Download as docx, pdf, or txt

You might also like

- Review Questions & Answers For Midterm1: BA 203 - Financial Accounting Fall 2019-2020Document11 pagesReview Questions & Answers For Midterm1: BA 203 - Financial Accounting Fall 2019-2020Ulaş GüllenoğluNo ratings yet

- Name: Section: Score:: ActivityDocument3 pagesName: Section: Score:: ActivityRae Michael57% (7)

- Makeup Service ContractDocument2 pagesMakeup Service ContractMary V. Warner-ReeseNo ratings yet

- Company A Was Incorporated On January 1Document5 pagesCompany A Was Incorporated On January 1Fakihusman Aliyasa81% (16)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Journal Entry To Post Closing Trial BalanceDocument5 pagesJournal Entry To Post Closing Trial BalanceRaez Rodillado100% (1)

- ACT Assignment FullDocument16 pagesACT Assignment Fullsadif sayeed100% (3)

- Kieso Chapter 10Document6 pagesKieso Chapter 10Dian Permata SariNo ratings yet

- Discussion Problems 1. You Plan To Retire 33 Years From Now. You Expect That You Will Live 27 Years After RetiringDocument10 pagesDiscussion Problems 1. You Plan To Retire 33 Years From Now. You Expect That You Will Live 27 Years After RetiringJape PreciaNo ratings yet

- Act Final-Group-AssignmentDocument15 pagesAct Final-Group-AssignmentTanvir Islam ShouravNo ratings yet

- Act 201 AssignmentDocument18 pagesAct 201 Assignmentrashedkhan1722No ratings yet

- Anna's Car Repair ShopDocument10 pagesAnna's Car Repair ShopNextdoor Cosplayer33% (3)

- JournalDocument2 pagesJournalakhtar140No ratings yet

- Business TransactionsDocument6 pagesBusiness TransactionsMarlyn Joy Yacon100% (1)

- Catacutan Allen Kevin B.: Date TransactionDocument1 pageCatacutan Allen Kevin B.: Date TransactionVon Steven OrtizNo ratings yet

- Journal Entries NewDocument2 pagesJournal Entries NewM Hassan BrohiNo ratings yet

- Journalizing Closing Entries For A Merchandising EnterpriseDocument36 pagesJournalizing Closing Entries For A Merchandising EnterpriseRodolfo CorpuzNo ratings yet

- Adjusting Entries Company A ExercisesDocument19 pagesAdjusting Entries Company A ExercisesRodolfo CorpuzNo ratings yet

- Assignment ACT201 SMR1Document15 pagesAssignment ACT201 SMR1Md.sabir 1831620030No ratings yet

- ACT201 AssignmentDocument27 pagesACT201 AssignmentArponNo ratings yet

- Major Assignment - Act 201 - Sec 20Document15 pagesMajor Assignment - Act 201 - Sec 20Nishat FarhatNo ratings yet

- Journal-Entries GABONDocument29 pagesJournal-Entries GABONrose gabonNo ratings yet

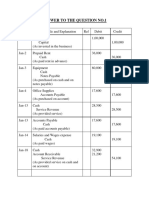

- Answer To The Question No. 1 (A) General JournalDocument16 pagesAnswer To The Question No. 1 (A) General JournalSurmaNo ratings yet

- Journal Entries - Financial AccountingDocument3 pagesJournal Entries - Financial AccountingElham JabarkhailNo ratings yet

- GroupingsDocument4 pagesGroupingsAnonymous EvbW4o1U7No ratings yet

- Nsu IbrahimDocument2 pagesNsu IbrahimMohammad KhalilNo ratings yet

- JournalDocument4 pagesJournal23102349No ratings yet

- Accounting Cycle: Journal EntriesDocument5 pagesAccounting Cycle: Journal EntriesNeha PandeyNo ratings yet

- Account Title Unadjusted Trial Balance Adjustments Adjusted Trial Balance Debit Credit Debit Credit DebitDocument15 pagesAccount Title Unadjusted Trial Balance Adjustments Adjusted Trial Balance Debit Credit Debit Credit DebitTwins VinesNo ratings yet

- Journal Entries - 1666100137Document12 pagesJournal Entries - 1666100137Van OneNo ratings yet

- First ExampleDocument11 pagesFirst ExampleJanna GunioNo ratings yet

- Southeast University: Midterm AssignmentDocument6 pagesSoutheast University: Midterm AssignmentNaufel Saad KhanNo ratings yet

- Journal, T Accounts, TrialDocument14 pagesJournal, T Accounts, TrialJasmine ActaNo ratings yet

- (Module 3) ProblemsDocument17 pages(Module 3) ProblemsArriane Dela CruzNo ratings yet

- WAC Chief HongDocument24 pagesWAC Chief HongJasmine ActaNo ratings yet

- JOURNALIZINGDocument2 pagesJOURNALIZINGArneld SantiagoNo ratings yet

- Soal Tugas Lab 3 - Ledger and AdjustingDocument4 pagesSoal Tugas Lab 3 - Ledger and AdjustingAlip alipNo ratings yet

- F003 NPO Exam TeachersDocument7 pagesF003 NPO Exam TeachersbhumikaaNo ratings yet

- DanielpadillaDocument8 pagesDanielpadillaJu ReyesNo ratings yet

- Full Download PDF of Solution Manual For Horngren's Financial & Managerial Accounting, 6th Edition All ChapterDocument99 pagesFull Download PDF of Solution Manual For Horngren's Financial & Managerial Accounting, 6th Edition All Chapterhleskoxboo100% (3)

- Final Marryland AccountingDocument15 pagesFinal Marryland AccountingNatnael AsnakeNo ratings yet

- Far 1Document2 pagesFar 1Stephanie Jane0% (1)

- Book 1Document16 pagesBook 1Bushra RizviNo ratings yet

- Practice Problem Jenny Light AccountantDocument17 pagesPractice Problem Jenny Light AccountantFranco James Sanpedro100% (1)

- Kertas Kerja Shawn Merry, CPA April 2018Document5 pagesKertas Kerja Shawn Merry, CPA April 2018khaira aprinaldo putraNo ratings yet

- Adjusted Assgn 1Document2 pagesAdjusted Assgn 1Ryan JacobsNo ratings yet

- Assignment No.5 AccountingDocument6 pagesAssignment No.5 Accountingibrar ghaniNo ratings yet

- Adjusting Entry Math LatestDocument4 pagesAdjusting Entry Math LatestOyon Nur newazNo ratings yet

- Accounting For Business DecisionsDocument7 pagesAccounting For Business DecisionsFaizan AhmedNo ratings yet

- Date Account Names Debit CreditDocument2 pagesDate Account Names Debit Creditfarhann JattNo ratings yet

- Answer Key Activity 39Document15 pagesAnswer Key Activity 39MAXINE CLAIRE CUTINGNo ratings yet

- PIA CF 1bi JDGDDocument16 pagesPIA CF 1bi JDGDDavid GuerreroNo ratings yet

- Anton Video Tech Sells The Play Station Portable (PSP) 1 2Document6 pagesAnton Video Tech Sells The Play Station Portable (PSP) 1 2Siti Marian V. OlmillaNo ratings yet

- Revision ch1&2 1thDocument23 pagesRevision ch1&2 1thYousefNo ratings yet

- ReviewDocument38 pagesReviewFiana DolinogNo ratings yet

- Journalizing Business Transactions-EspinaDocument3 pagesJournalizing Business Transactions-EspinaVanessa FajardoNo ratings yet

- General Journal: Date Account Titles and Explanation CreditDocument4 pagesGeneral Journal: Date Account Titles and Explanation CreditHarriane Mae GonzalesNo ratings yet

- AccountingDocument21 pagesAccountingReana ReyesNo ratings yet

- Books of Accounts TemplatesDocument18 pagesBooks of Accounts TemplatesMc Clent CervantesNo ratings yet

- Act1104 Quiz No. 3 Problem 1Document6 pagesAct1104 Quiz No. 3 Problem 1DyenNo ratings yet

- 1 - Journal Entries - Format & ExamplesDocument1 page1 - Journal Entries - Format & ExamplesShahbaz SyedNo ratings yet

- 134420Document2 pages134420Nicole GalvezNo ratings yet

- Short QuestionsDocument3 pagesShort QuestionsSadia ShithyNo ratings yet

- Lab Report 1Document4 pagesLab Report 1Sadia ShithyNo ratings yet

- Fraud, Internal Control, and Cash: Learning ObjectivesDocument15 pagesFraud, Internal Control, and Cash: Learning ObjectivesSadia ShithyNo ratings yet

- ENVL-12-Lab Report-Group 1-Nazia-SadiaDocument3 pagesENVL-12-Lab Report-Group 1-Nazia-SadiaSadia ShithyNo ratings yet

- Follow Up LessonsDocument11 pagesFollow Up LessonsFrancisco NiegasNo ratings yet

- Campbell GenealogyDocument28 pagesCampbell GenealogyJeff Martin100% (1)

- LS 101 Daylighting Controller Cut SheetDocument6 pagesLS 101 Daylighting Controller Cut SheetIgor NiculovicNo ratings yet

- MSF Degree PlanDocument1 pageMSF Degree PlanamitlkoyogaNo ratings yet

- Daniel's Law Week of ActionDocument1 pageDaniel's Law Week of ActionAdam PenaleNo ratings yet

- Gcu Student Teaching Evaluation of Performance Step Standard 1 Part II Part 1 - Signed-2Document5 pagesGcu Student Teaching Evaluation of Performance Step Standard 1 Part II Part 1 - Signed-2api-631448823No ratings yet

- Indian Railways Increasing The Axle Loading: Atul Sonkhla Naveen Tondan Rahul GautamDocument8 pagesIndian Railways Increasing The Axle Loading: Atul Sonkhla Naveen Tondan Rahul Gautam01202No ratings yet

- In The Matter of The Disbarment of DominadorDocument2 pagesIn The Matter of The Disbarment of DominadorRen ConchaNo ratings yet

- India Consumer: Wallet Watch - Vol 1/12Document6 pagesIndia Consumer: Wallet Watch - Vol 1/12Rahul GanapathyNo ratings yet

- Sala k35Document162 pagesSala k35Juan Pablo Alonso CardonaNo ratings yet

- Fieldwork Tradition in Anthropology Prof. Subhdra ChannaDocument18 pagesFieldwork Tradition in Anthropology Prof. Subhdra ChannaFaith RiderNo ratings yet

- Amon Llanca - My Gender Is A (Con) Fusion Experience - Non-Binary Bodies in Fictional NarrativesDocument61 pagesAmon Llanca - My Gender Is A (Con) Fusion Experience - Non-Binary Bodies in Fictional NarrativesvaleriamenaariasNo ratings yet

- The Art of Empathy Translation PDFDocument90 pagesThe Art of Empathy Translation PDFusrjpfptNo ratings yet

- Words EnglishDocument3 pagesWords EnglishOthmane BettemNo ratings yet

- Attabad LakeDocument3 pagesAttabad LakeTaymoor ArifNo ratings yet

- LUKOIL FIM Ice Speedway Gladiators World Championship Final 5 - Heerenveen NLDocument4 pagesLUKOIL FIM Ice Speedway Gladiators World Championship Final 5 - Heerenveen NLАлексей ПолянцевNo ratings yet

- MANSCIDocument3 pagesMANSCIJanesa Maxcen CabilloNo ratings yet

- 7094 s19 QP 1Document12 pages7094 s19 QP 1Matrîx GamesNo ratings yet

- Binance CoinDocument3 pagesBinance Coins160821004No ratings yet

- Final ExamDocument5 pagesFinal ExamaneesNo ratings yet

- Calif. Wildfire Surges To Nearly 200 Square Miles and Spreads Into Yosemite National ParkDocument3 pagesCalif. Wildfire Surges To Nearly 200 Square Miles and Spreads Into Yosemite National ParkCynthia TingNo ratings yet

- Final Project Plan Hcin 542Document33 pagesFinal Project Plan Hcin 542api-672832076No ratings yet

- LGBT FactsDocument43 pagesLGBT Factsjohn kaneNo ratings yet

- Email Marketing: Name: Mane Parikshit Ashok Class: S.Y.B.B.A. (Marketing Specialization)Document13 pagesEmail Marketing: Name: Mane Parikshit Ashok Class: S.Y.B.B.A. (Marketing Specialization)Parikshit Ashok ManeNo ratings yet

- Case Study: Salary Inequities at Acme ManufacturingDocument2 pagesCase Study: Salary Inequities at Acme ManufacturingUmialyNo ratings yet

- Jewish Standard, September 11, 2015Document76 pagesJewish Standard, September 11, 2015New Jersey Jewish StandardNo ratings yet

- ContractorsDocument12 pagesContractorsrx330No ratings yet

- PHASE 1 Project Identification and PlanningDocument7 pagesPHASE 1 Project Identification and PlanningDerrick DumolNo ratings yet