Download as pdf or txt

You might also like

- First Round 2015 Q1 LP LetterDocument4 pagesFirst Round 2015 Q1 LP LetterFirst Round Capital88% (8)

- Urdg 758Document33 pagesUrdg 758rupeshsingh1986No ratings yet

- Orbis Equity Annual Reports 2011Document32 pagesOrbis Equity Annual Reports 2011noranycNo ratings yet

- UST WC Finance With AnswersDocument11 pagesUST WC Finance With AnswersPauline Kisha Castro100% (1)

- Conceptual QuestionsDocument43 pagesConceptual Questionsbinod gaire0% (1)

- Tilson - t2 Annual LetterDocument27 pagesTilson - t2 Annual Lettermwolcott4No ratings yet

- LTR To Investors Jan 11Document6 pagesLTR To Investors Jan 11the_knowledge_pileNo ratings yet

- Einhorn Q4 2015Document7 pagesEinhorn Q4 2015CanadianValueNo ratings yet

- Fig Gold Man 120611 Final2Document27 pagesFig Gold Man 120611 Final2aadricapitalNo ratings yet

- 2017 Q3 MC LetterDocument9 pages2017 Q3 MC LetterAnonymous Ht0MIJNo ratings yet

- When Diversification Failed: Hite AperDocument11 pagesWhen Diversification Failed: Hite Apersf_freeman5645No ratings yet

- Lakewood Capital - 2020 Q2 Letter PDFDocument10 pagesLakewood Capital - 2020 Q2 Letter PDFcaleb wattsNo ratings yet

- Letter To Our Co Investors 2Q20Document26 pagesLetter To Our Co Investors 2Q20Andy HuffNo ratings yet

- Failed DiversificationDocument11 pagesFailed DiversificationsjuhawkNo ratings yet

- Einhorn - Q1 '12 Letter To PartnersDocument7 pagesEinhorn - Q1 '12 Letter To PartnersAAOI2No ratings yet

- Orbe Brazil Fund - Dec2012Document7 pagesOrbe Brazil Fund - Dec2012José Enrique MorenoNo ratings yet

- Detailed Tables Are Provided in The Appendix at The EndDocument9 pagesDetailed Tables Are Provided in The Appendix at The Endanil1820No ratings yet

- Stocks Have Rallied and Will Now Return Less. Hip Hip Hooray! But Now What?Document5 pagesStocks Have Rallied and Will Now Return Less. Hip Hip Hooray! But Now What?saif_shakeelNo ratings yet

- Kase Fund Annual Letter-2013Document12 pagesKase Fund Annual Letter-2013CanadianValueNo ratings yet

- Arlington Value 2014 Annual Letter PDFDocument8 pagesArlington Value 2014 Annual Letter PDFChrisNo ratings yet

- Greenstone Distressed Debt Investing Letter DEC 2010Document10 pagesGreenstone Distressed Debt Investing Letter DEC 2010oo2011No ratings yet

- Gmo Quarterly Letter Q4 2018Document17 pagesGmo Quarterly Letter Q4 2018Stirling AdelhelmNo ratings yet

- December 31, 2000Document3 pagesDecember 31, 2000grrarrNo ratings yet

- KaseFundannualletter 2015Document20 pagesKaseFundannualletter 2015CanadianValueNo ratings yet

- Fef 2023 Semi Annual Letter WebDocument7 pagesFef 2023 Semi Annual Letter WebBen2pop170686No ratings yet

- June 2010Document4 pagesJune 2010FalconPrideNo ratings yet

- Crossroads Capital 2019 Annual FINALDocument31 pagesCrossroads Capital 2019 Annual FINALYog MehtaNo ratings yet

- Friedberg 3Q ReportDocument16 pagesFriedberg 3Q Reportrichardck61No ratings yet

- Information Bite 15mar8Document4 pagesInformation Bite 15mar8information.biteNo ratings yet

- Eta Investment Report: A Year For The History BooksDocument31 pagesEta Investment Report: A Year For The History BooksTerence MollNo ratings yet

- TomT Stock Market Model 2012-05-20Document20 pagesTomT Stock Market Model 2012-05-20Tom TiedemanNo ratings yet

- Frontaura - Quarterly - Letter - 2019Q1 - Discussion About StocksDocument16 pagesFrontaura - Quarterly - Letter - 2019Q1 - Discussion About StocksqazimusaddeqNo ratings yet

- Selector September 2007 Quarterly NewsletterDocument12 pagesSelector September 2007 Quarterly Newsletterapi-237451731No ratings yet

- The End of Buy and Hold ... and Hope Brian ReznyDocument16 pagesThe End of Buy and Hold ... and Hope Brian ReznyAlbert L. PeiaNo ratings yet

- Tilson Full YearDocument30 pagesTilson Full Yearcbailey2847465No ratings yet

- Coho Capital 2020 Q4 LetterDocument11 pagesCoho Capital 2020 Q4 LetterEast CoastNo ratings yet

- Maran Partners Fund Q2 2020Document6 pagesMaran Partners Fund Q2 2020Paul AsselinNo ratings yet

- MostFactsheetJuly2019 PDFDocument18 pagesMostFactsheetJuly2019 PDFakshayNo ratings yet

- FPA Crescent Qtrly Commentary 0911Document4 pagesFPA Crescent Qtrly Commentary 0911James HouNo ratings yet

- "It's Déjà Vu All Over Again.": Investment Guide Second Quarter 2011 LetterDocument8 pages"It's Déjà Vu All Over Again.": Investment Guide Second Quarter 2011 LetterVALUEWALK LLCNo ratings yet

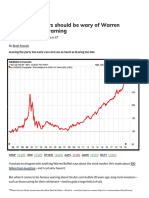

- Opinion:: Investors Should Be Wary of Warren Buffett's Crash WarningDocument5 pagesOpinion:: Investors Should Be Wary of Warren Buffett's Crash WarningNayeem RajaNo ratings yet

- Kase Quarterly Letter Q3 2013Document35 pagesKase Quarterly Letter Q3 2013CanadianValueNo ratings yet

- Hide and Seek: U.S. Economy UncertainDocument12 pagesHide and Seek: U.S. Economy UncertainCanadianValueNo ratings yet

- Arlington Value 2006 Annual Shareholder LetterDocument5 pagesArlington Value 2006 Annual Shareholder LetterSmitty WNo ratings yet

- Investment Commentar Y: Initial Thinking Another Update Investor CallDocument9 pagesInvestment Commentar Y: Initial Thinking Another Update Investor CallAnil GowdaNo ratings yet

- T2 Partners March LetterDocument5 pagesT2 Partners March LettermailimailiNo ratings yet

- Mason Hawkins 11q3letterDocument4 pagesMason Hawkins 11q3letterrodrigoescobarn142No ratings yet

- 1Q 2019 PresentationDocument8 pages1Q 2019 Presentationaugtour4977No ratings yet

- Kerr Is Dale Quarterly Letter 12-31-11Document3 pagesKerr Is Dale Quarterly Letter 12-31-11VALUEWALK LLCNo ratings yet

- February 2022 NewsletterDocument6 pagesFebruary 2022 NewsletterakkikediaNo ratings yet

- Wally Weitz Letter To ShareholdersDocument2 pagesWally Weitz Letter To ShareholdersAnonymous j5tXg7onNo ratings yet

- Q2 2021results For Cedar Creek Partners CorrectedDocument8 pagesQ2 2021results For Cedar Creek Partners Correctedl chanNo ratings yet

- Thackray Market Letter 2013 DecemberDocument11 pagesThackray Market Letter 2013 DecemberdpbasicNo ratings yet

- Managing Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Document6 pagesManaging Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Matt EbrahimiNo ratings yet

- First Quarter 2009 - NewsletterDocument6 pagesFirst Quarter 2009 - NewsletterEricNo ratings yet

- 5 Profit Makers in 2011Document18 pages5 Profit Makers in 2011Điểm ĐỗNo ratings yet

- Weitz Funds 4 Q2008 LetterDocument5 pagesWeitz Funds 4 Q2008 LetterfwallstreetNo ratings yet

- Don't Be Too SmartDocument2 pagesDon't Be Too SmartSam PellettieriNo ratings yet

- How Would Have a Low-Cost Index Fund Approach Worked During the Great Depression?From EverandHow Would Have a Low-Cost Index Fund Approach Worked During the Great Depression?No ratings yet

- The Smooth Ride Portfolio: How Great Investors Protect and Grow Their Wealth...and You Can TooFrom EverandThe Smooth Ride Portfolio: How Great Investors Protect and Grow Their Wealth...and You Can TooNo ratings yet

- The Motley Fool Million Dollar Portfolio: How to Build and Grow a Panic-Proof Investment PortfolioFrom EverandThe Motley Fool Million Dollar Portfolio: How to Build and Grow a Panic-Proof Investment PortfolioRating: 5 out of 5 stars5/5 (1)

- Investing for Beginners: Steps to Financial FreedomFrom EverandInvesting for Beginners: Steps to Financial FreedomRating: 4.5 out of 5 stars4.5/5 (3)

- Questionaire-Internal Control-1Document7 pagesQuestionaire-Internal Control-1Mirai KuriyamaNo ratings yet

- Classification of Financial MarketsDocument12 pagesClassification of Financial Marketsvijaybhaskarreddymee67% (6)

- Automation, Manual & Computerised AccountingDocument16 pagesAutomation, Manual & Computerised AccountingAayush AnandNo ratings yet

- Client Agreement BZ enDocument20 pagesClient Agreement BZ enGustavo JaramilloNo ratings yet

- 0812 Daniel Camacho Capital Markets FinalDocument20 pages0812 Daniel Camacho Capital Markets FinalJonathan AguilarNo ratings yet

- Can A Debit Card From A Different Bank Be Used at Another BankDocument5 pagesCan A Debit Card From A Different Bank Be Used at Another BankHabtamu AssefaNo ratings yet

- Sri Matushri Pushpaben Vinubhai Valia College of CommerceDocument7 pagesSri Matushri Pushpaben Vinubhai Valia College of CommerceVijay MauryaNo ratings yet

- Advantages and Disadvantages of Financial Equity and Financial DeptDocument4 pagesAdvantages and Disadvantages of Financial Equity and Financial Deptprince agbekoNo ratings yet

- Case Studies Unit 9 & 10 0f Business StudiesDocument14 pagesCase Studies Unit 9 & 10 0f Business StudiesSuchi SinghNo ratings yet

- Cost Accounting Sheet (5) Part (2) Chapter (3) Costing and Control of Materials and LaborDocument11 pagesCost Accounting Sheet (5) Part (2) Chapter (3) Costing and Control of Materials and Labormagdy kamelNo ratings yet

- CRISIL Ratings Readymade Garments 010312Document2 pagesCRISIL Ratings Readymade Garments 010312KritiNo ratings yet

- Fabm - Q2 - Las-For LearnersDocument113 pagesFabm - Q2 - Las-For LearnersABM-AKRISTINE DELA CRUZNo ratings yet

- Percentage Speed Test: B-123-A MANGAL MARG, BAPU NAGAR JAIPUR (M) +919782519669Document4 pagesPercentage Speed Test: B-123-A MANGAL MARG, BAPU NAGAR JAIPUR (M) +919782519669piakapoorNo ratings yet

- Accounting Assignment 3Document2 pagesAccounting Assignment 3aira mikaela ruazolNo ratings yet

- Test Calling SheetDocument51 pagesTest Calling SheetAnonymous qWY12CYlmNo ratings yet

- CIBIL Decision MatrixDocument3 pagesCIBIL Decision MatrixsureshkayambuNo ratings yet

- Savings and Credit Co-Operative League of South Africa Limited (Saccol)Document16 pagesSavings and Credit Co-Operative League of South Africa Limited (Saccol)astig79No ratings yet

- Michael D Randolph, ResumeDocument2 pagesMichael D Randolph, ResumemdrandolphNo ratings yet

- Excel ExerciseDocument5 pagesExcel ExercisemasturaNo ratings yet

- Memorandum of AgreementDocument1 pageMemorandum of AgreementKristel Alyssa MarananNo ratings yet

- 0 1Document4 pages0 1Sayantan HalderNo ratings yet

- The Palgrave Handbook of Esg and Corporate Governance Paulo Camara Full ChapterDocument67 pagesThe Palgrave Handbook of Esg and Corporate Governance Paulo Camara Full Chapterjerry.watkins103100% (11)

- Khatabook-Customer-Transactions-09 12 2023-04 45 01 PMDocument26 pagesKhatabook-Customer-Transactions-09 12 2023-04 45 01 PMPawan NayakNo ratings yet

- Aa Future Sunshine HSBC10710463 1 9M 24 05 2023Document7 pagesAa Future Sunshine HSBC10710463 1 9M 24 05 2023xhxbxbxbbx79No ratings yet

- Final Exam (Add)Document3 pagesFinal Exam (Add)samuel debebeNo ratings yet

- TT MalayesiaDocument2 pagesTT MalayesiaEllerNo ratings yet

- Why Are Ratios UsefulDocument5 pagesWhy Are Ratios UsefulLosing SleepNo ratings yet