Download as docx, pdf, or txt

You might also like

- 1 Audit Program ExpensesDocument14 pages1 Audit Program Expensesmaleenda100% (3)

- Black Book PDFDocument78 pagesBlack Book PDFSayali Parulekar55% (11)

- Report On Eicher MotorsDocument49 pagesReport On Eicher MotorsMayur Hadawale100% (1)

- Maintenance Inventory Audit ProgramDocument7 pagesMaintenance Inventory Audit ProgramWilliam Andrew Gutiera BulaqueñaNo ratings yet

- Internship - Report - On - E - Banking - For Merge05Document63 pagesInternship - Report - On - E - Banking - For Merge05ঘুম বাবুNo ratings yet

- Regulatory Framework For Investment Banking in IndiaDocument2 pagesRegulatory Framework For Investment Banking in IndiaDevanshee Kothari0% (1)

- FM Textbook Solutions Chapter 1 Second EditionDocument6 pagesFM Textbook Solutions Chapter 1 Second EditionlibredescargaNo ratings yet

- Inter Audit Module - 1-2-21Document20 pagesInter Audit Module - 1-2-21binu75% (4)

- Audit of Property, Plant, and Equipment - Hahu Zone - 1622367787308Document8 pagesAudit of Property, Plant, and Equipment - Hahu Zone - 1622367787308Iam AbdiwaliNo ratings yet

- M8 Appe LaDocument12 pagesM8 Appe LaGabriel OrolfoNo ratings yet

- AP.3401 Audit of InventoriesDocument8 pagesAP.3401 Audit of InventoriesMonica GarciaNo ratings yet

- Risk Assessment - : Reported By: Jenny Mae E. Estioco, CPADocument41 pagesRisk Assessment - : Reported By: Jenny Mae E. Estioco, CPAJoyce Anne GarduqueNo ratings yet

- Correction of ErrorsDocument5 pagesCorrection of ErrorsMikkaNo ratings yet

- Management AssertionsDocument2 pagesManagement AssertionsTeh Chu LeongNo ratings yet

- Audit Program: Property Plant and EquipmentDocument8 pagesAudit Program: Property Plant and EquipmentAqib Sheikh100% (3)

- 5-Auditing 2 - Chapter FiveDocument10 pages5-Auditing 2 - Chapter Fivesamuel debebeNo ratings yet

- Chapter 5 - Chapter FiveDocument9 pagesChapter 5 - Chapter FiveBantamkak FikaduNo ratings yet

- Auditing in CIS Environment Chapter 1 NotesDocument11 pagesAuditing in CIS Environment Chapter 1 NotesKrizza TerradoNo ratings yet

- Audit of Plant Property and EquipmentDocument17 pagesAudit of Plant Property and EquipmentChristian Lim0% (1)

- Chapter 4Document10 pagesChapter 4Jarra AbdurahmanNo ratings yet

- CA Inter Audit Question BankDocument315 pagesCA Inter Audit Question BankKhushi SoniNo ratings yet

- Audit of PPEDocument3 pagesAudit of PPERochelle ManayaoNo ratings yet

- Audit Program-Fixed AssetsDocument7 pagesAudit Program-Fixed AssetsNaomiNo ratings yet

- Ca Inter Audit CH 1 2 3 1693227643Document22 pagesCa Inter Audit CH 1 2 3 1693227643Zaara ShaikhNo ratings yet

- TOPIC 5: AUDIT OF FINANCIAL STATEMENTS: Verification of Balance Sheet ItemsDocument34 pagesTOPIC 5: AUDIT OF FINANCIAL STATEMENTS: Verification of Balance Sheet ItemsIan100% (1)

- MODULE 4 Biological AssetsDocument4 pagesMODULE 4 Biological AssetsJean Geibrielle RomeroNo ratings yet

- Physical Stock Taking & Cash CountingDocument24 pagesPhysical Stock Taking & Cash CountingrajuNo ratings yet

- CARO ChecklistDocument26 pagesCARO ChecklistSantosh KumarNo ratings yet

- Auditing ProjectDocument42 pagesAuditing ProjectSahad KalaveNo ratings yet

- Gooseberry Andromeda DarjeelingDocument8 pagesGooseberry Andromeda DarjeelingMansoor SharifNo ratings yet

- Audit of Inv Property, NCA HFS and Disc OpDocument32 pagesAudit of Inv Property, NCA HFS and Disc OpPaula BitorNo ratings yet

- Audit I CH IIIDocument8 pagesAudit I CH IIIAhmedNo ratings yet

- Auditing Problems Ap.402 Audit of Inventories: The Use of Assertions in Obtaining Audit EvidenceDocument10 pagesAuditing Problems Ap.402 Audit of Inventories: The Use of Assertions in Obtaining Audit EvidenceMarjorie PonceNo ratings yet

- 1 Objective PDFDocument37 pages1 Objective PDFsamaadhuNo ratings yet

- 55067bos44235p6 Iipc ADocument10 pages55067bos44235p6 Iipc AAshutosh KumarNo ratings yet

- Draft of Audit ProgramDocument4 pagesDraft of Audit ProgramCecile UmaliNo ratings yet

- Topic # 2: Introdu Ction To Auditin GDocument31 pagesTopic # 2: Introdu Ction To Auditin GRizza OmalinNo ratings yet

- Module 1 PDFDocument8 pagesModule 1 PDFKez MaxNo ratings yet

- Fau Dec 2011 AnswersDocument10 pagesFau Dec 2011 AnswersSara DoweNo ratings yet

- Audit Program For Inventory Legal Company Name Client: Balance Sheet DateDocument3 pagesAudit Program For Inventory Legal Company Name Client: Balance Sheet DateHannah TudioNo ratings yet

- Audit II 4newDocument22 pagesAudit II 4newTesfaye Megiso BegajoNo ratings yet

- Philippine Accounting StandardsDocument4 pagesPhilippine Accounting StandardsjoeyNo ratings yet

- Caro ChecklistDocument26 pagesCaro ChecklistKushalKaleNo ratings yet

- Module 1 3 Audi313Document12 pagesModule 1 3 Audi313Katrina PaquizNo ratings yet

- The Use of Assertions in Obtaining Audit EvidenceDocument7 pagesThe Use of Assertions in Obtaining Audit EvidenceJesebel AmbalesNo ratings yet

- Chapter FourDocument18 pagesChapter Fourmubarek oumerNo ratings yet

- Auditing: Fira Firmanila & Lyanda PasadhiniDocument22 pagesAuditing: Fira Firmanila & Lyanda PasadhiniADIN IHTISYAMUDDINNo ratings yet

- Fixed AssetsDocument10 pagesFixed AssetsMikka JoyNo ratings yet

- 5 Audit EvidenceDocument11 pages5 Audit EvidenceHussain MustunNo ratings yet

- Substantive Test OF Shareholders' EquityDocument46 pagesSubstantive Test OF Shareholders' EquityAldrin John TungolNo ratings yet

- Auditing Problems Ocampo/Cabarles AP.1901-Audit of Inventories OCTOBER 2015Document8 pagesAuditing Problems Ocampo/Cabarles AP.1901-Audit of Inventories OCTOBER 2015AngelouNo ratings yet

- Exercise - Audit of Biological AssetsDocument2 pagesExercise - Audit of Biological AssetsIan SantosNo ratings yet

- ERC AP 1901 InventoriesDocument8 pagesERC AP 1901 Inventoriesjikee11No ratings yet

- Audit of Inventories: The Use of Assertions in Obtaining Audit EvidenceDocument9 pagesAudit of Inventories: The Use of Assertions in Obtaining Audit EvidencemoNo ratings yet

- Lesson - Substantive ProceduresDocument8 pagesLesson - Substantive ProceduresCherise TrollipNo ratings yet

- HayesDocument37 pagesHayesfreebirdovkNo ratings yet

- Steps in Audit Engagement CDocument5 pagesSteps in Audit Engagement CReland CastroNo ratings yet

- CA Inter Paper 6 Compiler 8-8-22Document316 pagesCA Inter Paper 6 Compiler 8-8-22KaviyaNo ratings yet

- AP 1901 Inventories PDFDocument8 pagesAP 1901 Inventories PDFToni Rhys ArguellesNo ratings yet

- Chapter 5 & 6Document20 pagesChapter 5 & 6Tesfahun tegegnNo ratings yet

- Audit of Debtors Loans and AdvancesDocument17 pagesAudit of Debtors Loans and Advanceseequals mcsquaredNo ratings yet

- CA Inter Audit A MTP 2 May 23Document10 pagesCA Inter Audit A MTP 2 May 23Sam KukrejaNo ratings yet

- Risk Assessment and Internal Control: CA Inter - Auditing and Assurance Additional Questions For Practice (Chapter 4)Document4 pagesRisk Assessment and Internal Control: CA Inter - Auditing and Assurance Additional Questions For Practice (Chapter 4)Annu DuaNo ratings yet

- Chapter 4 Auditing For Inventories and Cost of Goods SoldDocument3 pagesChapter 4 Auditing For Inventories and Cost of Goods SoldsteveiamidNo ratings yet

- Accounting for Goodwill and Other Intangible AssetsFrom EverandAccounting for Goodwill and Other Intangible AssetsRating: 4 out of 5 stars4/5 (1)

- Safeguard Soap - IntroDocument1 pageSafeguard Soap - IntroKris Anne SamudioNo ratings yet

- Feasibility Study - SamudioDocument16 pagesFeasibility Study - SamudioKris Anne SamudioNo ratings yet

- National Homemade Cookies Day by SlidesgoDocument58 pagesNational Homemade Cookies Day by SlidesgoKris Anne SamudioNo ratings yet

- Organic Bakery Marketing PlanDocument26 pagesOrganic Bakery Marketing PlanKris Anne SamudioNo ratings yet

- Organic Bakery Marketing PlanDocument26 pagesOrganic Bakery Marketing PlanKris Anne SamudioNo ratings yet

- Marketig PlanDocument11 pagesMarketig PlanKris Anne SamudioNo ratings yet

- Sweet Trends Ala Pastries Marketing Plan 1Document17 pagesSweet Trends Ala Pastries Marketing Plan 1Kris Anne SamudioNo ratings yet

- Organic Bakery Marketing PlanDocument26 pagesOrganic Bakery Marketing PlanKris Anne SamudioNo ratings yet

- Oatmeal Chocolate Chip Cookies MARKETING PLANDocument12 pagesOatmeal Chocolate Chip Cookies MARKETING PLANKris Anne SamudioNo ratings yet

- Organic Bakery Marketing PlanDocument26 pagesOrganic Bakery Marketing PlanKris Anne SamudioNo ratings yet

- 020-500-Summary of Control WeaknessesDocument5 pages020-500-Summary of Control WeaknessesKris Anne SamudioNo ratings yet

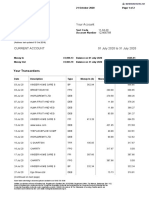

- Current Account 01 July 2020 To 31 July 2020: Your TransactionsDocument2 pagesCurrent Account 01 July 2020 To 31 July 2020: Your TransactionssadNo ratings yet

- 22 ExercisesDocument3 pages22 ExercisesTobio KageyamaNo ratings yet

- The New India Assurance Co. Ltd. (Government of India Undertaking)Document2 pagesThe New India Assurance Co. Ltd. (Government of India Undertaking)rajib paulNo ratings yet

- PINg Doce - ANASER Alimentação Fast FoodDocument13 pagesPINg Doce - ANASER Alimentação Fast Foodcaetano nunesNo ratings yet

- Acct Statement XX1940 05102022Document1 pageAcct Statement XX1940 05102022ARUN KUMARNo ratings yet

- Tech Mahindra Financial Statement: Balance SheetDocument45 pagesTech Mahindra Financial Statement: Balance SheetHRIDESH DWIVEDINo ratings yet

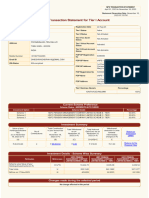

- Acct Statement - XX8192 - 30072021Document65 pagesAcct Statement - XX8192 - 30072021Vinay NandedkarNo ratings yet

- Assignment Financial AnalysisDocument15 pagesAssignment Financial AnalysisSilviu Andrei EneNo ratings yet

- 05 - Long Term Loans and AdvancesDocument5 pages05 - Long Term Loans and AdvancesAqib SheikhNo ratings yet

- PFRS 3, Business Combination: A) Formation of A Joint Venture - PFRS 11, Joint ArrangementsDocument7 pagesPFRS 3, Business Combination: A) Formation of A Joint Venture - PFRS 11, Joint ArrangementsBhosx KimNo ratings yet

- Accounting12 3ed Ch02Document18 pagesAccounting12 3ed Ch02rs8j4c4b5pNo ratings yet

- Grady Leasing Company Signs An Agreement On January 1 2010 PDFDocument1 pageGrady Leasing Company Signs An Agreement On January 1 2010 PDFAnbu jaromiaNo ratings yet

- Principles of Accounting I ModuleDocument243 pagesPrinciples of Accounting I Moduleyebegashet100% (5)

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- Schedule of Charges Yes Bank 6Document2 pagesSchedule of Charges Yes Bank 6Sayantika MondalNo ratings yet

- Simran Final Report1 PDFDocument40 pagesSimran Final Report1 PDFPriya Singh RajputNo ratings yet

- India's Journey Towards Cashless Economy-A Study: K. Sai Pavan KumarDocument9 pagesIndia's Journey Towards Cashless Economy-A Study: K. Sai Pavan KumarSai PavanNo ratings yet

- ABD - Financial Accounting Study Material 1Document35 pagesABD - Financial Accounting Study Material 1Sandesh LohakareNo ratings yet

- IntAcc Quiz 1 PDFDocument9 pagesIntAcc Quiz 1 PDFMyles Ninon LazoNo ratings yet

- Auditing TutorialDocument20 pagesAuditing TutorialDanisa NdhlovuNo ratings yet

- Tata Motors LTD - Axis Alpha - BUY - 05102020 (1) - 05-10-2020 - 09Document5 pagesTata Motors LTD - Axis Alpha - BUY - 05102020 (1) - 05-10-2020 - 09Rohit BhangaleNo ratings yet

- INDIAN Partnership DeedDocument2 pagesINDIAN Partnership DeedCA Vaibhav Maheshwari88% (17)

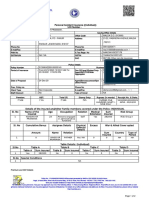

- NPS Account StatementDocument2 pagesNPS Account Statementdinesh rajendranNo ratings yet

- Company / Ratio Malaysia Resources Corporation Berhad IJM Corporation Berhad Gamuda Berhad Average Three Top Industries WTC BerhadDocument3 pagesCompany / Ratio Malaysia Resources Corporation Berhad IJM Corporation Berhad Gamuda Berhad Average Three Top Industries WTC BerhadGraceYeeNo ratings yet

- Problem 6 (Determination of Earnings and Earnings Per Share)Document8 pagesProblem 6 (Determination of Earnings and Earnings Per Share)TABOCTABOC JOHN PHILIP M.No ratings yet