Download as pdf or txt

You might also like

- Export Contract Template SampleDocument6 pagesExport Contract Template SampleShubhankarNo ratings yet

- FIDIC & ICTAD Formula DifferencesDocument5 pagesFIDIC & ICTAD Formula DifferencesTharaka Kodippily67% (3)

- Simple Linear Regression AnalysisDocument62 pagesSimple Linear Regression AnalysisTom Jubb100% (5)

- Chapter 12-Globalization and The New EconomyDocument21 pagesChapter 12-Globalization and The New EconomyJuMakMat MacNo ratings yet

- Chaos Craft by Steve Dee and Julian VayneDocument211 pagesChaos Craft by Steve Dee and Julian VayneṨĸṳlḷ Kȉď100% (4)

- PL Qa FinalDocument3 pagesPL Qa FinalMarketsWikiNo ratings yet

- Guidance C.2 Pricing DataDocument11 pagesGuidance C.2 Pricing DataKyle MoolmanNo ratings yet

- Basle Capital Accord:: Basle Committee On Banking SupervisionDocument9 pagesBasle Capital Accord:: Basle Committee On Banking SupervisionarunNo ratings yet

- PL Factsheet FinalDocument2 pagesPL Factsheet FinalMarketsWikiNo ratings yet

- Pitch Lake: Oiler Network May 2022Document8 pagesPitch Lake: Oiler Network May 2022lexiNo ratings yet

- 2010 CFTC Energy Rule Fact SheetDocument2 pages2010 CFTC Energy Rule Fact SheetHouston ChronicleNo ratings yet

- Ch9 2016 1Document48 pagesCh9 2016 1Mari MSNo ratings yet

- CECA NEC4 Bulletin No.27 Focus On Engineering and Construction Contract ECC Option B March 2023Document5 pagesCECA NEC4 Bulletin No.27 Focus On Engineering and Construction Contract ECC Option B March 2023Ming MingNo ratings yet

- CD 18178Document4 pagesCD 18178Srinu RachuriNo ratings yet

- Solving The Intertemporal Consumption/saving Problem in Discrete and Continuous TimeDocument42 pagesSolving The Intertemporal Consumption/saving Problem in Discrete and Continuous TimeJoab Dan Valdivia CoriaNo ratings yet

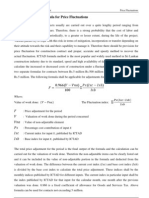

- Price FluctuationDocument13 pagesPrice FluctuationDavid Web50% (2)

- Ch10 Construction ContractsDocument21 pagesCh10 Construction ContractsiKarloNo ratings yet

- 4 Epwps Overivew of Target Cost Option Watermeyer April2007Document8 pages4 Epwps Overivew of Target Cost Option Watermeyer April2007sNo ratings yet

- Eurodollar Convexity Adjustment in Stochastic Vol ModelsDocument19 pagesEurodollar Convexity Adjustment in Stochastic Vol ModelsJamesMc1144No ratings yet

- Option C Target Contract - WatermeyerDocument7 pagesOption C Target Contract - WatermeyerCamilo RamirezNo ratings yet

- Ias 11 SummaryDocument6 pagesIas 11 Summarypradyp15No ratings yet

- Privatisation and Regulation of BusinessDocument24 pagesPrivatisation and Regulation of BusinessTarakeshwar AllamsettyNo ratings yet

- SPE 102874 Pricing of Long-Term Oil Service Contracts and Financial Risk ManagementDocument5 pagesSPE 102874 Pricing of Long-Term Oil Service Contracts and Financial Risk Managementjoo123456789No ratings yet

- E-Con 484 TranscriptDocument6 pagesE-Con 484 Transcriptjhj01No ratings yet

- CH 2 GaliDocument33 pagesCH 2 Galijesua21No ratings yet

- As LB 17764Document27 pagesAs LB 17764ratiNo ratings yet

- Pain/Gain-Sharing Mechanism: 3. Experience in The Application of CPFSDocument3 pagesPain/Gain-Sharing Mechanism: 3. Experience in The Application of CPFSAnonymous ufMAGXcskMNo ratings yet

- Suzy Tharwat Nashed Report 1Document8 pagesSuzy Tharwat Nashed Report 1Suzy TharwatNo ratings yet

- NEC Contracts - One Stop ShopDocument3 pagesNEC Contracts - One Stop ShopHarish NeelakantanNo ratings yet

- Standard EPC Documents: V. Energy Performance ContractsDocument10 pagesStandard EPC Documents: V. Energy Performance ContractsNaufal AlhadyNo ratings yet

- NPV PDFDocument8 pagesNPV PDFatolosaNo ratings yet

- Pricing Fixed Income Securities: Zero Coupon Yield CurvesDocument19 pagesPricing Fixed Income Securities: Zero Coupon Yield CurvesashishkjhaNo ratings yet

- Tender Estimation Lecture Note 05Document2 pagesTender Estimation Lecture Note 05rachuNo ratings yet

- Measure and Pay ContractsDocument3 pagesMeasure and Pay ContractsRanjith Ekanayake100% (2)

- Call Warrants FINAL TERMS Linked To OMX30SDocument62 pagesCall Warrants FINAL TERMS Linked To OMX30SJianhua CaoNo ratings yet

- Commodity Futures Trading Commission: Office of Public AffairsDocument2 pagesCommodity Futures Trading Commission: Office of Public AffairsMarketsWikiNo ratings yet

- C 1 June 2011 FM ArticleDocument2 pagesC 1 June 2011 FM ArticleDammika MadusankaNo ratings yet

- Bloomberg ModelDocument12 pagesBloomberg ModelDavid C PostiglioneNo ratings yet

- Cost-plus-Fixed-Fee Contracts With Payment Ceilings: Impact On Commercial Markets and Indirect Cost RecoveriesDocument25 pagesCost-plus-Fixed-Fee Contracts With Payment Ceilings: Impact On Commercial Markets and Indirect Cost RecoveriesyasinthaNo ratings yet

- T3TLC - Letters of Credit - R13 1Document436 pagesT3TLC - Letters of Credit - R13 1Gnana Sambandam100% (1)

- In Accounting For ContractsDocument7 pagesIn Accounting For Contractsone formanyNo ratings yet

- Accounting Seminar - Assignment CH 10 (Doni Rahmad & Fachriza Mizafin)Document5 pagesAccounting Seminar - Assignment CH 10 (Doni Rahmad & Fachriza Mizafin)Kazuyano DoniNo ratings yet

- Paper-ASCE-Model For Legal Principles of Compensation For Errors in Bills of Quantities-A Law and Economics AnalysisDocument10 pagesPaper-ASCE-Model For Legal Principles of Compensation For Errors in Bills of Quantities-A Law and Economics AnalysisegglestonaNo ratings yet

- Interest Rate DerivativesDocument17 pagesInterest Rate Derivativescharles luisNo ratings yet

- International Services Contract Template SampleDocument6 pagesInternational Services Contract Template SampleKushal BagdeNo ratings yet

- ProspectusDocument5 pagesProspectusAnno NymousNo ratings yet

- Chand Bhaiya ..Document26 pagesChand Bhaiya ..Aditya RajNo ratings yet

- Information Sheet: Overview of The Balancing and Settlement Code (BSC) ArrangementsDocument3 pagesInformation Sheet: Overview of The Balancing and Settlement Code (BSC) ArrangementsJana TufegdzicNo ratings yet

- Financial Reporting: IAS 11 - Construction ContractsDocument6 pagesFinancial Reporting: IAS 11 - Construction ContractsazmattullahNo ratings yet

- SPAN Margin Parameter Layout Guide v2.4Document15 pagesSPAN Margin Parameter Layout Guide v2.4Sourav ChakrabortyNo ratings yet

- LM06 Pricing and Valuation of Futures Contracts IFT NotesDocument7 pagesLM06 Pricing and Valuation of Futures Contracts IFT NotesRidhtang DuggalNo ratings yet

- NEC Contract ComparisonsDocument9 pagesNEC Contract ComparisonsKarl AttardNo ratings yet

- Transfer Pricing Eco CfaDocument17 pagesTransfer Pricing Eco CfaJoseph GrahamNo ratings yet

- 6812 - 2017 - Ex8 - 8-17-17 + ANSWERS - Fluctuations Defects Notification PeriodDocument7 pages6812 - 2017 - Ex8 - 8-17-17 + ANSWERS - Fluctuations Defects Notification Periodრაქსშ საჰაNo ratings yet

- Transfer PricingDocument18 pagesTransfer PricingSunny SharmaNo ratings yet

- IAS 11 Construction Contracts Summary With Example p4gDocument4 pagesIAS 11 Construction Contracts Summary With Example p4gvaradu1963No ratings yet

- 1530 Corrigendum-1Document7 pages1530 Corrigendum-1manojkumarmurlidharaNo ratings yet

- Id FuturesDocument3 pagesId Futuresnraja_accetNo ratings yet

- EU China Energy Magazine 2023 March Issue: 2023, #2From EverandEU China Energy Magazine 2023 March Issue: 2023, #2No ratings yet

- Practical Guide to the NEC3 Professional Services ContractFrom EverandPractical Guide to the NEC3 Professional Services ContractNo ratings yet

- CFTC Final RuleDocument52 pagesCFTC Final RuleMarketsWikiNo ratings yet

- Minute Entry 336Document1 pageMinute Entry 336MarketsWikiNo ratings yet

- Federal Register / Vol. 81, No. 88 / Friday, May 6, 2016 / Rules and RegulationsDocument6 pagesFederal Register / Vol. 81, No. 88 / Friday, May 6, 2016 / Rules and RegulationsMarketsWikiNo ratings yet

- 34 77617 PDFDocument783 pages34 77617 PDFMarketsWikiNo ratings yet

- Federal Register / Vol. 81, No. 55 / Tuesday, March 22, 2016 / NoticesDocument13 pagesFederal Register / Vol. 81, No. 55 / Tuesday, March 22, 2016 / NoticesMarketsWikiNo ratings yet

- Via Electronic Submission: Modern Markets Initiative 545 Madison Avenue New York, NY 10022 (646) 536-7400Document7 pagesVia Electronic Submission: Modern Markets Initiative 545 Madison Avenue New York, NY 10022 (646) 536-7400MarketsWikiNo ratings yet

- Commodity Futures Trading Commission: Office of Public AffairsDocument2 pagesCommodity Futures Trading Commission: Office of Public AffairsMarketsWikiNo ratings yet

- Eemac022516 EemacreportDocument14 pagesEemac022516 EemacreportMarketsWikiNo ratings yet

- Commodity Futures Trading Commission: Vol. 80 Wednesday, No. 246 December 23, 2015Document26 pagesCommodity Futures Trading Commission: Vol. 80 Wednesday, No. 246 December 23, 2015MarketsWikiNo ratings yet

- Douglas C I FuDocument4 pagesDouglas C I FuMarketsWikiNo ratings yet

- Commodity Futures Trading Commission: Office of Public AffairsDocument2 pagesCommodity Futures Trading Commission: Office of Public AffairsMarketsWikiNo ratings yet

- 2015-10-22 Notice Dis A FR Final-RuleDocument281 pages2015-10-22 Notice Dis A FR Final-RuleMarketsWikiNo ratings yet

- Commodity Futures Trading Commission: Office of Public AffairsDocument3 pagesCommodity Futures Trading Commission: Office of Public AffairsMarketsWikiNo ratings yet

- Commodity Futures Trading Commission: Office of Public AffairsDocument5 pagesCommodity Futures Trading Commission: Office of Public AffairsMarketsWikiNo ratings yet

- Daniel Deli, Paul Hanouna, Christof W. Stahel, Yue Tang and William YostDocument97 pagesDaniel Deli, Paul Hanouna, Christof W. Stahel, Yue Tang and William YostMarketsWikiNo ratings yet

- 34 76474 PDFDocument584 pages34 76474 PDFMarketsWikiNo ratings yet

- Odrgreportg20 1115Document10 pagesOdrgreportg20 1115MarketsWikiNo ratings yet

- ch1 NEW Physics 12 Study GuideDocument16 pagesch1 NEW Physics 12 Study GuidemllupoNo ratings yet

- Dio125 and Hornet2 RepsolDocument2 pagesDio125 and Hornet2 RepsolSibi SundarNo ratings yet

- Math in Focus 3B WorksheetDocument6 pagesMath in Focus 3B WorksheetBobbili PooliNo ratings yet

- 536805502401 (1)Document30 pages536805502401 (1)kedarkNo ratings yet

- LIC Exp Date: AetnaDocument66 pagesLIC Exp Date: AetnaTrudyNo ratings yet

- PGM List R1 - 05.04.2018Document58 pagesPGM List R1 - 05.04.2018Shubham Shinde100% (1)

- Energy Recovery From Landing AircraftDocument8 pagesEnergy Recovery From Landing AircraftRaniero FalzonNo ratings yet

- Starter Case 580M 1Document4 pagesStarter Case 580M 1JESUSNo ratings yet

- Central Nervous System StimulantsDocument6 pagesCentral Nervous System StimulantsNathalia CabalseNo ratings yet

- BI Strategy Roadmap Final v1.3Document201 pagesBI Strategy Roadmap Final v1.3Ange OraudNo ratings yet

- Cse320 MCQDocument12 pagesCse320 MCQAnsh Gulati ji100% (1)

- Department of Education: Republic of The PhilippinesDocument3 pagesDepartment of Education: Republic of The PhilippinesRussel RapisoraNo ratings yet

- Testes Avaliação Inglês 6º AnoDocument43 pagesTestes Avaliação Inglês 6º AnoRui PauloNo ratings yet

- Production of Xylitol From Corn Cob Hydrolysate - Mardawati - 2018 - IOP - Conf. - Ser. - Earth - Environ. - Sci. - 141 - 012019Document12 pagesProduction of Xylitol From Corn Cob Hydrolysate - Mardawati - 2018 - IOP - Conf. - Ser. - Earth - Environ. - Sci. - 141 - 012019RosalinaIlmiAmaliaNo ratings yet

- Mastering Sketching S11 BLAD Print2Document8 pagesMastering Sketching S11 BLAD Print2Interweave0% (1)

- Implicit and Explicit InformationDocument3 pagesImplicit and Explicit InformationAbbas GholamiNo ratings yet

- 2046 - Decorative Synthetic Bonded Laminated SheetsDocument53 pages2046 - Decorative Synthetic Bonded Laminated SheetsKaushik SenguptaNo ratings yet

- Kreativitas Dan Inovasi Berpengaruh Terhadap Kewirausahaan Usaha KecilDocument17 pagesKreativitas Dan Inovasi Berpengaruh Terhadap Kewirausahaan Usaha Kecilapsari hasanNo ratings yet

- RTS Unit 1 NotesDocument24 pagesRTS Unit 1 NotesSAROJ RAJANo ratings yet

- Mini WorkshopDocument27 pagesMini Workshopapi-548854218No ratings yet

- WBC Histogram - Interpretations of 3-Part Differentiation (Sysmex) PDFDocument5 pagesWBC Histogram - Interpretations of 3-Part Differentiation (Sysmex) PDFRuxandra Mesaros100% (1)

- Electromagnetic Compatibility: Interference Caused by The TransmitterDocument12 pagesElectromagnetic Compatibility: Interference Caused by The TransmitterpalahobaraNo ratings yet

- P PotassiumDocument12 pagesP PotassiumHeleneSmithNo ratings yet

- 02 Kinematics VectorsDocument16 pages02 Kinematics VectorsAnna HansenNo ratings yet

- Wisconsin Public Library Standards 6th Edition 2018 FINALDocument49 pagesWisconsin Public Library Standards 6th Edition 2018 FINALemac1983No ratings yet

- Legends of The Konkan - CrawfordDocument322 pagesLegends of The Konkan - CrawfordDeepak GoreNo ratings yet

- Heredity and EvolutionDocument5 pagesHeredity and EvolutionRahul Ecka100% (3)

- Blockchain For Iot: The Challenges and A Way Forward: July 2018Document13 pagesBlockchain For Iot: The Challenges and A Way Forward: July 2018ronicaNo ratings yet