Download as pdf or txt

You might also like

- Audit Test 120514Document3 pagesAudit Test 120514DanCoppe14% (7)

- Ch12 P11 Build A ModelDocument7 pagesCh12 P11 Build A ModelRayudu RamisettiNo ratings yet

- Chapter 3 Problem 9: R&E Supplies Facts and Assumptions ($ Thousands) Actual Forecast Forecast 2017 2018 2019Document5 pagesChapter 3 Problem 9: R&E Supplies Facts and Assumptions ($ Thousands) Actual Forecast Forecast 2017 2018 2019阮幸碧No ratings yet

- Chap 12 SolutionDocument15 pagesChap 12 SolutionMarium Raza0% (1)

- Ch12 Excel ModelDocument23 pagesCh12 Excel ModelDan Johnson50% (2)

- Ch02 P20 Build A ModelDocument6 pagesCh02 P20 Build A ModelLydia PerezNo ratings yet

- Assignment 1 - 2021 - 2022Document4 pagesAssignment 1 - 2021 - 2022Assya El MoukademNo ratings yet

- Export Import ManagementDocument7 pagesExport Import Managementsureya commerceNo ratings yet

- Fin 332 HW 3 Fall 2021Document5 pagesFin 332 HW 3 Fall 2021Alena ChauNo ratings yet

- 10408065Document4 pages10408065Joel Christian MascariñaNo ratings yet

- In These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsDocument53 pagesIn These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsAshekin MahadiNo ratings yet

- Integrative Case 2: Track Software, IncDocument8 pagesIntegrative Case 2: Track Software, IncMohamed Ahmed ZeinNo ratings yet

- Ch02 Tool KitDocument18 pagesCh02 Tool KitPopsy AkinNo ratings yet

- Beams11 ppt04Document49 pagesBeams11 ppt04Rika RieksNo ratings yet

- FedEx Project ReportDocument11 pagesFedEx Project ReportRameez Riaz100% (1)

- Chapter 4 Beams 13ed RevisedDocument28 pagesChapter 4 Beams 13ed RevisedEvan AnwariNo ratings yet

- Chapter 4: Consolidation Techniques and Procedures: Advanced AccountingDocument47 pagesChapter 4: Consolidation Techniques and Procedures: Advanced AccountingRizki BayuNo ratings yet

- AKL 1 - Consolidation Techniques & ProceduresDocument48 pagesAKL 1 - Consolidation Techniques & ProceduresPutri DzakiyyahNo ratings yet

- Chapter 4: Consolidation Techniques and Procedures: Advanced AccountingDocument48 pagesChapter 4: Consolidation Techniques and Procedures: Advanced AccountingDwi PutriAningrumNo ratings yet

- Beams - 12ge - LN04 - Consolidation TechniqueDocument48 pagesBeams - 12ge - LN04 - Consolidation TechniqueArisBachtiarNo ratings yet

- Beams Ch.4Document48 pagesBeams Ch.4Rara Rarara30No ratings yet

- Consolidation Techniques and ProceduresDocument48 pagesConsolidation Techniques and ProceduresSausan SaniaNo ratings yet

- Exam 1 Fall 19Document9 pagesExam 1 Fall 19April Grace TrinidadNo ratings yet

- Consolidation Techniques and Procedures - Cost MethodDocument21 pagesConsolidation Techniques and Procedures - Cost MethodJeremy JansenNo ratings yet

- Intermediate Financial Management 12th Edition Brigham Solutions Manual 1Document36 pagesIntermediate Financial Management 12th Edition Brigham Solutions Manual 1lawrencehigginsdvmepwcnbirjx100% (28)

- Intermediate Financial Management 12Th Edition Brigham Solutions Manual Full Chapter PDFDocument36 pagesIntermediate Financial Management 12Th Edition Brigham Solutions Manual Full Chapter PDFcindy.pettitt386100% (17)

- 04-01 - Financial AnalysisDocument98 pages04-01 - Financial AnalysisSalsabila AufaNo ratings yet

- Chapter 4-6 Advanced Accounting 5009: Roger Mayer 7:00 PM & 8:30 PMDocument43 pagesChapter 4-6 Advanced Accounting 5009: Roger Mayer 7:00 PM & 8:30 PMalejandra_giraldo_3No ratings yet

- 4Q and Full Year 2016 Results Conference CallDocument13 pages4Q and Full Year 2016 Results Conference CallJesusSalamancaNo ratings yet

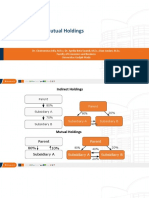

- 09 - IndirectMutual HoldingsDocument36 pages09 - IndirectMutual HoldingsLukas PrawiraNo ratings yet

- Fundamental Analysis of Stocks 1Document4 pagesFundamental Analysis of Stocks 1Vishakha RaiNo ratings yet

- Consolidation Techniques and Procedures (Revised) - Part1Document39 pagesConsolidation Techniques and Procedures (Revised) - Part1Raihan YonaldiiNo ratings yet

- Session 2 - Financial Statement AnalysisDocument43 pagesSession 2 - Financial Statement Analysisluoyifei1988No ratings yet

- Case 3 and 4Document4 pagesCase 3 and 4Syed Osama0% (1)

- Sneaker 2013Document5 pagesSneaker 2013Sheila NNo ratings yet

- New Microsoft Office Word DocumentDocument3 pagesNew Microsoft Office Word DocumentrupokNo ratings yet

- DividendsDocument19 pagesDividendsrezhafalaqNo ratings yet

- Ch03 Tool Kit 2017-09-11Document20 pagesCh03 Tool Kit 2017-09-11Roy HemenwayNo ratings yet

- Beams10e Ch04 Consolidation Techniques and ProceduresDocument48 pagesBeams10e Ch04 Consolidation Techniques and ProceduresLeini TanNo ratings yet

- Yahoo! Inc.: Q3'10 Financial HighlightsDocument24 pagesYahoo! Inc.: Q3'10 Financial HighlightsTechCrunchNo ratings yet

- Yahoo! Inc.: Q3'10 Financial HighlightsDocument24 pagesYahoo! Inc.: Q3'10 Financial HighlightsJay YarowNo ratings yet

- FIN 500 Extra Problems Fall 20-21Document4 pagesFIN 500 Extra Problems Fall 20-21saraNo ratings yet

- Acounting IDocument10 pagesAcounting Ikitty16.fonsecaNo ratings yet

- MK1 CH.4Document27 pagesMK1 CH.4vano aldiNo ratings yet

- The Walt Disney Company Reports Second Quarter and Six Months Earnings For Fiscal 2021Document18 pagesThe Walt Disney Company Reports Second Quarter and Six Months Earnings For Fiscal 2021Josh PetersNo ratings yet

- Annual Report of Lenovo CompanyDocument247 pagesAnnual Report of Lenovo Companychhaihuo pengNo ratings yet

- Tugas Week 8Document6 pagesTugas Week 8Carissa WindyNo ratings yet

- Answers - Partnership OperationsDocument18 pagesAnswers - Partnership OperationsAllondra DapengNo ratings yet

- Chapter 12. Tool Kit For Financial Planning and Forecasting Financial StatementsDocument57 pagesChapter 12. Tool Kit For Financial Planning and Forecasting Financial StatementsHenry RizqyNo ratings yet

- Facebook IPO caseHBRDocument29 pagesFacebook IPO caseHBRCrazy Imaginations100% (1)

- Exercise 5 SolutionDocument4 pagesExercise 5 SolutioneyNo ratings yet

- Department: Banking & Finance Course Title: Business Finance Chapter 3: Financial StatementsDocument14 pagesDepartment: Banking & Finance Course Title: Business Finance Chapter 3: Financial StatementsMhmdNo ratings yet

- PDF DocumentDocument43 pagesPDF DocumentHaris NurNo ratings yet

- Chapter 3Document48 pagesChapter 3Faisal SiddiquiNo ratings yet

- 12 Problem: 10: Corporate Valuation and Financial PlanningDocument141 pages12 Problem: 10: Corporate Valuation and Financial PlanningMarium RazaNo ratings yet

- Chapter 2 Partnership OperationsDocument9 pagesChapter 2 Partnership OperationsmochiNo ratings yet

- Tool Kit For Advanced Issues in Financial Forecasting: Income Statement (In Millions of Dollars)Document3 pagesTool Kit For Advanced Issues in Financial Forecasting: Income Statement (In Millions of Dollars)Thiện NhânNo ratings yet

- Bombardier - 2023 - Full-Year Results - Table - ENDocument1 pageBombardier - 2023 - Full-Year Results - Table - ENBrooklyn WilliamsNo ratings yet

- Chapter 2. Tool Kit For Financial Statements, Cash Flows, and TaxesDocument14 pagesChapter 2. Tool Kit For Financial Statements, Cash Flows, and TaxesAnshumaan SinghNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Beams - 12ge - LN04 - Consolidation TechniqueDocument48 pagesBeams - 12ge - LN04 - Consolidation TechniqueArisBachtiarNo ratings yet

- Lecture 4: Special Distribution Function & Joint Probability DistributionDocument30 pagesLecture 4: Special Distribution Function & Joint Probability DistributionArisBachtiarNo ratings yet

- Week 3Document36 pagesWeek 3ArisBachtiarNo ratings yet

- Week 2Document47 pagesWeek 2ArisBachtiarNo ratings yet

- The History of Life Insurance Companies in India Began With The Establishment of Oriental Life Insurance Company in The Year 1818 in CalcuttaDocument5 pagesThe History of Life Insurance Companies in India Began With The Establishment of Oriental Life Insurance Company in The Year 1818 in CalcuttaPappu JaiswalNo ratings yet

- MP 1st Module MBA 1st Sem 2019Document22 pagesMP 1st Module MBA 1st Sem 2019Babita SutarNo ratings yet

- PDF Chapter 16 30 Valix Practical Accounting 2011 DLDocument429 pagesPDF Chapter 16 30 Valix Practical Accounting 2011 DLChristabel Lecita PuigNo ratings yet

- Handstar Case Excel CalculationsDocument4 pagesHandstar Case Excel CalculationsNithya NairNo ratings yet

- Consumer Choice and Utility Maximization 1Document113 pagesConsumer Choice and Utility Maximization 1KUEENCY RONI TORRANONo ratings yet

- Capital Gains Charts - May 2024 & June 2024Document10 pagesCapital Gains Charts - May 2024 & June 2024CA Tushar GuptaNo ratings yet

- Climate Finance and Net ZeroDocument1 pageClimate Finance and Net ZeroMansiNo ratings yet

- Homework 4Document2 pagesHomework 4kworley89875% (8)

- CNK Firm ProfileDocument21 pagesCNK Firm ProfileSohail MavadiaNo ratings yet

- Lesson 1Document33 pagesLesson 1Cher NaNo ratings yet

- Answers:: Assignment # 1Document2 pagesAnswers:: Assignment # 1pamela dequillamorteNo ratings yet

- Darwin Capuno PT 2 Las 4Document3 pagesDarwin Capuno PT 2 Las 4Darwin CapunoNo ratings yet

- Strategic Management Report For Universal Robina CorporationDocument199 pagesStrategic Management Report For Universal Robina CorporationDoryllllNo ratings yet

- India Prepares - December 2011 (Vol.1 Issue 3)Document92 pagesIndia Prepares - December 2011 (Vol.1 Issue 3)India PreparesNo ratings yet

- Ihs Markit Is SectorsDocument2 pagesIhs Markit Is SectorsKapilanNavaratnamNo ratings yet

- Peregrine Financial Group (PFG), Inc. and Russell Wasendorf SRDocument5 pagesPeregrine Financial Group (PFG), Inc. and Russell Wasendorf SRReign EvansNo ratings yet

- HRISDocument4 pagesHRISAwais ShujaNo ratings yet

- Mba III Cost Management NotesDocument113 pagesMba III Cost Management NotesRavi Gupta67% (3)

- Sustainable RegenerationDocument72 pagesSustainable RegenerationDipayan BhowmikNo ratings yet

- 7 SCM Planning-ERP - 2019 - DISTDocument60 pages7 SCM Planning-ERP - 2019 - DISTJoe RobsonNo ratings yet

- Shayan - VIth Sem (R) - Roll 57 - Tax LAwDocument21 pagesShayan - VIth Sem (R) - Roll 57 - Tax LAwShayan ZafarNo ratings yet

- Ch07 ShowDocument57 pagesCh07 ShowBagus ZijlstraNo ratings yet

- FinanceDocument26 pagesFinanceBhargav D.S.No ratings yet

- Income From Salary Chapter QuestionsDocument5 pagesIncome From Salary Chapter Questionsanon_595315274100% (1)

- MBA Fashion Apparel ManagementDocument1 pageMBA Fashion Apparel ManagementAnonymous eq5zSUNo ratings yet

- Cred Case StudyDocument18 pagesCred Case StudyMohamed Arif PullatNo ratings yet

- Enquiries: 1. Enquiry From A Retailer To A Foreign ManufacturerDocument21 pagesEnquiries: 1. Enquiry From A Retailer To A Foreign ManufacturerVy KhánhNo ratings yet