Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Comparing Credit Card Offers Fcs 340Document2 pagesComparing Credit Card Offers Fcs 340api-350693115No ratings yet

- Market Corrections, Panics, and COVID-19Document5 pagesMarket Corrections, Panics, and COVID-19Rodrigo GRNo ratings yet

- The Salt Tolerance of The Freshwater Snail Melanoides Tuberculata (Mollusca, Gastropoda), A Bioinvader GastropodDocument11 pagesThe Salt Tolerance of The Freshwater Snail Melanoides Tuberculata (Mollusca, Gastropoda), A Bioinvader GastropodRodrigo GRNo ratings yet

- Animals in A Bacterial World. McFall-Ngai, Et Al. 2013Document8 pagesAnimals in A Bacterial World. McFall-Ngai, Et Al. 2013Rodrigo GRNo ratings yet

- Ascent of The Mammals: Scientific American May 2016Document9 pagesAscent of The Mammals: Scientific American May 2016Rodrigo GRNo ratings yet

- Insectivorous Bats As Biomonitor of Metal Exposure in The Megalopolis of Mexico and Rural Environments in Central MexicoDocument10 pagesInsectivorous Bats As Biomonitor of Metal Exposure in The Megalopolis of Mexico and Rural Environments in Central MexicoRodrigo GRNo ratings yet

- From The Origin of Species To The Origin of Bacterial FlagellaDocument8 pagesFrom The Origin of Species To The Origin of Bacterial FlagellaRodrigo GRNo ratings yet

- Modeling Distribution and Population Vibility of Ateles HybridusDocument1 pageModeling Distribution and Population Vibility of Ateles HybridusRodrigo GRNo ratings yet

- Hostplants and ClassificationsDocument109 pagesHostplants and ClassificationsRodrigo GRNo ratings yet

- Predation by Rainbow Trout Oncorhynchus Mykiss On A Western Australian Icon Marron Cherax CainiiDocument9 pagesPredation by Rainbow Trout Oncorhynchus Mykiss On A Western Australian Icon Marron Cherax CainiiRodrigo GRNo ratings yet

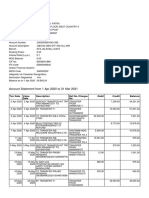

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancesayanNo ratings yet

- COST To COMPANY (CTC) For MR Hitesh Tomar Email: Tomar - Soft@Document1 pageCOST To COMPANY (CTC) For MR Hitesh Tomar Email: Tomar - Soft@tomar_softNo ratings yet

- Hc-Si22110190 Db-JeelytonDocument1 pageHc-Si22110190 Db-JeelytonHanh Nguyen KhacNo ratings yet

- Terengo AsmareDocument43 pagesTerengo Asmaretadesse beyeneNo ratings yet

- Huhu 105Document1 pageHuhu 105Mikko Gabrielle LangbidNo ratings yet

- Commerce General 1st SemesterDocument4 pagesCommerce General 1st SemestertNo ratings yet

- Krishna HSBC 20-21 StatementDocument175 pagesKrishna HSBC 20-21 StatementSumit VermaNo ratings yet

- Crypto Yield Farm Watcher DeFi Dashboard Apps OngcgstDocument4 pagesCrypto Yield Farm Watcher DeFi Dashboard Apps Ongcgstcablechive7100% (1)

- Lecture Notes Employee Benefits: Page 1 of 16Document16 pagesLecture Notes Employee Benefits: Page 1 of 16fastslowerNo ratings yet

- Ceylom Biscuit LimitedDocument24 pagesCeylom Biscuit LimitedLakshani fernandoNo ratings yet

- Rajiv Gandhi Equity Savings Scheme (80-CCG)Document9 pagesRajiv Gandhi Equity Savings Scheme (80-CCG)shaannivasNo ratings yet

- Ruis LK TW Iv 2022Document157 pagesRuis LK TW Iv 2022Ragil ArdianNo ratings yet

- Financial Management Live Project: A Study of Ratio Analysis of Axis BankDocument14 pagesFinancial Management Live Project: A Study of Ratio Analysis of Axis BankKreator's BlogNo ratings yet

- 3-PDIC-LAW' With YouDocument15 pages3-PDIC-LAW' With YoubeachyliarahNo ratings yet

- Paper6 Syl22 Dec23 Set1Document7 pagesPaper6 Syl22 Dec23 Set1koteshdarshanala82No ratings yet

- NorQuant Multi-Asset Fund White Paper 2023Document24 pagesNorQuant Multi-Asset Fund White Paper 2023oscar.haukvikNo ratings yet

- Financial Statements: College of Business Management and AccountancyDocument6 pagesFinancial Statements: College of Business Management and AccountancyJamie Rose AragonesNo ratings yet

- Sean Darby - JefferiesDocument18 pagesSean Darby - JefferiesKurnia NindyoNo ratings yet

- Topic 1 - Overview of Financial SystemsDocument23 pagesTopic 1 - Overview of Financial SystemsĐinh PhươngNo ratings yet

- 5010 XXXXXX 3202Document4 pages5010 XXXXXX 3202SHIVALAYA CONSTRUCTIONNo ratings yet

- Daibb - Mfi: Default Risk PremiumDocument14 pagesDaibb - Mfi: Default Risk Premiumanon_904021637No ratings yet

- Islamic Treasury Risk Management ProductsDocument4 pagesIslamic Treasury Risk Management ProductsjjangguNo ratings yet

- Chapter 10. Preparation Review of Night Audit 1Document36 pagesChapter 10. Preparation Review of Night Audit 1Cảnh DươngNo ratings yet

- Sss Salary Loan QuizDocument4 pagesSss Salary Loan QuizMeireen AnnNo ratings yet

- Unit 3 Risk Management Part 3Document8 pagesUnit 3 Risk Management Part 3Lylegwyneth SuperticiosoNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument14 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSanthosh Naik BhukyaNo ratings yet

- Acct Statement - XX3852 - 11012024Document5 pagesAcct Statement - XX3852 - 11012024Praveen SainiNo ratings yet

- 2.trial Balance-Hans Lee-9-6-2021Document5 pages2.trial Balance-Hans Lee-9-6-2021Dhairya AilaniNo ratings yet

- Gerrard Construction Co Is An Excavation Contractor The Following SummarizedDocument3 pagesGerrard Construction Co Is An Excavation Contractor The Following SummarizedCharlotteNo ratings yet