeDocument29 pagesTax Lectures TranscribeNeri DelfinNo ratings yet

- Estate Tax: Taxation 1Document22 pagesEstate Tax: Taxation 1Jess Guiang CasamorinNo ratings yet

- Transfer Taxation (CH 5 Deductions From Gross Estate)Document8 pagesTransfer Taxation (CH 5 Deductions From Gross Estate)Dahyun DahyunNo ratings yet

- Deductions From Gross EstateDocument34 pagesDeductions From Gross Estatesmosaldana.cvtNo ratings yet

- Module 2 - Estate TaxDocument16 pagesModule 2 - Estate TaxMaryrose SumulongNo ratings yet

- Estate TaxationDocument8 pagesEstate TaxationUbalda AbuboNo ratings yet

- Estate TaxDocument6 pagesEstate TaxElla CastilloNo ratings yet

- Estate Tax Notes LimDocument5 pagesEstate Tax Notes LimAustine Clarese VelascoNo ratings yet

- Citizen & Resident Within Without Within Within Within Within Within Within Within WithinDocument4 pagesCitizen & Resident Within Without Within Within Within Within Within Within Within WithinVon Andrei MedinaNo ratings yet

- Demo TeachingDocument2 pagesDemo TeachingPrincess Jane SuatNo ratings yet

- A. in Case of Resident Citizens, Nonresident Citizens and Resident AliensDocument2 pagesA. in Case of Resident Citizens, Nonresident Citizens and Resident AlienschosNo ratings yet

- Estate TaxationDocument8 pagesEstate TaxationVincent Fedrick G. LingaNo ratings yet

- Deduction From The Gross EstateDocument5 pagesDeduction From The Gross Estaterorrory683No ratings yet

- Chapter 3Document39 pagesChapter 3Rygiem Dela CruzNo ratings yet

- Estate Donors Taxation 1Document8 pagesEstate Donors Taxation 1Benjamin dela Cruz Cailao IIINo ratings yet

- Business TaxDocument7 pagesBusiness TaxCamille Torrejas ManatadNo ratings yet

- Transfer TaxesDocument5 pagesTransfer TaxesJohn Lester LantinNo ratings yet

- Chapter 6 Deductions From The Gross Estate PDFDocument7 pagesChapter 6 Deductions From The Gross Estate PDFDudz MatienzoNo ratings yet

- Estate - Donors TaxationDocument10 pagesEstate - Donors TaxationJames RelletaNo ratings yet

- Taxation Law II Green NotesDocument126 pagesTaxation Law II Green NotesNewCovenantChurchNo ratings yet

- Co-Ownership, Estate and TrustDocument6 pagesCo-Ownership, Estate and TrustRyan Christian Balanquit100% (2)

- Transfer TaxesDocument7 pagesTransfer TaxesDesiree Ann MiralNo ratings yet

- TAX May2021 1st Preboard Questions PDFDocument7 pagesTAX May2021 1st Preboard Questions PDFGoze, Cassandra Jane0% (1)

- F6 Iht Fa19Document18 pagesF6 Iht Fa19Wajih RehmanNo ratings yet

- Gutierrez v. Collector PDFDocument23 pagesGutierrez v. Collector PDFnichols greenNo ratings yet

- Deductions From The Gross EstateDocument14 pagesDeductions From The Gross Estatejungoos100% (1)

- The King Takes Your Castle: City Laws That Restrict Your Property RightsFrom EverandThe King Takes Your Castle: City Laws That Restrict Your Property RightsNo ratings yet

- TaxiDocument12 pagesTaxiKaiden AmaruNo ratings yet

- The Ten CommandmentsDocument3 pagesThe Ten CommandmentsKaiden AmaruNo ratings yet

- Regression QuizDocument2 pagesRegression QuizKaiden AmaruNo ratings yet

- Entrepreneurship - : EntrepreneurDocument2 pagesEntrepreneurship - : EntrepreneurKaiden AmaruNo ratings yet

- Capitalizing On Global and Regional IntegrationDocument2 pagesCapitalizing On Global and Regional IntegrationKaiden AmaruNo ratings yet

- Air Corporation Ad PDFDocument1 pageAir Corporation Ad PDFKaiden AmaruNo ratings yet

- StrengthDocument2 pagesStrengthKaiden AmaruNo ratings yet

- Implementation of Fsuu College Announcement Notification SystemDocument4 pagesImplementation of Fsuu College Announcement Notification SystemKaiden AmaruNo ratings yet

- 1.daftar Akun Dan Saldo Awal NeracaDocument2 pages1.daftar Akun Dan Saldo Awal NeracaHendri awanNo ratings yet

- View Yemi Invoice - ReceiptDocument1 pageView Yemi Invoice - ReceiptOBEMBE AYODELENo ratings yet

- 252289600057294Document1 page252289600057294Pricila MercyNo ratings yet

- Bansal BillDocument1 pageBansal Billwanna.wohNo ratings yet

- Revenue Regulations 9-98Document5 pagesRevenue Regulations 9-98Kayzer SabaNo ratings yet

- Tax Receipt Transport Department, Government of West Bengal Registration Authority MATHABHANGA ARTO, West BengalDocument1 pageTax Receipt Transport Department, Government of West Bengal Registration Authority MATHABHANGA ARTO, West BengalPawan KumarNo ratings yet

- Confirmation of Payment - First Deposit 14 Jan 2021Document1 pageConfirmation of Payment - First Deposit 14 Jan 2021emmanuel santoyo rioNo ratings yet

- Credit Transaction Codes Description Debit Transaction Codes Description Current AccountDocument1 pageCredit Transaction Codes Description Debit Transaction Codes Description Current AccountHakuna MatataNo ratings yet

- A Brief History of Money - 22sept2021Document44 pagesA Brief History of Money - 22sept2021Mj RodriguesNo ratings yet

- CP575Notice 1630515078861Document2 pagesCP575Notice 1630515078861Serkan idilNo ratings yet

- Foa Ii Individual AssignmentDocument3 pagesFoa Ii Individual Assignmentyosef mechalNo ratings yet

- Assignment 3 TAX3702Document3 pagesAssignment 3 TAX3702GenevieveNo ratings yet

- J. P. Morgan Chase: Tax CalculatorDocument1 pageJ. P. Morgan Chase: Tax Calculatoranon-930095No ratings yet

- CIR vs. Pineda, 21 SCRA 105Document1 pageCIR vs. Pineda, 21 SCRA 105SURITA, FLOR DE MAE PNo ratings yet

- Chapter 6 Accounting For Income Collections and Related TransactionsDocument3 pagesChapter 6 Accounting For Income Collections and Related TransactionsJapsNo ratings yet

- July 2023Document1 pageJuly 2023heliaha266No ratings yet

- Reliance Infrastructure Fund - NFO - Application Form & KIM-DOWNLOADDocument4 pagesReliance Infrastructure Fund - NFO - Application Form & KIM-DOWNLOADvinodNo ratings yet

- 2023 10 22 16 34 45sep 23 - 122001Document7 pages2023 10 22 16 34 45sep 23 - 122001Neha YadavNo ratings yet

- SubhashDocument1 pageSubhashsubhash221103No ratings yet

- Flipkart Labels 19 Jun 2019-08-09Document10 pagesFlipkart Labels 19 Jun 2019-08-09Shakti MalikNo ratings yet

- TWSH Schedule of Online ApplicationsDocument3 pagesTWSH Schedule of Online ApplicationsBikshapathi Naik BanothuNo ratings yet

- Jawaharlal Nehru College: BokoDocument3 pagesJawaharlal Nehru College: BokoGrace HoagnNo ratings yet

- Acct Statement XX4094 10112023Document18 pagesAcct Statement XX4094 10112023satyaraghu532No ratings yet

- Acct Statement XX3571 07112022Document36 pagesAcct Statement XX3571 07112022ashutoshpal21No ratings yet

- Tax467, Tax 267 Practice QuestionsDocument4 pagesTax467, Tax 267 Practice QuestionsRISNATUL UZMA HELMI RIZALNo ratings yet

- Payssion PricingDocument1 pagePayssion PricingSigit IrawanNo ratings yet

- Account StatementDocument39 pagesAccount StatementSun SivathaNo ratings yet