Ôn NHTMNC

Ôn NHTMNC

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Quiz On Cash and Cash Equivalents - Quiz 1 On Prelim Term PeriodDocument2 pagesQuiz On Cash and Cash Equivalents - Quiz 1 On Prelim Term PeriodMae Jessa67% (6)

- Tutorial 3 - Bad Debts and Provision For Doubtful Debt - Copy - 41137Document2 pagesTutorial 3 - Bad Debts and Provision For Doubtful Debt - Copy - 41137Sarah RanduNo ratings yet

- Reliability: Reliability /variables Sd1 Sd2 Sd3 /scale ('All Variables') All /model Alpha /summary TotalDocument4 pagesReliability: Reliability /variables Sd1 Sd2 Sd3 /scale ('All Variables') All /model Alpha /summary TotalVi TrươngNo ratings yet

- TB Bank loans-đã chuyển sang wordDocument8 pagesTB Bank loans-đã chuyển sang wordVi TrươngNo ratings yet

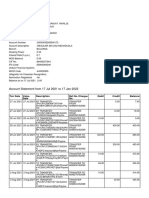

- Date: 28/05/2021 Current Price: 101,000 VND The Highest: 103,000 VND The Shortest: 100,800 VND Transaction Volume: 8,505,700Document6 pagesDate: 28/05/2021 Current Price: 101,000 VND The Highest: 103,000 VND The Shortest: 100,800 VND Transaction Volume: 8,505,700Vi TrươngNo ratings yet

- Answers To Final ExamsDocument42 pagesAnswers To Final ExamsVi TrươngNo ratings yet

- Tax Declaration ObligationsDocument2 pagesTax Declaration ObligationsVi TrươngNo ratings yet

- Assignment Financial ManaDocument2 pagesAssignment Financial ManaVi TrươngNo ratings yet

- Module 6 IRR and Payback PeriodDocument13 pagesModule 6 IRR and Payback PeriodRhonita Dea AndariniNo ratings yet

- iMS - CAPITAL MARKETSDocument4 pagesiMS - CAPITAL MARKETSJalbuena T JanuaryNo ratings yet

- Pridhvi Asset Reconstruction and Securitisation Company Ltd.Document8 pagesPridhvi Asset Reconstruction and Securitisation Company Ltd.neetu0411No ratings yet

- Cha 4 Schadul A Income From EmploymentDocument88 pagesCha 4 Schadul A Income From EmploymentLakachew GetasewNo ratings yet

- IIMC - Edelweiss EGIA JDDocument3 pagesIIMC - Edelweiss EGIA JDVaishnaviRaviNo ratings yet

- Fabm ReportingDocument5 pagesFabm ReportingJean Marie PatalinghogNo ratings yet

- Working Capital of Plastic IndustryDocument59 pagesWorking Capital of Plastic Industryctansari50% (2)

- Compliance Portal - Non-Filing of Return - User Guide - V1.0Document94 pagesCompliance Portal - Non-Filing of Return - User Guide - V1.0Swathi PriyaNo ratings yet

- Chapter 9 - Finance Lease-LESSEEDocument2 pagesChapter 9 - Finance Lease-LESSEElooter198No ratings yet

- Ch07 Tool KitDocument21 pagesCh07 Tool KitQazi Mohammed AhmedNo ratings yet

- Get Your Payments Electronically: Socialsecurity - GovDocument8 pagesGet Your Payments Electronically: Socialsecurity - GovJacqueline VillaltaNo ratings yet

- Mock Test Papers On Financial Awareness Including Economic and Monetary ScenarioDocument4 pagesMock Test Papers On Financial Awareness Including Economic and Monetary ScenarioSuvasish DasguptaNo ratings yet

- Dwnload Full Macroeconomics Canadian 6th Edition Abel Test Bank PDFDocument35 pagesDwnload Full Macroeconomics Canadian 6th Edition Abel Test Bank PDFmichelettigeorgianna100% (12)

- Demurrer To EvidenceDocument27 pagesDemurrer To EvidenceShelamarie M. Beltran100% (1)

- Hari 2Document3 pagesHari 2preeti gahlotNo ratings yet

- ACC 106 - Table of Specifications Final Exam CoverageDocument1 pageACC 106 - Table of Specifications Final Exam CoverageEunice Lyafe PanilagNo ratings yet

- Research Paper On FCIDocument12 pagesResearch Paper On FCIAnkit RastogiNo ratings yet

- Indian Financial SystemDocument27 pagesIndian Financial SystemDurga Prasad DashNo ratings yet

- Money The Nature and Function of MoneyDocument9 pagesMoney The Nature and Function of MoneySenelwa AnayaNo ratings yet

- Business Blue Print - ProjectDocument228 pagesBusiness Blue Print - ProjectThakkarSameerNo ratings yet

- Fairlight Alpha Fund Partnership Q2 2022 LetterDocument6 pagesFairlight Alpha Fund Partnership Q2 2022 LetterChristopher CardonaNo ratings yet

- Banking Crisis ProjectDocument9 pagesBanking Crisis Projectpanda catNo ratings yet

- RBL Free AccountDocument3 pagesRBL Free AccountDineshKumarPandaNo ratings yet

- Consolidated Income Statements Actuals Estimates Period Ending December 31 2010A 2011A 2012A 2013 Current Case - Case A (Street) CaseDocument30 pagesConsolidated Income Statements Actuals Estimates Period Ending December 31 2010A 2011A 2012A 2013 Current Case - Case A (Street) Casemarcmyomyint1663No ratings yet

- FIIs in India.........Document12 pagesFIIs in India.........JogenderNo ratings yet

- Advance Accounting 2 Home Office and BranchesDocument3 pagesAdvance Accounting 2 Home Office and BranchesCasper John Nanas MuñozNo ratings yet

- Ashish Nikalje StatementDocument15 pagesAshish Nikalje StatementRajesh PatilNo ratings yet

- Money Laundering Regulation and Risk Based Decision-MakingDocument6 pagesMoney Laundering Regulation and Risk Based Decision-MakingAmeer ShafiqNo ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Quiz On Cash and Cash Equivalents - Quiz 1 On Prelim Term PeriodDocument2 pagesQuiz On Cash and Cash Equivalents - Quiz 1 On Prelim Term PeriodMae Jessa67% (6)

- Tutorial 3 - Bad Debts and Provision For Doubtful Debt - Copy - 41137Document2 pagesTutorial 3 - Bad Debts and Provision For Doubtful Debt - Copy - 41137Sarah RanduNo ratings yet

- Reliability: Reliability /variables Sd1 Sd2 Sd3 /scale ('All Variables') All /model Alpha /summary TotalDocument4 pagesReliability: Reliability /variables Sd1 Sd2 Sd3 /scale ('All Variables') All /model Alpha /summary TotalVi TrươngNo ratings yet

- TB Bank loans-đã chuyển sang wordDocument8 pagesTB Bank loans-đã chuyển sang wordVi TrươngNo ratings yet

- Date: 28/05/2021 Current Price: 101,000 VND The Highest: 103,000 VND The Shortest: 100,800 VND Transaction Volume: 8,505,700Document6 pagesDate: 28/05/2021 Current Price: 101,000 VND The Highest: 103,000 VND The Shortest: 100,800 VND Transaction Volume: 8,505,700Vi TrươngNo ratings yet

- Answers To Final ExamsDocument42 pagesAnswers To Final ExamsVi TrươngNo ratings yet

- Tax Declaration ObligationsDocument2 pagesTax Declaration ObligationsVi TrươngNo ratings yet

- Assignment Financial ManaDocument2 pagesAssignment Financial ManaVi TrươngNo ratings yet

- Module 6 IRR and Payback PeriodDocument13 pagesModule 6 IRR and Payback PeriodRhonita Dea AndariniNo ratings yet

- iMS - CAPITAL MARKETSDocument4 pagesiMS - CAPITAL MARKETSJalbuena T JanuaryNo ratings yet

- Pridhvi Asset Reconstruction and Securitisation Company Ltd.Document8 pagesPridhvi Asset Reconstruction and Securitisation Company Ltd.neetu0411No ratings yet

- Cha 4 Schadul A Income From EmploymentDocument88 pagesCha 4 Schadul A Income From EmploymentLakachew GetasewNo ratings yet

- IIMC - Edelweiss EGIA JDDocument3 pagesIIMC - Edelweiss EGIA JDVaishnaviRaviNo ratings yet

- Fabm ReportingDocument5 pagesFabm ReportingJean Marie PatalinghogNo ratings yet

- Working Capital of Plastic IndustryDocument59 pagesWorking Capital of Plastic Industryctansari50% (2)

- Compliance Portal - Non-Filing of Return - User Guide - V1.0Document94 pagesCompliance Portal - Non-Filing of Return - User Guide - V1.0Swathi PriyaNo ratings yet

- Chapter 9 - Finance Lease-LESSEEDocument2 pagesChapter 9 - Finance Lease-LESSEElooter198No ratings yet

- Ch07 Tool KitDocument21 pagesCh07 Tool KitQazi Mohammed AhmedNo ratings yet

- Get Your Payments Electronically: Socialsecurity - GovDocument8 pagesGet Your Payments Electronically: Socialsecurity - GovJacqueline VillaltaNo ratings yet

- Mock Test Papers On Financial Awareness Including Economic and Monetary ScenarioDocument4 pagesMock Test Papers On Financial Awareness Including Economic and Monetary ScenarioSuvasish DasguptaNo ratings yet

- Dwnload Full Macroeconomics Canadian 6th Edition Abel Test Bank PDFDocument35 pagesDwnload Full Macroeconomics Canadian 6th Edition Abel Test Bank PDFmichelettigeorgianna100% (12)

- Demurrer To EvidenceDocument27 pagesDemurrer To EvidenceShelamarie M. Beltran100% (1)

- Hari 2Document3 pagesHari 2preeti gahlotNo ratings yet

- ACC 106 - Table of Specifications Final Exam CoverageDocument1 pageACC 106 - Table of Specifications Final Exam CoverageEunice Lyafe PanilagNo ratings yet

- Research Paper On FCIDocument12 pagesResearch Paper On FCIAnkit RastogiNo ratings yet

- Indian Financial SystemDocument27 pagesIndian Financial SystemDurga Prasad DashNo ratings yet

- Money The Nature and Function of MoneyDocument9 pagesMoney The Nature and Function of MoneySenelwa AnayaNo ratings yet

- Business Blue Print - ProjectDocument228 pagesBusiness Blue Print - ProjectThakkarSameerNo ratings yet

- Fairlight Alpha Fund Partnership Q2 2022 LetterDocument6 pagesFairlight Alpha Fund Partnership Q2 2022 LetterChristopher CardonaNo ratings yet

- Banking Crisis ProjectDocument9 pagesBanking Crisis Projectpanda catNo ratings yet

- RBL Free AccountDocument3 pagesRBL Free AccountDineshKumarPandaNo ratings yet

- Consolidated Income Statements Actuals Estimates Period Ending December 31 2010A 2011A 2012A 2013 Current Case - Case A (Street) CaseDocument30 pagesConsolidated Income Statements Actuals Estimates Period Ending December 31 2010A 2011A 2012A 2013 Current Case - Case A (Street) Casemarcmyomyint1663No ratings yet

- FIIs in India.........Document12 pagesFIIs in India.........JogenderNo ratings yet

- Advance Accounting 2 Home Office and BranchesDocument3 pagesAdvance Accounting 2 Home Office and BranchesCasper John Nanas MuñozNo ratings yet

- Ashish Nikalje StatementDocument15 pagesAshish Nikalje StatementRajesh PatilNo ratings yet

- Money Laundering Regulation and Risk Based Decision-MakingDocument6 pagesMoney Laundering Regulation and Risk Based Decision-MakingAmeer ShafiqNo ratings yet