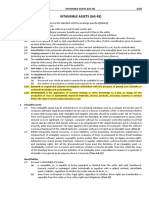

Topic 10 - Intangible Assets

Topic 10 - Intangible Assets

You might also like

- Petition For ReissuanceDocument6 pagesPetition For Reissuanceasdfg100% (7)

- IS 105 - IM - Unit 2 - Lesson 2-3Document15 pagesIS 105 - IM - Unit 2 - Lesson 2-3Eki Omallao100% (1)

- GE EL 102 Gender and Society With Signed FL SyllabusDocument73 pagesGE EL 102 Gender and Society With Signed FL SyllabusEki Omallao100% (9)

- Newham Property Licensing GuideDocument37 pagesNewham Property Licensing GuideRyan HengNo ratings yet

- Universal College of Parañaque: Working Capital ManagementDocument23 pagesUniversal College of Parañaque: Working Capital ManagementEmelita ManlangitNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 IntangiblesEarl ENo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 Intangiblestite ko'y malakeNo ratings yet

- 19 - Intangible AssetsDocument10 pages19 - Intangible AssetsYudna YuNo ratings yet

- Objective: o o o o oDocument5 pagesObjective: o o o o oShakeel AhmedNo ratings yet

- Summary of IAS 38Document5 pagesSummary of IAS 38Jaanu SanthiranNo ratings yet

- Summary of IAS 38Document7 pagesSummary of IAS 38Cyhra Diane MabaoNo ratings yet

- Intangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceDocument6 pagesIntangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceGianrie Gwyneth CabigonNo ratings yet

- Ias 38 Intangible AssetsDocument4 pagesIas 38 Intangible AssetsYogesh BhattaraiNo ratings yet

- AP.1205B Intangible-Assets-W HIGHLIGHTSDocument16 pagesAP.1205B Intangible-Assets-W HIGHLIGHTSdave excelleNo ratings yet

- Summary of IAS 38Document6 pagesSummary of IAS 38Rey Jr AlipisNo ratings yet

- DocumentDocument44 pagesDocumentKenjie Mae ResurreccionNo ratings yet

- Intangible Assets NotesDocument6 pagesIntangible Assets NotesRaizel RamirezNo ratings yet

- Intangible Assets Lecture and ExercisesDocument16 pagesIntangible Assets Lecture and ExercisesRNo ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical SummaryFoititika.net100% (2)

- Pas 38Document8 pagesPas 38AngelicaNo ratings yet

- L6 Intangible AssetsDocument43 pagesL6 Intangible AssetsЛинкольн ХaйдаровNo ratings yet

- Summary of IAS 38-Intangible AssetsDocument5 pagesSummary of IAS 38-Intangible AssetsVikash HurrydossNo ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- Accounting For Property, Plant and Equipment, Intangibles and Impairment of Assets Week 12-13 AssessmentsDocument13 pagesAccounting For Property, Plant and Equipment, Intangibles and Impairment of Assets Week 12-13 AssessmentsAllia LandigNo ratings yet

- Intangible AssetDocument38 pagesIntangible AssetRimissha Udenia 2No ratings yet

- Accounting GuidanceDocument5 pagesAccounting GuidanceVibha MittalNo ratings yet

- Ias 38 Intangible Assets SummaryDocument8 pagesIas 38 Intangible Assets SummaryPandu WiratamaNo ratings yet

- 04 Ias 38Document4 pages04 Ias 38Irtiza AbbasNo ratings yet

- Chapter 20Document25 pagesChapter 20Crysta LeeNo ratings yet

- Indas 38Document6 pagesIndas 38SanjayNo ratings yet

- Intangible AssetDocument5 pagesIntangible AssetRozele DonesNo ratings yet

- Module 4 - INTACC2 Intangible AssetsDocument20 pagesModule 4 - INTACC2 Intangible AssetsKhan TanNo ratings yet

- Chapter 21 INTANGIBLE ASSSETSDocument38 pagesChapter 21 INTANGIBLE ASSSETSmarj ponceNo ratings yet

- Intangible AssetsDocument99 pagesIntangible AssetsXNo ratings yet

- Intangible Assets1Document22 pagesIntangible Assets1hamarshi2010No ratings yet

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical Summaryanon-553693100% (2)

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- Lecture Notes: Nature of Intangible Assets RecognitionDocument5 pagesLecture Notes: Nature of Intangible Assets RecognitionRyan Carta50% (2)

- Intangible Assets: International Accounting Standard 38Document19 pagesIntangible Assets: International Accounting Standard 38ZayaNo ratings yet

- Intangible AssetsDocument16 pagesIntangible Assets566973801967% (3)

- IAS 38 Intangible AssetsDocument20 pagesIAS 38 Intangible AssetsEmon EftakarNo ratings yet

- Intangible AssetsDocument6 pagesIntangible Assetsmark fernandezNo ratings yet

- Solution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDocument22 pagesSolution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDouglasWhiteheadxkwi100% (49)

- Ias 38Document7 pagesIas 38Researcher BrianNo ratings yet

- Chapter 21 Intangible AssetsDocument10 pagesChapter 21 Intangible AssetsEllen MaskariñoNo ratings yet

- Accounting For Intangibles ACC C205 202A INTERMEDIATE ACCTG 1 PDFDocument5 pagesAccounting For Intangibles ACC C205 202A INTERMEDIATE ACCTG 1 PDFAsdfghjkl LkjhgfdsaNo ratings yet

- Chapter 11 Intagible AssetsDocument5 pagesChapter 11 Intagible Assetsmaria isabellaNo ratings yet

- #23 Intangible Assets (Notes For 6208)Document6 pages#23 Intangible Assets (Notes For 6208)jaysonNo ratings yet

- Inte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleDocument9 pagesInte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleVMRONo ratings yet

- Chapter 7 Intangible AssetsDocument34 pagesChapter 7 Intangible AssetsHammad Ahmad100% (5)

- IAS 38 - Intangible AssetsDocument13 pagesIAS 38 - Intangible AssetsKhuraim Abu BakrNo ratings yet

- Isa 38Document7 pagesIsa 38shahidgondal17No ratings yet

- Notes PDFDocument36 pagesNotes PDFtp linkNo ratings yet

- Ind As 38Document14 pagesInd As 38Juthika Bora100% (1)

- CFAS Notes For FINALS PDFDocument26 pagesCFAS Notes For FINALS PDFMarife PangesbanNo ratings yet

- Accounting For Intangible Asset IAS 38Document2 pagesAccounting For Intangible Asset IAS 38MIKIYAS BERHENo ratings yet

- 6) Ias-38Document15 pages6) Ias-38manvi jainNo ratings yet

- Ias 38Document33 pagesIas 38Reever River100% (1)

- Module 5 - Intangible AssetsDocument8 pagesModule 5 - Intangible AssetsLui0% (2)

- Chapter 7 Intangible AssetsDocument70 pagesChapter 7 Intangible AssetsLovely AbadianoNo ratings yet

- IAS 38 Intangible For PresentDocument20 pagesIAS 38 Intangible For Presentnati100% (2)

- FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3Document2 pagesFR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3User Upload and downloadNo ratings yet

- F7 Summary Dec 2011Document30 pagesF7 Summary Dec 2011artkodis100% (1)

- Quiz 6 - Lesson 3 - Writing Product and Office ManualsDocument5 pagesQuiz 6 - Lesson 3 - Writing Product and Office ManualsEki OmallaoNo ratings yet

- PATH FIT - ACTIVATE Activity 4Document1 pagePATH FIT - ACTIVATE Activity 4Eki OmallaoNo ratings yet

- Test Your Knowledge!: Encircle The Letter of The Correct AnswerDocument1 pageTest Your Knowledge!: Encircle The Letter of The Correct AnswerEki OmallaoNo ratings yet

- Test Your Knowledge!: Encircle The Letter of The Correct AnswerDocument1 pageTest Your Knowledge!: Encircle The Letter of The Correct AnswerEki OmallaoNo ratings yet

- LESSON 2 Establishing A NationDocument1 pageLESSON 2 Establishing A NationEki OmallaoNo ratings yet

- Ia 2 NotesDocument1 pageIa 2 NotesEki OmallaoNo ratings yet

- Lesson 9 ActivityDocument1 pageLesson 9 ActivityEki OmallaoNo ratings yet

- Apply Activity 12Document2 pagesApply Activity 12Eki OmallaoNo ratings yet

- Gella, Shekinah O. Bsa 2B Apply: Activity 6: Understanding The Notes!Document1 pageGella, Shekinah O. Bsa 2B Apply: Activity 6: Understanding The Notes!Eki OmallaoNo ratings yet

- Cost Acc. QuizDocument3 pagesCost Acc. QuizEki OmallaoNo ratings yet

- Anti-Sexual Harassment ACT OF 1995: Republic Act (Ra) No. 7877Document1 pageAnti-Sexual Harassment ACT OF 1995: Republic Act (Ra) No. 7877Eki OmallaoNo ratings yet

- Intro To IS 105 - Parts of SpeechDocument9 pagesIntro To IS 105 - Parts of SpeechEki OmallaoNo ratings yet

- These Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoDocument8 pagesThese Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoEki OmallaoNo ratings yet

- Phil - History FINALDocument8 pagesPhil - History FINALEki Omallao90% (10)

- Unit-3 NSTP2 Worksheet 2Document4 pagesUnit-3 NSTP2 Worksheet 2Eki OmallaoNo ratings yet

- Weighted and FIFO Costing - Practice ProblemsDocument9 pagesWeighted and FIFO Costing - Practice ProblemsEki OmallaoNo ratings yet

- FAR 2922 Investments in Equity Instruments PDFDocument5 pagesFAR 2922 Investments in Equity Instruments PDFEki OmallaoNo ratings yet

- These Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoDocument7 pagesThese Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoEki OmallaoNo ratings yet

- Topic 18-22 - Investments and Basic Derivatives (Compiled)Document37 pagesTopic 18-22 - Investments and Basic Derivatives (Compiled)Eki OmallaoNo ratings yet

- Chapter 7Document10 pagesChapter 7Eki OmallaoNo ratings yet

- Assessing Four SkillsDocument19 pagesAssessing Four SkillsEki OmallaoNo ratings yet

- Call FlowDocument1 pageCall FlowEki OmallaoNo ratings yet

- Ae12 Course File Econ DevDocument49 pagesAe12 Course File Econ DevEki OmallaoNo ratings yet

- Categories of Historical SourcesDocument8 pagesCategories of Historical SourcesEki OmallaoNo ratings yet

- Freer On Corporations BarbriDocument38 pagesFreer On Corporations BarbriJEL100% (1)

- Rule 111 JM Dominguez V Liclican DIGESTDocument1 pageRule 111 JM Dominguez V Liclican DIGESTStephen Celoso EscartinNo ratings yet

- PriceList - Realtech The Indiana - 99acresDocument3 pagesPriceList - Realtech The Indiana - 99acresSayantanSamaddar100% (1)

- Isaca Crisc SampleDocument50 pagesIsaca Crisc SampleKirthika BojarajanNo ratings yet

- Risk Surcharge: AWB No: H63537762 Owner CarrierDocument1 pageRisk Surcharge: AWB No: H63537762 Owner CarrierAnandNo ratings yet

- Term Paper About Human TraffickingDocument7 pagesTerm Paper About Human Traffickingeryhlxwgf100% (1)

- Agreement PreviewDocument7 pagesAgreement PreviewKumar utsavNo ratings yet

- English 9 Module 1 Activity 1Document1 pageEnglish 9 Module 1 Activity 1Rowell Digal BainNo ratings yet

- Sweden: WHAT CAN WE LEARN FROM SWEDEN'S DRUG POLICY EXPERIENCE?Document11 pagesSweden: WHAT CAN WE LEARN FROM SWEDEN'S DRUG POLICY EXPERIENCE?Paul Gallagher100% (1)

- Big Tech InjunctionDocument155 pagesBig Tech InjunctionWashington ExaminerNo ratings yet

- HDFC Life InsuranceDocument1 pageHDFC Life InsuranceSureshKarnanNo ratings yet

- Weimer, D.L. Vining, A.R. Policy Analysis Concepts & Practice in Policy Analysis Concepts (274-279)Document8 pagesWeimer, D.L. Vining, A.R. Policy Analysis Concepts & Practice in Policy Analysis Concepts (274-279)HM KNo ratings yet

- ANSWER Unlawful DetainerDocument5 pagesANSWER Unlawful DetainerJoshua100% (1)

- Electronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationDocument10 pagesElectronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationStan J. CaterboneNo ratings yet

- 5 6334567979774116073 PDFDocument418 pages5 6334567979774116073 PDFSuman Sourav0% (1)

- RealEstate SingaporeDocument2 pagesRealEstate SingaporeKyaw Kyaw AungNo ratings yet

- Business Ethics: Dr. Rajinder KaurDocument24 pagesBusiness Ethics: Dr. Rajinder KaurDeepak SarojNo ratings yet

- Jeff Pippenger - Seven Times in LeviticusDocument16 pagesJeff Pippenger - Seven Times in LeviticusKelly K.R. RossNo ratings yet

- New Stockiest Appointment Check ListDocument18 pagesNew Stockiest Appointment Check ListRamana GNo ratings yet

- RA 8799 - Securities Regulation CodeDocument38 pagesRA 8799 - Securities Regulation CodeJacinto Jr Jamero100% (1)

- United Food Imports V Baroody ImportsDocument13 pagesUnited Food Imports V Baroody ImportspropertyintangibleNo ratings yet

- Registration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Document2 pagesRegistration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Sunlight FoundationNo ratings yet

- The HR Management and Payroll CycleDocument97 pagesThe HR Management and Payroll CycleErwin David SianturiNo ratings yet

- Invoice: List of ContainersDocument1 pageInvoice: List of ContainersCHINo ratings yet

- Financial Ratio Template Free V61Document9 pagesFinancial Ratio Template Free V61Tommy RamadanNo ratings yet

- ICSE IX Maths LogarithmsDocument2 pagesICSE IX Maths LogarithmsBarnali DuttaNo ratings yet

- Confessions of An Economic Hit ManDocument4 pagesConfessions of An Economic Hit ManMuhammad AamirNo ratings yet

Download as pdf or txt

You might also like

- Petition For ReissuanceDocument6 pagesPetition For Reissuanceasdfg100% (7)

- IS 105 - IM - Unit 2 - Lesson 2-3Document15 pagesIS 105 - IM - Unit 2 - Lesson 2-3Eki Omallao100% (1)

- GE EL 102 Gender and Society With Signed FL SyllabusDocument73 pagesGE EL 102 Gender and Society With Signed FL SyllabusEki Omallao100% (9)

- Newham Property Licensing GuideDocument37 pagesNewham Property Licensing GuideRyan HengNo ratings yet

- Universal College of Parañaque: Working Capital ManagementDocument23 pagesUniversal College of Parañaque: Working Capital ManagementEmelita ManlangitNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 IntangiblesEarl ENo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 Intangiblestite ko'y malakeNo ratings yet

- 19 - Intangible AssetsDocument10 pages19 - Intangible AssetsYudna YuNo ratings yet

- Objective: o o o o oDocument5 pagesObjective: o o o o oShakeel AhmedNo ratings yet

- Summary of IAS 38Document5 pagesSummary of IAS 38Jaanu SanthiranNo ratings yet

- Summary of IAS 38Document7 pagesSummary of IAS 38Cyhra Diane MabaoNo ratings yet

- Intangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceDocument6 pagesIntangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceGianrie Gwyneth CabigonNo ratings yet

- Ias 38 Intangible AssetsDocument4 pagesIas 38 Intangible AssetsYogesh BhattaraiNo ratings yet

- AP.1205B Intangible-Assets-W HIGHLIGHTSDocument16 pagesAP.1205B Intangible-Assets-W HIGHLIGHTSdave excelleNo ratings yet

- Summary of IAS 38Document6 pagesSummary of IAS 38Rey Jr AlipisNo ratings yet

- DocumentDocument44 pagesDocumentKenjie Mae ResurreccionNo ratings yet

- Intangible Assets NotesDocument6 pagesIntangible Assets NotesRaizel RamirezNo ratings yet

- Intangible Assets Lecture and ExercisesDocument16 pagesIntangible Assets Lecture and ExercisesRNo ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical SummaryFoititika.net100% (2)

- Pas 38Document8 pagesPas 38AngelicaNo ratings yet

- L6 Intangible AssetsDocument43 pagesL6 Intangible AssetsЛинкольн ХaйдаровNo ratings yet

- Summary of IAS 38-Intangible AssetsDocument5 pagesSummary of IAS 38-Intangible AssetsVikash HurrydossNo ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- Accounting For Property, Plant and Equipment, Intangibles and Impairment of Assets Week 12-13 AssessmentsDocument13 pagesAccounting For Property, Plant and Equipment, Intangibles and Impairment of Assets Week 12-13 AssessmentsAllia LandigNo ratings yet

- Intangible AssetDocument38 pagesIntangible AssetRimissha Udenia 2No ratings yet

- Accounting GuidanceDocument5 pagesAccounting GuidanceVibha MittalNo ratings yet

- Ias 38 Intangible Assets SummaryDocument8 pagesIas 38 Intangible Assets SummaryPandu WiratamaNo ratings yet

- 04 Ias 38Document4 pages04 Ias 38Irtiza AbbasNo ratings yet

- Chapter 20Document25 pagesChapter 20Crysta LeeNo ratings yet

- Indas 38Document6 pagesIndas 38SanjayNo ratings yet

- Intangible AssetDocument5 pagesIntangible AssetRozele DonesNo ratings yet

- Module 4 - INTACC2 Intangible AssetsDocument20 pagesModule 4 - INTACC2 Intangible AssetsKhan TanNo ratings yet

- Chapter 21 INTANGIBLE ASSSETSDocument38 pagesChapter 21 INTANGIBLE ASSSETSmarj ponceNo ratings yet

- Intangible AssetsDocument99 pagesIntangible AssetsXNo ratings yet

- Intangible Assets1Document22 pagesIntangible Assets1hamarshi2010No ratings yet

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical Summaryanon-553693100% (2)

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- Lecture Notes: Nature of Intangible Assets RecognitionDocument5 pagesLecture Notes: Nature of Intangible Assets RecognitionRyan Carta50% (2)

- Intangible Assets: International Accounting Standard 38Document19 pagesIntangible Assets: International Accounting Standard 38ZayaNo ratings yet

- Intangible AssetsDocument16 pagesIntangible Assets566973801967% (3)

- IAS 38 Intangible AssetsDocument20 pagesIAS 38 Intangible AssetsEmon EftakarNo ratings yet

- Intangible AssetsDocument6 pagesIntangible Assetsmark fernandezNo ratings yet

- Solution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDocument22 pagesSolution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDouglasWhiteheadxkwi100% (49)

- Ias 38Document7 pagesIas 38Researcher BrianNo ratings yet

- Chapter 21 Intangible AssetsDocument10 pagesChapter 21 Intangible AssetsEllen MaskariñoNo ratings yet

- Accounting For Intangibles ACC C205 202A INTERMEDIATE ACCTG 1 PDFDocument5 pagesAccounting For Intangibles ACC C205 202A INTERMEDIATE ACCTG 1 PDFAsdfghjkl LkjhgfdsaNo ratings yet

- Chapter 11 Intagible AssetsDocument5 pagesChapter 11 Intagible Assetsmaria isabellaNo ratings yet

- #23 Intangible Assets (Notes For 6208)Document6 pages#23 Intangible Assets (Notes For 6208)jaysonNo ratings yet

- Inte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleDocument9 pagesInte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleVMRONo ratings yet

- Chapter 7 Intangible AssetsDocument34 pagesChapter 7 Intangible AssetsHammad Ahmad100% (5)

- IAS 38 - Intangible AssetsDocument13 pagesIAS 38 - Intangible AssetsKhuraim Abu BakrNo ratings yet

- Isa 38Document7 pagesIsa 38shahidgondal17No ratings yet

- Notes PDFDocument36 pagesNotes PDFtp linkNo ratings yet

- Ind As 38Document14 pagesInd As 38Juthika Bora100% (1)

- CFAS Notes For FINALS PDFDocument26 pagesCFAS Notes For FINALS PDFMarife PangesbanNo ratings yet

- Accounting For Intangible Asset IAS 38Document2 pagesAccounting For Intangible Asset IAS 38MIKIYAS BERHENo ratings yet

- 6) Ias-38Document15 pages6) Ias-38manvi jainNo ratings yet

- Ias 38Document33 pagesIas 38Reever River100% (1)

- Module 5 - Intangible AssetsDocument8 pagesModule 5 - Intangible AssetsLui0% (2)

- Chapter 7 Intangible AssetsDocument70 pagesChapter 7 Intangible AssetsLovely AbadianoNo ratings yet

- IAS 38 Intangible For PresentDocument20 pagesIAS 38 Intangible For Presentnati100% (2)

- FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3Document2 pagesFR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3User Upload and downloadNo ratings yet

- F7 Summary Dec 2011Document30 pagesF7 Summary Dec 2011artkodis100% (1)

- Quiz 6 - Lesson 3 - Writing Product and Office ManualsDocument5 pagesQuiz 6 - Lesson 3 - Writing Product and Office ManualsEki OmallaoNo ratings yet

- PATH FIT - ACTIVATE Activity 4Document1 pagePATH FIT - ACTIVATE Activity 4Eki OmallaoNo ratings yet

- Test Your Knowledge!: Encircle The Letter of The Correct AnswerDocument1 pageTest Your Knowledge!: Encircle The Letter of The Correct AnswerEki OmallaoNo ratings yet

- Test Your Knowledge!: Encircle The Letter of The Correct AnswerDocument1 pageTest Your Knowledge!: Encircle The Letter of The Correct AnswerEki OmallaoNo ratings yet

- LESSON 2 Establishing A NationDocument1 pageLESSON 2 Establishing A NationEki OmallaoNo ratings yet

- Ia 2 NotesDocument1 pageIa 2 NotesEki OmallaoNo ratings yet

- Lesson 9 ActivityDocument1 pageLesson 9 ActivityEki OmallaoNo ratings yet

- Apply Activity 12Document2 pagesApply Activity 12Eki OmallaoNo ratings yet

- Gella, Shekinah O. Bsa 2B Apply: Activity 6: Understanding The Notes!Document1 pageGella, Shekinah O. Bsa 2B Apply: Activity 6: Understanding The Notes!Eki OmallaoNo ratings yet

- Cost Acc. QuizDocument3 pagesCost Acc. QuizEki OmallaoNo ratings yet

- Anti-Sexual Harassment ACT OF 1995: Republic Act (Ra) No. 7877Document1 pageAnti-Sexual Harassment ACT OF 1995: Republic Act (Ra) No. 7877Eki OmallaoNo ratings yet

- Intro To IS 105 - Parts of SpeechDocument9 pagesIntro To IS 105 - Parts of SpeechEki OmallaoNo ratings yet

- These Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoDocument8 pagesThese Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoEki OmallaoNo ratings yet

- Phil - History FINALDocument8 pagesPhil - History FINALEki Omallao90% (10)

- Unit-3 NSTP2 Worksheet 2Document4 pagesUnit-3 NSTP2 Worksheet 2Eki OmallaoNo ratings yet

- Weighted and FIFO Costing - Practice ProblemsDocument9 pagesWeighted and FIFO Costing - Practice ProblemsEki OmallaoNo ratings yet

- FAR 2922 Investments in Equity Instruments PDFDocument5 pagesFAR 2922 Investments in Equity Instruments PDFEki OmallaoNo ratings yet

- These Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoDocument7 pagesThese Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoEki OmallaoNo ratings yet

- Topic 18-22 - Investments and Basic Derivatives (Compiled)Document37 pagesTopic 18-22 - Investments and Basic Derivatives (Compiled)Eki OmallaoNo ratings yet

- Chapter 7Document10 pagesChapter 7Eki OmallaoNo ratings yet

- Assessing Four SkillsDocument19 pagesAssessing Four SkillsEki OmallaoNo ratings yet

- Call FlowDocument1 pageCall FlowEki OmallaoNo ratings yet

- Ae12 Course File Econ DevDocument49 pagesAe12 Course File Econ DevEki OmallaoNo ratings yet

- Categories of Historical SourcesDocument8 pagesCategories of Historical SourcesEki OmallaoNo ratings yet

- Freer On Corporations BarbriDocument38 pagesFreer On Corporations BarbriJEL100% (1)

- Rule 111 JM Dominguez V Liclican DIGESTDocument1 pageRule 111 JM Dominguez V Liclican DIGESTStephen Celoso EscartinNo ratings yet

- PriceList - Realtech The Indiana - 99acresDocument3 pagesPriceList - Realtech The Indiana - 99acresSayantanSamaddar100% (1)

- Isaca Crisc SampleDocument50 pagesIsaca Crisc SampleKirthika BojarajanNo ratings yet

- Risk Surcharge: AWB No: H63537762 Owner CarrierDocument1 pageRisk Surcharge: AWB No: H63537762 Owner CarrierAnandNo ratings yet

- Term Paper About Human TraffickingDocument7 pagesTerm Paper About Human Traffickingeryhlxwgf100% (1)

- Agreement PreviewDocument7 pagesAgreement PreviewKumar utsavNo ratings yet

- English 9 Module 1 Activity 1Document1 pageEnglish 9 Module 1 Activity 1Rowell Digal BainNo ratings yet

- Sweden: WHAT CAN WE LEARN FROM SWEDEN'S DRUG POLICY EXPERIENCE?Document11 pagesSweden: WHAT CAN WE LEARN FROM SWEDEN'S DRUG POLICY EXPERIENCE?Paul Gallagher100% (1)

- Big Tech InjunctionDocument155 pagesBig Tech InjunctionWashington ExaminerNo ratings yet

- HDFC Life InsuranceDocument1 pageHDFC Life InsuranceSureshKarnanNo ratings yet

- Weimer, D.L. Vining, A.R. Policy Analysis Concepts & Practice in Policy Analysis Concepts (274-279)Document8 pagesWeimer, D.L. Vining, A.R. Policy Analysis Concepts & Practice in Policy Analysis Concepts (274-279)HM KNo ratings yet

- ANSWER Unlawful DetainerDocument5 pagesANSWER Unlawful DetainerJoshua100% (1)

- Electronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationDocument10 pagesElectronic Filing - Recorded 1915 MDA 2015 Form Report 3012 Reply Letter Request Filled Out Form For ORAL ARGUMENTS or JUST BRIEF February 13, 2016 With Proof of Service and VerificationStan J. CaterboneNo ratings yet

- 5 6334567979774116073 PDFDocument418 pages5 6334567979774116073 PDFSuman Sourav0% (1)

- RealEstate SingaporeDocument2 pagesRealEstate SingaporeKyaw Kyaw AungNo ratings yet

- Business Ethics: Dr. Rajinder KaurDocument24 pagesBusiness Ethics: Dr. Rajinder KaurDeepak SarojNo ratings yet

- Jeff Pippenger - Seven Times in LeviticusDocument16 pagesJeff Pippenger - Seven Times in LeviticusKelly K.R. RossNo ratings yet

- New Stockiest Appointment Check ListDocument18 pagesNew Stockiest Appointment Check ListRamana GNo ratings yet

- RA 8799 - Securities Regulation CodeDocument38 pagesRA 8799 - Securities Regulation CodeJacinto Jr Jamero100% (1)

- United Food Imports V Baroody ImportsDocument13 pagesUnited Food Imports V Baroody ImportspropertyintangibleNo ratings yet

- Registration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Document2 pagesRegistration by DEVON ENERGY CORP To Lobby For DEVON ENERGY CORP (200034716)Sunlight FoundationNo ratings yet

- The HR Management and Payroll CycleDocument97 pagesThe HR Management and Payroll CycleErwin David SianturiNo ratings yet

- Invoice: List of ContainersDocument1 pageInvoice: List of ContainersCHINo ratings yet

- Financial Ratio Template Free V61Document9 pagesFinancial Ratio Template Free V61Tommy RamadanNo ratings yet

- ICSE IX Maths LogarithmsDocument2 pagesICSE IX Maths LogarithmsBarnali DuttaNo ratings yet

- Confessions of An Economic Hit ManDocument4 pagesConfessions of An Economic Hit ManMuhammad AamirNo ratings yet