Bajaj Finserce - Project

Bajaj Finserce - Project

You might also like

- Attachment Disturbances in Adults Treatment For Comprehensive Repair (Etc.) (Z-Library)Document477 pagesAttachment Disturbances in Adults Treatment For Comprehensive Repair (Etc.) (Z-Library)fa ab100% (8)

- Sandal Magna Primary SchoolDocument36 pagesSandal Magna Primary SchoolsaurabhNo ratings yet

- Role of Bajaj Finance in Consumer DurablDocument84 pagesRole of Bajaj Finance in Consumer DurablNiraj tiwariNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Bajaj FinanceDocument65 pagesBajaj FinanceAshutoshSharmaNo ratings yet

- Blackbook Project On Internet MarketingDocument88 pagesBlackbook Project On Internet MarketingRithik ThakurNo ratings yet

- Consumer Behaviour - Maruti SuzukiDocument63 pagesConsumer Behaviour - Maruti SuzukiBipin BopaiahNo ratings yet

- Project NEWSTUDY OF CUSTOMER RELATIONSHIP MANAGEMENT INDocument94 pagesProject NEWSTUDY OF CUSTOMER RELATIONSHIP MANAGEMENT INYash Batra100% (1)

- Comparative Analysis of Sharekhan and Other Stock Broker HouseDocument78 pagesComparative Analysis of Sharekhan and Other Stock Broker Housekunal khaireNo ratings yet

- SU Copic ChartDocument6 pagesSU Copic ChartErin Dunegan RenfrowNo ratings yet

- Summer Internship Project ReportDocument58 pagesSummer Internship Project ReportArjun Gami67% (3)

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- A Project Report On BajajDocument17 pagesA Project Report On BajajSandeep Tripathi71% (7)

- A Study On The Role of Bajaj Finserv in Consumer Durable FinanceeDocument58 pagesA Study On The Role of Bajaj Finserv in Consumer Durable Financeeshwetha17% (6)

- Project Report On BFLDocument33 pagesProject Report On BFLSaurabh BhagatNo ratings yet

- A Project Report On Loan Procedure of Consumer Durable Product at Bajaj Finserv LendingDocument65 pagesA Project Report On Loan Procedure of Consumer Durable Product at Bajaj Finserv LendingHusna Majid50% (2)

- Indus Bank - Report On Summer TrainingDocument34 pagesIndus Bank - Report On Summer TrainingZahid Bhat100% (1)

- Company Profile of HDFC LifeDocument19 pagesCompany Profile of HDFC LifeNazir HussainNo ratings yet

- A Comparative Study of Bancassurance Products in Banks - SynopsisDocument8 pagesA Comparative Study of Bancassurance Products in Banks - Synopsisammukhan khan100% (1)

- Customer Satisfaction - HDFC LifeDocument49 pagesCustomer Satisfaction - HDFC Liferaj0% (1)

- Sriram Insight Financial ProjectDocument99 pagesSriram Insight Financial ProjectVinay Bhandari100% (1)

- Literature ReviewDocument7 pagesLiterature ReviewAshu SharmaNo ratings yet

- Project Report - Shriram Transport FinanceDocument40 pagesProject Report - Shriram Transport FinanceVikas Rathod100% (1)

- SynopsisDocument11 pagesSynopsiskrishna bajait100% (1)

- HDFC Life Insurance 2011Document66 pagesHDFC Life Insurance 2011nupurgupta19100% (1)

- Mba Project Report On HDFC BankDocument13 pagesMba Project Report On HDFC BanknehaNo ratings yet

- Full Project in Angel Broking ServicesDocument73 pagesFull Project in Angel Broking ServicesHarichandran KarthikeyanNo ratings yet

- Brand Image of Icici Prudential Life InsuranceDocument40 pagesBrand Image of Icici Prudential Life InsuranceShehbaz KhannaNo ratings yet

- Shriram-Life-Insurance Project Report 786Document60 pagesShriram-Life-Insurance Project Report 786Javeed GurramkondaNo ratings yet

- Investors Attitude Towards Primary MarketDocument62 pagesInvestors Attitude Towards Primary MarketRonak Singhal50% (2)

- Project On Demat AccountDocument62 pagesProject On Demat Accountsmruti bansod100% (1)

- An Internship Project Report On Shriram Life Insurance Contents Madhav RajbanshiDocument41 pagesAn Internship Project Report On Shriram Life Insurance Contents Madhav RajbanshiMadhav RajbanshiNo ratings yet

- SIP Report Bajaj Finserv Updated - NiharikaDocument44 pagesSIP Report Bajaj Finserv Updated - NiharikaAniket AgrahariNo ratings yet

- SIP Project ReportDocument54 pagesSIP Project Reportjigar_kansagra100% (13)

- Bajaj Finserve SIP ReportDocument41 pagesBajaj Finserve SIP Reportvipul deshmukhNo ratings yet

- Bajaj FinanceDocument18 pagesBajaj FinanceVipin CoolNo ratings yet

- Comparative Study of Life InsuranceDocument61 pagesComparative Study of Life InsuranceParinShah83% (6)

- Comparative Study of HDFC Slic, Bajaj Allianz, Birla Sun Life and LicDocument62 pagesComparative Study of HDFC Slic, Bajaj Allianz, Birla Sun Life and Licasafali20658198% (64)

- Project Report On The HDFC BANK LTD.Document58 pagesProject Report On The HDFC BANK LTD.preeyankagupta67% (9)

- Ashish Project Report On Icici BankDocument134 pagesAshish Project Report On Icici BankAshish Goyal82% (11)

- A Summer Internship ProjectDocument36 pagesA Summer Internship ProjectRubina MansooriNo ratings yet

- MBA 4th Sem A STUDY ON BANKING OPERATIONS IN AN ECONOMYDocument42 pagesMBA 4th Sem A STUDY ON BANKING OPERATIONS IN AN ECONOMYraghav bansalNo ratings yet

- A Study On Financial Investment in Indian Commodity MarketDocument60 pagesA Study On Financial Investment in Indian Commodity Marketramagarwal1No ratings yet

- 4TH Sem. Final ProjectDocument63 pages4TH Sem. Final ProjectPratik ZalkeNo ratings yet

- Project Report On Indusind BankDocument80 pagesProject Report On Indusind Bankrosy tudu100% (1)

- Summer Training Report On HDFC LifeDocument90 pagesSummer Training Report On HDFC LifePrateek LoganiNo ratings yet

- Summer Internship Project HDFC Bank PDFDocument109 pagesSummer Internship Project HDFC Bank PDFarunima100% (1)

- Summer Intership Project Bajaj FinservDocument48 pagesSummer Intership Project Bajaj FinservOMSAINATH MPONLINENo ratings yet

- A Comparative Study On The Offerings of Insurance Products Between LICDocument26 pagesA Comparative Study On The Offerings of Insurance Products Between LICk b paliwal91% (22)

- Detailed Study On Insurance Preference As An Investment and Consumer PerceptionDocument54 pagesDetailed Study On Insurance Preference As An Investment and Consumer PerceptionHimanshu H100% (1)

- Punjab National Bank Ratio AnalysisDocument62 pagesPunjab National Bank Ratio AnalysiskodalipragathiNo ratings yet

- Comparitive Study ICICI & HDFCDocument94 pagesComparitive Study ICICI & HDFCshah faisal75% (16)

- Comparision of Publick Sector Bank and Private Sector BankDocument37 pagesComparision of Publick Sector Bank and Private Sector Bankjaypatel2201No ratings yet

- Research Project Report: To Study The Retial Banking in Present ScenarioDocument94 pagesResearch Project Report: To Study The Retial Banking in Present Scenariodiwakar0000000No ratings yet

- Kotak FinalDocument46 pagesKotak FinalRahul FaliyaNo ratings yet

- BankingDocument75 pagesBankingGenesian Nikhilesh PillayNo ratings yet

- Hemant MBA Final ProjectDocument48 pagesHemant MBA Final ProjectDashing HemantNo ratings yet

- Digital BankingDocument60 pagesDigital BankingRaja RayadurgamNo ratings yet

- Research Paper On Fundamental Analysis of Banking Sector in IndiaDocument4 pagesResearch Paper On Fundamental Analysis of Banking Sector in Indiaafeawfxlb100% (1)

- Finance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)Document40 pagesFinance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)AneesAnsariNo ratings yet

- Kotak Mahindra Bank 121121123739 Phpapp02Document112 pagesKotak Mahindra Bank 121121123739 Phpapp02RahulSinghNo ratings yet

- Arif Iqbal SarvaDocument1 pageArif Iqbal SarvaCyber VirginNo ratings yet

- Sohel AliDocument1 pageSohel AliCyber VirginNo ratings yet

- Heaven Little Grandson Heaven Little Grandson: Rejoice! Rejoice!Document1 pageHeaven Little Grandson Heaven Little Grandson: Rejoice! Rejoice!Cyber VirginNo ratings yet

- Shaikh Shabina ShakeelDocument1 pageShaikh Shabina ShakeelCyber VirginNo ratings yet

- Odisha Beaches InfomationDocument6 pagesOdisha Beaches InfomationCyber VirginNo ratings yet

- Honda MotorsDocument68 pagesHonda MotorsCyber VirginNo ratings yet

- Puma ProjectDocument52 pagesPuma ProjectCyber VirginNo ratings yet

- Indian Armed ForcesDocument23 pagesIndian Armed ForcesCyber VirginNo ratings yet

- The Manufacturing Process of FabricDocument3 pagesThe Manufacturing Process of FabricCyber VirginNo ratings yet

- Medical Fttness FormatDocument1 pageMedical Fttness FormatCyber VirginNo ratings yet

- Multiple Choice QuestionsDocument13 pagesMultiple Choice QuestionsCyber VirginNo ratings yet

- Online LecturesDocument2 pagesOnline LecturesCyber VirginNo ratings yet

- Form 9 - Consent of DP and Subscriber SheetDocument5 pagesForm 9 - Consent of DP and Subscriber SheetCyber VirginNo ratings yet

- "Study of With Respect To '': Padmashri Annasaheb Jadhav Bharatiya Samaj Unnati Mandal'SDocument61 pages"Study of With Respect To '': Padmashri Annasaheb Jadhav Bharatiya Samaj Unnati Mandal'SCyber VirginNo ratings yet

- Effect of Mobile Marketing On Youngsters in Gorakhpur RegionDocument9 pagesEffect of Mobile Marketing On Youngsters in Gorakhpur RegionCyber VirginNo ratings yet

- Top 10 Most Promising Experimental Cancer Treatments: Radiation TherapiesDocument7 pagesTop 10 Most Promising Experimental Cancer Treatments: Radiation TherapiesCyber VirginNo ratings yet

- BissiDocument1 pageBissiCyber VirginNo ratings yet

- Month: Cleaned By: Working Area:: Washroom Cleaning ScheduleDocument1 pageMonth: Cleaned By: Working Area:: Washroom Cleaning ScheduleCyber VirginNo ratings yet

- C4 Tech Spec Issue 2Document5 pagesC4 Tech Spec Issue 2Дмитрий КалининNo ratings yet

- Cemex Holdings Philippines Annual Report 2016 PDFDocument47 pagesCemex Holdings Philippines Annual Report 2016 PDFFritz NatividadNo ratings yet

- Major Crops of Pakistan Wheat, Cotton, Rice, Sugarcane: and MaizeDocument17 pagesMajor Crops of Pakistan Wheat, Cotton, Rice, Sugarcane: and MaizeWaleed Bin khalidNo ratings yet

- Literary Devices DefinitionsDocument2 pagesLiterary Devices DefinitionsAlanna BryantNo ratings yet

- Teaching PronunciationDocument6 pagesTeaching PronunciationKathryn LupsonNo ratings yet

- Sun Pharma ProjectDocument26 pagesSun Pharma ProjectVikas Ahuja100% (1)

- Weekly Home Learning Plan in Mathematics 8: Quarter 1, Week 3, October 19 - 23, 2020Document7 pagesWeekly Home Learning Plan in Mathematics 8: Quarter 1, Week 3, October 19 - 23, 2020Zaldy TabugocaNo ratings yet

- Why Romanian Journal of Food ScienceDocument2 pagesWhy Romanian Journal of Food ScienceAna Vitelariu - RaduNo ratings yet

- Maternal and Infant Care Beliefs Aeta Mothers in PhilippinesDocument8 pagesMaternal and Infant Care Beliefs Aeta Mothers in PhilippinesChristine Joy MolinaNo ratings yet

- 2011 Diving Catalogue BEUCHATDocument60 pages2011 Diving Catalogue BEUCHATRalph KramdenNo ratings yet

- Application DevelopmentDocument14 pagesApplication DevelopmentReema MubarakNo ratings yet

- Hockey - Indian National Game-2compDocument21 pagesHockey - Indian National Game-2compRaj BadreNo ratings yet

- Butterflies and MothsDocument59 pagesButterflies and MothsReegen Tee100% (3)

- The DJ Test: Personalised Report and Recommendations For Alex YachevskiDocument34 pagesThe DJ Test: Personalised Report and Recommendations For Alex YachevskiSashadanceNo ratings yet

- Chords Like Jeff BuckleyDocument5 pagesChords Like Jeff BuckleyTDROCKNo ratings yet

- God Will Protect His Church God Will Protect His ChurchDocument17 pagesGod Will Protect His Church God Will Protect His ChurchLaura GarciaNo ratings yet

- RMS Infosheet Classic Vehicle Scheme Mou 2016 12Document21 pagesRMS Infosheet Classic Vehicle Scheme Mou 2016 12www.toxiconlineNo ratings yet

- Full Download 2014 Psychiatric Mental Health Nursing Revised Reprint 5e Test Bank PDF Full ChapterDocument36 pagesFull Download 2014 Psychiatric Mental Health Nursing Revised Reprint 5e Test Bank PDF Full Chapterpassim.pluvialg5ty6100% (17)

- Agent ListDocument23 pagesAgent ListMayuresh ShakyawarNo ratings yet

- Auto Motivations Digital Cinema and KiarDocument11 pagesAuto Motivations Digital Cinema and KiarDebanjan BandyopadhyayNo ratings yet

- ModulationDocument7 pagesModulationSyeda MiznaNo ratings yet

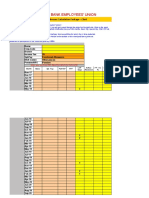

- Karur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDocument10 pagesKarur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDeepa ManianNo ratings yet

- Satellite CommunicationsDocument57 pagesSatellite Communicationsheritage336No ratings yet

- 8.b SOAL PAT B INGGRIS KELAS 8Document6 pages8.b SOAL PAT B INGGRIS KELAS 8M Adib MasykurNo ratings yet

- Blockchain-Enabled Drug Supply Chain: Sheetal Nayak, Prachitee Shirvale, Nihar Naik, Snehpriya Khul, Amol SawantDocument4 pagesBlockchain-Enabled Drug Supply Chain: Sheetal Nayak, Prachitee Shirvale, Nihar Naik, Snehpriya Khul, Amol SawantWaspNo ratings yet

- L4 02 Causative Verbs Teaching JobDocument4 pagesL4 02 Causative Verbs Teaching JobGeorge VieiraNo ratings yet

- Ecocriticism and Narrative Theory An IntroductionDocument12 pagesEcocriticism and Narrative Theory An IntroductionIdriss BenkacemNo ratings yet

Download as docx, pdf, or txt

You might also like

- Attachment Disturbances in Adults Treatment For Comprehensive Repair (Etc.) (Z-Library)Document477 pagesAttachment Disturbances in Adults Treatment For Comprehensive Repair (Etc.) (Z-Library)fa ab100% (8)

- Sandal Magna Primary SchoolDocument36 pagesSandal Magna Primary SchoolsaurabhNo ratings yet

- Role of Bajaj Finance in Consumer DurablDocument84 pagesRole of Bajaj Finance in Consumer DurablNiraj tiwariNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Bajaj FinanceDocument65 pagesBajaj FinanceAshutoshSharmaNo ratings yet

- Blackbook Project On Internet MarketingDocument88 pagesBlackbook Project On Internet MarketingRithik ThakurNo ratings yet

- Consumer Behaviour - Maruti SuzukiDocument63 pagesConsumer Behaviour - Maruti SuzukiBipin BopaiahNo ratings yet

- Project NEWSTUDY OF CUSTOMER RELATIONSHIP MANAGEMENT INDocument94 pagesProject NEWSTUDY OF CUSTOMER RELATIONSHIP MANAGEMENT INYash Batra100% (1)

- Comparative Analysis of Sharekhan and Other Stock Broker HouseDocument78 pagesComparative Analysis of Sharekhan and Other Stock Broker Housekunal khaireNo ratings yet

- SU Copic ChartDocument6 pagesSU Copic ChartErin Dunegan RenfrowNo ratings yet

- Summer Internship Project ReportDocument58 pagesSummer Internship Project ReportArjun Gami67% (3)

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- A Project Report On BajajDocument17 pagesA Project Report On BajajSandeep Tripathi71% (7)

- A Study On The Role of Bajaj Finserv in Consumer Durable FinanceeDocument58 pagesA Study On The Role of Bajaj Finserv in Consumer Durable Financeeshwetha17% (6)

- Project Report On BFLDocument33 pagesProject Report On BFLSaurabh BhagatNo ratings yet

- A Project Report On Loan Procedure of Consumer Durable Product at Bajaj Finserv LendingDocument65 pagesA Project Report On Loan Procedure of Consumer Durable Product at Bajaj Finserv LendingHusna Majid50% (2)

- Indus Bank - Report On Summer TrainingDocument34 pagesIndus Bank - Report On Summer TrainingZahid Bhat100% (1)

- Company Profile of HDFC LifeDocument19 pagesCompany Profile of HDFC LifeNazir HussainNo ratings yet

- A Comparative Study of Bancassurance Products in Banks - SynopsisDocument8 pagesA Comparative Study of Bancassurance Products in Banks - Synopsisammukhan khan100% (1)

- Customer Satisfaction - HDFC LifeDocument49 pagesCustomer Satisfaction - HDFC Liferaj0% (1)

- Sriram Insight Financial ProjectDocument99 pagesSriram Insight Financial ProjectVinay Bhandari100% (1)

- Literature ReviewDocument7 pagesLiterature ReviewAshu SharmaNo ratings yet

- Project Report - Shriram Transport FinanceDocument40 pagesProject Report - Shriram Transport FinanceVikas Rathod100% (1)

- SynopsisDocument11 pagesSynopsiskrishna bajait100% (1)

- HDFC Life Insurance 2011Document66 pagesHDFC Life Insurance 2011nupurgupta19100% (1)

- Mba Project Report On HDFC BankDocument13 pagesMba Project Report On HDFC BanknehaNo ratings yet

- Full Project in Angel Broking ServicesDocument73 pagesFull Project in Angel Broking ServicesHarichandran KarthikeyanNo ratings yet

- Brand Image of Icici Prudential Life InsuranceDocument40 pagesBrand Image of Icici Prudential Life InsuranceShehbaz KhannaNo ratings yet

- Shriram-Life-Insurance Project Report 786Document60 pagesShriram-Life-Insurance Project Report 786Javeed GurramkondaNo ratings yet

- Investors Attitude Towards Primary MarketDocument62 pagesInvestors Attitude Towards Primary MarketRonak Singhal50% (2)

- Project On Demat AccountDocument62 pagesProject On Demat Accountsmruti bansod100% (1)

- An Internship Project Report On Shriram Life Insurance Contents Madhav RajbanshiDocument41 pagesAn Internship Project Report On Shriram Life Insurance Contents Madhav RajbanshiMadhav RajbanshiNo ratings yet

- SIP Report Bajaj Finserv Updated - NiharikaDocument44 pagesSIP Report Bajaj Finserv Updated - NiharikaAniket AgrahariNo ratings yet

- SIP Project ReportDocument54 pagesSIP Project Reportjigar_kansagra100% (13)

- Bajaj Finserve SIP ReportDocument41 pagesBajaj Finserve SIP Reportvipul deshmukhNo ratings yet

- Bajaj FinanceDocument18 pagesBajaj FinanceVipin CoolNo ratings yet

- Comparative Study of Life InsuranceDocument61 pagesComparative Study of Life InsuranceParinShah83% (6)

- Comparative Study of HDFC Slic, Bajaj Allianz, Birla Sun Life and LicDocument62 pagesComparative Study of HDFC Slic, Bajaj Allianz, Birla Sun Life and Licasafali20658198% (64)

- Project Report On The HDFC BANK LTD.Document58 pagesProject Report On The HDFC BANK LTD.preeyankagupta67% (9)

- Ashish Project Report On Icici BankDocument134 pagesAshish Project Report On Icici BankAshish Goyal82% (11)

- A Summer Internship ProjectDocument36 pagesA Summer Internship ProjectRubina MansooriNo ratings yet

- MBA 4th Sem A STUDY ON BANKING OPERATIONS IN AN ECONOMYDocument42 pagesMBA 4th Sem A STUDY ON BANKING OPERATIONS IN AN ECONOMYraghav bansalNo ratings yet

- A Study On Financial Investment in Indian Commodity MarketDocument60 pagesA Study On Financial Investment in Indian Commodity Marketramagarwal1No ratings yet

- 4TH Sem. Final ProjectDocument63 pages4TH Sem. Final ProjectPratik ZalkeNo ratings yet

- Project Report On Indusind BankDocument80 pagesProject Report On Indusind Bankrosy tudu100% (1)

- Summer Training Report On HDFC LifeDocument90 pagesSummer Training Report On HDFC LifePrateek LoganiNo ratings yet

- Summer Internship Project HDFC Bank PDFDocument109 pagesSummer Internship Project HDFC Bank PDFarunima100% (1)

- Summer Intership Project Bajaj FinservDocument48 pagesSummer Intership Project Bajaj FinservOMSAINATH MPONLINENo ratings yet

- A Comparative Study On The Offerings of Insurance Products Between LICDocument26 pagesA Comparative Study On The Offerings of Insurance Products Between LICk b paliwal91% (22)

- Detailed Study On Insurance Preference As An Investment and Consumer PerceptionDocument54 pagesDetailed Study On Insurance Preference As An Investment and Consumer PerceptionHimanshu H100% (1)

- Punjab National Bank Ratio AnalysisDocument62 pagesPunjab National Bank Ratio AnalysiskodalipragathiNo ratings yet

- Comparitive Study ICICI & HDFCDocument94 pagesComparitive Study ICICI & HDFCshah faisal75% (16)

- Comparision of Publick Sector Bank and Private Sector BankDocument37 pagesComparision of Publick Sector Bank and Private Sector Bankjaypatel2201No ratings yet

- Research Project Report: To Study The Retial Banking in Present ScenarioDocument94 pagesResearch Project Report: To Study The Retial Banking in Present Scenariodiwakar0000000No ratings yet

- Kotak FinalDocument46 pagesKotak FinalRahul FaliyaNo ratings yet

- BankingDocument75 pagesBankingGenesian Nikhilesh PillayNo ratings yet

- Hemant MBA Final ProjectDocument48 pagesHemant MBA Final ProjectDashing HemantNo ratings yet

- Digital BankingDocument60 pagesDigital BankingRaja RayadurgamNo ratings yet

- Research Paper On Fundamental Analysis of Banking Sector in IndiaDocument4 pagesResearch Paper On Fundamental Analysis of Banking Sector in Indiaafeawfxlb100% (1)

- Finance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)Document40 pagesFinance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)AneesAnsariNo ratings yet

- Kotak Mahindra Bank 121121123739 Phpapp02Document112 pagesKotak Mahindra Bank 121121123739 Phpapp02RahulSinghNo ratings yet

- Arif Iqbal SarvaDocument1 pageArif Iqbal SarvaCyber VirginNo ratings yet

- Sohel AliDocument1 pageSohel AliCyber VirginNo ratings yet

- Heaven Little Grandson Heaven Little Grandson: Rejoice! Rejoice!Document1 pageHeaven Little Grandson Heaven Little Grandson: Rejoice! Rejoice!Cyber VirginNo ratings yet

- Shaikh Shabina ShakeelDocument1 pageShaikh Shabina ShakeelCyber VirginNo ratings yet

- Odisha Beaches InfomationDocument6 pagesOdisha Beaches InfomationCyber VirginNo ratings yet

- Honda MotorsDocument68 pagesHonda MotorsCyber VirginNo ratings yet

- Puma ProjectDocument52 pagesPuma ProjectCyber VirginNo ratings yet

- Indian Armed ForcesDocument23 pagesIndian Armed ForcesCyber VirginNo ratings yet

- The Manufacturing Process of FabricDocument3 pagesThe Manufacturing Process of FabricCyber VirginNo ratings yet

- Medical Fttness FormatDocument1 pageMedical Fttness FormatCyber VirginNo ratings yet

- Multiple Choice QuestionsDocument13 pagesMultiple Choice QuestionsCyber VirginNo ratings yet

- Online LecturesDocument2 pagesOnline LecturesCyber VirginNo ratings yet

- Form 9 - Consent of DP and Subscriber SheetDocument5 pagesForm 9 - Consent of DP and Subscriber SheetCyber VirginNo ratings yet

- "Study of With Respect To '': Padmashri Annasaheb Jadhav Bharatiya Samaj Unnati Mandal'SDocument61 pages"Study of With Respect To '': Padmashri Annasaheb Jadhav Bharatiya Samaj Unnati Mandal'SCyber VirginNo ratings yet

- Effect of Mobile Marketing On Youngsters in Gorakhpur RegionDocument9 pagesEffect of Mobile Marketing On Youngsters in Gorakhpur RegionCyber VirginNo ratings yet

- Top 10 Most Promising Experimental Cancer Treatments: Radiation TherapiesDocument7 pagesTop 10 Most Promising Experimental Cancer Treatments: Radiation TherapiesCyber VirginNo ratings yet

- BissiDocument1 pageBissiCyber VirginNo ratings yet

- Month: Cleaned By: Working Area:: Washroom Cleaning ScheduleDocument1 pageMonth: Cleaned By: Working Area:: Washroom Cleaning ScheduleCyber VirginNo ratings yet

- C4 Tech Spec Issue 2Document5 pagesC4 Tech Spec Issue 2Дмитрий КалининNo ratings yet

- Cemex Holdings Philippines Annual Report 2016 PDFDocument47 pagesCemex Holdings Philippines Annual Report 2016 PDFFritz NatividadNo ratings yet

- Major Crops of Pakistan Wheat, Cotton, Rice, Sugarcane: and MaizeDocument17 pagesMajor Crops of Pakistan Wheat, Cotton, Rice, Sugarcane: and MaizeWaleed Bin khalidNo ratings yet

- Literary Devices DefinitionsDocument2 pagesLiterary Devices DefinitionsAlanna BryantNo ratings yet

- Teaching PronunciationDocument6 pagesTeaching PronunciationKathryn LupsonNo ratings yet

- Sun Pharma ProjectDocument26 pagesSun Pharma ProjectVikas Ahuja100% (1)

- Weekly Home Learning Plan in Mathematics 8: Quarter 1, Week 3, October 19 - 23, 2020Document7 pagesWeekly Home Learning Plan in Mathematics 8: Quarter 1, Week 3, October 19 - 23, 2020Zaldy TabugocaNo ratings yet

- Why Romanian Journal of Food ScienceDocument2 pagesWhy Romanian Journal of Food ScienceAna Vitelariu - RaduNo ratings yet

- Maternal and Infant Care Beliefs Aeta Mothers in PhilippinesDocument8 pagesMaternal and Infant Care Beliefs Aeta Mothers in PhilippinesChristine Joy MolinaNo ratings yet

- 2011 Diving Catalogue BEUCHATDocument60 pages2011 Diving Catalogue BEUCHATRalph KramdenNo ratings yet

- Application DevelopmentDocument14 pagesApplication DevelopmentReema MubarakNo ratings yet

- Hockey - Indian National Game-2compDocument21 pagesHockey - Indian National Game-2compRaj BadreNo ratings yet

- Butterflies and MothsDocument59 pagesButterflies and MothsReegen Tee100% (3)

- The DJ Test: Personalised Report and Recommendations For Alex YachevskiDocument34 pagesThe DJ Test: Personalised Report and Recommendations For Alex YachevskiSashadanceNo ratings yet

- Chords Like Jeff BuckleyDocument5 pagesChords Like Jeff BuckleyTDROCKNo ratings yet

- God Will Protect His Church God Will Protect His ChurchDocument17 pagesGod Will Protect His Church God Will Protect His ChurchLaura GarciaNo ratings yet

- RMS Infosheet Classic Vehicle Scheme Mou 2016 12Document21 pagesRMS Infosheet Classic Vehicle Scheme Mou 2016 12www.toxiconlineNo ratings yet

- Full Download 2014 Psychiatric Mental Health Nursing Revised Reprint 5e Test Bank PDF Full ChapterDocument36 pagesFull Download 2014 Psychiatric Mental Health Nursing Revised Reprint 5e Test Bank PDF Full Chapterpassim.pluvialg5ty6100% (17)

- Agent ListDocument23 pagesAgent ListMayuresh ShakyawarNo ratings yet

- Auto Motivations Digital Cinema and KiarDocument11 pagesAuto Motivations Digital Cinema and KiarDebanjan BandyopadhyayNo ratings yet

- ModulationDocument7 pagesModulationSyeda MiznaNo ratings yet

- Karur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDocument10 pagesKarur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDeepa ManianNo ratings yet

- Satellite CommunicationsDocument57 pagesSatellite Communicationsheritage336No ratings yet

- 8.b SOAL PAT B INGGRIS KELAS 8Document6 pages8.b SOAL PAT B INGGRIS KELAS 8M Adib MasykurNo ratings yet

- Blockchain-Enabled Drug Supply Chain: Sheetal Nayak, Prachitee Shirvale, Nihar Naik, Snehpriya Khul, Amol SawantDocument4 pagesBlockchain-Enabled Drug Supply Chain: Sheetal Nayak, Prachitee Shirvale, Nihar Naik, Snehpriya Khul, Amol SawantWaspNo ratings yet

- L4 02 Causative Verbs Teaching JobDocument4 pagesL4 02 Causative Verbs Teaching JobGeorge VieiraNo ratings yet

- Ecocriticism and Narrative Theory An IntroductionDocument12 pagesEcocriticism and Narrative Theory An IntroductionIdriss BenkacemNo ratings yet