Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Whats NewDocument3 pagesWhats Newphani raja kumarNo ratings yet

- GST Audit Cannot Be Conducted After Winding Up of BusinessDocument3 pagesGST Audit Cannot Be Conducted After Winding Up of Businessphani raja kumarNo ratings yet

- Addition For Cash Deposited in Bank Out of Business Receipts - Draft SubmissionDocument69 pagesAddition For Cash Deposited in Bank Out of Business Receipts - Draft Submissionphani raja kumarNo ratings yet

- Test AttachmentDocument1 pageTest Attachmentphani raja kumarNo ratings yet

- Socieity Registration Required DetailsDocument1 pageSocieity Registration Required Detailsphani raja kumarNo ratings yet

- ACT Invoice FOR JANDocument2 pagesACT Invoice FOR JANphani raja kumarNo ratings yet

- Taxation of Income Earned From Selling SharesDocument5 pagesTaxation of Income Earned From Selling Sharesphani raja kumarNo ratings yet

- Leelavati Service Tax ReturnDocument6 pagesLeelavati Service Tax Returnphani raja kumarNo ratings yet

- Vat 112Document2 pagesVat 112phani raja kumarNo ratings yet

- Affidavit For Society Registration For Own House Amma PremashramDocument1 pageAffidavit For Society Registration For Own House Amma Premashramphani raja kumarNo ratings yet

- I Disabled HiberfilDocument3 pagesI Disabled Hiberfilphani raja kumarNo ratings yet

- Some Important Aspects of HUF Under Income Tax, 1961Document16 pagesSome Important Aspects of HUF Under Income Tax, 1961phani raja kumarNo ratings yet

- Income Tax Scrutiny NormsDocument6 pagesIncome Tax Scrutiny Normsphani raja kumarNo ratings yet

- Stampduty For Firm ReconstitutionDocument2 pagesStampduty For Firm Reconstitutionphani raja kumarNo ratings yet

- Tan Application Form Form-49b 1-3-19Document5 pagesTan Application Form Form-49b 1-3-19phani raja kumarNo ratings yet

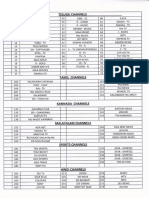

- Channels ListDocument2 pagesChannels Listphani raja kumarNo ratings yet

- 2 of 2008 8 % To 10 % Duty ChangeDocument3 pages2 of 2008 8 % To 10 % Duty Changephani raja kumarNo ratings yet

- Acception of Cforms After Issuing of Assessment Order Godrej Agrovet CaseDocument1 pageAcception of Cforms After Issuing of Assessment Order Godrej Agrovet Casephani raja kumarNo ratings yet

- Capital Gain Compensation Recd From Central GovernmentDocument45 pagesCapital Gain Compensation Recd From Central Governmentphani raja kumarNo ratings yet

- BALAJI SOFTTECK DIGITAL SIGNATURE APPLICATION TCS - Class 2 IndividualDocument2 pagesBALAJI SOFTTECK DIGITAL SIGNATURE APPLICATION TCS - Class 2 Individualphani raja kumarNo ratings yet

- Digital Signature Certificate Subscription FormDocument1 pageDigital Signature Certificate Subscription Formphani raja kumarNo ratings yet

- Faculty of Law Jamia Millia Islamia: Income From House PropertyDocument21 pagesFaculty of Law Jamia Millia Islamia: Income From House PropertyMohdSaqibNo ratings yet

- StatementsDocument2 pagesStatementsmahak.gupta1902No ratings yet

- Payroll TemplateDocument1 pagePayroll Templatejenny PrietoNo ratings yet

- Canara Credit Cards User Manual - For WebsiteDocument11 pagesCanara Credit Cards User Manual - For WebsiteSuperdudeGauravNo ratings yet

- TAX-501 (Excise Taxes - Part 1)Document4 pagesTAX-501 (Excise Taxes - Part 1)lyndon delfinNo ratings yet

- Optimizing Customs Revenue: Unveiling The Impact of Import Taxes On Taxable Goods in Ternate City, IndonesiaDocument13 pagesOptimizing Customs Revenue: Unveiling The Impact of Import Taxes On Taxable Goods in Ternate City, Indonesiaindex PubNo ratings yet

- Fixed Deposit Maintenance FormDocument1 pageFixed Deposit Maintenance FormSridhar Ramachandran SrinivasanNo ratings yet

- Laptop PO - QbithubDocument1 pageLaptop PO - QbithubsmithNo ratings yet

- Week 9 - Amalgamations and Wind UpsDocument15 pagesWeek 9 - Amalgamations and Wind UpsMike RaitsinNo ratings yet

- Presidential Order 5Document1 pagePresidential Order 5acaudit VJA.INo ratings yet

- Terms and Conditions of NPCI Platinum Rupay Debit CardDocument24 pagesTerms and Conditions of NPCI Platinum Rupay Debit CardPrince MathewNo ratings yet

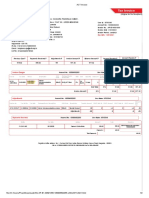

- Tax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanDocument1 pageTax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanAshihsNo ratings yet

- 23Document2 pages23Alberto Sarabia100% (2)

- Composition of Cash Petty CashDocument7 pagesComposition of Cash Petty CashRyou ShinodaNo ratings yet

- GST Export Invoice Format NewDocument4 pagesGST Export Invoice Format Newmanas022No ratings yet

- ZFB01N TemplateDocument18 pagesZFB01N TemplatePrateek MohapatraNo ratings yet

- CA Final IDT MCQ by Tharun Raj Sir-May 2019Document115 pagesCA Final IDT MCQ by Tharun Raj Sir-May 2019Karthik Srinivas Narapalle0% (1)

- CRN7757714844Document3 pagesCRN7757714844Sabyasachi BangalNo ratings yet

- Lotto For Deaf PeopleDocument11 pagesLotto For Deaf PeoplePREMIUM LANo ratings yet

- E-Auctions - MSTC Limited-BelghoriaDocument8 pagesE-Auctions - MSTC Limited-BelghoriamannakauNo ratings yet

- Train Law ConsDocument2 pagesTrain Law ConsgabbieseguiranNo ratings yet

- ITP No 979 English Version1Document93 pagesITP No 979 English Version1elias worku100% (3)

- Business and Other Local TaxesDocument73 pagesBusiness and Other Local Taxesflordeliza de jesusNo ratings yet

- Revenue Memorandum Circular 36-2021 v2Document32 pagesRevenue Memorandum Circular 36-2021 v2lizzyNo ratings yet

- BIR Citizens Charter-2017Document89 pagesBIR Citizens Charter-2017Iacel Joy SeseNo ratings yet

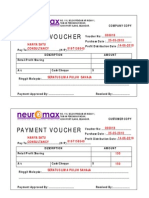

- Payment Voucher: 000018 25-05-2010 14-06-2010 Hanya Satu Consultancy 0167159540Document1 pagePayment Voucher: 000018 25-05-2010 14-06-2010 Hanya Satu Consultancy 0167159540Dalila ZakariaNo ratings yet

- List of All SWIFT-ISO MessagesDocument47 pagesList of All SWIFT-ISO Messagessanjayjogs50% (2)

- Computaion Pre FinalDocument4 pagesComputaion Pre FinalPaupauNo ratings yet

- Miss Naledi Saul 10106 Mareetsane Village Mahikeng 2745: Page 1 of 2Document2 pagesMiss Naledi Saul 10106 Mareetsane Village Mahikeng 2745: Page 1 of 2saulnaledi28No ratings yet

- Heichala Dream Enterprise (Ns0262486-H) : InvoiceDocument1 pageHeichala Dream Enterprise (Ns0262486-H) : InvoiceEmir NazrenNo ratings yet